Print

PrintRobert F. Serio is head partner in the New York office of Gibson, Dunn & Crutcher and co-chair of the Securities Litigation Practice Group. This post is based on a Gibson Dunn client alert.

2012 proved to be a mixed year for defendants in securities litigation, with several open questions and rare causes for optimism. The raw statistics show a steady stream of new filings, increasing median settlement amounts, and relatively low dismissal rates for existing cases. The Supreme Court will decide an important case this coming term on the issue of class certification in securities class actions, while another important case on standing awaits the Court’s decision on a pending petition for certiorari. In the appellate courts, a number of trial court decisions dismissing class action suits were affirmed, but district courts continue to issue conflicting rulings on critical disclosure issues, including the application of the SEC’s Regulation S-K to private class actions-where several courts have allowed class claims to proceed on the basis of alleged failure to disclose “known trends.”

Trial courts are issuing divergent opinions on the application of the Supreme Court’s 2010 decision in Morrison v. Australia National Bank to claims involving the extraterritorial reach of the federal securities laws. District courts also are struggling to define who can be sued for primary liability for “making” an allegedly false statement, following the Supreme Court’s 2011 ruling in Janus Capital Group Inc. v. First Derivative Traders. We discuss each of these trends below. Finally, we summarize several notable decisions arising in the world of M&A litigation, an area of securities litigation that has shown explosive growth over the last few years. For a comprehensive review of related trends in the Securities Enforcement and the Foreign Corrupt Practices Act areas, please see our 2012 Year-End Client Alerts, here and here.

Filing and Settlement Trends

2012 was a “down” year for defendants in securities class actions: filing rates remained steady, dismissal rates deteriorated, and median settlement values jumped dramatically to record levels. The ratio of settlement values to investor losses also worsened (i.e., with higher recoveries) from the prior year. All in all, the 2012 trends suggest “business as usual” for the plaintiffs’ bar for the upcoming year-hundreds of suits and significant settlement values are expected.

Class Action Filings

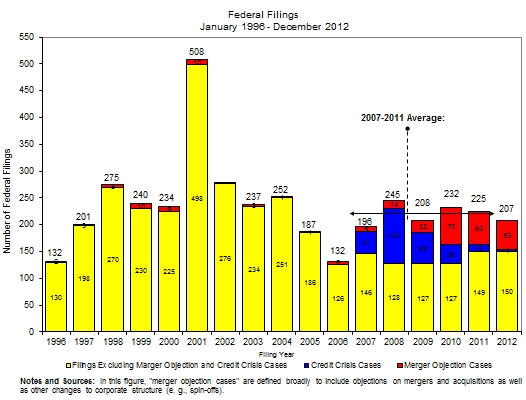

According to a study by NERA Economic Consulting issued in December 2012, the number of new class actions filed in federal court in 2012 under the Private Securities Litigation Reform Act of 1995 (“PSLRA”) decreased slightly from the level of new filings in 2011, and fell below the average of cases filed in the period 2007-2011. See Dr. Renzo Comoli, Dr. Ron Miller, Svetlana Starykh, & Sukaina Klein, 2012 Trends in Securities Class Actions: Settlements Plummet; Dismissals Down Even More, NERA Economic Consulting (December 11, 2012). The overall filing rates are reflected in Figure 1 below (all charts courtesy of NERA Economic Consulting). NERA reports a total of 207 new cases filed in 2012, down from 225 in 2011. Merger objection cases represent a sliver of those cases, but do not include the many such class suits filed in state courts, most notably the Delaware Chancery Court.

Credit Crisis Cases. The total volume of filings in 2012 reflects the gradual decline of “credit crisis” class action cases, which achieved their zenith in 2008 (with more than one hundred new cases), but now have sunk to an all-time low in 2012 (only four cases). This is not to say that “credit crisis” cases do not continue to plague financial institutions who have been sued over the last five years for securities fraud arising out of the issuance of subprime mortgages, mortgage-backed securities, auction rate securities, and the like. On the contrary, many major credit crisis cases are still pending, and are garnering massive settlement amounts in some cases. In addition, while credit crisis class actions may be on the decline, a new generation of cases have replaced them: single-plaintiff suits by government agencies (such as the Federal Housing Finance Agency on behalf of Fannie Mae and Freddie Mac), monoline insurers (such as MBIA), and institutional and pension fund investors who purchased a wide variety of mortgage-back securities, have accelerated in the last two years. A number of these have been filed in state court, and involve state law claims for misrepresentation in the MBS securitization offering documents. The stakes in these cases, even when not brought on a class-wide basis, can be massive, and likely will continue to plague the industry for some time to come.

Chinese Reverse Merger Cases. Also on the decline are the once highly publicized Chinese “reverse merger” cases, which represented a significant portion of new case filings in 2011. The predictions of some defense counsel that these types of cases would continue to grow have proven off the mark, but many such cases remain pending. The level of new case filings involving Chinese-based companies declined from 37 in 2011 to only 16 in 2012.

Merger Cases. As has been widely reported in the last few years, merger litigation is on the rise, as the plaintiffs’ bar has made a cottage industry out of filing class action cases objecting to the terms of an announced merger or acquisition. Indeed, it can almost be assumed that any M&A transaction stands a relatively high risk of at least one, if not multiple, class and derivative securities lawsuits being filed, often in multiple competing actions in different courts. This is so even where target shareholders are paid very substantial premiums and no procedural or disclosure issues exist in the transaction. Also discussed below in our “Notable Delaware M&A Litigation Trends in 2012” section, M&A litigation trends are frightening, particularly as eight-figure fee awards to plaintiffs’ counsel in several high profile M&A cases have provided new economic incentives for the plaintiffs’ bar to file more and more such cases. “Ready, shoot, aim” is an apt metaphor for the growing phenomenon of M&A suits filed within 24 hours of the announcement of a significant transaction. As the 2012 study by NERA reports, merger class actions account for a heavy percentage of total class action filings in the federal courts in the last three years: 53 M&A class actions were filed in 2012 alone, contributing to a three-year average of over sixty such cases a year. See Figure 1 above.

Filing by Industry Sector. The trends in new case filings against particular industry sectors reflect the precipitous decline in “credit crisis” cases, as new suits against financial institutions have dropped from record-shattering levels in 2008 to third place in 2012, behind new case filings against companies in the health technology and electronic technology sectors. Notable also is the steady increase in new case filings against companies in the energy sector, ranked fourth in 2012, and increasing every year since 2008. While there is no clear explanation for the rise in suits against health technology companies, it is clearly a trend to watch in 2013.

Dismissals of Class Actions

Almost all securities class actions follow one of two paths: dismissal or settlement. When the PSLRA was enacted in 1995, issuers and their directors and officers had high hopes that the new pleading standards in the PSLRA would put a stop to the kinds of meritless cases brought by “pet plaintiffs”-popular sport for many years following the Supreme Court’s adoption of the “fraud-on-the-market” presumption of reliance in cases brought under Section 10(b) of the Securities Exchange Act of 1934. Alas, over the last 17 years since the PSLRA became law, the annual rate of dismissals has never exceeded the rate of settlements. As reflected in Figure 3 below, 2012 was no exception: defendants settled 93 cases, while achieving a dismissal of only 60 cases. According to NERA, the 60 cases dismissed in 2012 represents the lowest number of dismissed cases since 1998. And while 2012 dismissals represent improvement over the three years immediately following passage of the PSLRA, it hardly provides encouraging statistical evidence that the stringent pleading standards Congress put into place in the PSLRA are having their intended results. One notable exception may be the PSLRA’s impact on appellate courts, whose willingness to uphold trial courts’ dismissals is discussed below in “Pleading and Proving ‘Scienter’ or State of Mind.”

The dismissal rates reflected in Figure 3 do not speak to another important trend that makes the modern securities class action so frustrating to the clients who are sued, and the lawyers who must defend them: in general, the average disposition time of PSLRA class actions has lengthened considerably, to the point that in many cases the threshold motions to dismiss can take years, as courts now routinely grant leave to amend even when the case clearly lacks merit. As a result, the “inventory” of cases pending in any given year is enormous. Over the last five years, NERA calculates that the number of securities class action cases pending in the federal courts averages 582 annually. In 2012, total pending cases are projected to have totaled 593, higher than any year since the boom year of 2008 when the credit crisis hit the financial markets. See Dr. Renzo Comolli, et al., 2012 Trends in Securities Class Action Litigation, at 3. Clearly, the statistical odds of obtaining a dismissal of a securities class action are not attractive, and are not improving.

Class Action Settlements

Average and median settlements in 2012 increased in all categories over the previous year, even when excluding settlements over $1 billion (and certain other non-representative categories of cases). Average settlements in 2012 were $36 million, compared to $31 million in 2011. As Figure 3 shows, median settlements-generally a better barometer of settlement trends-also increased in 2012 over 2011, at $12 million compared to $7.5 million. According to NERA, the 2012 median settlement amount is the highest since passage of the PSLRA in 1995. See Dr. Renzo Comolli, et al., 2012 Trends in Securities Class Action Litigation, at 5.

