Print

PrintMatteo Tonello is managing director of corporate leadership at the Conference Board. This post is based on an issue of the Conference Board’s Director Notes series by James Cerruti, senior partner of strategy and research at Brandlogic Corp. This Director Note is based on an article written by Mr. Cerruti; the full publication is available here.

Major companies across industrial sectors are putting more effort and investment into demonstrating good corporate citizenship on environmental, social, and related governance factors. However, research shows that it may be getting harder for companies to gain recognition for doing so.

Last year, Brandlogic and CRD Analytics prepared the 2012 Sustainability Leadership Report: Measuring Perception vs. Reality, marking the second year for the annual report and continuing our pioneering work in measuring and comparing real sustainability performance to the perceptions of key stakeholders. This follow-on study used the same methodology established for the inaugural report, as described in a November 2012 issue of Director Notes (see “About the Sustainability Leadership Report,” p. 2, for a summary). [1] Moreover, the follow-on study validated the methodology’s usefulness as a management framework for making decisions about if and where to invest in sustainability, both on the operational and communications fronts.

With a second set of data in hand, we are able to observe year-over-year movement. Overall, real performance on sustainability is rising, reflecting ongoing and intensifying corporate efforts to define and achieve sustainability goals.

However, perceived performance, on average, is declining. The findings suggest that it is becoming more difficult to achieve differentiation among those audiences who are most attentive to sustainability, despite a better track record. This finding is both striking and surprising. Why is perception slipping despite an increasing volume of communications around sustainability? In what follows, we explore possible answers.

2012 Report Findings: A Story of Divergence

The good news is that, in 2012, real total environmental, social, and governance (ESG) performance rose for 93 of the 94 companies surveyed in both years of the report (six companies were replaced for various reasons pertaining to selection criteria). The increase suggests that businesses are taking sustainability seriously and making it a part of the business strategy. It also has an implication for rankings: better performance, generally, raised the mean by 9 points, making it more difficult for companies to rise into the Leaders quadrant of the Brandlogic Sustainability IQ Matrix™.

(See “About the Sustainability Leadership Report” for details on the quadrants found in the Sustainability IQ Matrix.)

In a number of cases, these gains in real ESG performance were dramatic. Roughly one-fifth of companies increased their scores by more than 10 points. Seven of these saw increases of more than 24 points on the 100-point Sustainability Reality Score (SRS) scale.

On the perception front, the story was very different. The mean Sustainability Perception Score (SPS) dropped from 47.2 in 2011 to 44.5, and, of the 94 companies surveyed in both years, more than two-thirds (68) saw a decline in their score. Twenty-seven companies experienced declines of five points or more, with 12 of these dropping by more than eight points.

Looking at the relationship of reality scores to perception scores also yielded some interesting findings. In almost every case in which a company’s reality score was higher than its perception score (32 of 33 companies), the gap has widened. Given the general improvement in real performance and the decline in perceived performance, this is not surprising. Similarly, in all 26 cases in which the reverse situation exists—the company’s perception score was higher than its reality score—the gap has narrowed. In 35 instances, the gap flipped direction, and, in all of these cases, the shift was from perception leading reality to the opposite.

What’s notable is how dramatic some of the changes were. In 2011, 15 companies had a perception score that was higher than the reality score by more than 20 points. In 2012, there were only two: Facebook and Amazon. Both had very low scores across all dimensions, Facebook performing worst on the social dimension (12.5 points) and Amazon struggling most on environmental (8 points). Bank of America also saw a marked shift. Its perception score remained stable, while its real performance score jumped 28 points after more than doubling its environmental score and almost doubling its social score.

What the Findings Suggest

It’s clear from the divergence in the SRS and SPS scores that companies’ ability to deliver on sustainability is outstripping their ability to communicate their sustainability achievements effectively. But why? We know that the volume of communications, in the form of corporate responsibility reports and similar messaging, as well as in advertising and other brand communications, is on the rise. Brand reputation— both positive and negative—plays strongly here.

For example, Apple has the highest perceived performance score, despite below-mean real performance and a relatively modest commitment to ESG factors. Meanwhile, ExxonMobil has a high sustainability reality score, but, despite major efforts to communicate its sustainability commitments, the company can’t seem to elevate perception. Its industry’s poor reputation creates significant headwinds. This reinforces the long-term value of investing to build a positive brand image.

