Print

PrintMary Ann Cloyd is leader of the Center for Board Governance at PricewaterhouseCoopers LLP. This post is based on an edition of ProxyPulse™, a collaboration between Broadridge Financial Solutions and PwC’s Center for Board Governance; the full report, including additional figures, is available here.

This post looks at results from 2,788 shareholder meetings held between January 1 and May 22, 2014. We provide data and analyses on areas such as share ownership composition, director elections, say-on-pay, proxy material distribution and the mechanics of shareholder voting. We also look at differences in proxy voting by company size.

With about three-quarters of the 2014 proxy season complete, voting results continue to show that public company executives and directors must remain vigilant regarding corporate governance matters. In comparison to last proxy-season at this time, large-cap ($10b+) companies have attained higher levels of shareholder support both for directors and for executive compensation plans. In contrast, support levels for executive compensation plans fell at mid-cap ($2b–$10b), small-cap ($300m–$2b) and micro-cap ($300m or less) companies, and support for directors fell at mid-cap companies.

2014 Proxy Season Developments:

- Average shareholder support remains strong for most directors, but there were 702 directors (4%) who failed to attain at least 70% support, a key threshold for some proxy advisory firms.

- There was an increase in the number of say-on-pay proposals that failed to attain a majority of shares voted in support—from 54 through May of 2013 to 72 through May of 2014. While average support levels for executive compensation plans rose from 89% to 91% at large-cap companies, a greater percentage of mid-cap and small-cap companies failed to attain at least 50% of shares voted in support. The percentage of mid-cap companies failing to reach majority support rose from 2% last season to 5% so far this season.

- Board declassification proposals continue to attain high levels of support when they are put to a shareholder vote—with an average of 96% of shares voted in favor. We are also seeing increases year over year in the number of proposals related to the disclosure of corporate political spending and social and environmental matters.

- Shareholder engagement efforts are intensifying and a growing number of companies are taking a more targeted approach—resulting in increasingly efficient communications campaigns. Some companies are refining their approach to communications by analyzing historical voting participation and tailoring their outreach accordingly.

- Technologies for virtual shareholder meetings have improved since their introduction 5 years ago, and the number of companies using them has increased from 4 in 2009 to 67 in 2013. The 2014 proxy season is on pace to set an annual record for the number of virtual shareholder meetings held.

- Because proxy materials are more frequently distributed electronically or through a mailed Notice, shareholder communications costs are falling. There was a 3 percentage point decrease in the volume of paper proxy materials sent to retail shareholders (from 43% last season to 40% this season).

Public Company Ownership

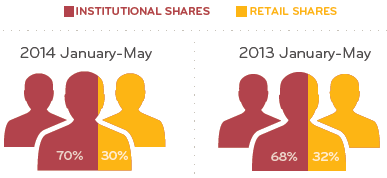

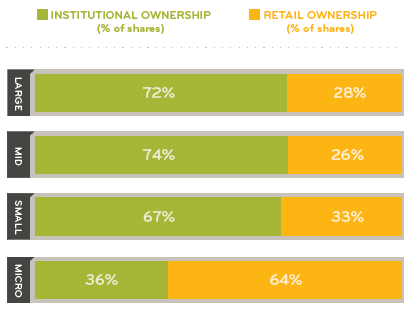

Institutional shareholder ownership increased slightly. Through May of the 2014 proxy season, 70% of street shares were owned by institutional shareholders and 30% by retail shareholders—an increase of about 2 percentage points compared to last year. Average share ownership varies by company size. For instance, mid-cap companies have the highest average rate of institutional ownership (74%), while micro-cap companies have the highest average rate of retail ownership (64%).

Ownership Composition

Share Ownership by Company Size—2014 January–May

Shareholder Voting

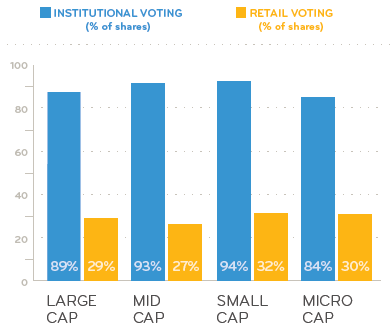

Low retail voting rates continue to present companies with engagement challenges and opportunities. Institutional shareholders voted 90% of their shares thus far in 2014, but retail shareholders voted just 29% of their shares. Voting rates also vary by company size. For example, institutional shareholders voted 94% of their shares at small-cap companies but only 84% at micro-caps. Retail shareholder voting rates were in the range of 27% to 32%—depending on market cap.

With only about three of ten retail shares voted, companies have a significant opportunity to encourage participation from this historically supportive shareholder segment. Companies interested in expanding their retail shareholder engagement efforts can benefit from a deeper understanding of the type of retail shareholders they have: registered (direct) or beneficial (via broker), the size of these accounts, and their geographical location. Combined with an understanding of historical retail shareholder participation data, this information becomes a basis for development of an efficient retail shareholder outreach program.

Companies may wish to consider applying a “test and learn” approach to their shareholder communications. After all, not all shareholders are motivated to vote. This is particularly true of retail shareholders—where low rates of participation may be driven by such diverse factors as apathy or lack of understanding of complex proposals. As some companies engage more frequently with their retail shareholders, they are growing their information “databank” and can apply known successes to future efforts.