One can speculate about what may account for the rising trend in 2012, and whether it represents a trend at all. In any given year, of course, the statistics can mask a number of important factors that contribute to settlement value, such as (i) the amount of D&O insurance; (ii) the presence of parallel proceedings, including government investigations and enforcement actions; (iii) the nature of the events that triggered the suit, such as the announcement of a major restatement; (iv) the range of provable damages in the case; and (v) whether the suit is brought under Section 10(b) of the ’34 Act or Section 11 of the ’33 Act. The last two years also included the resolution of several of the major credit crisis cases that just now are reaching the settlement stage (with more such cases to come). For example, the Lehman Brothers litigation settled in 2012, which had the effect of increasing both the average and median settlement amounts in 2012.

Whatever the variables, the 2012 median settlement of $12 million should raise concern for issuers with cases still in “inventory,” because plaintiffs’ counsel and mediators often look to prior settlement “benchmarks” when assigning settlement values to cases. A system of justice that consistently rewards plaintiffs’ lawyers with eight-figure settlements in the typical case is a disturbing trend, to say the least.

One other aspect of 2012 settlement trends concerns how settlement amounts compare to the actual damages exposure in a given case. According to NERA, the ratio of median settlement dollars to investor losses ticked up last year, from 1.3% in 2011 to 1.8% in 2012, bringing the five-year average to 2.12%. The bright spot among these statistics, perhaps, is that despite the record level of median settlements in 2012, settlements continue to represent a small fraction of overall investor losses.

A final note on attorneys’ fees in securities class action settlements: they continue to be in the hundreds of millions of dollars per year. Indeed, according to NERA, plaintiffs’ lawyers’ “take” in the last five years has averaged $850 million per year. In 2012, the haul totaled $558 million. While many courts have grown skeptical about fee awards, and many plaintiffs’ firms have voluntarily reduced their fee petitions seeking a percentage of the aggregate settlement recovery, courts continue to award eye-popping amounts in some of the larger class actions. As one example, the fee award in the Lehman Brothers class action in the Southern District of New York, which settled in 2012, was over $56 million, despite the district court’s comments that most of the plaintiffs’ case-and therefore its settlement value-derived from the report of the Examiner appointed by the bankruptcy court to investigate potential wrongdoing by former officers and directors. On a percentage basis, the Lehman Brothers fee award worked out to “only” 10.99% of the settlement, with a multiplier of “only” 1.5, which the court said was because “we live in hard times.” Nevertheless, the fee award represented a huge recovery for plaintiffs’ counsel in absolute terms. With these kinds of paydays, the economic incentives for plaintiffs’ lawyers to keep bringing cases seem to be irresistible.

Supreme Court Developments

The two most significant high court developments in 2012 relating to securities litigation will have a lasting impact on how future shareholder class actions are brought and maintained.

Amgen Inc. v. Connecticut Retirement Plans & Trust Fund

On November 5, 2012, the Supreme Court heard oral argument in Amgen Inc. v. Connecticut Retirement Plans & Trust Funds, No.11-1085. The Amgen case presented two questions: First, whether a district court must require proof of materiality before certifying a plaintiff class based on the fraud-on-the-market presumption, and second, whether the court must allow the defendant to present evidence rebutting the presumption’s applicability before certifying the class. The Court focused on both the proper interpretations of Federal Rule of Civil Procedure 23 and the decision’s practical implications. During argument, the justices appeared divided along ideological lines. The liberal-leaning judges expressed concern that an immateriality determination at the class certification stage would simultaneously end any individual’s claim on the merits. Justice Scalia’s questioning focused on the practical implications of certifying a class-namely, that it all but guarantees a settlement. A decision is expected in June 2013.

Goldman Sachs & Co. v. NECA-IBEW Health & Welfare Fund

In November, Goldman Sachs filed a petition for certiorari, asking the Supreme Court to review the Second Circuit’s February 2012 decision in Goldman Sachs v. NECA-IBEW Health & Welfare Fund, 693 F.3d 145 (2d Cir. 2012), petition for cert. filed, 2012 WL 5361534 (U.S. Oct. 26, 2012) (No. 12-528) (“Goldman Sachs Cert. Pet.“). In that well-publicized decision, the Second Circuit held that a named plaintiff may assert claims on behalf of a putative class that the named plaintiff would not have standing to raise itself. The Second Circuit’s decision directly conflicts with a recent-and nearly factually identical-case in the First Circuit, Plumbers’ Union Local No. 12 Pension Fund v. Nomura Asset Acceptance Corp., 632 F.3d 762, 769-71 (1st Cir. 2011) (“Nomura”) (holding representative plaintiffs cannot assert claims involving securities that they did not purchase). Both analyze claims in the context of multiple trusts of residential mortgage-backed securities (“RMBS”).

Goldman Sachs issued certificates representing interests in 17 separate trusts of mortgages. Plaintiff NECA purchased certificates in two of those 17 trusts. The Second Circuit acknowledged that NECA “clearly lacks standing to assert” by itself claims regarding securities it never purchased, but nonetheless held that a plaintiff has class standing to assert the claims of purchasers of certificates in all 17 trusts. Goldman Sachs v. NECA, 693 F.3d at 148-49, 158 (citing Gratz v. Bollinger, 539 U.S. 244, 267 (2003)). When faced with the same issue in Nomura, the First Circuit concluded that “the claims related to the [trusts] from which the named plaintiffs never purchased securities were properly dismissed” for lack of standing, even in the context of a class action. Id. at 771.

The petition for certiorari asks the Supreme Court to decide whether the Second Circuit erred in concluding “that a representative plaintiff has standing to assert on behalf of absent class members claims for relief that the representative plaintiff lacks standing to assert on its own behalf.” Goldman Sachs Cert. Pet. at *i. The question as framed contrasts the Second Circuit’s NECA decision with both the First Circuit’s Nomura decision and Supreme Court precedent that the injury requirement for Article III standing must be made “for each claim” and that a plaintiff’s decision to style a suit as a class action “adds nothing to the question of standing.” Id. at *2 (citing DaimlerChrysler Corp. v. Cuno, 547 U.S. 332, 352 (2006) and Lewis v. Casey, 518 U.S. 343, 352 (1996)).

The implications of the Second Circuit’s decision, and the potential reach of a Supreme Court decision overturning it, are significant. Regardless of the merits, class certification in cases with significant amounts at stake generates tremendous pressure to settle. Additionally, the standard crafted by the Second Circuit that claims have “sufficiently similar … concerns” provides little guidance to lower courts in the Second Circuit and beyond. Goldman Sachs Cert. Pet. at *28.

Perhaps unsurprisingly, the Second Circuit decision has generated controversy in the district courts. District Courts outside the Second Circuit have rejected the decision outright. See, e.g., F.D.I.C. v. Countrywide Fin. Corp., No. 2:12-CV-4354 MRP, 2012 WL 5900973, at *10-12 (C.D. Cal. Nov. 21, 2012) (“The decision in NECA-IBEW has thrown the jurisprudence in this area into disarray … [w]ith respect, the Court is not persuaded). Even within the Second Circuit reactions have been mixed. Some judges responded by reviving previously dismissed claims, see, e.g., Plumbers’ & Pipefitters’ Local No. 562 Supplemental Plan & Trust v. J.P. Morgan Acceptance Corp. I, No. 08 CV 1713(ERK)(WDW), 2012 WL 4053716, at *1 (E.D.N.Y. Sep. 14, 2012), while others denied motions for reconsideration, in favor of awaiting Supreme Court guidance, see, e.g., In re IndyMac Mortgage-Backed Sec. Litig., No. 09 Civ. 4583 (LAK), Dkt. No. 390 (S.D.N.Y.) (“Lead plaintiffs’ motion for reconsideration … is denied without prejudice to renewal after the Supreme Court acts on the petition for a writ of certiorari in [Goldman Sachs v. NECA], and, if the writ is granted, decides the case.”).

Although NECA waived its right to respond to Goldman Sachs’s petition, the Supreme Court requested a response, due February 4, 2013. A decision on the petition is expected in March 2013. Gibson Dunn represents Goldman Sachs in its petition for certiorari.

