Print

PrintThe following post comes to us from Cornerstone Research, and is based on a Cornerstone report by Olga Koumrian, principal researcher at Cornerstone Research, and Robert M. Daines, Pritzker Professor of Law and Business at Standford Law School. The publication is available for download here.

This report looks at litigation challenging M&A transactions, filed by shareholders of large U.S. public target companies. These lawsuits usually take the form of class actions. Plaintiff attorneys typically allege that the target’s board of directors violated its fiduciary duties by conducting a flawed sales process that failed to maximize shareholder value. Common allegations include the failure to conduct a sufficiently competitive sale, the existence of restrictive deal protections that discouraged additional bids, and conflicts of interests, such as executive retention or change-of-control payments to executives. Another typical allegation is that the target board failed to disclose enough information about the sale process and the financial advisor’s valuation.

We used Thomson Reuters’ SDC database to obtain a list of all acquisitions of U.S. public targets valued at or over $100 million, announced in each year. We searched the SEC filings of the targets and acquirers for discussion of shareholder litigation. After the deals were closed, we used court dockets to trace litigation outcomes.

Review of 2012 M&A Litigation

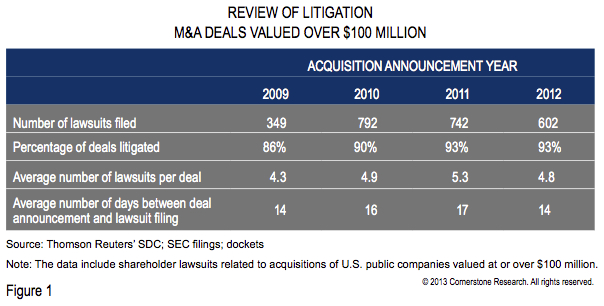

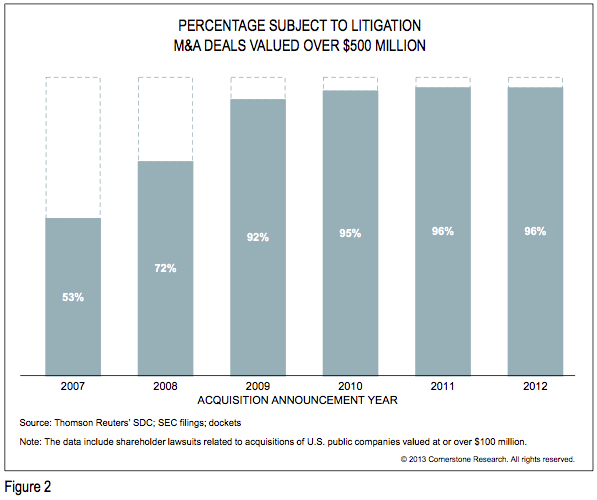

Continuing a recent trend, shareholders challenged the vast majority of M&A deals in 2012. Among deals valued over $100 million, 93 percent were challenged, with an average of 4.8 lawsuits filed per deal (Figure 1). These lawsuits were filed an average of 14 days after the merger announcement, with plaintiff firms sometimes announcing investigations within hours of the merger announcement. For deals valued over $500 million, 96 percent of target firms reported deal-related litigation in their Securities and Exchange Commission (SEC) filings (Figure 2), with an average of 5.4 lawsuits per deal.

Jurisdiction

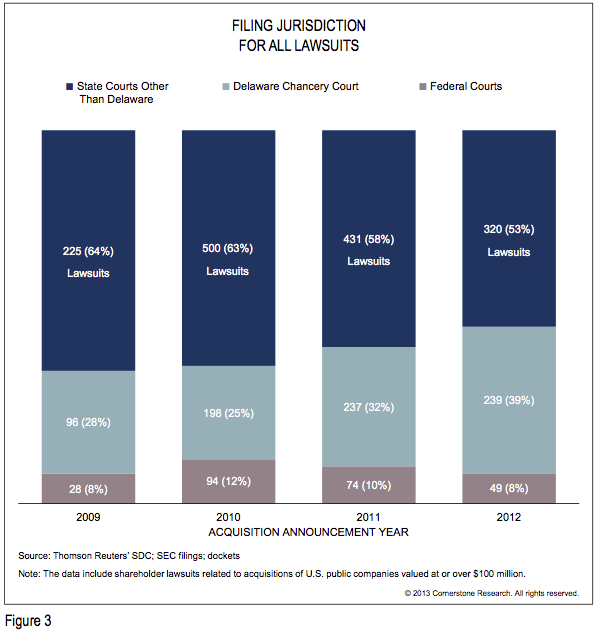

Before 2002, most M&A lawsuits were filed in the Delaware Court of Chancery. From 2002 through 2007, much of this litigation moved to other states (a phenomenon sometimes called the flight from Delaware). More recently, this trend appears to have reversed. The proportion of all lawsuits filed in the Delaware Court of Chancery grew in 2011 and 2012, drawing filings away from both federal and other state courts (Figure 3).