Companies’ poor perception scores may also reflect increasing skepticism by key stakeholders, some of whom may not be seeing the benefits they expect from these companies’ sustainability practices. Part of the data that supports the SPS rankings is highly suggestive and supports this idea.

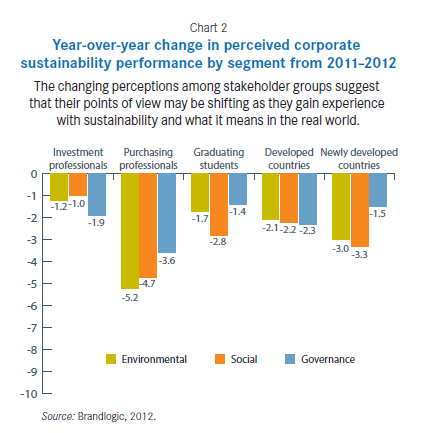

In both the 2011 and 2012 studies, graduating students provided the lowest overall ratings of corporations, perhaps reflecting a natural skepticism about corporate citizenship among younger people. Perceptions from the two other stakeholder groups changed significantly. As shown in Chart 2, in 2012, downgrades in perceptions by purchasing professionals were twice to four times as large as those among investment professionals. Given that those directly involved in the supply chain are exposed to operational realities, while investors focus on financial results, it’s easy to see why purchasing professionals may be less willing to buy into a company’s sustainability story if it’s not supported by what they see on a daily basis.

There were also distinct differences in the magnitude of perception change between respondents in newly developed countries and those with more mature economies. Overall, environmental and social perception scores saw larger declines among newly developed countries, while governance perception scores for those countries held up better than the scores for developed countries. It should be noted that in the inaugural 2011 study, perception ratings were much higher overall in newly developed countries; the changes shown in Chart 2 actually reflect a closer alignment between newly developed and developed countries, although perception scores are still higher in newly developed countries than in developed countries. It is possible that these differences are cultural in nature: those respondents in mature markets could be applying higher personal standards to corporate citizenship.

Why This Should Matter to You

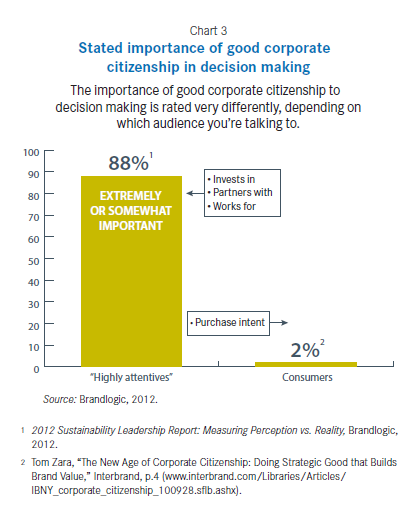

As a rule, consumers do not make choices based on perceptions of corporate citizenship, so if they don’t care, why should you? The answer is that there are audiences for whom sustainability is vitally important and for whom corporate citizenship—especially on social factors—plays a large role in decision making. We refer to these audiences as “highly attentive” and they include:

- Investment professionals They base their decisions on all aspects of corporate performance.

- Purchasing managers Increasingly, their own organization’s sustainability policies give preference to suppliers that also operate sustainably.

- Graduating university students They are in the process of deciding where they want to work, and the long-term sustainability of prospective employers is of great importance to them.

Eighty-eight percent of respondents characterized as “highly attentive” state that corporations’ good corporate citizenship is either extremely or somewhat important in the decisions they make to invest in, partner with, or work for a company. Half say it is extremely important. Attracting investment, forging solid business relationships, and nurturing the talent pipeline are all critical to any company’s long-term success—ample reasons to make a serious commitment to both sustainability performance and communicating it.