Disclosing Material “Trends or Uncertainties” under Sec Regulation S-K Item 303

In our 2012 Mid-Year Securities Litigation Update, we highlighted the Second Circuit’s controversial decision in Panther Partners, Inc. v. Ikanos Comm’ns, Inc., which permitted a plaintiff’s claim under Section 11 and Section 12(a)(2) based on the defendant issuer’s alleged failure to comply with Item 303’s obligation to disclose “any known trends or uncertainties … that the registrant reasonably expects will have a material … unfavorable impact on … revenues or income from continuing operations.” Panther Partners, Inc. v. Ikanos Comm’ns, Inc., 681 F.3d 114, 120 (2d Cir. 2012) (quoting 17 C.F.R. § 229.303(a)(3)(ii)). As anticipated, several district courts have tackled Regulation S-K Item 303-related claims post-Panther Partners, and the general trend in the latter half of 2012 has been generally favorable to plaintiffs.

For example, a second decision from the McKenna v. Smart Technologies, Inc. litigation, highlighted in our 2012 Mid-Year Securities Litigation Update, offered further support for plaintiffs looking to expand potential liability using Item 303. See McKenna II, No. 11 Civ. 7673 (KBF), 2012 WL 3589655 (S.D.N.Y. Aug. 21, 2012). In the McKenna I decision, the court permitted Item 303-related claims to survive or provided for re-pleading as to when defendants knew about the “trend” at issue. See McKenna I, No. 11 Civ. 7673 (KBF), 2012 WL 1131935 (S.D.N.Y. Apr. 3, 2012). In analyzing the surviving and re-pleaded claims, the Court noted that evaluation of whether a “known trend or uncertainty” is presently known to management and reasonably likely to have a material impact on a company’s financial condition is not a mechanical evaluation, but rather turns on the “totality of the circumstances alleged.” McKenna II at *4-5. The court found that plaintiffs easily met the Fed. R. Civ. P. 8(a) pleading standard to survive the renewed motion to dismiss, especially where plaintiffs did not allege fraud (thus triggering the higher pleading standards of Fed. R. Civ. P. 9(b)).

Of particular note is the McKenna court’s rejection of the defendant’s cautionary language in its prospectus as too generic, despite the fact that the defendant specifically noted the “trend.” The plaintiffs alleged that the defendant knew or should have known that federal funding, which provided a significant market for the defendant’s core product, was drying up. The defendant’s prospectus specifically noted its customers’ dependence on federal funding, which, if declined, could cause a loss in revenue. But the court held that this statement did not directly address the risk: the defendant should have included a sentence that “there were uncertainties around whether-and to what extent-[federal] funding would continue at the levels it had in the past.” Id. at *6.

Defendants have, however, experienced some victories post-Panther Partners. The Southern District of New York, for example, found an issuer’s warning statement sufficient in another Item 303 case just a month after the McKenna II decision. The court in In re Proshares Trust Sec. Litig. granted defendants’ motion to dismiss, finding no material omission regarding an Item 303 disclosure because the defendants’ registration statements accurately conveyed the specific risk. No. 09 Civ. 6935 (JGK), 2012 WL 3878141, at *10 U.S. Dist. LEXIS 128542 (S.D.N.Y. Sep. 7, 2012). In this putative class action, the plaintiffs claimed that the defendants, investment companies that sold Exchange Traded Funds, had developed a mathematical formula that demonstrated a “must lose” risk scenario. After this scenario allegedly occurred, defendants changed their risk disclosure to include stronger language. But the court upheld the adequacy of the previous risk disclosure, noting that each registration statement warned that the investments were aggressive, speculative, based on single-day results only, and leveraged (which could create magnified losses). Further, the registration statements warned that investors could bet correctly on the direction of the underlying index but could still suffer double-digit losses if the investor held on to the shares too long. The court found that the precise risk that the plaintiffs identified as necessitating disclosure under Item 303 was directly disclosed. The court also found that a failure to predict future market performance is not a material omission. Id. The mathematical formula allegation was therefore implausible because it could not be known until after the underlying index had gained or lost.

Plaintiffs survived a motion to dismiss in another putative class action based on Item 303 disclosures in Underland v. Alter, No. 10-3621, 2012 WL 2912330 (E.D. Pa. July 16, 2012). The Underland court found that, among other things, the defendants failed to disclose a known trend or uncertainty under Item 303 and that the defendants’ general disclosure language was insufficient. The plaintiffs alleged that the defendants, who issued credit cards to small businesses, failed to disclose the re-pricing of 68% of their credit card holders (resulting in increased finance charge rates, etc.), which occurred without regard to customer credit histories. This re-pricing caused a significant increase in customer delinquencies and an accompanying loss in share value. The court found insufficient the defendants’ general disclosure language about monitoring credit quality, changing finance charges, etc., because the language contemplated only that something might happen. Here, the defendants actually had changed finance charges. The court also found that the defendants essentially admitted that re-pricing would materially impact its financials by providing the conditional (but insufficient) risk disclosure.

Finally, the Northern District of Georgia held that the plaintiffs sufficiently alleged that the defendant failed to disclose, under Item 303, that its growth trend was primarily through acquisition rather than organic. In re Ebix, Inc., Sec. Litig., No. 1:11-CV-02400-RWS, 2012 WL 4482798, at *16 (N.D. Ga. Sept. 28, 2012). While also finding sufficient allegations of scienter, recklessness, and other material misrepresentations, the court observed generally that defendants were “severely reckless in their representations about [their] organic growth rates.” See also In re Municipal Mortgage & Equity Sec. Litig., No. MJG-08-1961-MDL, 2012 WL 2450161 (D. Md. June 26, 2012) (denying a motion to dismiss predicated on Item 303 disclosures where plaintiffs adequately pleaded materially false statements or omissions).

Primary Liability After JANUS

As discussed previously in our 2012 Mid-Year Securities Litigation Update, the Supreme Court in Janus Capital Group Inc. v. First Derivative Traders held that an individual or corporation cannot be held primarily liable in a Rule10b-5(b) private securities action for “making” a misleading statement or omission unless the person or corporation had “ultimate authority” over the statement’s “content” and “whether and how to communicate it.” 131 S. Ct. 2296, 2307 (2011). The Court concluded that Janus Capital Management, an investment adviser, could not be held primarily liable for drafting allegedly misleading prospectuses issued by its mutual-fund client, the Janus Investment Fund. “One who prepares or publishes a statement on behalf of another,” wrote Justice Thomas, “is not its maker …. Even when a speechwriter drafts a speech, the content is entirely within the control of the person who delivers it.” Id. at 2302. (Gibson Dunn successfully represented Janus.) Since the Supreme Court’s decision, lower courts have worked to define the limits of the Janus holding.

Who “Made” the Allegedly False Statement?

Janus has forced lawyers and courts to think carefully about who specifically “made” the alleged misleading statement. District courts have split between applying the Janus limitation within a single company or entity, and applying it only between two different entities, one supplying information to the other.

One district court, for instance, held that a plaintiff could allege, consistent with Janus, a Section 10(b) claim based on false statements “published collectively by a group of equally authoritative individuals within an organization.” Touchstone Group, LLC v. Rink, No. 11-cv-02971, 2012 WL 6652850, at *10 (D. Colo. Dec. 21, 2012). Unlike Janus, in which one organization drafted a statement for another, there is no such hierarchy of “ultimate authority” when a “group-published statement” is offered by a corporation’s directors and officers. Id. Liable individuals included the CFO and Chief Legal Counsel, but not the Financial Controller, who only reported to the CFO. The contested statements appeared in the firm’s promotional materials and in a private placement memorandum. Id. at *8.

Similarly, a court refused to reverse a verdict against a defendant who claimed that a jury instruction was inconsistent with Janus. Sawant v. Ramsey, No. 07-cv-980, 2012 WL 3265020, at *14 (D. Conn. Aug. 9, 2012). The instruction indicated that an individual was a “maker” of a statement where he or she was “involved with the production or dissemination of the statement, such as through drafting, producing, reviewing, or assisting with the preparation of the statement.” Id. This accorded with Janus, replied the court, because Janus only concerned liability for statements by “secondary actors,” not statements by company executives in carrying out their responsibilities as corporate agents. Id. at *15.

On the other hand, other courts insist that theories of liability premised on treating corporate insiders collectively did not survive Janus. See, e.g., Ho v. Duoyuan Global Water, Inc., No. 10-cv-7233, 2012 WL 3647043, at *16 n. 13 (S.D.N.Y. Aug. 24, 2012); In re UBS AG Sec. Litig., No. 07-cv-11225, 2012 WL 4471265, at *10 (S.D.N.Y. Sept. 28, 2012). According to these courts, Janus allows an individual to be held liable only if he himself “made” the misstatement-and not upon a theory of “group pleading.” Id. The latter, wrote one court, allows a plaintiff to “circumvent the general pleading rule that fraudulent statements must be linked directly to the party accused of the fraudulent intent by allowing a court to presume that certain group-published documents [such as SEC filings and press releases] … are attributable to corporate insiders involved in the everyday affairs of the company.” In re UBS AG Sec. Litig., 2012 WL 4471265 at *9 (citations omitted).

What Constitutes “Making” a Statement?

