Print

PrintThe following post comes to us from Jordan A. Thomas, partner at Labaton Sucharow LLP and former assistant director at the Securities and Exchange Commission, and is based on a Labaton Sucharow publication by Mr. Thomas and Vanessa De Simone.

Four years ago this month, with the country still reeling from financial crisis, Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act–the most sweeping financial reform effort since the Great Depression. The goal of Dodd-Frank was as ambitious as its scope; as President Barack Obama remarked, the legislation would “restore markets in which we reward hard work and responsibility and innovation, not recklessness and greed.”

For the Securities and Exchange Commission and the citizens whom the Commission protects, one of the key innovations of Dodd-Frank was the creation of a new and game-changing whistleblower program. Understanding the many risks that underpin a report of misconduct, Congress developed three key counter-incentives to encourage individuals to come forward: (1) enhanced protections from employment-related retaliation; (2) the ability to report securities violations anonymously; and (3) the opportunity to obtain significant monetary awards when the information provided results in a successful enforcement action. Together, these incentives embodied a simple idea: rewarding integrity can help uncover wrongdoing in the securities markets more quickly, more easily and more effectively—potentially stopping misconduct before it wreaks substantial harm on investors.

Today, the SEC Whistleblower Program is well underway. While we have witnessed the Program’s enormous potential as a law enforcement tool, we also see that more work must be done to stop fraud in the securities markets, bring transparency to investors and protect whistleblowers. In this report, we examine the major developments—landmark cases, significant awards, SEC statistics and hot button issues—related to the SEC Whistleblower Program over the past 12 months and how these developments may impact the future of corporate whistleblowing.

The SEC Whistleblower Program Picks Up Steam

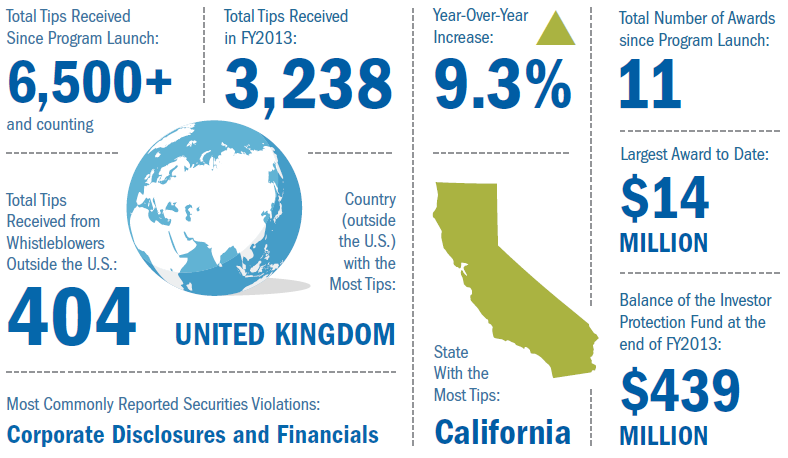

Growth was a central theme over the last year, as awareness of the program continued to build and cases based on early whistleblower tips began to make their way through the SEC’s investigative pipeline. It was also a period of notable firsts. In September 2013, the SEC made its first major award—more than $14 million to an anonymous whistleblower. And in June 2014, it brought its first retaliation claim against the investment advisor Paradigm Capital Management.

Equally significant, the program continued to generate a substantial number of tips. According to its Annual Report to Congress, the Office of the Whistleblower received 3,238 tips in fiscal year 2013, a 9.3% increase over the prior year. These tips came from all corners of the country and around the globe, signaling an increased domestic and international awareness of the program. Notably, the tips were not only high quantity, but also high quality. According to SEC Chair Mary Jo White, “the SEC’s whistleblower program, which has been fully operational for three years, has already had a significant impact on our investigations. The tips have helped the Enforcement Division identify more possible fraud and other violations and earlier than would otherwise have been possible.” These remarks echoed similar comments by other SEC officials, including Enforcement Director Andrew Ceresney, who stated in November 2013 that “our whistleblower program continues to pick up steam” and that “[w]e are increasingly sourcing our own cases through whistleblower tips.” Associate Director of Enforcement Steve Cohen also reported that many SEC investigations have been “turbocharge[d].”

