Print

PrintAlberto Manconi is Assistant Professor of Finance at Bocconi University. This post is based on a forthcoming article by Professor Manconi; Elisabeth Kempf, Assistant Professor of Finance at University of Chicago Booth School of Business; and Oliver G. Spalt, Professor of Behavioral Finance at Tilburg University.

Do institutional shareholders have an unlimited capacity to monitor firms, or are they subject to attention constraints? And if they are, what are the consequences for firm governance? While a growing literature in economics studies limited attention, its impact on corporate actions is largely unexplored (few exceptions include Teoh, Welch, and Wong (1998a,b), and Hirshleifer and Teoh (2003)). In our article, forthcoming in the Review of Financial Studies, we aim to fill this gap by focusing on the link between managerial actions and temporary changes in the attention of the institutional shareholders of the firm. We exploit unique features of the U.S. institutional holdings data to show that managers respond to temporarily looser monitoring, induced by investors focusing their attention on other parts of their portfolio, by engaging in investments that maximize their private benefits at the expense of shareholders.

The key empirical challenge is that shareholder attention cannot be directly observed. To circumvent this difficulty, we exploit two important features of the institutional holdings data from 13f filings. Institutional investors are required to report their holdings on a periodic basis, so we can observe (i) the pool of institutional shareholders for each firm at a given point in time, and (ii) which other stocks each shareholder concurrently holds. These features of the data enable us to capture shifts in investor attention by looking at large price movements (“shocks”) in unrelated industries held by a given firm’s institutional shareholders to mark periods where shareholders are likely to shift attention away from the firm and towards the part of their portfolio subject to the shock. We then construct firm-level distraction measures by aggregating information about institutional investors for each firm, and we relate those measures to corporate actions.

The following thought experiment illustrates our empirical approach. Consider two otherwise identical firms 1 and 2 in a given industry and quarter. Firm 1’s representative shareholder holds two stocks: firm 1 itself, and another firm belonging to a different industry, say “banks.” Firm 2’s representative shareholder, on the other hand, does not hold any bank stocks. Suppose now there is an attention-grabbing event in the banking industry; for example, a banking crisis. Assuming limited attention, the representative shareholder in firm 1 may—potentially rationally—shift attention towards banks and away from firm 1. As a result, monitoring at firm 1 is looser, and firm 1’s management has more room to pursue private benefits. In contrast, firm 2 is unaffected. We can therefore identify the impact of variation in investor attention by analyzing changes in policies of firm 1 relative to firm 2 around the time of the exogenous shock. Motivated by Barber and Odean (2008), we use “extreme” industry returns (both positive and negative) as our main empirical proxy for attention-grabbing events. We call shareholders with a larger exposure to shocks in unrelated parts of their portfolios “distracted.”

What happens when shareholders are distracted is an empirical question. Potentially, policies at firm 1 do not change—for example, if other governance mechanisms (e.g., boards) can substitute for shareholder monitoring. Alternatively, managers might react by becoming passive and “enjoying the quiet life” (Bertrand and Mullainathan (2003)). Finally, managers might actively seek to maximize private benefits. Our results provide strong evidence for the latter scenario.

A first set of tests establishes that our proposed proxy indeed measures lack of investor attention. When our proxy indicates a high level of distraction, fewer questions are asked during earnings conference calls. Further, we find that institutional investors are less likely to make proposals in shareholder general meetings, and they are less likely to make large changes to their portfolios. These patterns are consistent with a diversion of shareholder attention (i.e., distraction), and support our conjecture that attention is not unbounded for institutional investors.