Courts also have tackled what “making” a statement means. A court recently rejected a claim that a senior vice president, not alleged to have made any statements himself, nonetheless made “decisions” to “manipulate” his company’s “financial results” in ways that made misleading statements “inevitable.” Curry v. Hansen Med., Inc., No. 09-cv-5094, 2012 WL 3242447, at * 4 (N.D. Cal. Aug. 10, 2012). “[T]he lack of allegations that an individual was the maker of a statement,” wrote the court, “is fatal to a Rule 10b-5(b) claim against that individual.” Id. at *5. Another court found that a private suit could be brought against a corporate secretary who emailed an allegedly false statement directly to the plaintiff, but that no such action lay against the chief financial officer, who was alleged only to have “prepared” financial statements using “unsubstantiated” numbers. Red River Res., Inc. v. Mariner Sys., Inc., No. 11-cv-02589, 2012 WL 2507517, at *6 (D. Ariz. June 29, 2012). A third court, on a motion for reconsideration in light of Janus, reversed itself to hold that the company accounting director, who allegedly made improper accounting entries that led to false financial statements, was not liable: she herself did not “publish the press releases or file the financial statements,” but only “prepared” the documents. Louisiana Mun. Police Employees Ret. Sys. v. KPMG, LLP, No. 1:10-cv-1461, 2012 WL 3903335, at *2 (N.D. Ohio Aug. 31, 2012).

In Fulton County Employees Retirement System v. MGIC Inv. Corp. (discussed in our 2012 Mid-Year briefing), the Seventh Circuit relied on Janus to affirm the dismissal of Section 10(b) claims against a mortgage insurer named MGIC after it merely “invit[ed]” two executives from another company to speak on an earnings call. MGIC neither “made” the statements, said the court, nor had a “duty to correct” any supposed misstatements. 675 F.3d 1047, 1051-52 (7th Cir. 2012). The proposition that a defendant may not be held liable for failing to correct another’s misstatements was relied upon in part in In re Fannie Mae 2008 Sec. Litig., No. 08-cv-7831, 2012 WL 3758537, at *17 (S.D.N.Y. Aug. 30, 2012) (underwriter Goldman Sachs not liable for alleged Fannie Mae misstatements in part because it had “no freestanding duty to disclose”).

Janus, of course, does not serve as a defense for those who give their imprimatur to fraudulent statements. A court refused to dismiss a suit against a chief risk officer who made misstatements on conference calls and who, although he did not sign any SEC filings, possessed ultimate authority over them in drafting, reviewing, and approving them. In re Fannie Mae 2008 Sec. Litig., No. 08-cv-7831, 2012 WL 3758537, at *6 (S.D.N.Y. Aug. 30, 2012). See also In re Longtop Fin. Tech. Ltd. Sec. Litig., No. 11-cv-3658, 2012 WL 2512280, at *9 (S.D.N.Y. June 29, 2012) (“Palaschuk, the CFO, had authority over the content and delivery of his own oral and written statements” such as “signed press release commentary” and “conference call statements”). Signing a document generally equates to making the statements the document contains. In re Smith Barney Transfer Agent Litig., No. 05-cv7583, 2012 WL 3339098, at *9 (S.D.N.Y. Aug. 15, 2012) (“courts consistently hold that signatories of misleading documents ‘made’ the statements in those documents”); S.E.C. v. Brown, No. 09-cv-1423, 2012 WL 2927712 at *5 (D.D.C. July 19, 2012) (same).

Of special significance is a holding that a statement can still be “made” under Rule 10b-5(b) when it is not given directly to the investing public by the defendant-speaker but is nevertheless relayed to investors by third parties. See S.E.C. v. Daifotis, 874 F. Supp. 2d 870, 879 (N.D. Cal. 2012). The Daifotis court ruled that a Charles Schwab Corporation chief investment officer was not liable for comments made to other Schwab employees during an internal company call-but that liability could very well attach when those employees then repeated his remarks to their clients among the investing public. The court explained that “in the wake of Janus, an executive who undisputably [sic] exercised authority over his own non-casual statements with the intent and reasonable expectation that such statement would be relayed to the investing public, should be deemed to be the person who ‘made’ the statements to the investing public.” Id. at 88

Post-Janus Claims Against Auditors, Underwriters, and Other Third Parties

Courts continue to seize on Janus to forestall private securities litigation against third parties connected in some way to the production of a supposedly misleading statement. One court rejected a claim against an outside accountant in part because its allegedly false letters were not its “audited or certified statements” and thus not “attributable” to them. Krasner v. Rahfco Funds LP, No. 11-cv-4092, 2012 WL 4069300, at *7 (S.D.N.Y. Aug. 9, 2012). A court refused to permit a suit against an external auditor that exercised control over local affiliates-who performed the actual auditing-merely because the auditor had “power to sanction” the affiliates for failing to adhere to its standards. Ho v. Duoyuan Global Water, Inc., No. 10-cv-7233, 2012 WL 3647043, at *20 (S.D.N.Y. Aug. 24, 2012). The plaintiffs claimed that this parent-affiliate relationship established that the defendant parent company exercised “control over what information was released in the audits,” but in the court’s view this “sanctioning power” did not equate “to making the statements in the audits.” Id.

At the same time, however, courts allow Rule 10b-5(b) actions to proceed against underwriters for public offerings when the underwriter’s participation was “instrumental” enough to permit the inference that it was “specially designated” to speak for the issuer, that the statements were a “shared product” of the underwriter and issuer, or that the underwriter itself “issued” or “made” the statement. See Scott v. ZST Digital Networks, Inc., No. 11-cv-03531, 2012 WL 4459572, at *11-12 (C.D. Cal. Aug. 7, 2012) (citing In re Allstate Life Ins. Co. Litig., 2012 WL 176497, at *5 (D. Ariz. Jan. 23, 2012) and In re National Century Fin. Enterprises, Inc., 846 F.Supp.2d 828, 861 (S.D. Ohio 2012)). The Scott court found it significant that the underwriter’s name was “featured prominently on the offering documents.” Id. at *12.

A court also found that an attorney “made” a statement when he drafted letters for a company on his own letterhead, identified them as his legal opinions, signed them, and forwarded them to his client, fully aware that they would be posted by the company on an online database. S.E.C. v. Merkin, No. 11-cv-23585, 2012 WL 5245561, at *7 (S.D. Fla. Oct. 3, 2012).

Janus’ Application Beyond Private Rule 10b-5(b) Actions

Janus only explicitly purported to limit private causes of action-the “narrow scope” that such judicially implied claims receive drove the decision, 131 S. Ct. 2296, 2303-and did not explicitly purport to limit actions brought by the SEC. At least one court has suggested that the holding of Janus never applies to the SEC. S.E.C. v. Pentagon Capital Mgmt. PLC, 844 F. Supp. 2d 377, 421-22 (S.D.N.Y. 2012), as amended (Aug. 22, 2012) (stating that the Supreme Court limited its holding in Janus to “‘accord [ ] with the narrow scope” of Rule 10b-5 as applied to private plaintiffs in contrast to the Commission, and that “[t]here is no indication that the Court or Congress intended for actions brought by the SEC to be so limited”). Yet the majority of courts, without much discussion, apply Janus to SEC actions. See, e.g., S.E.C. v. C.J.’s Fin., No. 10-cv-13083, 2012 WL 3600239, at *6 (E.D. Mich. July 30, 2012), report and recommendation adopted, S.E.C. v. C.J.’s Fin., No. 10-cv-13083, 2012 WL 3597644 (E.D. Mich. Aug. 21, 2012). And the SEC itself apparently concedes that its suits under Rule 10b-5(b) are governed by Janus. See, e.g., S.E.C. v. Brown, No. 09-cv-1423, 2012 WL 2927712, at *11 (D.D.C. July 19, 2012) (SEC concedes that after Janus a claim against an officer who only “prepared” documents cannot rest on Rule 10b-5(b)). Other courts consider the question open. S.E.C. v. True N. Fin. Corp., No. 10-cv-3995, 2012 WL 5471063, at *38 (D. Minn. Nov. 9, 2012) (noting division among district courts as to “whether Janus applies to a public securities fraud action”).

