Print

PrintThe following post comes to us from Michael A. Moran, Pension Strategist at Goldman Sachs Asset Management. This post is based on a Goldman Sachs white paper by Mr. Moran.

Executive Summary

Recently issued rules by the Governmental Accounting Standards Board (GASB) will notably change the way state and local governments account for and report the results of their defined benefit pension plans. Some plans may see their reported funded percentages fall under the new requirements. A plan’s funded status will now be reflected on the balance sheet, increasing transparency as well as the focus on measures that plan sponsors are taking to address these shortfalls. Funded status and pension expense measures are also likely to be more volatile under the revised reporting standards.

While the new GASB rules change some important aspects of public DB plan reporting, they do not change others. In particular, they neither mandate use of a lower discount rate for calculating liabilities nor higher contribution requirements. These are changes to accounting and financial reporting, not economics. Nonetheless, they do represent a notable change to the calculation and reporting of various pension-related metrics.

Some public DB plan sponsors are already facing significant challenges, such as relatively low funded levels. In addition, given budgetary challenges, some state and local governments do not have the flexibility to increase contributions at this time. All of this is occurring in an environment where long-term expected returns across a wide variety of asset classes have been falling. The GASB changes may add yet another layer of stress, if not complexity, for some public plan sponsors.

This paper reviews the following aspects of the GASB changes:

- I. Recap of what will change and what will not change. Specifically, we highlight four key changes for plans and their sponsors to consider.

- II. Examination of the potential impact of the GASB changes. In particular, we look at similar revisions that were made on the corporate pension side several years ago and how those changes influenced plan sponsor behavior.

- III. Identification of steps that plan sponsors may likely take in response to the rule changes. We believe that the changes will likely not result in a change in behavior, but will likely accelerate trends that have already been in place for several years. These include efforts to reduce liabilities, increase contributions and adjust asset allocation to generate higher, but less volatile, returns. Some public plans have diversified plan assets in recent years by increasing allocations to alternative investments and exposure to growth markets. We expect this trend to continue.

I. Notable change to the way public DB pensions will be accounted for and reported

New rules issued this summer by the GASB will alter how state and local governments account for and report the results of their defined benefit pension plans. The new rules, issued as GASB 67 and 68, will begin to go into effect in 2014, although earlier application is allowed. While this may seem like a long time into the future, the complexity and importance of the changes mandate that plan sponsors begin to evaluate their implications sooner rather than later. [1] Below we highlight some of the key aspects of the new standards.

1. Funded status will be reported on the balance sheet

Historically, public DB plan sponsors have been required to recognize an amount known as the Net Pension Obligation, or NPO, on their balance sheets. The NPO represented the cumulative difference between actual contributions into the plan and what was known as the Annual Required Contribution, or ARC. Consequently, plans that fully paid their ARCs each year showed no liability on their balance sheets even if the plan was underfunded.

The new GASB requirements will place the actual funded status of the plan on the balance sheet. In other words, if a plan had $1 billion of assets and an actuarially determined gross pension obligation of $1.2 billion, a liability of $200 million would now be recognized on the balance sheet.

This is, in many ways, a philosophical change in how to view the responsibility of the plan sponsor with respect to pensions. Under the old GASB accounting, where the balance sheet reflected the NPO, the sponsor had a responsibility to pay contributions. To the extent contributions were less than the ARC, a liability was recorded to reflect that shortfall. Under the new GASB rules, the sponsor has a responsibility to pay benefits since any shortfall between assets and liabilities, the present value of future benefits, is recognized as the liability.

This change is similar to one made for corporate DB plan sponsors in 2006 after the Financial Accounting Standards Board (FASB) issued what was known at the time as FAS 158. Prior to 2006, pension deficits were largely off-balance sheet in the corporate universe. FAS 158 placed the funded status of the plan on the balance sheet of the sponsor. The GASB change in essence aligns the balance sheet reporting of corporate and public plan sponsors, although important differences in the calculation of funded status, discussed later, still exist.