Given that the typical life cycle of an SEC investigation is two to four years, these reports suggest that in the months (and years) ahead, we are likely to see many more major cases built on whistleblower intelligence. Success tends to build upon itself, so the uptick in major SEC awards is likely to motivate even more whistleblowers to come forward in the future.

Momentum is only part of the story. The past 12 months have also revealed persistent challenges, for both whistleblowers and the securities markets as a whole. Misconduct is still prevalent on Wall Street and the forces that often cause financial calamities remain very concerning.

While it is not clear when or where the next major corporate scandal will arise, statistics like those referenced below suggest it’s almost inevitable.

Persistent Challenges: The Financial Markets Are Still Risky Territory

Click image to enlarge

Click image to enlargeDespite the fact that whistleblowing can be an effective and empowering deterrent against misconduct, many organizations are taking steps to stifle whistleblowing by instituting policies that discourage employees from coming forward, trying to silence employees through overly-restrictive confidentiality agreements, or retaliating against individuals when they do come forward. These problems, discussed in depth later in the post, not only harm individual whistleblowers, they also limit the SEC’s ability to protect investors. Over the past year, the SEC has taken steps to address these issues, and we expect to see more action by the SEC in this area.

The SEC Whistleblower Program has not and cannot transform the securities enforcement landscape overnight. Nevertheless, over the last 12 months, we have witnessed steady, incremental and meaningful change. We look forward to seeing what the next year brings.

SEC Whistleblower Score Card

Click image to enlarge

Click image to enlargeEmployment Update: Retaliation in the Cross-Hairs

Although Dodd-Frank’s whistleblowing provisions are part of the federal securities laws, they have important employment implications for both whistleblowers and their counsel. In particular, Dodd-Frank toughened the penalties for employers who retaliate against whistleblowers and made it easier for whistleblowers to bring retaliation claims in federal court.

Retaliation Levels Remain High

The past year showed that retaliation against whistleblowers is a real threat—and that the SEC will take a firm stand against it. In its most recent National Business Ethics Survey, the Ethics Resource Center (ERC) data indicated that an alarming 21% of employees who reported workplace misconduct experienced some form of retaliation—one percentage shy of the all-time record. These figures are consistent with Labaton Sucharow’s U.S. Financial Services Industry Survey, released in July 2013, which revealed that 24% of respondents felt their employers would likely retaliate if they were to report workplace misconduct. An even higher percentage of the women surveyed—36%—expected they would be retaliated against if they blew the whistle. Not surprisingly, the fear of retaliation leads to silent witnesses; the ERC found that that 34% of those who declined to report wrongdoing feared retribution within their companies.

The good news is that the SEC has shown a willingness to fight for whistleblowers and take retaliation head on. In June, the Commission brought its first ever retaliation charge against a company, Paradigm Capital Management. Paradigm and its chief executive, were also charged with failing to properly disclose principal transactions to clients, agreed to pay nearly $2.2 million to settle the SEC’s claims. This pioneering case—in which Labaton represented the whistleblower—serves as a warning to companies that retaliating against a whistleblower can lead to added scrutiny from the SEC and, in certain cases, heightened sanctions.

– SEC Chair Mary Jo White

These are positive developments both for whistleblowers and companies. To be sure, many companies continue to lag behind when it comes to implementing whistleblower-friendly compliance systems, but our hope is that the SEC’s continued focus on retaliation will motivate more of these organizations to improve their internal systems as well.

The Debate over Internal Reporting: The SEC Takes A Stand, But Unsettled Questions Remain

With the SEC placing greater focus on retaliation, one of the key questions for whistleblowers, companies and their respective counsel has been whether, and the extent to which, Dodd-Frank protects whistleblowers who have reported misconduct internally, but have not (or not yet) reported that misconduct to the SEC.

