Print

PrintAlicia H. Munnell is director of the Center for Retirement Research (CRR) at Boston College and the Peter F. Drucker Professor of Management Sciences at Boston College’s Carroll School of Management. Jean-Pierre Aubry is assistant director of state and local research at the CRR. This post is based on a CRR report by Ms. Munnell and Mr. Aubry.

In an effort to increase the visibility of pension commitments, the Governmental Accounting Standards Board (GASB) Statement 68 beginning in 2015: 1) moved pension funding information from the footnotes of financial statements to the balance sheets of employers; and 2) required employers that participate in so-called “cost-sharing” plans to provide information regarding their share of the “net pension liability” on their books as well. The Center for Retirement Research at Boston College recently completed a study that examined the impact of the new GASB rules on cities. Subsequently, the Center broadened the scope of the analysis and examined the impact on school districts and counties as well as cities, and the diminution of liabilities at the state level as a result of the reallocation.

“Cost-sharing” plans are a type of multiple-employer plan. GASB divides multiple-employer plans into two groups—agent plans and cost-sharing plans. In agent plans, assets are pooled for investment purposes but the plan maintains separate accounts so that each employer’s share of the pooled assets is legally available to pay benefits for only its employees. Until the new rules, funded information for employers in agent plans appeared in the notes of their financial statements, so the only change was to move that information into the balance sheet. In cost-sharing plans, the pension obligations, as well as the assets, are pooled, and the assets can be used to pay the benefits of any participating employer. Before the new rules, no information appeared for employers participating in cost-sharing plans. The new rules involve determining each employer’s share of the net pension liability and including that amount on the balance sheet.

Note that this calculation does not create new liabilities; it simply reallocates them from the state to the city.

The analysis uses a sample of 173 cities and towns, which includes cities that administer their own local plans, cities that participate only in state plans, and cities that have some combination of the two. In state cost-sharing plans, we allocated the state liability to cities based on their share of the Annual Required Contribution (ARC) and, if that information was not available, based on the ratio of actual city contributions to the actual state plan’s total contributions. One would think that other measures, such as the ratio of the city’s payrolls covered under the plan to the state plan’s total payrolls, might also be acceptable under GASB.

Of the 173 cities in our sample, 92 participate in cost-sharing state plans and were affected by GASB 68. For these 92 cities, the impact was substantial. The unfunded liability as a percentage of revenue rises from 37 percent before GASB 68 to 70 percent after. Moreover, some cities that escape scrutiny altogether when the focus is solely on locally-administered plans emerge as potential problems when the state burden is apportioned. For example, Newark, NJ, which does not administer a plan of its own and therefore is never included in studies of local plans, faces significant future demands on its revenue because it participates in three of New Jersey’s cost-sharing state plans. The impact on our full sample of 173 cities is more modest, because many of the 92 affected cities (within the group of 173 major cities) are relatively small.

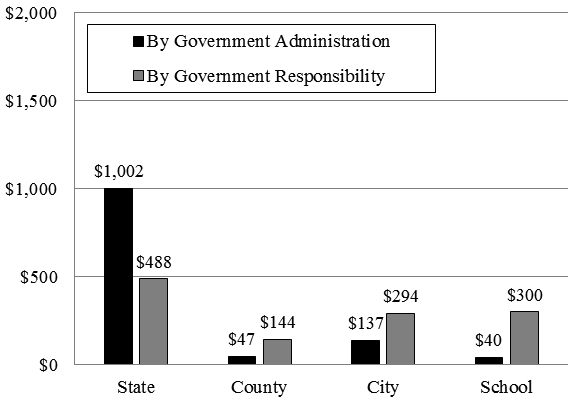

The broader study extended the analysis beyond cities to look at the impact of the reallocation among all units of government. The results are shown in Figure 1. When unfunded liabilities are reported by the level of plan administration, they appear clustered at the state level, with trivial amounts attributable to counties, cities, and school districts. Once the pension liabilities and assets are allocated to those entities participating in state-administered cost-sharing plans as required under GASB 68, the state responsibility is cut roughly in half, with school districts picking up the largest amount of the reallocation.

Figure 1. Pension Unfunded Liability

Source: Center for Retirement Research at Boston College.

The key question is whether the reallocation of pension burden from the state to cities will have any impact. Simply reporting part of state plan unfunded liabilities on local government balance sheets will not change the required payments made by local governments: their ARC already reflects their share of both the normal cost and the payment to amortize the unfunded liability of the state plan. But, local governments—now saddled with a portion of the state plan’s unfunded liabilities on their books—may be more interested in seeing the unfunded liability decline over time and will have a vested interest in ensuring that their contributions are doing just that. Only time will tell if accounting changes have any real impact.

The complete publication is available here.