Importantly, these changes do not mandate an increase in contribution requirements. GASB rules have no jurisdiction over mandating contributions into public DB plans. Despite its name, the ARC, as used under existing GASB standards, did not represent legally required contributions for a given year. [2] Partially as a consequence of the newly issued GASB rules, a number of groups are currently reviewing funding policies (see below).

A number of groups are reviewing funding policies and practices

The changes to public pension expense recognition under the new GASB rules means that plan sponsors will no longer be able to use the ARC as the de facto contribution requirement. While the ARC had been in effect the guiding measure for contributions, the GASB changes differentiate accounting from funding.

Due to these developments a number of actuarial groups have set out to develop standards or “best practices” in public DB funding. These groups include the Society of Actuaries, the California Actuarial Advisory Panel and the “Big 7,” a group of public sector organizations that includes the National Governors Association and the National League of Cities.

Much of the work of these groups has focused on basing pension funding on actuarially determined contributions, maintaining intergenerational equity and being disciplined about funding. Plan sponsors and other interested parties should consider monitoring the work of these groups, and others, as recommendations on policies and standards from these groups will likely be adopted by many plan sponsors.

2. Increased volatility of funded status and pension expense

Both funded status and pension expense will be calculated differently under the new GASB rules. Under the old calculations, the asset value used to calculate funded status could be smoothed, often around five years. This had the effect of minimizing the volatility of funded status, since market fluctuations were not immediately reflected in the asset value.

Under the new GASB rules, the actual fair market value of plan assets will be used for determining the funded status that will be placed on the balance sheet. This is consistent with the way corporate plans account for and report the asset side of their funded status equations. Use of the fair value of plan assets, as opposed to an actuarially determined smoothed value, will increase the volatility of reported funded status.

Reported pension expense will also be more volatile. Today pension expense is defined by the ARC, and includes two components: 1) normal cost, which is the present value of benefits earned by participants in the current period, and 2) amortization of the unfunded actuarial accrued liability (UAAL). The UAAL represents the unfunded amount of the liability and, therefore, a portion of it is amortized through the ARC calculation each year. This amortization can often be up to 30 years. Both of these components of the ARC are fairly stable year to year, resulting in a relatively consistent amount of pension expense each year.

Under the new GASB rules, most changes in the net pension liability will be included in pension expense immediately. Other aspects will be recognized over time, but under a much shorter amortization schedule than the 30 years that some plans use today. For example, differences between assumed and actual plan asset returns will be introduced into pension expense over a maximum period of five years. These changes, therefore, will result in pension expense being reported sooner and being more volatile on a year-to-year basis.

3. Potentially lower discount rates may increase pension obligations and lower funded ratios

Public DB plans have historically used their expected return on assets (EROA) assumption as the discount rate for their liabilities. The new GASB rules retain the use of the EROA as the discount rate to the extent that current and projected future assets are available to pay expected future benefit payments. If projected assets do not cover projected benefit payments, the excess expected benefit payments would be discounted at a tax-exempt, high-quality municipal bond rate.

Consequently, plans in this situation would be using a blended rate that reflected both the EROA and the municipal bond rate. Use of a blended rate would be lower than the standalone EROA. A lower discount rate would raise the present value of pension obligations, thereby lowering funded status.

Note that determining the appropriate discount rate to use is not based on current funded status. Rather, as described above, it involves a projection of whether current and expected future assets will cover future benefit payments. Therefore, it is possible that an underfunded plan would still be able to use the EROA as the discount rate. In general, though, the lower the funded status of a plan, the more likely that it will need to use a blended rate. In other words, plans with low funded ratios today are more at risk to see those ratios fall even further as a result of using a blended rate for discounting purposes.

Our conversations with actuaries suggest that in practice, many public plans will still be able to justify using the expected return assumption as the liability discount rate. Even in those situations where a blended rate will be used, the EROA will likely dominate the calculation, resulting in only a modest decline in the discount rate.