The debate over internal reporting is complex, pivoting on an apparent conflict between Dodd-Frank’s general definition of a whistleblower and language found in Section 21F(h) (1)(A) of the statute.” The SEC’s interpretation of this incongruous statutory language is that Congress did not unambiguously intend to limit Dodd-Frank’s retaliation remedies to external whistleblowers. In an attempt to clarify matters, the SEC adopted Rule 21F-2(b)(1), which provides that any individual who engages in activities covered by Section 21F(h) (1)(A)—including internally reporting fraud at a public company—is covered by Dodd-Frank’s anti-retaliation provisions. So far, the majority of district-level courts to consider the issue have deferred to the SEC’s interpretation and found that internal whistleblowing can, in certain circumstances, constitute protected conduct. The only circuit-level court to consider the issue, however, reached the opposite conclusion. In Asadi v. G.E. Energy (USA), L.L.C., 720 F.3d 620, 630 (5th Cir. 2013), the Court concluded that internal whistleblowing was not actionable under Dodd-Frank, because Congress intended to protect only those individuals who report misconduct to the SEC.

The internal reporting issue is now before the Second Circuit Court of Appeals in Liu Meng-Lin v. Siemens AG, with a decision expected soon. The SEC weighed in on Siemens in February 2014 with a compelling amicus brief arguing in favor of the whistleblower and urging deference to Rule 21F-2(b)(1). If the Second Circuit comes down on the side of the SEC, it will create a circuit split and set the stage for a potential Supreme Court showdown on the issue (it’s also possible that the Second Circuit will decide Siemens on other grounds).

For now, though, whistleblowers, companies and counsel are left with some measure of uncertainty. Employers may find it harder to encourage employees to use the company’s reporting systems if employees understand that internal whistleblowing is not protected conduct. Prospective whistleblowers also face a difficult dilemma: on the one hand, the rules of the SEC Whistleblower Program offer benefits to employees who report internally first, including the potential for a larger award. On the other hand, an employee that is retaliated against based on internal whistleblowing may be left out in the cold without any recourse against the employer under Dodd-Frank (he or she may still be able to bring a claim under Sarbanes-Oxley or state whistleblower laws). Even more troubling, since the SEC rules indicate that some internal whistleblowing is protected conduct under Dodd-Frank, individuals may decide to report internally first in reliance upon the SEC rules, without realizing that they may have limited recourse for subsequent retaliation.

In light of these obvious challenges, Labaton Sucharow, in partnership with the Government Accountability Project (GAP), the nation’s leading non-profit whistleblower advocacy group, has petitioned the SEC to provide additional guidance to whistleblowers on the potential risks and rewards of reporting internally before submitting a tip to the SEC. Guidance from the SEC will enable whistleblowers to make informed decisions about reporting misconduct internally. We’re hopeful that the SEC will take swift and decisive action on this critical issue.

A Supreme Court Win For Whistleblowers

Whistleblowers earned an important Supreme Court victory this year in Lawson v. FRM LLC, in which the Court ruled that Sarbanes-Oxley’s anti-retaliation provisions apply not only to employees of public companies who report misconduct, but also to private contractors retained by public companies. This is an important decision for private contractors who are considering becoming SEC whistleblowers, since those individuals will now be able to bring a claim under Sarbanes-Oxley if they suffer for reporting misconduct to the SEC.

Courts have not yet squarely confronted the related question of whether Dodd-Frank’s separate anti-retaliation provisions protect private contractors, although one court allowed a contractor’s Dodd-Frank claims to go forward without expressly examining the significance of her contractor status. Since neither Dodd-Frank nor the SEC Whistleblower Rules limit the definition of a “whistleblower” to an “employee,” an argument can be made contractors should be protected from retaliation, whether they are retaliated against by their own employer (e.g. a consulting group, law firm or contractor agency) or the company for which they are providing services. On the other hand, Dodd-Frank specifically directs that “No employer may discharge, demote, suspend, threaten, harass, directly or indirectly, or in any other manner discriminate against, a whistleblower in the terms and conditions of employment,” creating an opening for defendants to argue that contractors can only bring claims against their direct employers, not companies that retain them to provide services in a non-employee role. As companies continue to shift work to outside contractors to save costs, such contractors are likely to play an increasingly vital role in uncovering potential securities violations, making the rights and remedies available to them especially important.

Emerging Issues: Can Confidentiality Agreements Be Used to Stifle Whistleblowing?