For firms incorporated in Delaware, 16 percent of all acquisitions were challenged only in the Delaware Court of Chancery in 2012, compared with 9 percent of deals in 2011 and 8 percent of deals in 2010 (Figure 4).

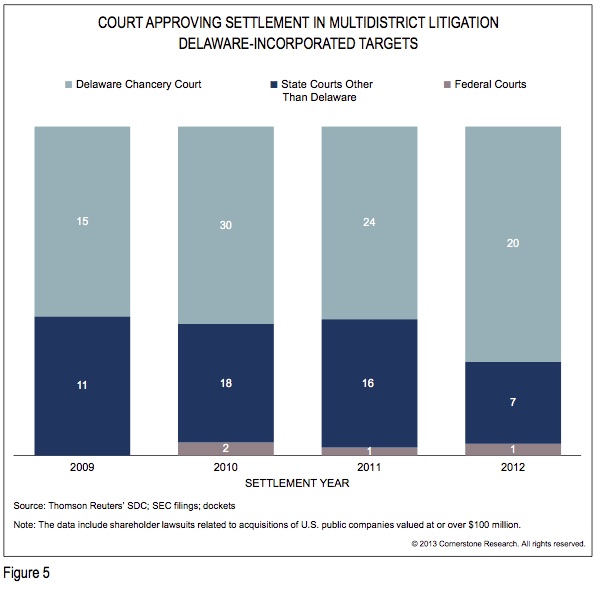

Moreover, a larger share of lawsuits filed in both the Delaware Court of Chancery and another court went to the Delaware Court of Chancery for settlement approval in 2012, compared with prior years (Figure 5).

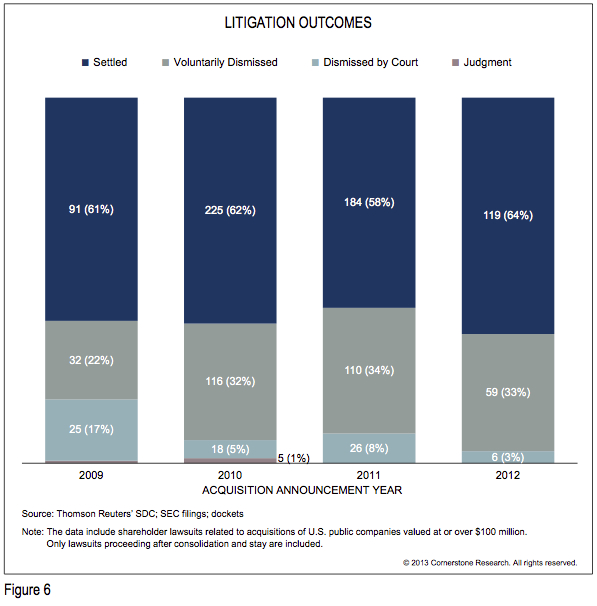

Outcomes

We were able to determine the outcome of 182, or 58 percent, of the consolidated lawsuits related to 2012 deals (Figure 6). [1] As in the previous two years, the majority (119) of the 2012 lawsuits settled. The settlements occurred before the deals closed and an average of 42 days after the lawsuit was filed. Plaintiffs voluntarily dismissed 59 lawsuits, and the court dismissed six cases (Figure 6).

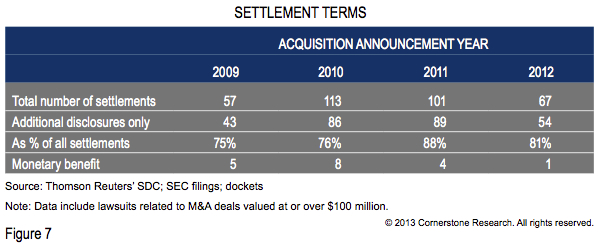

Settlements

As in prior years, most 2012 settlements resulted only in additional disclosures and fees awarded to plaintiff attorneys. The 119 settling lawsuits resulted in 67 unique settlements (several awarded lawsuits often settle together). Of the 67 settlements, shareholders received supplemental disclosures (and nothing else) in 54 settlements, or 81 percent, and the parties in only one settlement acknowledged that litigation contributed to an increase in the merger price (Figure 7). Additionally, the deal termination fee was reduced in four cases and the parties reached agreements about appraisal rights in six cases.