Nonetheless, we also note that the outcome is asymmetrical. Most plans will likely end up using either the same discount rate or one that is slightly lower—it will not result in the use of a higher discount rate. [3] Consequently, this could contribute to downward pressure on reported funded ratios for some plans.

4. Increased disclosure requirements

Plan sponsors will be required to disclose much more information about their plans, such as the sensitivity of pension calculations to a change in the discount rate and the derivation of the expected return assumption. This will increase the transparency around pension-related metrics and will likely invite new analysis and comparisons between plans and their sponsors.

II. Potential impact of the GASB changes: Financial reporting, not economics

The rule changes passed by the GASB alter neither the amount of benefits that must be paid to retirees nor contribution requirements for plan sponsors. From a purely theoretical perspective, the GASB changes do not change the economics of the plans and, consequently, should not change the way the plans are viewed by outsiders or the way they are managed by plan sponsors.

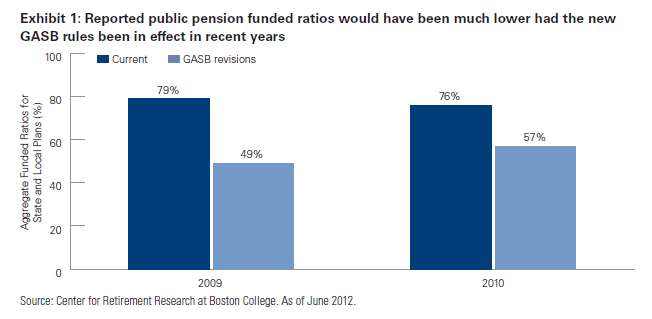

Nonetheless, the implementation of these rules will make some public plans look less well funded than they previously had. Exhibit 1 details the results of an analysis by the Center for Retirement Research at Boston College which demonstrated that the aggregate reported funded status of state and local plans would have been significantly lower in 2009 and 2010 had the new GASB rules been in effect at that time.

Much of the downward adjustment in funded ratios during 2009 and 2010 was due to losses from 2008. Such losses were still being smoothed into the actuarial value of plan assets, and would be fully reflected under the revised rules using market values. Such adjustments can reverse during periods of strong asset performance, whereby reported funded ratios under the revised rules would be higher than those under the previous rules with asset smoothing. The path of future plan asset values will ultimately determine whether plans report higher or lower funded ratios when the new rules go into effect. In some cases, the use of a lower discount rate to value liabilities also contributed to lower reported funded levels in the calculations summarized in Exhibit 1.

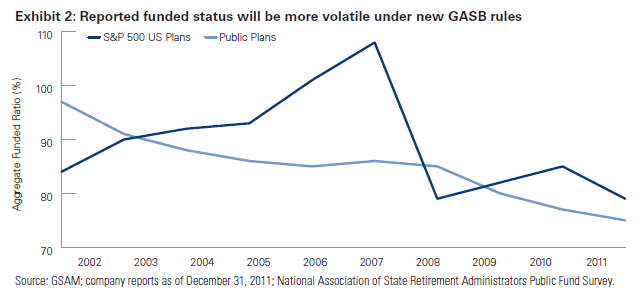

Regardless of whether adoption of the new rules results in higher or lower funded ratios, reported funded ratios will be more volatile. Exhibit 2 compares reported funded ratios for corporate plans, using the S&P 500 as the universe, with reported funded ratios for state and local plans. Of particular note is how much more volatile the corporate ratios are than the public ratios. Some of the difference in volatility is explained by different accounting liabilities, since public plans use a relatively stable EROA assumption for the discount rate each year while corporate plans adjust annual discount rates based on market interest rates. However, use of market value for assets by corporate plans versus actuarially smoothed asset values by public plans certainly contributed as well. Movement to market values will increase volatility of reported public plan funded ratios.

