Print

PrintMarc S. Gerber and Richard J. Grossman are partners in the Mergers & Acquisitions practice at Skadden, Arps, Slate, Meagher & Flom LLP. This post is based on a Skadden alert.

Although the 2015 annual meeting season is still winding down, there is no doubt that proxy access has gained considerable momentum and will remain a front-and-center corporate governance issue for the foreseeable future. For the boards of directors of the many companies who were bystanders on this issue for the 2015 proxy season, the question will be whether to act now or wait and watch for further developments. In any event, as proxy access is likely to be a topic of discussion during companies’ “off season” shareholder engagement efforts, companies and their boards should understand how the proxy access landscape has evolved.

The Lead-Up to 2015

In important ways, the groundwork for the 2015 proxy access campaign was carefully laid in the 2012-14 proxy seasons. Targets of proxy access shareholder proposals modeled on the vacated SEC proxy access rule—granting holders of 3 percent of a company’s shares for three years access to the company’s proxy statement for nominees for up to 25 percent of the board—were carefully selected, and a coalition of institutional investors came together to provide majority support for most of these proposals. As a result, a small number of large companies—including Hewlett-Packard, Western Union, CenturyLink and Verizon Communications—walked through the proxy access door, making it only a matter of time before other companies—willingly or unwillingly—would have to follow.

In November 2014, the Office of the New York City Comptroller, in its capacity as trustee of various pension funds, launched the “Boardroom Accountability Project” by submitting proxy access proposals to 75 companies. The recipients were selected on the basis of investor concerns over excessive CEO compensation, a lack of board diversity or a perceived failure to address climate change. Combined with proposals from other institutional investors, as well as from individual investors who conformed their proxy access proposals to the “3-3-25” model favored by institutional investors, over 100 proxy access proposals were submitted for 2015 annual meetings.

At the same time, Whole Foods Market attempted to exclude a 3-3-25 proxy access shareholder proposal by submitting its own proxy access proposal to a shareholder vote—albeit with much more restrictive terms, 9 percent ownership for five years and limited to the nomination of one director. Whole Foods’ approach was entirely consistent with the SEC staff’s no-action letters on conflicting proposals (not relating to proxy access), and its no-action request was granted on December 1, 2014. Whole Foods’ success was short-lived when, in response to investor outcry, SEC Chair Mary Jo White directed the staff to review its application of the relevant rule, and the Whole Foods no-action letter was withdrawn. Nevertheless, the episode galvanized many institutional investors to vocally support 3-3-25 proxy access over alternative formulations and to warn companies of repercussions in director elections if companies attempted to pre-empt shareholder votes on 3-3-25 proxy access.

These events were followed in short order by statements from BlackRock supportive of 3-3-25 proxy access and by Vanguard, supportive of proxy access but expressing a preference for proxy access terms of 5 percent share ownership for three years and 20 percent of the board. In February, TIAA-CREF sent letters to many of the companies in which it had investments, supporting 3-3-25 proxy access and asking them to take voluntary action in 2015. CalPERS, CalSTRS, ISS and others also expressed support for 3-3-25 proxy access.

