Print

PrintThe following post comes to us from Michal Barzuza, Professor of Law at the University of Virginia School of Law, and David Smith, Professor of Finance at the University of Virginia.

In our paper, What Happens in Nevada? Self-Selecting into Lax Law, forthcoming in the Review of Financial Studies, we study the financial reporting behavior of firms that incorporate in Nevada, the second most popular state for out-of-state incorporations, after Delaware. Compared to Delaware, Nevada law has weak fiduciary requirements for corporate managers and board members. We find evidence consistent with the idea that lax shareholder protection under Nevada law induces firms prone to financial reporting errors to incorporate in Nevada, and that lax Nevada law may also cause firms to engage in risky reporting behavior. [1] In particular, we find that Nevada-incorporated firms are 30 – 40% more likely to report financial results that later require restatement than firms incorporated in other states, including Delaware. These results hold when we narrow our set of restatements to more serious infractions, including restatements that reduce reported earnings, and to restatements that raise suspicions of fraud or lead to regulatory investigations.

The results are also robust to use of a propensity score estimator that matches Nevada firms to Delaware firms using a multivariate matching model. Our findings are further strengthened by comparing accounting “aggressiveness” ratings for Nevada firms with other states, as tracked by the data intelligence service GMIRatings. Holding other characteristics constant, Nevada firms stand out as especially aggressive users of risky accounting techniques.

We document a close link between restatement behavior and changes to Nevada law. Firms that incorporated in Nevada after it adopted its broad exculpation statute, particularly those Nevada firms that completed initial public offerings (IPOs) during the period 1988 to 2003 are most responsible for the high restatement rates. If restatements are a proxy for unobserved agency problems (Arlen and Carney, 1992; Gordon, 2003; Coffee, 2005; Burns and Kedia, 2006; Efendi, Srivastava, and Swanson, 2007) our results suggest that Nevada lax law attracts firms with relatively high agency costs. Employing a two-stage instrumental variable (IV) regression using the location of a firm’s headquarters as an instrument for Nevada incorporation, we also find some evidence that lax law causes firms to engage in risky and aggressive accounting behavior. We find that our Nevada incorporation instrument is positive and, at least for one specification, statistically significant at the 5% level. We also find some evidence that firms moving their state of incorporation to Nevada from another state are predisposed to restate financials prior to the “reincorporation,” although “reincorporations” are relatively uncommon, so the power of the test is low.

Finally, we examine the valuation implications for incorporating in Nevada. In regressions of firm-level measures of Tobin’s q on a Nevada incorporation dummy, we find no discernible valuation effect for firms that incorporate in Nevada. Overall, our valuation findings are inconclusive and make it difficult to draw strong conclusions regarding the efficiency of the decision to incorporate in Nevada.

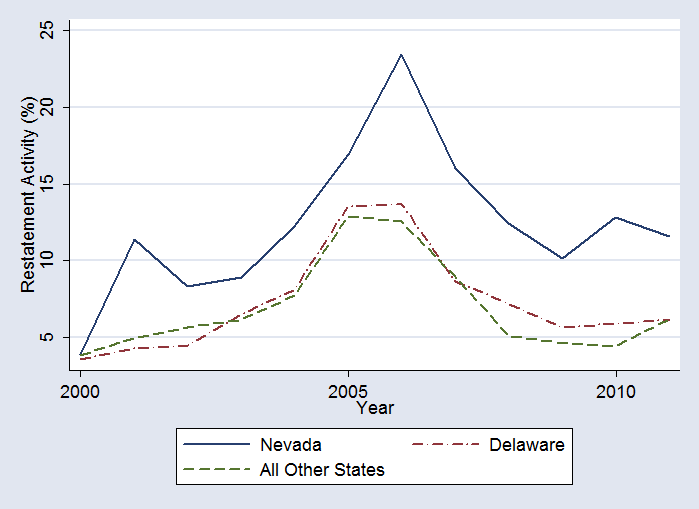

Figure 1. Financial restatement activity 2000–2011 for Nevada, Delaware, and other states

This figure compares financial annual restatement activity by graphing the annual percentage of publicly traded firms incorporated in Nevada, Delaware, and other states that report at least one restatement of their financial activities. Data on financial restatements are from Audit Analytics for the years 2000 through 2011. The number of publicly traded firms incorporated in each state is based on firms listed in Compustat during the same period.

The full paper is available for download here.

Endnotes:

[1] Figure 1 graphs the annual number of accounting restatements as a percentage of total public companies incorporated in Nevada, Delaware, and all other states for the years 2000 through 2011.

(go back)