Note also that these differences in reporting can lead to seemingly different results for each universe. For example, reported corporate DB funded ratios were rising between 2002 and 2006, while reported state and local funded ratios were falling.

Credit rating agencies incorporating their own methodologies – GASB changes a non-event?

Interest in public DB pension issues has never been higher. Many policymakers, investors, academics and the financial media have focused on public pension deficits in recent years (see following page). In addition, several credit rating agencies are incorporating their own methodologies for evaluating the status of pension programs as part of their ratings processes. These efforts are an attempt to bring greater transparency and consistency to the analysis of pension obligations. For example, in 2011 Fitch announced changes to its methodology whereby investment return/discount rate assumptions and asset valuations were adjusted. Moody’s currently has a proposal to use a uniform discount rate and remove asset smoothing when evaluating public pension programs. Given that the GASB changes do not alter the economics of the plans, and that rating agencies are making their own adjustments to reported data anyway, it can be argued the GASB changes should not lead to immediate ratings actions.

Nonetheless, several rating agencies have indicated they may reassess their methodologies once the new reporting is in place, particularly the enhanced disclosure requirements. Gaps in information in the existing reporting framework meant that some users of pension-related disclosures were left to draw conclusions and “connect the dots” themselves. More information helps to facilitate incremental analysis which could, at times, contribute to a change in view. This will be an important aspect of these changes to monitor once the new reporting is in place.

Intense focus on public DB issues is likely to only increase with new GASB reporting

The new GASB rules were finalized at a time when interest in public DB pension issues has never been greater. Increasingly this focus has not only been from municipal bond investors, academics and the financial media, but also policymakers and regulators. As seen in some of the excerpts from recent studies below, a great deal of the focus has been on the transparency and accuracy of pension data as well as the potential implications of underfunded plans on governmental sponsors. The new GASB rules will increase transparency but also make some plans look less well off than under existing rules. Implementation of the new GASB rules will likely increase the attention on an area that has seen its fair share of it in recent years.

Policymakers and other government officials increasingly focused on public pension issue

SEC Report on the Municipal Securities Market – July 31, 2012

(Securities & Exchange Commission)

“Regardless of the methodology used for measuring pension and OPEB liabilities, the accuracy and adequacy of disclosure regarding pension and OPEB funding obligations by municipal securities is a focus of legislators, the Commission, issuers, and investors alike.”

Report of the State Budget Crisis Task Force – July 17, 2012

(State Budget Crisis Task Force)

“Pension plans need to account clearly for the obligations they assume and disclose the potential shortfalls and risks they face. Legislators, administrators, and beneficiaries alike need to develop and adopt rules for the responsible management of pension plans and mechanisms to ensure that required contributions are paid.”

State and Local Government Defined Benefit Pension Plans: The Pension Debt Crisis that Threatens America – January 2012

(United States Senate Committee on Finance)

“Although the debt associated with underfunded pension plans is not as transparent to the public as municipal bond debt, it represents the greater portion of aggregate municipal debt.”

The Underfunding of State and Local Pension Plans – May 2011

(Congressional Budget Office)

“The recent financial crisis and economic recession have left many states and localities with extraordinary budgetary difficulties for the next few years, but structural shortfalls in their pension plans pose a problem that is likely to endure for much longer.”

Changes to corporate DB accounting and reporting contributed to asset allocation shifts