The trend in the last six months seems to be toward a rule that Janus applies to SEC actions under Rule 10b-5(b), but not (as some defendants claim) to SEC actions under Rules 10b-5(a) and (c), which do not require a defendant to “make” any untrue statement. S.E.C. v. Sells, No. 11-cv-4941, 2012 WL 3242551, at *7 (N.D. Cal. Aug. 10, 2012) (Janus “did not address” Rules 10b-5(a) and (c)). Nor has Janus been applied to SEC actions under Section 17(a), which does not provide a private cause of action. See, e.g., Sells, 2012 WL 3242551, at *7 (Janus does “not apply to claims premised on § 17(a)”); S.E.C. v. Daifotis, 874 F. Supp. 2d 870, 878 (N.D. Cal. 2012) (“Janus only applies to Section 10(b) and Rule 10b-5″). Courts generally point to the different language in Sections 10(b) and 17(a). In S.E.C. v. Stoker, 865 F. Supp. 2d 457, 465 (S.D.N.Y. 2012), the court observed that Section 17(a) prohibits a defendant from obtaining money “by means of” an untrue statement, which “plainly covers a broader range of activity” than Section 10(b), which only enjoins a defendant from “making” false statements. See also S.E.C. v. Sentinel Management Group, Inc., No. 07-cv-4684, 2012 WL 1079961, at *15 (N.D. Ill. Mar. 30, 2012) (Janus is inapplicable to Section 17(a) claims for both textual and policy reasons); S.E.C. v. Big Apple Consulting USA, Inc., No. 09-cv-1963, 2012 WL 3264512, at *3 (M.D. Fla. Aug. 9, 2012) (Janus does not apply to Section 17(a) because Janus interpreted the “to make” language that only appears in 10(b)).

Federal district courts also have rejected arguments that Janus serves as a limit or defense to actions based on common-law fraud; usually the courts reason that Janus turned largely on the Supreme Court’s concern about the judicial expansion of implied private securities actions. See, e.g., Fed. Hous. Fin. Agency v. Goldman, Sachs & Co., No. 11-civ-6198, 2012 WL 5494923, at *3 (S.D.N.Y. Nov. 12, 2012) (Janus “emphasized repeatedly that its decision was compelled, in part, by ‘[c]oncerns with the judicial creation of a private cause of action'”); Louisiana Mun. Police Employees Ret. Sys. v. KPMG, LLP, No. 1:10-cv-01461, 2012 WL 3903335, at *3 (N.D. Ohio Aug. 31, 2012) (“the Janus Court made clear it was maintaining the ‘narrow scope’ of private rights of action”).

Extraterritorial Application of the Securities Laws After Morrison

Litigants and courts continue to define the extra-territorial securities litigation landscape following the Supreme Court’s decision in Morrison v. National Australia Bank, 561 U.S. ___, 130 S. Ct. 2869 (2010). As also discussed in our 2012 Mid-Year Securities Litigation Update, in Morrison, foreign citizens sued a foreign issuer in the United States for alleged fraud under Section 10(b) in connection with securities transactions in a foreign country. The Court affirmed dismissal of the lawsuit on the ground that Section 10(b) does not apply extraterritorially. The Court held that the statute applies only to “the purchase or sale of a security listed on an American stock exchange, and the purchase or sale of any other security in the United States.” Id. at 2888; see also id. at 2886 (describing the “transactional test” as “whether the purchase or sale is made in the United States, or involves a security listed on a domestic exchange”). Perhaps not surprisingly, plaintiffs began turning to state courts to avoid dismissal in federal court under Morrison.

Two New York state court decisions highlight the trend. In Basis Yield Alpha Fund, a New York Supreme Court justice refused to dismiss a fraud claim brought against Goldman Sachs by an Australian hedge fund. See Basis Yield Alpha Fund v. Goldman Sachs Group, Inc., 37 Misc. 3d 1212(A) (N.Y. Sup. Ct. 2012). The case was originally filed in federal district court the same month the Supreme Court decided Morrison. See Basis Yield Alpha Fund, 37 Misc. 3d 1212(A), at *4. The federal court quickly dismissed the suit following the Morrison decision, and plaintiffs filed a parallel case in state court alleging state law claims. See Basis Yield Alpha Fund v. Goldman Sachs Group, Inc., No. 652996/2011 (Oct. 19, 2012) (acknowledging that the S.D.N.Y dismissed the same case “on the ground that the underlying transactions were not domestic securities transactions, and, therefore, not subject to federal securities laws”). The state law claims included a variety of common law claims. While the court granted defendants’ motion to dismiss on some of those claims, it denied the motion with respect to most of plaintiffs’ claims. Id. at 19.

In Viking Global Equities, LP v. Porsche Automobil Holding SE, No. 650432/11, 2012 WL 6699216 (N.Y. App. Div. Dec. 27, 2012), plaintiff hedge funds allegedly sustained losses as a result of misrepresentations made by Porsche relating to its intention to acquire shares in Volkswagen AG. Although plaintiffs initially survived a motion for summary judgment, the victory was short-lived. In December 2012, only a month after argument on Porsche’s appeal, New York’s Appellate Division, First Department reversed the trial court, holding-in an opinion only two paragraphs long-that the plaintiffs were barred on the ground of forum non conveniens. Id.

Federal courts applying Morrison have grappled with what constitutes a “domestic transaction” in securities not listed on a U.S. stock exchange. In our 2012 Mid-Year Securities Litigation Update, we discussed the Second Circuit’s resolution of this question in Absolute Activist Value Master Fund Ltd. v. Ficeto, 677 F.3d 60 (2d Cir. 2012). There, the Second Circuit held that “to sufficiently allege a domestic securities transaction in securities not listed on a domestic exchange,” a plaintiff must “allege facts suggesting that irrevocable liability was incurred or title transferred within the United States.” Id. at 68. The court noted that its test combines the “title transfer” test adopted by the Eleventh Circuit in Quail Cruises and the “irrevocable liability” test employed by district courts within the Second Circuit. Id. During the second half of 2012, district courts within and outside the Second Circuit have begun to apply the Absolute Activist test.

For example, the court in Bayerische Landesbank v. Barclays Capital, Inc., denied a motion to dismiss, finding the plaintiffs made “at least a plausible showing that [the notes at issue] were purchased by the New York branch,” which satisfied the issue of whether “irrevocable liability was incurred or title was transferred within the United States” sufficiently to survive a motion to dismiss. 2012 WL 5383572, at *1 (S.D.N.Y Nov. 5, 2012) (quoting Absolute Activist). Several months earlier, the same judge dismissed the claim in Pope Investments II, LLC v. Deheng Law Firm, finding plaintiffs’ allegations that they “drafted the Securities Purchase Agreement, presumably in China” without “alleg[ing] where that agreement was negotiated or signed” were insufficient to avoid dismissal. 2012 WL 3526621, at *6-7 (S.D.N.Y. Aug. 15, 2012) (citing Absolute Activist). Similarly, in MVP Asset Mmgt. (USA) LLC v. Vestbirk, the court dismissed plaintiffs’ claims “that certain funds were transferred in between New York-based banking institutions,” finding them “insufficient to establish the existence of a domestic transaction,” citing Absolute Activist. 2012 WL 2873371 (E.D. Cal. July 12, 2012).

Pleading and Proving “Scienter” or State of Mind

Despite the low dismissal rates of private securities actions discussed above, federal circuits continue generally to affirm trial courts when those courts do in fact dismiss a claim. Perhaps in one context in which the PSLRA has achieved its intended bite, federal circuits emphasize the exacting pleading standard, which obligates plaintiffs to “state with particularity facts giving rise to a strong inference that the defendant acted with the required state of mind,”a standard enacted to “to curb frivolous, lawyer-driven litigation, while preserving investors’ ability to recover on meritorious claims.” Tellabs, Inc. v. Makor Issues & Rights, Ltd., 551 U.S. 308, 314, 322 (2007).

For example, in In re Boston Scientific Corp. Sec. Litig., the First Circuit affirmed the dismissal of a Section 10(b) putative class action against a medical-supply company whose CEO, on a conference call, spoke “blandly but favorably” about its cardiac-device sales team, without disclosing that ten salespeople had been fired for ethical violations and at least some re-hired by a competitor. 686 F.3d 21, 30-31 (1st Cir. 2012). The court declared that this omitted information was “at best marginally material”-among other things, the ten salespeople constituted less than a percent of the company’s device sales force and the loss attributable to their termination was also about 1%. The marginal materiality “not only defeats any independent inference of deliberate withholding but also makes the pled facts insufficient for a fact finder to find the ‘extreme recklessness in not disclosing the fact’ that is the least that is required to establish scienter.” Id. at 31. The court emphasized that the PSLRA’s heightened pleading standards were “aimed at permitting early termination-before discovery-of such ‘routine filings’ of unpromising cases.” Id. at 30.

In In re Rigel Pharmaceuticals, Inc. Sec. Litig., the Ninth Circuit affirmed the dismissal of a Section 10(b) claim that alleged false statements by a drug developer about the efficacy and safety of an arthritis drug. 697 F.3d 869 (9th Cir. 2012). The plaintiffs did not adequately plead scienter because they failed to show that the defendant-doctors believed they were making false or misleading statements; rather, the plaintiffs’ allegations amounted merely to a suggestion that the defendant-doctors chose not to relate particular information that, in the doctors’ view, was not medically of concern. Nor did it “make sense” that defendants-intent on overstating a drug’s safety-would “choose to disclose” the most severe adverse events. Id. at 884. The plaintiffs claimed that defendants’ “motive” in seeking business partners and capital supported an inference of scienter, but the court disagreed. “[A]llegations of routine corporate objectives such as the desire to obtain good financing and expand are not, without more, sufficient to allege scienter; to hold otherwise would support a finding of scienter for any company that seeks to enhance its business prospects.” Id. at 884. Finally, none of the defendants sold stock between the time of the alleged misstatements and the public disclosure of the clinical data-the period when they might have benefitted-undercutting any inference of fraud. Their non-sale, in fact, “supports the opposite inference.” Id. at 885.