One of the most concerning trends over the past 12 months has been the increasing use of employment, severance and confidentiality agreements to attempt to stifle whistleblowing. Our clients are regularly asked to sign agreements that, if adhered to, would prevent them from sharing documents or information about their employer (or former employer) with any third party, including the SEC. Many agreements also seek to require individuals to tell their employer before communicating with the SEC or other government officials, a requirement that would effectively strip employees of their statutory right to report anonymously. Still other agreements would force whistleblowers to waive their right to receive a monetary award from the SEC in order to receive a fair severance package.

We view such agreements as unlawful and unenforceable under prevailing law. In addition, law developed in the employment discrimination and False Claims Act contexts also establishes that companies cannot use private contracts to prevent employees from communicating with law enforcement authorities. In more extreme cases, obstructing a whistleblower from reporting possible crimes could even subject a company to obstruction of justice or compounding charges.

Likewise, these agreements also appear to run afoul of SEC Rule 21F-17, which makes it a separate violation of law to “take any action to impede an individual from communicating directly with the Commission staff about a possible securities law violation, including enforcing, or threatening to enforce, a confidentiality agreement.” Agreements that eliminate an individual’s right to report violations anonymously or the ability to receive a whistleblower award can “impede” communications with the Commission staff by removing the important incentives that Congress created to promote whistleblowing. The SEC has issued a call for examples of employee agreements that in form or substance impede communications with the Commission. We fully expect that the SEC will take a broad view of the types of agreements that fall under Rule 21F-17.

Nevertheless, the fact that these agreements are likely unlawful and unenforceable doesn’t mean they’re harmless. Indeed, they pose a profound danger to prospective whistleblowers and the SEC Whistleblower Program itself. Particularly in this tough economic environment, many prospective whistleblowers may be unwilling to challenge an employer, and instead decide to remain silent. Other prospective whistleblowers, especially those who are unrepresented by counsel, may simply assume that such agreements are a normal part of employment. Put simply, individuals may not realize that they have an unwaivable right to report possible violations of law to the government.

Left unchecked, this problem could silence scores of whistleblowers possessing actionable intelligence about serious securities violations, undermining the potency of the whistleblower program as a whole. In a petition to the SEC, we asked the SEC to strengthen Rule 21F-17, to make it clear that agreements that limit an individual’s right to receive a monetary award, or otherwise undercut the incentives that Congress created, are unlawful.

In the meantime, it’s crucial that whistleblowers are educated, and that counsel remain vigilant when negotiating agreements that could impede an employee’s ability to participate in whistleblowing programs. It’s also important for companies and their counsel to understand the limits of lawful confidentiality provisions. Ultimately, agreements must strike a balance between protecting a company’s legitimate confidentiality interests, and ensuring that the SEC is not deprived of potentially vital information about unlawful activities.

Top 5 Takeaways for organizations, Employers and Compliance Personnel

1. Take concrete steps to avoid even the perception of retaliation: Responsible organizations must treat employees who report misconduct—whether internally or externally–with fairness and respect. This is important for workplace culture and will also help to avoid or defend retribution claims by the employee or the SEC. It also strengthens attitudes about, and usage of, internal compliance mechanisms. The fact is, most employees first report concerns about misconduct internally. Unfortunately, and as the ERC reported in its preeminent workplace survey in 2013, 40% of workers who reported externally said that they did so because they were retaliated against after making an initial report inside their company. More than a third of external whistleblowers said that their company acted on their internal report, but that they were dissatisfied with the company’s response. An alarming 29% reported that the company did not act on their initial internal reports at all. Bottom line: Employers must respond to internal complaints in an open, serious and sensitive manner.

2. Make it clear that internal reporting is protected conduct under company policies: Courts are currently split over whether internal whistleblowers have the right to bring retaliation claims under Dodd-Frank. This legal uncertainty creates a strong incentive for individuals to report misconduct directly to the SEC. Organizations that want to encourage internal reporting–which can help companies nip problems in the bud and, in some cases, reap the advantages of self-reporting to the SEC–should implement, promote and enforce strong policies against retaliation.