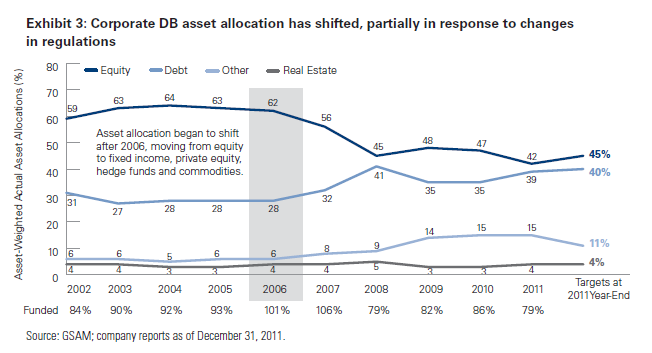

Similar rule changes in the corporate DB space enacted in 2006 contributed to behavioral changes by plan sponsors which, in some cases, resulted in changes in investment strategy and asset allocation. In general, corporate DB plans have increased de-risking activities in recent years partially as a result of more stringent regulatory and financial reporting rules. Exhibit 3 details the historical asset-weighted asset allocations for US corporate DB plans of S&P 500 companies. [4] Note that after 2006, asset allocation shifted with equity allocations decreasing and fixed income and “other” increasing. For many plans, other includes allocations to alternative asset classes such as private equity, hedge funds and commodities. It is possible that these changes by the GASB could have similar influences on sponsors of public DB plans.

Important differences between corporate and public plans

Nonetheless, important differences between public plans and private plans will likely result in a different reaction by state and local sponsors. We highlight several important differences below:

- Funding deficits are larger in public plans than in corporate plans: As previously detailed in Exhibit 1, when reported funded ratios are calculated in a similar (although not exactly the same) manner, it becomes apparent that the funded ratios in the public sector are much lower than in the private sector. Consequently, the need to generate returns to help plug funding gaps remains a priority. Many corporate plans are in de-risking mode and are therefore increasing allocations to fixed income to better match the characteristics of their liabilities. But for public DB plans, the need to generate returns to help make up funding deficits is leading many to be in a re-risking mode.

- De-risking would increase reported pension obligations and lower reported funded status: Liabilities are still valued differently between corporate and public plans. Moving to a fixed income-oriented portfolio would result in the use of a lower discount rate since long-term expected returns on that asset class are generally below those of equities, alternatives and real estate. This would result in larger reported pension obligations and, therefore, even larger funded deficits. Simply changing asset allocation in this way would therefore have negative ramifications on reported pension results.

- Many public DB plans are still open and accruing new benefits: The trend in the corporate space of closing and freezing plans and concurrently moving employees to a defined contribution program has been going on for several decades. A recent study by Aon Hewitt indicated that over 60% of companies have closed their DB plans to new entrants. While there have been efforts in recent years to enact the same sort of changes in the public DB universe, many plans remain open. The need to help fund new benefit accruals will require public DB plans to continue to focus on return generation as opposed to de-risking strategies.

- Corporate plans went through other regulatory/reporting changes that also influenced their behavior: Passage of the Pension Protection Act of 2006, which moved the calculation of regulatory funded status and contribution requirements to more of a mark-to-market system, was certainly a significant influence. Potential future accounting changes in the US corporate space, foreshadowed by changes recently issued by the International Accounting Standards Board, have also influenced some plan sponsors. The GASB changes do not change contribution requirements directly, nor would changes to international corporate pension accounting have a direct effect on public DB plans. [5]

III. Focusing on the course of action: Public plans looking at liabilities, contributions and diversifying asset allocation

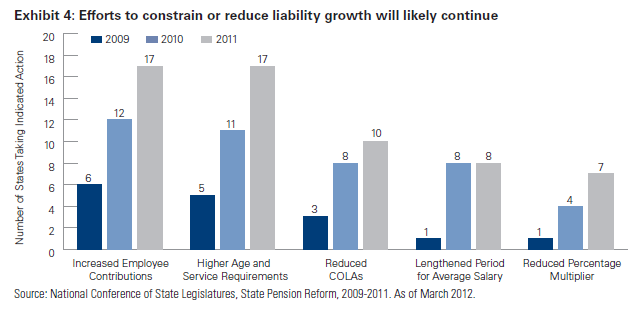

We believe that rather than resulting in changes in strategy, the GASB rule changes may serve to accelerate trends that have already been in place in the public sector over the past several years. On the liability side, many state and local governments have moved to reduce pension obligations or curb their future growth by taking actions such as eliminating cost of living adjustments (COLAs) or raising retirement ages. Increased transparency around funded levels and, in some cases, larger funding deficits which may be reported under the new GASB rules, will likely provide further impetus for public officials to seek ways to constrain the growth of future pension obligations. Exhibit 4 summarizes actions taken by state and local governments over the past few years with respect to pension obligations.