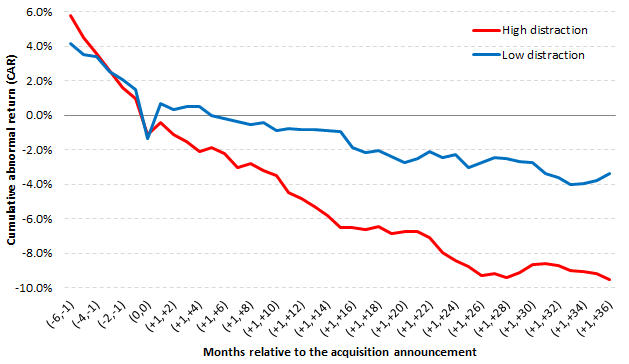

Our main finding is that, when shareholders are distracted, managers make more value-destroying acquisitions. Our baseline tests show that the probability of making an acquisition increases by 29% for a one-standard-deviation increase in investor distraction. They also indicate that these are likely bad deals. First, the distraction effect is concentrated in diversifying acquisitions, which are commonly thought to disproportionately benefit managers, for reasons of empire building or job security through more stable cash flows (e.g., Amihud and Lev (1981) and Morck, Shleifer, and Vishny (1990)). Second, bidder and combined bidder and target announcement returns (“synergies”) are lower, relative to the average, when shareholders are more distracted. Third, over the three-year period following the deal, bidding firms have significantly lower stock returns if shareholders are distracted at the announcement, as illustrated in Figure 1. All these results are consistent with the idea that managers take advantage of looser monitoring by tilting capital budgets towards acquisitions that may be privately optimal, but are value-destroying for shareholders.

Figure 1— Stock performance around the acquisition announcements

The graph plots the long-run cumulative abnormal returns of bidder stocks for the subgroups of high and low distraction. High- (low-) distraction stocks are those with above (below) median distraction in a given bidder industry and announcement year. Abnormal returns are calculated using Ibbotson’s (1975) returns across time and securities (IRATS) method, combined with the Fama-French three-factor model.

Additional evidence suggests the effect of shareholder distraction is not specific to takeovers. Building on work by Bebchuk, Grinstein, and Peyer (2010), we show that CEOs are more likely to receive opportunistically timed (“lucky”) equity grants when shareholders are distracted. This test is useful because lucky grants are (i) directly related to managerial wealth, (ii) unlikely related to economic fundamentals at the granting firm, and (iii) in no obvious way related to our merger analysis. We also find that when shareholders are distracted, firms are more likely to cut dividends and CEOs are less likely to be fired after bad performance. Consistent with the idea that distraction is costly for shareholders, a portfolio strategy long in firms with non-distracted shareholders and short in firms with distracted shareholders earns significant abnormal returns.

In sum, our findings indicate that shareholder distraction has an economically important impact on a broad range of corporate actions, including the likelihood of announcing a merger, merger performance, CEO pay, dividend cuts, and stock returns. A unifying explanation is that managers maximize their own private benefits at the expense of shareholders at times when institutional investors focus their attention elsewhere. Our results suggest that analyzing managerial responses to temporally relaxed monitoring constraints may significantly improve our understanding of value creation in firms.

The full article is available for download here.

References

Amihud, Y., and B. Lev. 1981. Risk Reduction as a Managerial Motive for Conglomerate Mergers. Bell Journal of Economics 12:605-17.

Barber, B. M., and T. Odean. 2008. All that glitters: The effect of attention and news on the buying behavior of individual and institutional investors. Review of Financial Studies 21:785-818.

Bebchuk, L. A., Y. Grinstein, and U. C. Peyer. 2010. Lucky CEOs and Lucky Directors. Journal of Financial Economics 65:2363-401.

Bertrand, M. and S. Mullainathan. 2003. Enjoying the quiet life? Corporate Governance and Managerial Preferences. Journal of Political Economy 111:1043-75.

Hirshleifer, D., and S. H. Teoh. 2003. Limited Attention, Information Disclosure, and Financial Reporting. Journal of Accounting and Economics 36:387-400.

Ibbotson, R. G. 1975. Price performance of common stock new issues. Journal of Financial Economics 2:235-72.

Morck, R., A. Shleifer, and R. W. Vishny. 1990. Do Managerial Objectives Drive Bad Acquisitions? Journal of Finance 45:31-48.

Teoh, S. H., I. Welch, and T. J. Wong. 1998a. Earnings Management and the Long-Run Market Performance of Initial Public Offerings. Journal of Finance 53:1935-74.

Teoh, S. H., I. Welch, and T. J. Wong. 1998b. Earnings Management and the Underperformance of Seasoned Equity Offerings. Journal of Financial Economics 50:63-99.