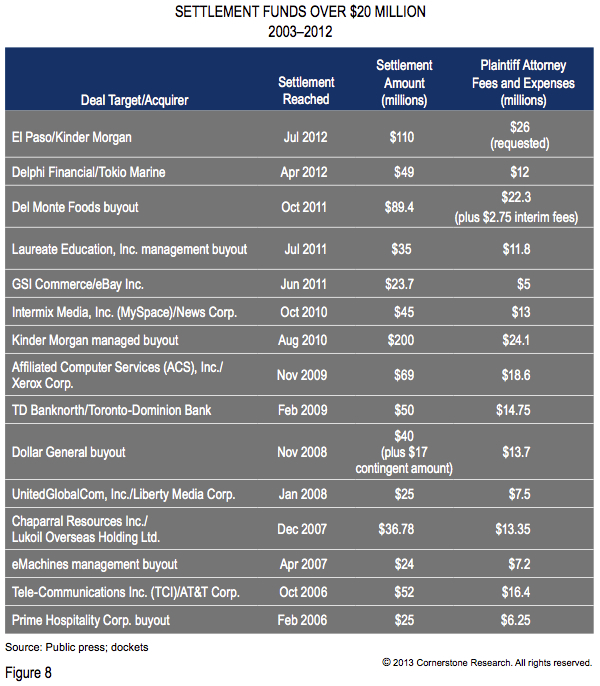

Two of the largest settlements in recent years occurred in 2012: $110 million in the El Paso Corp./Kinder Morgan Inc. deal and $49 million in the acquisition of Delphi Financial Group, Inc. by Tokio Marine Holdings, Inc. Both of these settlements involved transactions announced in 2011.

We also researched the largest settlements of the last decade. The largest settlements have increased in size over the past 10 years, and the three largest settlements were reached in the last three years (Figure 8). The average settlement fund between 2010 and 2012 was $78 million, compared with $36 million in 2003 through 2009.

Most of the large settlements shown in Figure 8 included allegations of significant conflicts of interest, such as:

- Target companies’ managements negotiated premiums for share classes they held.

- Delphi Financial’s class B stock

- Intermix Media’s preferred shares

- ACS’s class B shares

- TCI’s class B stock

- Target companies’ chief executive officers negotiated side deals with acquirers to purchase some of the targets’ assets.

- El Paso

- GSI Commerce

- Majority shareholders gained ownership of the remaining shares in the companies at allegedly unfair terms.

- TD Banknorth, allegedly in violation of the stockholders’ agreement

- UnitedGlobalCom, at a discount to the stock price before the announcement

- Chaparral Resources, after an alleged campaign to depress the target’s stock price

- Target companies’ financial advisors had conflicts of interest.

- In the Kinder Morgan buyout, the acquirer, the target’s advisor, and the acquirer’s financing provider were each Goldman Sachs affiliates.

- In the El Paso acquisition by Kinder Morgan several years later, El Paso’s advisor was Goldman Sachs’ investment banking arm, while Goldman Sachs’ private equity arm owned 19 percent of Kinder Morgan and had two appointees on Kinder Morgan’s board. Goldman Sachs agreed to forego the $20 million advisor fee or indemnity as part of the settlement, after Chancellor Leo E. Strine Jr. criticized the conflict of interest in his opinion denying the injunction.

- Del Monte’s advisor, Barclays Capital, contributed $23.7 million to the settlement after Vice-Chancellor J. Travis Laster’s injunction opinion had criticized Barclays for helping with the buy-side financing of the deal and failing to disclose the conflict of interest.

- The deal was a management-led buyout.

- eMachines was taken private by its founder, Lap Shun Hui, one year after its initial public offering.

- Laureate Education was a proprietary buyout by a consortium led by its CEO, Douglas Becker.

- The Kinder Morgan buyout was allegedly controlled by CEO Richard Kinder, who had close ties with the buyout consortium.