Shares Voted by Company Size—2014 January–May

Director Elections

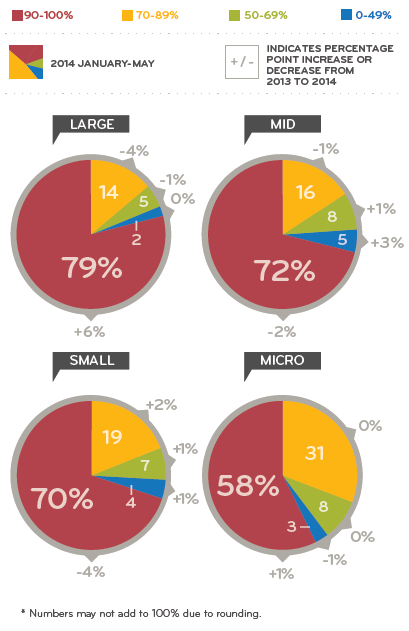

Shareholder support for directors is strong on average, but 702 directors failed to receive at least 70% support of the shares voted. On average, directors received 97% of shares voted in favor through May 22, 2014. However, support levels vary by company size. At large-cap companies, 94% of directors up for election received over 90% shareholder approval compared to 78% of directors at micro-cap companies. Among mid-cap companies, there was an increase over last season in the number of directors that failed to attain at least 70% of shares voted in support—from 99 last year at this time to 116 this proxy season. Generally speaking, large-cap companies have been first to adopt the governance reforms seen as “leading practice” by some shareholders. For example, a significant majority of large-cap companies have adopted practices such as annual director elections and majority voting. Many large-cap companies have also provided shareholders with voluntary reporting in areas like sustainability, corporate social responsibility and political spending. These actions may explain in part the higher levels of shareholder support for large-cap company directors.

Say-On-Pay

There was high support for executive compensation plans at large-cap companies, but support at small- and mid-cap companies decreased since last proxy season. Ninety-three percent of large-cap company say-on-pay proposals attained at least 70% shareholder support and large-cap companies had the highest average approval rates for their pay plans. Yet, across companies of all sizes, 11% failed to attain the 70% support threshold looked at closely by some proxy advisory firms. Among small and mid-cap companies, support levels fell as a greater percentage of their proposals dipped below the 70% support threshold. This means that some of these companies should expect proxy advisors to look more closely at, and potentially recommend a vote against, their compensation plans next year. Among micro-cap firms, the average level of support fell from 90% last season at this time to 88% this season. There was a season-over-season increase in the number of pay plans that failed to receive majority shareholder support from 54 through May of 2013 to 72 through May of 2014.

Say-on-Pay Voting Rates by Company Size

Shareholder Activism

While 2013 saw an increase from 2012 in the number of proxy contests and exempt solicitations (communications such as “vote no” campaigns against directors), 2014 has seen a decline in both of these phenomena. There have been 23 proxy contests in the 2014 proxy season thus far, compared to 28 at the same point last year. Exempt solicitations have decreased from 18 to 10 over the same time period. However, this data does not necessarily indicate a decrease in activism overall. In many instances, companies and investors have chosen to negotiate and come to a settlement in advance of a shareholder vote.

Board declassification proposals pass with high support and are moving downstream to smaller companies. The annual election of all of a company’s directors as a group has become the dominant practice of the largest public companies over the last ten years. According to the Spencer Stuart 2014 US Board Index, 91% of S&P 500 companies now have declassified boards compared to only 60% in 2003. Over the last three years, board declassification reform has been advocated by, among others, the Shareholder Rights Project (SRP), a program at Harvard Law School acting in coordination with public pension funds and charitable organizations. The SRP continued to file board declassification proposals at companies in 2014, with significant success. Of the proposals that have gone to a vote this year, average shareholder support was 96%. It is noteworthy that in the 2014 proxy season mid-cap companies have experienced the greatest prevalence of these proposals (54%). This attention, once reserved for large-cap companies, is not particularly surprising, as most of the largest companies have already adopted annual director elections.

Communications and Voting Methods

Electronic delivery of proxy materials continues to increase. Technology continues to transform the means by which shareholders receive proxy materials and vote their shares. Virtually all institutional investors received proxy materials through an electronic platform in the 2014 proxy season and 98% of voted institutional shares were cast through an electronic platform.

Retail shareholders continue to receive their proxy materials in a variety of ways and they use a more diverse mix of voting methods. Thirty-two percent of retail investors received their 2014 proxy materials electronically and 28% through a mailed Notice of Internet Availability (up from 30% and 27%, respectively, through May of the 2013 proxy season). There was a 3 percentage point decrease in the volume of paper proxy materials sent to retail shareholders (from 43% through May of the 2013 proxy season to 40% through May of the 2014 proxy season)—consistent with a trend we have observed over the last several years. The technology shift in the distribution of proxy materials results in decreased printing and mailing costs for companies.

In terms of voting, individuals used technology platforms for 73% of their shares. While many retail shareholders express a clear preference for receiving proxy materials in hard copy form, among those who vote, most vote their shares electronically.

Use of virtual shareholder meetings is growing. While the vast majority of companies continue to hold “in-person” annual meetings, a small, but growing number have added a virtual component. Virtual meetings come in two main varieties: “hybrid” meetings where audio and/or video broadcasts are available to attendees in addition to the live meeting, and “fully virtual” meetings which are solely online. Whereas only 4 companies held virtual annual meetings in 2009, 67 held them in 2013. We expect a further increase for 2014. The use of virtual meetings allows a greater number of shareholders to participate without travel. Shareholders are able to watch/listen, ask questions and vote their shares during a virtual meeting. From the point of view of the company, virtual meetings can more effectively ensure security—as shareholder identity is validated through unique control numbers. Virtual meetings can also help companies build their shareholder engagement programs, as data can be tracked on meeting attendance and activity for use in future years.

The complete publication is available here.