In Pipefitters Local No. 636 Defined Benefit Plan v. Zale Corp, the Fifth Circuit affirmed the dismissal of a Section 10(b) suit alleging accounting improprieties and misstatements. No. 11-10936-cv, 2012 WL 5985075 (5th Cir. Nov. 30, 2012). The plaintiffs asserted that the Zale Corporation was at a minimum severely reckless in releasing allegedly suspicious accounting figures produced by a marketing vice-president, but the court declined to “generally consider it to be ‘severely reckless'” for a company to “rely” on its own executives to provide numbers and follow company rules. Id. at *5. Moreover, even though Zale later conceded that it violated its own accounting policies, this itself did not show that the officers responsible for Zale’s public financial statements “knew about the inaccurate information or recklessly ignored evidence of its falsity.” Id. Finally, broad statements about “financial rigor” by Zale officers suggested only that the company valued thriftiness, not that it “intended to double-check accounting figures submitted by high-level executives.” Id. The vice-president likely acted with intent to “maintain the good appearance of her department rather than to defraud investors.” Id.

In Meridian Horizon Fund, LP v. KPMG (Cayman), the Second Circuit affirmed the dismissal of a suit claiming that auditors ignored the “red flags” of the Madoff fraud. No. 11-3311-cv, 2012 WL 2754933 (2d Cir. July 10, 2012). The court held that for a plaintiff to plead that a non-fiduciary accountant was so reckless as to properly allege the securities-fraud scienter, it must present “conduct that is highly unreasonable, representing an extreme departure from the standards of ordinary care,” such that it “approximate[s] an actual intent to aid in the fraud being perpetrated by the audited company.” Id. at *3 (citations omitted). Here, however, blame lay not with allegedly reckless auditors but with Madoff himself and his “proficiency in covering up his scheme.” Id. (citations omitted). The court, like others in recent months, reminded plaintiffs that a “strong inference” must be more than “merely plausible or reasonable-it must be cogent and at least as compelling as any opposing inference of nonfraudulent intent.” Id. at *2 (citations omitted). Here, the plaintiffs presented an “archetypical example of impermissible allegations of fraud by hindsight.” Id. at *3 (citations omitted).

Yet failing to act on glaring, tell-tale warning signs provided the basis for the Second Circuit’s affirmance of a jury verdict against an ex-Adelphi chief accounting officer. S.E.C. v. Delphi Corp., No. 11-2624, 2012 WL 6600324, at *6-7 (6th Cir. Dec. 18, 2012). He ignored “multiple red flags” with regard to two dubious transactions and then failed “personally” to conduct a “critical investigation” or to “personally undertake a more searching inquiry.” Id. This, said the court, was sufficient to allow a jury inference that he may have been “willfully blind, or reckless” and so possessed the culpable fraud scienter. Id.

In Boca Raton Firefighters & Police Pension Fund v. Bahash, the Second Circuit affirmed the dismissal of a putative Section 10(b) class action that alleged that statements by McGraw-Hill executives about the operation of Standard & Poor’s Rating Services amounted to fraud. No. 12-1776-cv, 2012 WL 6621391 (2d Cir. Dec. 20, 2012). The court reiterated that things like remarks in the nature of puffery, generalizations about company practice, “mere” instances of corporate mismanagement, expressions of general optimism about future profits, or failure to demonstrate “prescience,” are all beyond the ambit of Section 10(b)’s fraud provisions. Id. at *3-6. The Second Circuit rejected plaintiffs’ claim that statements about S&P’s “integrity” and “credibility” were not puffery because they were specifically directed at the agency. The word “puffery,” said the court, “stems from the generic, indefinite nature of the statements at issue, not their scope.” Id. at *4. Finally, the court, in a common bench criticism, explained that plaintiffs alleging fraud must explain how specific allegations of fact support their claim, whereas in that case the sprawling 280-page, quotation-stuffed complaint left the trial court to work it out “on its own initiative.” Id. at *5.

For an exception to the trend of appellate courts affirming dismissals for failure to adequately plead scienter, see In re VeriFone Holdings, Inc. Sec. Litig., No. 11-15860-cv, 2012 WL 6634351 (9th Cir. Dec.21, 2012) (reversing dismissal of securities fraud class action, finding that plaintiffs’ allegations demonstrated an “overwhelming inference” of probable intent to defraud sufficient to survive a motion to dismiss).

Class Certification

Fraud-on-the-Market: The Market Efficiency Standard

Several cases decided in the last six months have addressed the market-efficiency element of the fraud-on-the-market presumption. As discussed in Basic v. Levinson, the market for a stock is presumed efficient if the market price for the stock reflects or incorporates, in a timely fashion, any material, unexpected information. 485 U.S. 224 (1988) (citing Lipton v. Documation, Inc., 734 F.2d 740, 748 (11th Cir. 1984), cert. denied, 469 U.S. 1132 (1985)).

Recent court decisions applied the Cammer factors (discussed in our 2010 Year-End and 2011 Mid-Year Securities Litigation Updates) to find that the New York Stock Exchange operated as an efficient market for the respective stock at issue. In re Computer Sciences Corp. Sec. Litig., No. 1:11cv610, 2012 WL 6651971 (E.D. Va. Dec. 19, 2012); In re Merck & Co., Inc., Vytorin/Zetia Sec. Litig., No. 08-2177, 2012 WL 4482041 (D.N.J. Sept. 25, 2012); Vinh Nguyen v. Radient Pharmaceuuticals Corp., No. SA CV 11-0406, 2012 WL 5947028 (C.D. Cal. Nov. 26, 2012). In Merck, the court noted that “securities traded on the NYSE are routinely recognized as trading in an efficient market,” and, though trading on the NYSE is not a per se indicator of market efficiency, the Cammer analysis usually will demonstrate that the NYSE is an efficient market for a particular stock. Id. at *5.

The defendants in In re Computer Sciences Corp. Sec. Litig. argued that the NYSE was not an efficient market for its stock. No. 1:11CV610-TSE-IDD, 2012 WL 6651971, at *3 (E.D. Va. Dec. 19, 2012). They alleged that the plaintiffs did not meet their burden to establish market efficiency because they did not provide an event study showing that the allegedly false statements caused an upward movement in the price of the stock. The court held that the preponderance of the evidence standard for proving market efficiency does not require use of an event study. Id. at *6.

The defendants further relied on Gariety v. Grant Thornton, LLP, 368 F.3d 356 (4th Cir. 2004) and In re Federal Home Loan Mortgage Corp (Freddie Mac) Sec. Litig., 281 F.R.D. 174 (S.D.N.Y. 2012) to support their claim that the NYSE was not an efficient market. In Gariety, the Fourth Circuit cited the Cammer factors, one of which states that “a cause and effect relationship between unexpected corporate events or financial releases and an immediate response in the stock price” is the essence of an efficient market. Gariety, 368 F.3d at 368 (citing Cammer v. Bloom, 711 F. Supp. 1264, 1285-87 (D.N.J. 1989)). The defendants in Computer Sciences argued that the Fourth Circuit viewed the cause and effect relationship as the most important element in demonstrating market efficiency. The court disagreed, stating that Gariety merely cited the Cammer factors as elements to be considered and did not require the use of event studies to demonstrate a causal relationship. The defendants also relied on Freddie Mac, which held that plaintiffs failed to show a causal relationship and therefore could not rely on the fraud-on-the-market theory. Freddie Mac, 281 F.R.D. at 182. The Computer Sciences court distinguished Freddie Mac because the stock involved in Freddie Mac was “a limited series of preferred shares, which traded in patterns significantly different from the trading patterns typical of common shares.” Computer Sciences, 2012 WL 6651971, at *7. The court observed that “[i]t is not surprising that no other federal courts have concluded that common shares traded on the NYSE are not traded in an efficient market.” Id.