Only two of these settlements did not involve allegations of specific, significant conflicts of interest: Prime Hospitality and Dollar General. The Prime Hospitality litigation originally settled for additional disclosures. The plaintiffs renewed allegations that the purchase price of $790 million was inadequate after the acquirer, Blackstone, sold some of the acquired hotels for $645 million.

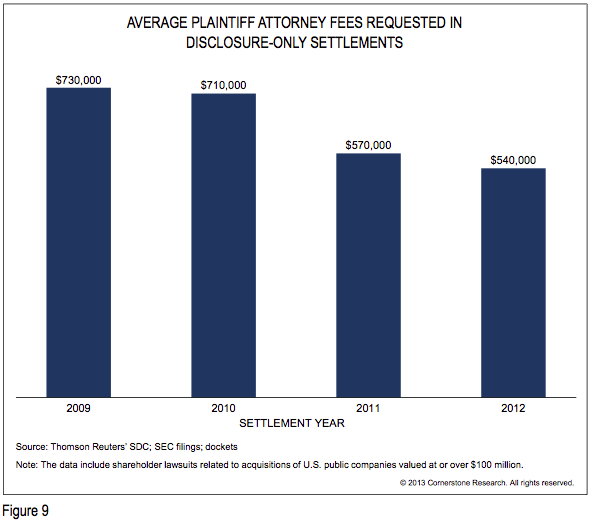

Plaintiff Attorney Fees

In the settlements related to 2012 deals, the average agreed-upon plaintiff attorney fee was $725,000. Of the 27 disclosed fee amounts, only three were $1 million or more; the largest fee was $3.9 million awarded in the Amerigroup Corp. litigation. The average plaintiff fee requested in settlements that resulted only in supplemental disclosures declined in 2012 for the third consecutive year (Figure 9).

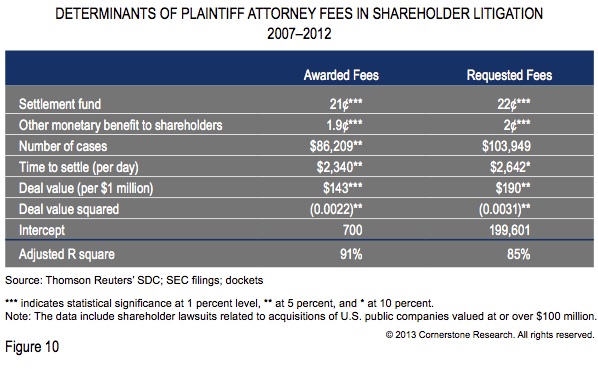

We researched the determinants of plaintiff attorney fees awarded in 101 judgments by the Delaware Court of Chancery between 2007 and 2012. Five factors had a statistically significant effect on the amount awarded (Figure 10):

- For settlements with payments to shareholders, a one dollar increase in the settlement fund was associated with an increase in plaintiff attorney fees of 21 cents.

- For settlements with indirect monetary benefit to shareholders (such as an increase in the purchase price during litigation, or an agreement to pay a special dividend), plaintiff attorney fee awards were larger by 1.9 cents for each additional dollar of such benefit.

- Each additional lawsuit consolidated into the settlement was associated with additional attorney fees of $86,000 on average.

- Each additional day between the lawsuit filing and the settlement was associated with an average increase in fees of more than $2,300.

- Larger deals are associated with larger awards, roughly $143 per $1 million of deal value. This relationship was nonlinear—additional size mattered less for the largest deals.

The same factors determined the fees requested by plaintiffs. The five factors listed above explained 91 percent of the variation in awarded fees, and 85 percent of the variation in fee requests.

We found no statistically significant relationships between the amount of attorney fee awards and the following factors:

- Any reduction in the deal termination fee as a result of the settlement,

- The number of jurisdictions in which litigation was filed before consolidation, • Whether a preliminary injunction was granted, or

- The year in which the settlement occurred.