However, these actions, in isolation, may not be enough to help some plans to return to funding levels deemed to be acceptable. While additional contributions from plan sponsors would also help to improve funded balances, some state and local governments are not in a position to increase contributions in the current economic environment.

Given this, the ability for many plan sponsors to generate returns on existing and future plan assets will take on even more importance in a post-GASB world. Plan sponsors will need to:

- 1. generate acceptable returns to help alleviate funding deficits while also

- 2. minimizing volatility, since funded status will now be on the balance sheet and will be based on actual asset values as opposed to smoothed actuarial asset values, and do this

- 3. in an environment where long-term expected returns across a wide swath of asset classes are falling.

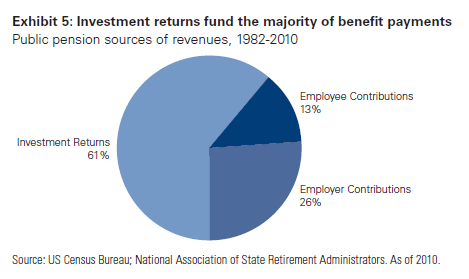

Investment returns are a crucial source of funds for pension programs. As seen in Exhibit 5, over 60% of public pension revenues over the roughly 30-year period through 2010 were derived from investment returns. Lower investment returns going forward would place an even larger burden on contributions, from both employers and employees, as well as likely increase efforts to constrain liability growth.

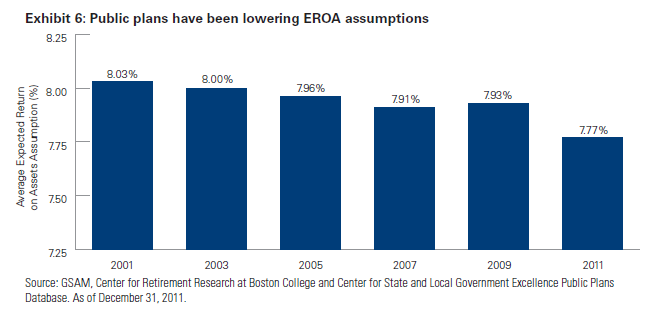

Unfortunately return expectations across multiple asset classes are declining. Indeed, while the median return expectation for public plan sponsors is 8%, where it has been anchored for the last several years, the average return expectation has been steadily declining. Exhibit 6 details the historical average expected return assumption for state and local plans. We note that corporate DB EROA assumptions have been declining at an even faster rate in recent years, although some portion of these reductions is linked to changes in asset allocation previously detailed in Exhibit 3.

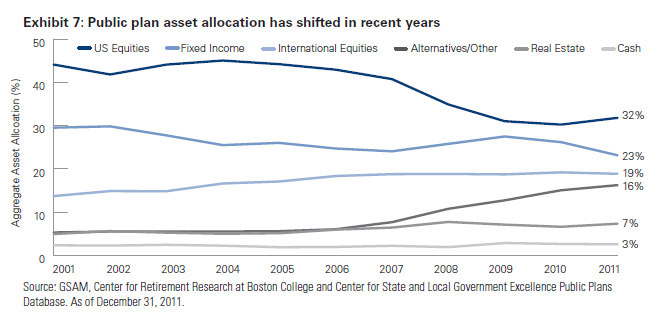

In response to these realities, many public DB plan sponsors have moved to diversify their portfolios as a means to achieve better risk-adjusted returns. Some plans have, in recent years, reduced exposure to US public equities and increased exposure to non-US equities and alternative investments such as private equity, real estate, commodities and hedge funds. Exhibit 7 details how many of these changes also began to occur around 2006, just as they did in the corporate sector as previously detailed in Exhibit 3.

