Print

PrintJames Woolery is Co-Head of North American Mergers & Acquisitions at JPMorgan. This post is based on a JPMorgan report.

1. The Trillion Dollar Question

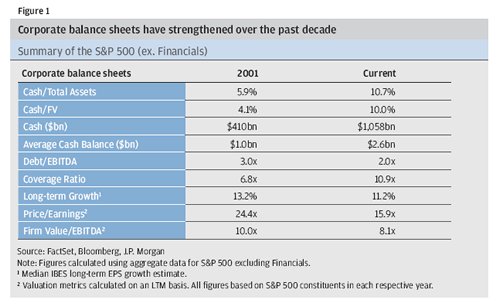

How would a trillion dollars affect the strategic M&A landscape? By now, virtually everybody who reads the financial press is aware that corporate cash balances are massive. In fact, the largest U.S. firms collectively have in excess of $1 trillion on their balance sheets. These firms have accumulated liquidity during the crisis by cutting back on shareholder distributions, capital expenditures, R&D and acquisitions. Since the crisis, these same firms have delevered by paying down debt and growing their earnings, further enhancing their liquidity positions. As one can see in Figure 1 below, cash balances surged from 5.9% to 10.7% of total assets and from $410bn to $1.1trn, while leverage declined from 3.0x to 2.0x.

As we discussed in several recent reports, the cash-rich environment is ripe for a significant increase in shareholder distributions. [1] Albeit resurging from crisis lows, existing dividend and buyback levels are not nearly enough to consume these firms’ cash flows, let alone put a dent into the record high cash balances. Moreover, distributions do not address the major issue facing large firms today: declining growth rates. The scarcity of organic growth opportunities is perhaps more concerning than any other current corporate issue. Over the last decade, large-cap long-term EPS growth rates declined from 13.2% to 11.2% currently.

Mergers and acquisitions occupy a prime spot in a firm’s growth arsenal. M&A generates top and bottom line growth through synergies and allows firms to complete or expand product portfolios and enter new geographies. It is not surprising, therefore, that pundits have been forecasting an M&A boom over the next few years. In this report, we show how M&A has indeed rebounded as expected. With cash rich balance sheets and cheap financing alternatives, one might fear that acquirers would tend to overpay for acquisitions, leading to poor investor acceptance. In refreshing contrast, we show that investors have been applauding a large number of recent transactions, leading to higher stock prices not only for the target, but also for the acquirer.

2. Anatomy of 2011 M&A

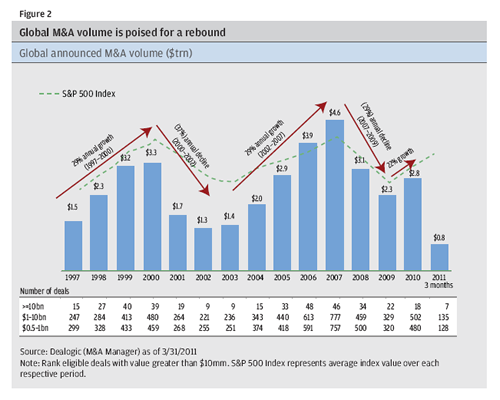

M&A is rebounding. As shown in Figure 2, global M&A volumes dropped by 50% from a peak of $4.6 trillion in 2007 to $2.3 trillion in 2009. During this period the confidence of senior executives suffered and firms focused on defense rather than offense. Lately, however, M&A volumes have started to rebound. After a more than 20% increase in 2010 to $2.8 trillion, transaction volume this year is expected to approach 2006 levels. Interestingly, we show that the S&P 500 stock performance is highly correlated with global M&A volumes.

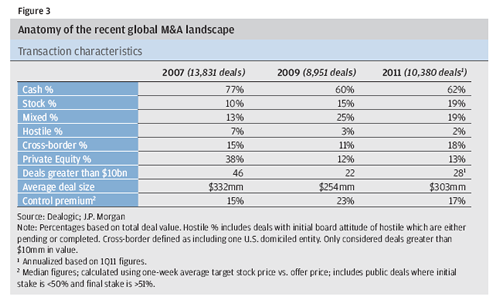

Pre-crisis versus post-crisis M&A. The biggest difference between pre- and post-crisis M&A is that private equity plays a minor role relative to strategic buyers in today’s market. Pre-crisis, almost 40% of M&A volume was related to private equity transactions. Today, private equity only constitutes 13% of transaction volume. Because most private equity transactions are executed with cash only, 77% of 2007 transactions were paid in cash, versus only 62% today. Another notable difference exists in the types of bids placed, as 7% of transactions were viewed as hostile in 2007 versus 2% today. Interestingly, other transaction characteristics remain quite similar. In 2007, 15% of transactions were cross-border relative to 18% today. Additionally, the typical 2011 deal size and premium are quite close to those seen in 2007. The latter result is remarkable as the S&P 500 is still around 15% below peak pre-crisis levels. That is, a $10bn transaction today represents a larger portion of the S&P 500 market capitalization than a similar sized transaction in 2007.

3. Well-Received Acquisitions in Today’s Environment

The reaction of investors to acquisition announcements has been the subject of decades of academic debate. The traditional view is that acquirer stock prices have declined on announcement. Yet, there are several characteristics that were typically associated with well-received transactions: (i) paid in cash only; (ii) buying an asset or unit of another firm; (iii) acquirer has a strong track-record; and (iv) focused transactions (like-for-like acquisitions). In contrast, investors tended to punish acquirers for: (i) transactions paid for in stock; (ii) hostile transactions; (iii) diversifying transactions; and (iv) highly competitive/multiple bidder situations.