An Opportunity for Action

Whether the slip in perception ratings signals a trend or a one-time correction remains to be seen. It does, however, point to an important opportunity for companies across all industries. Facing greater skepticism across the board, it is important for companies to ramp up their efforts to communicate both their sustainability commitments and accomplishments in a way that resonates with their key audiences. Many do this in the form of a corporate sustainability report (CSR) that is prepared in parallel with their annual report. Others take an integrated approach and blend ESG data into their annual reports. However, these are not the only communications channels being leveraged. An increasing number of companies are moving toward integrating sustainability messages directly into corporate brand communications and customer value propositions, thus gaining the efficiencies of leveraging primary channels of persuasion. [2]

Most of the Leaders in the 2012 study have also become quite adept at incorporating sustainability into the presentations they use to engage directly with discrete stakeholder groups, whether an investor road show or a campus recruitment visit. As a whole, these initiatives are still relatively new and the quality of communications varies widely. It’s worth the effort to sample what’s available, whether in the form of a CSR, sustainability website, or other communications, and learn from it to guide your own strategy.

An Ongoing Examination of Perception vs. Reality

In addition to providing a follow-on set of data, the second annual Sustainability Leadership Report also features detailed breakdowns of specific GICS industry categories, allowing direct comparisons of peer companies. In a forthcoming Director Notes, we’ll take a closer look at them and highlight some standout companies from this year’s group.

Common Characteristics of Sustainability Leaders

- Treat sustainability as an integral part of business strategy, not just a compliance issue. Some Leaders build a corporate strategy that focuses on the value of adherence to key sustainability principles in terms of enhanced operations, finances, and relationships. They have evolved a clear business case for sustainability initiatives and see that it is possible to “do well by doing good.”

- Take responsibility for the impact of internal operations and those of associated entities, such as supply chain partners. Leading companies have issued formal codes of conduct for suppliers that define minimum performance standards on ESG and also hold suppliers responsible for the conduct of subcontractors. Having these codes shows an understanding that sustainability is not an isolated concept, but one that is based on understanding and managing interdependencies in the value chain of the business.

- Implement GRI standards for reporting and ensure that the materiality of sustainability issues is understood by all stakeholder groups. Leaders excel at meeting the GRI standards fully and transparently. Using recognized standards is essential because it helps ensure acceptance by stakeholders. In addition, highlighting the materiality of sustainability issues in a way that is meaningful for each stakeholder group sets the tone for both operational and strategic decisions across the enterprise.

- Integrate sustainability into the brand and client value propositions. Making sustainability a central part of the customer conversation can yield enormous benefits in terms of brand value, fundamentally changing how a company is viewed in the marketplace.

- Focus their operational initiatives and related communications on carefully selected themes tied to the core of the business. Leaders tend to use relevant themes to create varied, yet complementary, communications to key stakeholder groups.

For specific examples of practices used by leading companies, see James Cerruti, “Charting a Path to Sustainability Leadership,” Director Notes, Vol. 4, No. 22, The Conference Board, November 2012.

About the Sustainability Leadership Report

The rationale and methodology behind the annual Sustainability Leadership Report is described in detail in the November 2012 Director Notes, “Charting a Path to Sustainability Leadership.” In summary:

- 100 leading global brands were sampled across nine selected Global Industry Standard Classification (GICS) categories.

- Real reported performance ratings on 141 environmental, social, and governance factors were provided by CRD Analytics, the company behind the NASDAQ OMX CRD Global Sustainability Indexsm.

- Brandlogic conducted the quantitative perception survey among three highly attentive audiences: investment professionals, purchasing/supply professionals, and graduating students who will soon be entering the workforce. These audiences were located in six countries, representing both mature and emerging economies: the United States, the United Kingdom, China, Japan, India, and Germany.

- The two sets of data were aggregated and mapped to a pair of 100-point scores: the Sustainability Reality Score (SRS) and Sustainability Perception Score (SPS). These were plotted on a grid—the Brandlogic Sustainability IQ Matrix™—allowing direct comparison of all surveyed companies. The Sustainability IQ Matrix comprises four quadrants:

- 1 Leaders Those who excel in both real and perceived performance

- 2 Promoters Those with relatively high perceived performance, but relatively low real performance

- 3 Challengers Those with good real performance but low perception ratings

- 4 Laggards Companies that trail on both dimensions

For a copy of the 2012 Sustainability Leadership Report, visit www.sustainabilityleadershipreport.com.

Endnotes

[1] James Cerruti, “Charting a Path to Sustainability Leadership,” Director Notes, The Conference Board, Vol. 4, No. 22, November 2012.

(go back)

[2] John Peloza et al., “Sustainability: How Stakeholder Perceptions Differ from Corporate Reality,” California Management Review, Vol. 55, No. 1, Fall 2012, pp. 74–97.

(go back)