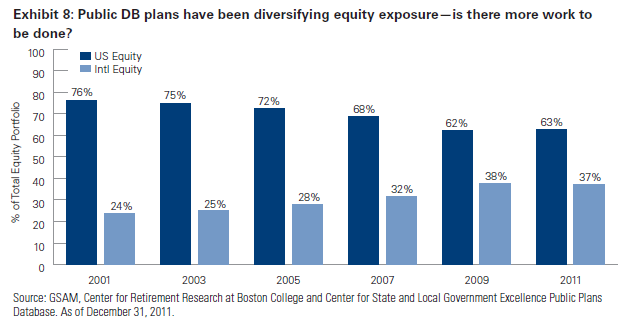

Not only have equity allocations declined in recent years, but the composition of equity allocations has shifted as well. Exhibit 8 demonstrates that roughly 10 years ago almost three-quarters of a public plan’s equity allocation was in US equities. More recently, that percentage has dropped to 63%. A key question is, despite this shift, whether there is more re-allocation to be done in this asset class?

Considering that US equities currently account for less than half of the total value of global equities and US GDP comprises only about 20% of global GDP, it can be argued that even though the allocation to US equities has declined, additional shifts would be warranted. Despite these changes, US equities still, in many cases, comprise the largest component of a plan’s asset allocation. We might expect public DB plan sponsors to continue to diversify their equity allocations away from US/developed equity to emerging/growth markets.

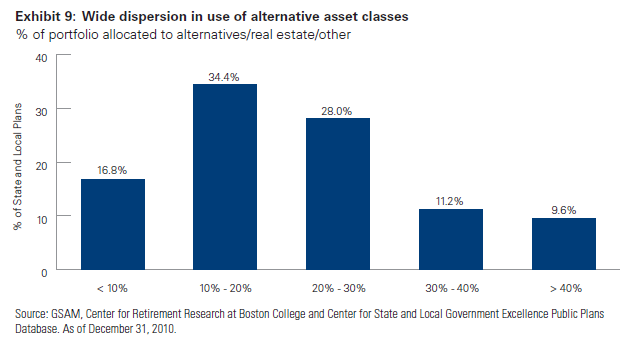

Similarly, the data in Exhibit 7 indicate that public DB plans have doubled their allocations to alternative investments in recent years while also increasing allocations to real estate. However, Exhibit 9 details that there is wide dispersion in the use of alternatives and real estate by public DB plan sponsors. While almost 10% of public plans had at least a 40% allocation to these asset classes, almost 17% had less than a collective 10% allocation.

We believe inclusion of alternative investments in a portfolio will take on even more importance for public DB plan sponsors given the GASB changes. We might expect more plans to increase allocations in these areas for both return enhancement and volatility dampening attributes.

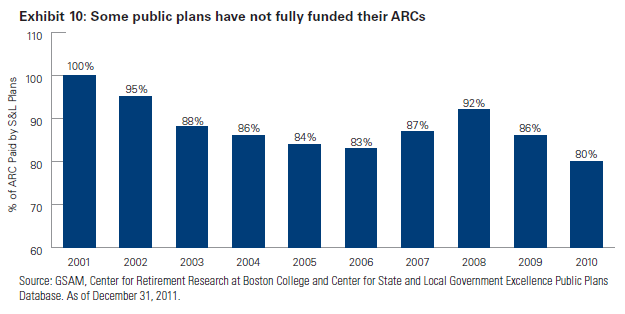

Finally, we note that while the new GASB rules will not have a direct effect on contributions, they could indirectly provide an incentive for plan sponsors to increase contributions in future years. Placing the funded status directly on the balance sheet will make this deficit more prominent and may lead to an increase in pressure on state and local governments to take actions to raise funded levels. As seen in Exhibit 10, state and local plans have not, in aggregate, fully funded their ARC over the past several years.