Addressing the fraud-on-the-market presumption, the court in City of Livonia Employees’ Ret. Sys. v. Wyeth held that, in a case involving a material omission, the impact of the misrepresentation should be measured by the stock price reaction following the corrective disclosure. 284 F.R.D. 173, 182 (S.D.N.Y. 2012). In City of Livonia, a local union pension fund brought a class action against Wyeth, alleging that Wyeth defrauded the purchasers of its common stock by making materially false misstatements and omissions related to the safety of a drug that it was marketing. Wyeth challenged class certification, arguing that plaintiffs failed to meet the predominance requirement of Rule 23(b) because Wyeth rebutted the “fraud-on-the-market” presumption under Basic v. Levinson by showing that there was no statistically significant price impact on the dates of the alleged misrepresentations and omissions. The court disagreed and held that, in a case concerning omissions, the failure of the stock price to significantly increase on the date of the omissions is not dispositive. Id. Misstatements may cause inflation “simply by maintaining existing market expectations,” and therefore the impact of Wyeth’s misrepresentation should be measured after the truth was disclosed to the market, rather than on the date the omission was made. Id. at 182.

Wyeth also claimed that the lead plaintiff was an inadequate class representative because it purchased some of its stock after Wyeth’s disclosures, and because there was a monitoring agreement between the lead plaintiff and lead counsel. The court rejected these arguments, explaining that “[t]he post-disclosure purchase of the additional shares . . . will not necessarily present individual issues of reliance that render the investor atypical or inadequate to represent the class members who did not purchase such additional shares.” Id. at 178. Additionally, the court recognized that courts routinely appoint institutional investors with monitoring agreements as lead plaintiffs and class representatives, and that the existence of a monitoring agreement is not disqualifying. Id. at 180.

According to the Second Circuit, plaintiffs seeking certification of a settlement class need not demonstrate that the fraud-on-the-market presumption applies. In In re Am. Int’l Group, Inc. Sec. Litig., 689 F.3d 229 (2d Cir. 2012), the court heard a rare joint appeal from the district court’s order denying plaintiffs’ motion to certify a settlement class. The district court held that the class could not satisfy the predominance requirement of Rule 23(b)(3) because, under Stoneridge Investment Partners, LLC v. Scientific-Atlanta, Inc., 552 U.S. 148 (2008), the fraud-on-the-market presumption does not apply to a defendant whose deceptive acts were not communicated to the public. Because the lead plaintiffs could not establish that the defendants made any public misstatement or omission, the district court held that the fraud-on-the-market presumption was not satisfied and individual issues of reliance predominated over common issues. On appeal, the Second Circuit held that, under Amchem Products, Inc. v. Windsor, 521 U.S. 591, 620 (1997), a securities fraud class’s failure to satisfy the fraud-on-the-market presumption primarily threatens class certification by creating “intractable management problems” at trial. Am. Int’l Group, 689 F.3d at 232. “Because settlement eliminates the need for trial, a settlement class ordinarily need not demonstrate that the fraud-on-the-market presumption applies to its claims in order to satisfy the predominance requirement.” Id.

The Predominance Requirement After N.J. Carpenters Health Fund v. RALI

In our 2012 Mid-Year Securities Litigation Update, we discussed the Second Circuit’s decision in N.J. Carpenters Health Fund v. RALI Series 2006-Q01, 477 Fed. App’x 809 (2d Cir. 2012), affirming the denial of class certification because common issues did not predominate with respect to whether class members knew of the alleged untruth or omission at the time of their respective securities purchases. After the Second Circuit denied class certification, the plaintiffs submitted an amended motion to the district court attempting to narrow the class. N.J. Carpenters Health Fund v. Residential Capital, LLC, No. 08 CV 8781, 2012 WL 4865174, at *1 (S.D.N.Y. Oct. 15, 2012). The defendants again opposed the motion for class certification on the ground that the Rule 23(b)(3) predominance requirements were not satisfied, arguing that various class members had different levels of knowledge about the defendants’ practices. The district court granted in part the amended motion for class certification, finding that the expanded record presented by the plaintiffs demonstrated that “even the most sophisticated class members” did not have access to all of the relevant information and that the class members were therefore likely to have been subject to the same knowledge defense. Id. at *3. While the court found that the defendants’ affirmative defenses were not so individualized as to preclude class certification, it exercised its discretion to certify a narrower class of purchasers than the plaintiffs had requested. Id. at *4.

The defendants in In re IndyMac Mortgage-Backed Sec. Litig., No. 09 Civ. 4583, 2012 WL 3553083 (S.D.N.Y. Aug. 17, 2012) and Katz v. China Century Dragon Media, Inc., No. LA CV11-02769, 2012 WL 6644353 (C.D. Cal. Dec. 18, 2012) both relied on the earlier N.J. Carpenters decision upheld by the Second Circuit to argue that common issues did not predominate in their respective cases. In IndyMac, the defendants claimed that individualized questions predominated over common ones under Rule 23(b)(3) under N.J. Carpenters‘s holding that the inference of disparities in knowledge within the two proposed classes was enough to defeat predominance. See New Jersey Carpenters Health Fund v. Residential Capital, LLC, 272 F.R.D. 160, 169-70 (S.D.N.Y. 2011). The IndyMac defendants argued that the plaintiffs likely already knew of the allegedly misleading nature of the offering documents because the class consisted of many sophisticated or institutional investors and many had the benefit of investment advisors. The court rejected this, holding that “[i]nvestor sophistication does not alone defeat a finding of predominance in a class action” and demonstrating that certain class members were sophisticated investors does not establish that any prospective class member knew or had notice that the offering documents contained misstatements or omissions. IndyMac, 2012 WL 3553083, at *7. The court distinguished N.J. Carpenters because, in IndyMac, there were no specific statements by class members demonstrating individual knowledge of misstatements.

Similarly, in Katz, the court refused to apply N.J. Carpenters because the defendant (a Chinese company) did not show that those who purchased its shares had special access to information or special experience in connection with the purchase of securities from Chinese companies. Further, “almost all of the evidence submitted as to knowledge concerned disclosures prior to the commencement of the class period.” Thus, the defendant did not show a need for individualized assessments of class members with respect to the knowledge defense. Katz, 2012 WL 6644353, at *14.

In another predominance case under Rule 23(b)(3), the Eighth Circuit upheld the district court’s denial of class certification, holding that churning and unauthorized trading are both highly individualized claims that do not satisfy the uniformity requirements of Rule 23(b)(3). McCrary v. Stifel, Nicolaus & Co., Inc., 687 F.3d 1052, 1059 (8th Cir. 2012). McCrary filed an action in Missouri state court against a brokerage and investment banking firm alleging violations of Missouri securities law. The defendant removed the case to federal court, where the district court found that the plaintiffs’ claims were ineligible for class treatment because of the individualized nature of the churning, unauthorized trading, and misrepresentation claims. The plaintiffs appealed, asserting that such class certification issues can only be addressed after a Rule 12(b)(6) analysis of plaintiffs’ individual claims. The court disagreed, stating that a court is not required to analyze the appropriateness of class treatment only after the merits of the individual claims have been examined. The court affirmed the district court’s denial of class certification because churning and unauthorized trading are both “highly individualized claims that do not satisfy the uniformity requirements of Rule 23(b)(3).” Id. at 1059. Further, McCrary did not allege any materially uniform omissions or misrepresentations that were made to all members of the class. Id.

Loss Causation

Several courts rejected claims on loss-causation grounds in the second half of 2012, either finding no corrective disclosure or finding the relationship between the disclosure and the loss too tenuous.

In an unpublished opinion, the Eleventh Circuit affirmed the district court’s grant of summary judgment, holding that the plaintiffs failed to eliminate alternative explanations for the drop in the defendant’s share price, and therefore had not established loss causation. Phillips v. Scientific-Atlanta, No. 10-15910, 2012 WL 3854795, at *4 (11th Cir. Sept. 6, 2012) (per curiam). The defendant, a cable set-top manufacturer, allegedly engaged in “channel-stuffing” to hide decreasing sales. The defendant’s earnings reports attributed the declining sales to market uncertainties. In a conference call, though, the defendant’s CEO attributed part of the announced decline in new orders to the absorption of inventory by purchasers. A month later, the defendant’s CFO stated in a press release that sales had declined as a result of the slowing market and “a correction in customer inventory levels.” Id. at *2. After these revelations, the defendant’s stock price fell steeply. The court determined that the plaintiffs failed to establish loss causation, because they had not determined how much of the defendant’s depressed share price was specifically linked to the alleged “channel-stuffing” and how much was linked to the company’s statements that the market had slowed down. Id. at *3-4. Although the plaintiffs’ expert concluded that industry factors alone could not explain the share price, “he did not disaggregate (and made no attempt to disaggregate) the impact of Defendants’ statements that accurately presented the industry-wide factors” that had affected the defendants. Id. at *4. Because the plaintiffs had not disaggregated this external factor, “no basis exist[ed] in the record by which any fact-finder could sufficiently determine that the revelation of the supposed ‘channel stuffing’ in this case satisfied the pertinent causation requirement.” Id.