Company Responses and 2015 Voting Results

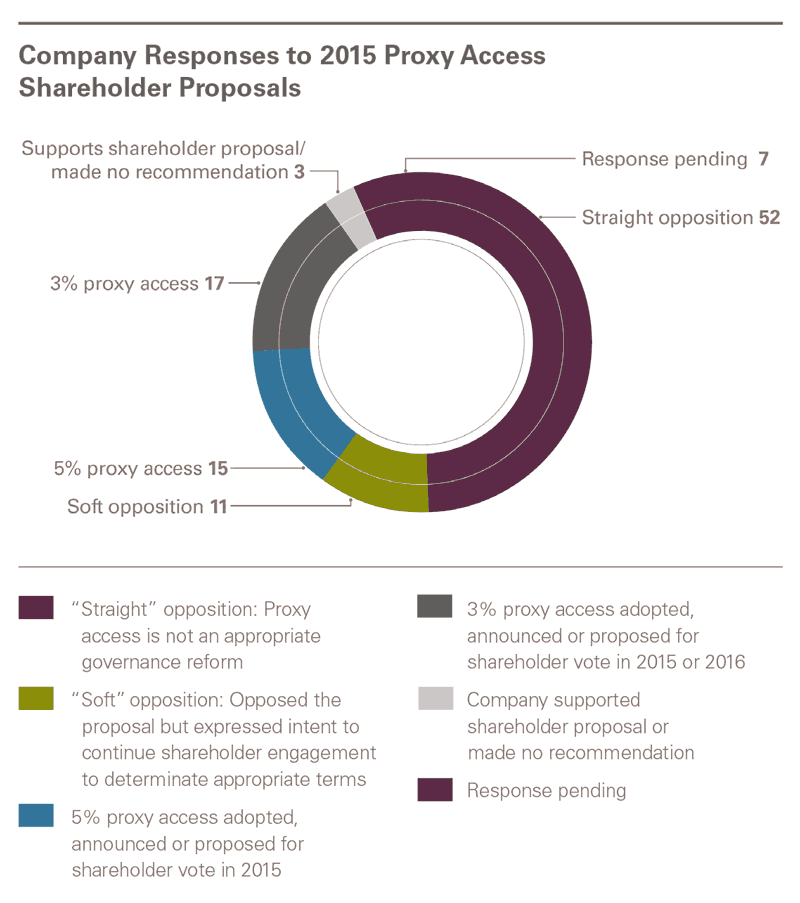

As shown in Figure 1, company responses have varied. Approximately half of the companies simply opposed the shareholder proposal as usurping the power of the nominating and governance committee and presenting an inappropriate or unnecessary governance reform. On the other end of the spectrum, approximately 15 percent of the companies either adopted 3 percent proxy access, announced an intention to do so or agreed with the proponent to submit a company 3 percent proxy access proposal for shareholder approval at the 2015 or 2016 annual meeting.

Whether influenced by Vanguard’s announced preference for 5 percent proxy access or by their own shareholder engagement efforts, another 15 percent of companies took the approach of adopting a 5 percent proxy access bylaw, announcing an intention to do so or submitting to a shareholder vote a company proposal for 5 percent proxy access—in competition with the shareholder proposal for 3 percent access. Finally, about 10 percent of companies opposed the shareholder proposal but, to varying degrees, expressed a willingness to continue to engage with shareholders to determine appropriate proxy access terms.

