Print

PrintThe following post comes to us from Sullivan & Cromwell LLP, and is based on a Sullivan & Cromwell publication by Matthew M. Friestedt, Marc Trevino, and Jane Y. Wang.

We have reviewed the 365 merger agreements that were announced during the two years after the “Say-on-Golden-Parachute” vote rule went into effect on April 25, 2011 and that were subject to the rule. [1] We found that 39 companies (11% of the total) substantively enhanced executive compensation arrangements in connection with the transactions.

Some of the more common executive compensation enhancements, which generally did not result in negative vote recommendations from Institutional Shareholder Services (“ISS”), were: granting deal closing bonuses (in 17 deals), granting retention bonuses (in 16 deals) and granting additional equity awards that vest on or post-closing (in 13 deals). However, the following executive compensation enhancements generally did result in negative vote recommendations from ISS: granting new excise tax gross-ups (three out of four deals received negative ISS recommendations), cashing-out severance or converting severance into a retention bonus without an actual termination of employment (five out of eight deals received negative ISS recommendations) and accelerating the vesting of equity awards when the stated performance hurdles were not achieved or were artificially low (five out of six deals received negative ISS recommendations).

Each of the 27 companies that substantially enhanced executive compensation arrangements and received a positive ISS recommendation passed its say-on-golden-parachute vote. On the other hand, five of the 12 companies that enhanced arrangements and received a negative ISS recommendation failed the vote. For all 39 companies, shareholders overwhelmingly approved the deal itself and only one company failed its say-on-pay vote at the next annual shareholder meeting (for reasons unrelated to the say-on-golden-parachute vote).

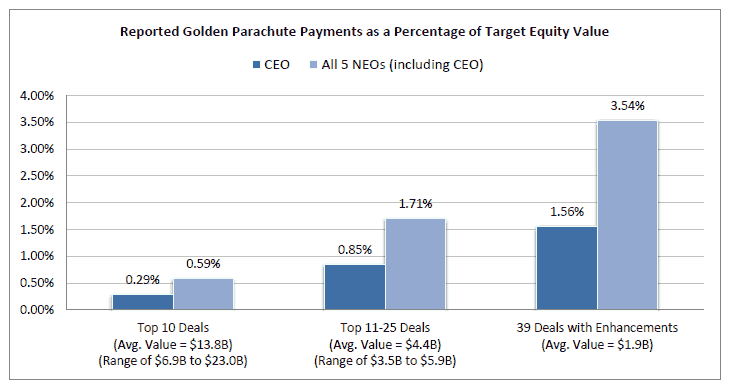

We also reviewed the size of the aggregate reported golden parachute payments as a percentage of the target’s equity value for the 25 largest deals announced during the first two years after the say-on-golden- parachute vote went into effect (this top 25 list includes tender offer acquisitions) and for the 39 companies that substantively enhanced executive compensation arrangements:

In general, golden parachute amounts as a percentage of the target’s equity value tend to increase as deals become smaller. Notably, for the largest 25 deals, only two companies reported golden parachute payments that were above two times the average percentage of target equity value. In contrast, for the 39 deals with enhancements, a meaningful number of companies reported golden parachute payments that were above two times the average (six companies for the CEO, and five companies for the NEOs as a group).

Endnotes:

[1] Although golden parachute arrangements must be disclosed in connection with acquisitions implemented through a tender offer, there is no related say-on-golden-parachute vote and, accordingly, tender offers were not included in our review.

(go back)