Note that contributing cash into the plan may, for some, help both sides of the funded status equation. Contributing cash directly raises plan assets and lowers funded deficits. However, for pension plans that must use a blended discount rate if projected future assets do not cover expected future benefit payments, raising asset levels may allow the plan to justify use of just the expected return assumption for discounting purposes. Use of the expected return assumption as opposed to a blended rate would result in a higher discount rate, lowering the present value of the obligation and also raising funded status.

Conclusion

New rules issued by the GASB will alter the way state and local governments account for and report the results of their defined benefit pension plans. Under the new rules, some plans may report larger pension deficits because they 1) will no longer be able to smooth asset values for financial reporting purposes, 2) may use a lower discount rate if their projected assets are not sufficient to cover benefit payments or 3) both. These deficits will now be recognized on the balance sheet just as they are accounted for by corporate DB plan sponsors. In addition, certain metrics, such as funded status and pension expense, will be more volatile going forward.

Interest in public DB pension issues has never been greater. Many policymakers, investors, academics and the financial media have focused on public pensions in recent years. Several rating agencies are incorporating their own methodologies for evaluating the status of pension programs as part of their ratings processes. These changes by the GASB may serve to further focus attention on many of the most stressed state and local pension programs.

These changes, however, do not affect the economics of the pension plans. They do not change the benefit payments owed to participants or contribution requirements by plan sponsors. In some respects the changes are not as dramatic as some had expected over the course of the GASB’s multi-year project which resulted in these revisions. Nonetheless, they may make reported pension data appear worse for some plans. In addition, pension status and performance will be more transparent and more volatile.

Similar rule changes in the corporate DB space several years ago contributed to changes in behavior by private plan sponsors. These behavioral changes led to, at times, changes in investment strategy and asset allocation. It is possible that the GASB changes could have a similar influence on sponsors of public DB plans. However, important differences between corporate plans and public plans will likely lead to different reactions by the public universe.

We believe that rather than resulting in changes in strategy, the GASB rule changes will serve to accelerate trends that have already been in place over the past several years. On the liability side, many state and local governments have moved to reduce pension obligations or curb their future growth. They have taken actions such as eliminating COLAs or raising retirement ages. Larger funding deficits, which may be reported under the new GASB rules, would provide further impetus for public officials to seek ways to constrain the growth of future pension obligations.

However, these actions in isolation will not be enough to help some plans return to acceptable funding levels. While additional contributions from plan sponsors would also help to improve funded balances, some state and local governments are not in a position to increase contributions in the current economic environment. Consequently, for many plan sponsors, their ability to generate returns on existing and future plan assets will take on even more importance.

Many public DB plan sponsors have moved to diversify their portfolios in recent years by reducing exposure to US public equities and increasing exposure to non-US equities and alternative investments such as private equity, real estate, commodities and hedge funds. However, there has been wide dispersion in the adoption of these strategies. We believe the need to achieve acceptable returns— while also minimizing the volatility of returns—will become an even higher priority, especially in an environment where long-term expected returns across a variety of asset classes are falling.

Endnotes

[1] The two new standards include almost 400 pages of guidance.

(go back)

[2] Many public DB plans, however, did use the ARC as the de facto amount to be contributed and many interested parties, such as credit rating agencies, looked at actual contributions versus the ARC as a measure of whether or not a pension plan was on track to fund its obligations.

(go back)

[3] Assuming a plan does not adjust its EROA higher which would, of course, increase the discount rate. As we discuss later in this paper, such a change would seem unlikely in the current environment and considering recent trends in EROAs across both public and corporate DB plans.

(go back)

[4] These plans collectively account for approximately half of the total assets in the US corporate DB system.

(go back)

[5] Although we acknowledge that any change in pension reporting/regulation, whether it be in the US or abroad or with public or private plan sponsors, enlightens the conversation around the rules and regulations for any plan sponsor. This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. Please see additional disclosures.

(go back)

Copyright © 2012 Goldman Sachs. All rights reserved.