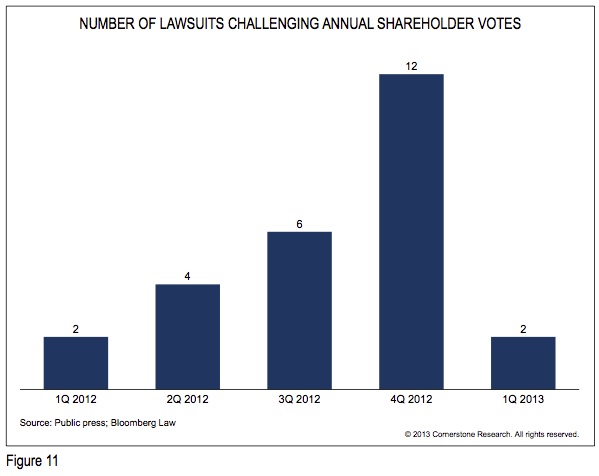

New Lawsuits Challenging Annual Proxies

In 2012, plaintiff attorneys active in shareholder M&A litigation filed a wave of lawsuits challenging annual proxy votes. Like the complaints alleging inadequate disclosures in merger votes, these lawsuits asked the courts to enjoin annual shareholder votes because of allegedly insufficient disclosures about executive compensation. The number of these filings increased as the year progressed (Figure 11).

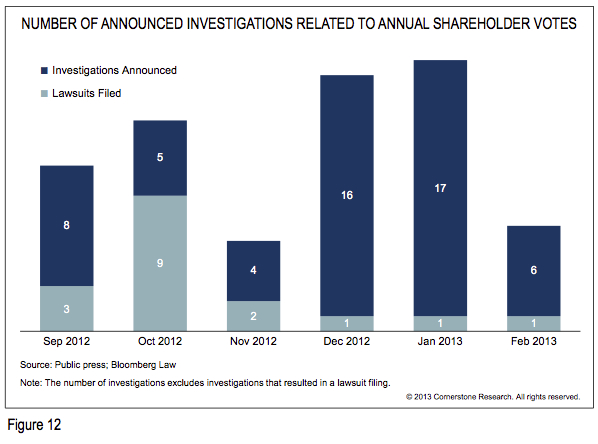

Initially, these cases focused on advisory votes on executive compensation (say on pay) and increases in the number of shares authorized for equity compensation plans. The say-on-pay claims were largely unsuccessful—the courts expressed skepticism about plaintiffs’ ability to demonstrate irreparable harm to shareholders resulting from advisory votes. Plaintiffs had more success with the argument that an increase in the number of shares can be dilutive to existing shareholders. As a result, recently announced investigations have focused on claims related to the increase in the number of shares, both those available to equity compensation plans and the firms’ total authorized shares (in votes to amend certificates of incorporation).

Plaintiffs have had some early successes. In April 2012, the Superior Court of California, County of Santa Clara, granted a preliminary injunction in Knee v. Brocade Communications, which was followed by a quick settlement for additional disclosures and $625,000 in plaintiff attorney fees. The court approved this settlement in October 2012. Several quick settlements in other cases followed. In these, defendant companies provided additional disclosures and agreed to pay plaintiff attorney fees, reportedly ranging from $125,000 to $450,000. These included:

- Martha Stewart Living Omnimedia, Inc., May 2012

- WebMD Health Corp., August 2012

- Microchip Technology Inc., August 2012

- H&R Block, August 2012

- NeoStem Inc., October 2012

- Applied Minerals, November 2012

However, not all cases were as successful for plaintiffs. We know of only one injunction request (other than Brocade) that was granted, and it was granted only in part, in a lawsuit challenging the proxy of Abaxis Inc. Many more injunction motions were denied, including:

- Ultratech, Inc., July 2012

- AAR Corp., October 2012

- Symantec Corp., October 2012

- Clorox Co., November 2012

- Globecomm Systems, November 2012

- Hain Celestial Group, Inc., November 2012

Plaintiffs also voluntarily dismissed several lawsuits:

- Amdocs Inc., January 2012

- Angiodynamics, October, 2012

- Microsoft, November 2012

- Lifevantage, November 2012

- Accuray Inc., January 2013

As the 2013 proxy season approaches, it is too early to tell how much plaintiff law firms will expand this litigation. On one hand, we have observed an increase in the number of announced investigations of potential breaches of fiduciary duties related to annual shareholder votes and the number of plaintiff law firms that pursue these cases. While all the 2012 litigation was filed by a single plaintiff law firm, two more have recently announced similar investigations. These three firms announced investigations of 16 public companies in December 2012 and of an additional 17 companies in January 2013, an increase over the average number in the prior three months. On the other hand, actual lawsuit filings of this type have declined from the October 2012 high. We know of only two complaints filed in the first two months of 2013, against PriceSmart, Inc. in January and Apple Inc. in February (Figure 12).

Endnotes:

[1] Consolidated lawsuits are the lawsuits that proceed after the courts consolidated multiple lawsuits in the same jurisdiction or stayed litigation in another jurisdiction.

(go back)