As we discussed in our 2012 Mid-Year Securities Litigation Update, several for-profit colleges successfully moved to dismiss securities class actions in the beginning of 2012, based on plaintiffs’ failure to adequately plead loss causation. The plaintiffs in one of these cases, Kinnett v. Strayer Educ., Inc., No. 12-12196, 2012 WL 6571112 (11th Cir. Dec. 13, 2012), appealed the dismissal to the Eleventh Circuit. The plaintiffs argued that Strayer’s fraud concerning its recruitment and enrollment practices caused new student enrollments to decrease by 20%, which lowered the stock price. The plaintiffs relied on statements made by Strayer’s CEO in a conference call with investors, which plaintiffs alleged constituted an admission that Strayer had engaged in improper recruiting to the detriment of its stock prices. The Eleventh Circuit agreed with the district court’s finding that these statements did not constitute an admission that Strayer had engaged in improper recruitment practices. The plaintiffs argued that the CEO’s statements were at least ambiguous, and that the ambiguity should be resolved in favor of the plaintiff. But the court explained that a complaint must allege “something beyond the mere possibility of loss causation,” and that “unwarranted deductions of fact are not admitted as true in a motion to dismiss.” Id. at *3. The court held that it was not reasonable to infer that the statements had been an admission by Strayer that it had engaged in improper recruiting practices. As a result, the plaintiff had not shown any corrective disclosures by Strayer and had therefore failed to adequately plead loss causation. Id.

Also in our 2012 Mid-Year Update, we discussed the Second Circuit’s opinion in Acticon AG v. China Northeast Petroleum Holdings Ltd., 692 F.3d 34 (2d Cir. Aug. 1, 2012). Rejecting the view taken by many district courts, the Second Circuit held that a securities plaintiff may still have suffered a loss even if the company’s stock price later rises above the plaintiff’s original purchase price. Id. at 40-41. The Second Circuit noted that its holding was consistent with the “traditional out-of-pocket measure of damages, which calculates economic loss based on the value of the security at the time that the fraud became known, and with the PSLRA’s bounce-back provision, which refines the traditional measure by capping recovery based on the mean price over the look-back period.” Id.

No subsequent district court decisions have thoroughly examined the Acticon holding, but in George v. China Automotive Sys., Inc., the Southern District of New York cited to Acticon in holding that “recovery of stock price subsequent to the class period ‘does not negate the inference that [the plaintiff] has suffered economic loss.'” No. 11 Civ. 7533, 2012 WL 3205062, at *12 (S.D.N.Y. Aug. 8, 2012) (quoting Acticon, 692 F.3d at 41). In George, the defendants argued that the plaintiffs could not show loss causation because the stock price rose following the defendants’ disclosure. The court held that this argument was foreclosed by Acticon and denied the motion to dismiss. Id.

In Kuriakose v. Fed. Home Loan Mortg. Corp., the court found no corrective disclosure because all of the relevant information was already known to investors. No. 08 Civ. 7281, 2012 WL 4364344, at *5 (S.D.N.Y. Sept. 24, 2012). The investors brought a class action against Freddie Mac and its former officers, alleging that they bought shares at inflated prices based on Freddie Mac’s misrepresentations about its exposure to subprime mortgage products and the sufficiency of its capital. The court previously dismissed the plaintiffs’ first amended complaint for failure to “plausibly allege[] that [Freddie Mac’s] misrepresentations proximately caused them economic harm.” Kuriakose v. Fed. Home Loan Mortg. Corp., No. 08 Civ. 7281, 2011 WL 1158028, at *14 (S.D.N.Y. Mar. 30, 2011). The plaintiffs’ second amended complaint set forth a series of “partial disclosures” made by Freddie Mac that allegedly constituted corrective disclosures about its alleged misrepresented capital adequacy. Kuriakose, 2012 WL 4364344, at *5. But the court found that none of these disclosures revealed anything about the alleged scheme underlying the lawsuit. Rather, they simply indicated that Freddie Mac was in a precarious financial position and synthesized information that was already known to investors. Because all relevant information had already been revealed, the disclosures could not be “corrective” and could not have caused the plaintiffs’ losses. Id.

In Prime Mover Capital Partners L.P. v. Elixir Gaming Technologies, Inc., the court found that the plaintiffs had not sufficiently pleaded either a corrective disclosure or a materialization of a concealed risk, and therefore they could not establish loss causation. 10 Civ. 2737, 2012 WL 4714799, at *7 (S.D.N.Y. Sept. 27, 2012). Defendant Elixir Gaming Technologies (“EGT”) allegedly made several false and misleading statements, including an assertion that it expected electronic gaming machines placed in Asian gaming venues to generate a profit, or “net win,” of $125 per day per machine. EGT later disclosed additional information indicating that this net win figure assumed a twelve-month prior operating history, and did not represent the daily net win over the first year of operation. The plaintiffs claimed that this disclosure “marked the beginning of the materialization of the risks.” Id. at *6. The court disagreed, finding that none of the risks was concealed by the alleged inaccuracy of the $125 net-win figure. Instead, the statements were forward-looking and “repeatedly warned of risks that projections-including the $125 net-win rate-would not be met.” Id. at *7. Plaintiffs also failed to plead that corrective disclosures caused a stock price decline by not adequately alleging that the truth about the alleged misstatements was ever revealed to the public.

In Plumbers, Pipefitters & MES Local Union No. 392 Pension Fund v. Fairfax Fin. Holdings Ltd., the plaintiff argued that a series of five press releases detailing an SEC investigation against Fairfax constituted corrective disclosures about Fairfax’s alleged improper accounting schemes. No. 11 Civ. 5097, 2012 WL 3283481, at *7 (S.D.N.Y. Aug. 13, 2012). Because Fairfax’s share price declined after each press release, the plaintiff argued that the disclosures must have been corrective. The court found that the “purported relationship between the press releases and Fairfax’s improper accounting mechanisms [was] far too tenuous to support a claim.” Id. at *8. The plaintiff failed to demonstrate a “sufficient nexus” between Fairfax’s “irresponsibility” and the press releases, because an investor would not have been put on notice that Fairfax was engaging in the type of fraudulent accounting practices alleged by the plaintiff. Id.

In Wu v. Stomber, the plaintiffs argued that under Dura, a complaint need only allege some causal relationship between the fraud and the loss. No. 11-2287, 2012 WL 3276975, at *30 (D.D.C. Aug. 13, 2012). Plaintiffs claimed to satisfy this requirement by asserting that a series of partial disclosures by the defendants caused the stock price to decline over a two-month period. The court found that the plaintiffs did not establish the necessary connection between the disclosure of the previously undisclosed information and the drop in the stock price. The plaintiffs also argued that the “totality of the circumstances” surrounding the decline in the stock price “negate[d] any inference that the economic loss . . . was caused by changed market conditions . . . or other facts unrelated to [d]efendants’ fraudulent conduct.” Id. The court disagreed, finding that allegations of something resulting from the “totality of the circumstances” do not meet the Dura loss causation standard. Id.

While most recent decisions held that plaintiffs did not show a sufficient causal link between the defendants’ misconduct and the harm suffered by the plaintiffs, a few courts recently found adequately-pleaded loss causation. For example, the Second Circuit in Gould v. Winstar Communications, Inc., 692 F.3d 148, 161 (2d Cir. 2012), rejected the defendants’ argument that the district court’s award of summary judgment should be affirmed because the plaintiffs failed to show loss causation. The plaintiffs submitted proof of loss causation in the form of press releases exposing the defendant’s financial weaknesses and suggested that the defendant had engaged in improper revenue recognition practices. The defendant argued that the subsequent decline in the stock price could have been caused by other factors, including broader market trends and the downgrading of the defendant’s credit rating. The Second Circuit held that even if these facts were established, it would not “foreclose the reasonable inference that some part of the decline was substantially caused by the disclosures about the fraud itself.” Id. at 162. The court concluded that a jury could reasonably infer that the decline in the defendant’s stock price “was attributable in part to the alleged fraud.” Id. at 161.

In a motion to dismiss, the defendant in George v. China Automotive Sys., Inc. argued that the plaintiffs could not show the requisite causal link because the fall in the stock price was attributable to market-wide public scrutiny over Chinese reverse mergers. No. 11 Civ. 7533, 2012 WL 3205062, at *11-12 (S.D.N.Y. Aug. 8, 2012). The district court noted that when a plaintiff’s loss coincides with a market-wide phenomenon that causes similar losses to other investors, the likelihood that plaintiff’s loss was caused by the fraud decreases. But the court refused to dismiss in this case, noting it would be erroneous to find that a plaintiff cannot plead loss causation anytime the alleged loss “coincides with a market-wide event.” Id. at *11. The court explained that “[c]ourts granting motions to dismiss based upon the plaintiff’s failure to plead loss causation due to a coinciding ‘marketwide phenomenon,’ did so where the stock of the defendant-company was ‘clearly linked’ to a large-scale market event, such as the collapse of the housing market.” Id. at 12.