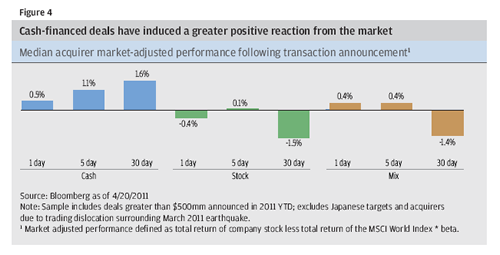

Are today’s transactions different? With all of this excess cash and excess flexibility on balance sheets, one might have feared that today’s acquirers would overpay and hence investors would respond quite negatively to acquisitions. As we show in Figure 4, acquirers’ returns were actually positive for cash acquisitions and flat to negative for stock acquisitions. It should be noted, however, that the negative market performance of large stock acquisitions is typically affected by short-selling pressure from risk arbitrage funds and it is not always indicative of the quality of the transaction.

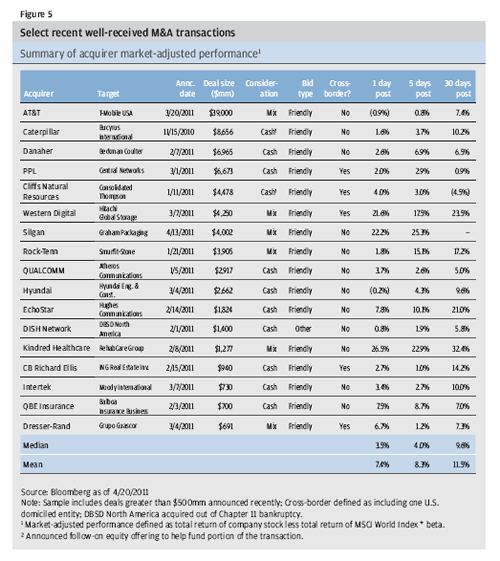

Figure 5 lays out a selected list of well-received transactions that have been announced since the beginning of the year. These transactions have generated an average excess return (over the risk-adjusted MSCI World return) of around 10% in the 30 days following the announcement. Most of the transactions in this list were financed with cash, focused (like-for-like acquisitions) and friendly.

4. Why Do Investors Appreciate M&A Even More Today?

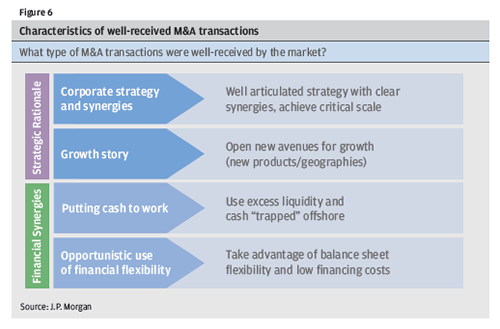

Well-articulated strategy with clear synergies. Investors applaud firms that pursue M&A opportunities that fit well with their stated strategic goals and existing assets (like-for-like acquisitions). Recent transactions that have highlighted significant cost and revenue synergies were well received by the market. Specifically, acquisitions that helped the pro-forma company in achieving critical scale and a stronger competitive position. Conversely, “python-swallows-an-elephant” transactions typically lead to a negative reaction as these acquisitions tend to introduce integration challenges.

Expanding the product or geographical reach. Various recent large transactions allowed the buyer to expand its geographical reach or to complement the existing product suite. In an environment where growth prospects are limited, such transactions provide hope for an acceleration of the acquirer’s future growth. Cross-border deals that provided the acquirer with growth opportunities in new geographies (such as emerging markets) were also supported by investors.

Putting cash to work. U.S. firms have accumulated a record amount of cash, but a sizable portion of this cash is “trapped” offshore (cannot be repatriated to the U.S. without incurring incremental taxes). By acquiring foreign targets, firms can effectively use their trapped cash to pursue growth opportunities abroad without repatriation tax consequences. This is especially valuable when the return of cash as an asset continues to be minimal in today’s low interest rate environment, leading to a significant negative-carry cost. Indeed, in several recent cross-border transactions, analysts commented favorably on foreign acquisitions by U.S. firms that utilize offshore cash.

Opportunistic use of financial flexibility and debt markets. With low Treasury rates and spreads that have tightened post crisis, the cost of debt has been at or close to historic lows. As large firms have delevered over the past decade, many currently have significant debt capacity within their ratings. Acquisitions where firms acquire incremental cash flow and gain scale and diversity are also viewed more favorably relative to some alternative uses of capital (e.g. share buybacks). Simultaneously, while equity investors appreciate the optionality this flexibility provides, they encourage firms that employ it in a disciplined manner.

Though we highlight reasons that foster a climate that is more receptive to M&A, transactions should be executed with discipline as it relates to the balance sheet and value. In particular, we continue to believe in the value of financial flexibility and recommend that firms do not jeopardize their balance sheet. Acquirers must also maintain pricing discipline. Even when an acquisition achieves the appropriate strategic rationale, senior decision makers need to ensure they do not overpay.

Endnotes

[1] See “Dividends: The 2011 guide to dividend policy trends and best practices,” J.P. Morgan, January 2011 and “Q1 2011 Distributions: Facts & Trends,” J.P. Morgan, April 2011.

(go back)