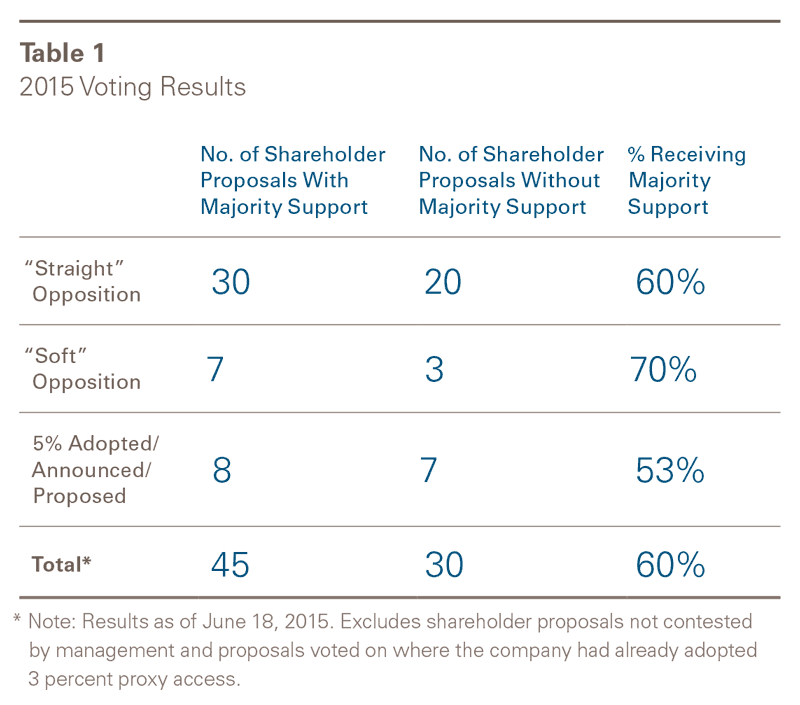

The voting results (Table 1) show that 3 percent proxy access has enjoyed significant but not universal support in the 2015 proxy season. Overall, to date, the shareholder proposal has achieved majority support at 60 percent of the companies where it was opposed. In some cases, the shareholder proposal failed to achieve majority support in the face of “straight” or “soft” opposition. However, the most likely path to defeating 3 percent proxy access was by adopting or proposing 5 percent proxy access, with almost half of those shareholder proposals failing to achieve majority support. Nevertheless, there is no guaranteed way to defeat the proposal and, absent a controlling or significant shareholder, almost all of the shareholder proposals failing to achieve majority support still had meaningful support at 40 percent or higher.

When the dust settles, more than 60 companies will have either adopted or announced 3 percent proxy access, will have agreed to submit a company 3 percent access proposal to a shareholder vote, or will have had a 3 percent shareholder proposal receive majority support. Where a 3 percent proposal received majority support, boards will face pressure to fully implement the majority-supported proposal, especially in light of ISS and investor policies to recommend or vote against directors if a majority-supported proposal is not implemented. Monsanto, which was the first proxy access vote of 2015 and where the proposal received majority support, recently announced its adoption of a 3-3-20 proxy access bylaw. A handful of other companies will have 5 percent proxy access (having defeated the 3 percent shareholder proposal) or will have already expressed some willingness to adopt access at a level of ownership still to be determined. Some companies will have defeated the proxy access proposal, but with significant support at many of those companies, such that the proposal is likely to be submitted again.

Going Forward

As the proxy season concludes, many companies will begin to transition to a period of “off season” shareholder engagement, a review of 2015 developments and consideration of corporate governance enhancements to implement in advance of the 2016 proxy season. For most companies, proxy access should be on the agenda for discussion.

Companies and boards of directors will face the question of whether to act in advance of possibly receiving a proxy access shareholder proposal or wait as long as possible and act only once the company receives a shareholder proposal or after shareholders vote on one. As the voting results show, majority support for 3 percent proxy access is likely but is not a foregone conclusion. Some companies may be tempted to oppose the shareholder proposal. Of course, any determination requires an informed analysis based on a company’s shareholders and their voting patterns and preferences, as well as a company’s particular facts and circumstances. There is no single right answer.

At the margins, proxy access may increase a company’s vulnerability to an election contest. But in the current age of shareholder activism, the marginal risk may be negligible. Proxy access election contests are not predicted to become commonplace and are not expected to be used by “true” shareholder activists. Also, the circumstances that would motivate an access nomination also might trigger an activist investor to nominate (not using proxy access) a short slate of directors.

Importantly, companies may be in a unique window of time where they retain some flexibility when considering proxy access terms beyond the 3-3-25 or 3-3-20 headline terms. For example, precedent varies on the number of shareholders permitted to come together to form a group to satisfy the ownership requirements. In addition, there are various formulations to account for “creeping control”—limits on the use of proxy access in successive years to prevent a majority of the board consisting of members nominated through proxy access. Another important question is whether and when to suspend proxy access in the event nonaccess nominations are made by shareholders. Adopting a proxy access bylaw sooner may permit companies to adopt a bylaw with a number of favorable provisions and, at the same time, significantly reduce the likelihood of receiving a shareholder proposal in the first place.

Another factor to consider is that shareholder proposals, as well as shareholder views, sometimes evolve. Today’s proxy access proposals focus on the 3-3-25 headline requirements. Will the next generation of proposals become more prescriptive and, if so, will that impact the level of shareholder support? If a more prescriptive proposal is received, there is no guarantee that adopting the headline provisions but including other terms that vary from those proposed will induce a proponent to withdraw the proposal or satisfy the SEC staff that a proposal has been substantially implemented and should be excluded. Similarly, shareholders’ views on proxy access are not uniform at the moment, and it is quite possible that shifting views could result in proxy access proposals receiving even greater support in future years.

Both companies and proponents will be assessing the results of the 2015 proxy season and determining their approaches to proxy access for the next round of shareholder proposals. Depending on one’s assessment, including the company’s vulnerability to receiving a proxy access shareholder proposal in the near term, there may be advantages for companies to move quickly.