3. Assume the whistleblower is right: We regularly see companies miss an opportunity to quickly fix problems because they failed to undertake a thorough investigation of a report of misconduct. As SEC Chair Mary Jo White cautioned at an address to corporate directors: “You may well have doubts about the bona fides of a particular whistleblower—perhaps because his or her prior 9 tips have not proven to be true or management tells you that the would-be whistleblower is a disgruntled employee. But always think—because it is so—that her tenth tip may be right on target…it is a mistake not to take all tips from whistleblowers seriously.”

4. Be aware of potential pitfalls in your employment agreements: Businesses have a legitimate interest in protecting their trade secrets and other confidential information. But confidentiality or employment agreements that do not carve-out an employee’s ability to report possible violations to law enforcement agencies can land employers in hot water. Over the past year, the SEC has placed more scrutiny on such agreements, which may violate Rule 21F-17, with SEC Whistleblower Chief Sean McKessy warning that lawyers who draft such agreements could be barred from practice before the Commission.

5. Do not assume that auditors, lawyers and risk managers cannot be whistleblowers: Employers received an important reminder this year that auditors, compliance personnel, risk managers and other corporate “gatekeepers” can act as whistleblowers with all attendant legal protections. In Yang v. Navigators Group, Inc., a company sought to dismiss Sarbanes-Oxley and Dodd-Frank retaliation claims brought by its former risk manager based in part on the argument that reporting risk concerns was “part and parcel” of her position. The court flatly rejected this argument and denied the defendant’s motion to dismiss. Auditors, lawyers and compliance personnel do face some additional eligibility requirements if they plan to seek a monetary award through the SEC Whistleblower Program, but those requirements do not bar participation in the program. To be sure, these gatekeepers often have the best view into potential misconduct, so their complaints should be taken especially seriously.

Top 5 Takeaways for Whistleblowers and Their Counsel

1. Seek guidance when it comes to confidentiality agreements. Whistleblowers do not need an attorney to submit a complaint to the SEC (although individuals must be represented by an attorney in order to submit a complaint on an anonymous basis). But, we do recommend that current or prospective whistleblowers seek the advice of an experienced attorney when it comes to certain issues, including confidentiality agreements. Many companies use employment contracts to restrict whistleblowing, and individuals should be sure that their rights are protected with respect to such agreements. Even though the SEC rules provide protections to whistleblowers who report confidential information to the SEC, individuals should also strongly consider consulting with experienced counsel before taking confidential documents from their employer, since taking certain types of documents, particularly those that are unrelated to possible violations or obtained in an unlawful manner, may expose the whistleblower to liability.

2. Know the Whistleblower Program rules. In addition to granting a significant number of awards this year, the SEC’s Office of the Whistleblower also denied a number of award applications, including several applications that were filed more than 90 days after the relevant Notice of Covered Action. Whistleblowers must be mindful of the logistical rules of the Program, such as filing deadlines, to ensure that they preserve their rights and maximize their chances of obtaining a monetary award.

3. Understand the reality of retaliation: Statistics show that the risk of whistleblower-related retaliation is substantial. It’s important for whistleblowers to understand this reality before deciding when, whether and how to come forward— in particular, whistleblowers should carefully consider the option of reporting possible violations to the SEC on an anonymous basis, since anonymity is one of the most effective ways to prevent retaliation.

4. Know the risks and rewards of internal reporting: The question of whether internal reporting can give rise to a Dodd-Frank retaliation claim remains an unsettled question, with courts coming down on both sides of the issue over the past year. At the same time, the SEC Whistleblower Program offers significant incentives—including a better chance of obtaining a maximum monetary award–for whistleblowers who report internally. Prospective whistleblowers should weigh these potential costs and benefits, as well as other factors such as their company’s internal policies and level of commitment to compliance, when deciding whether to report internally, or to go direct to the SEC.

5. The SEC is an ally and whistleblowing can work: The SEC has been a vocal supporter of both internal and external whistleblowers and is taking action to punish unlawful retaliation. We expect the SEC to bring more retaliation claims in the year ahead. The past year demonstrates that the SEC Whistleblower Program can work–to root out misconduct, reward whistleblowers for actionable information, and protect whistleblowers from retaliation. These developments should give real encouragement to individuals who are considering coming forward.