Print

PrintSteve Lydenberg is Founder and CEO of The Investment Integration Project (TIIP). This post is based on a TIIP publication by Mr. Lydenberg. The complete publication, including footnotes, is available here.

This post addresses the question of how asset owners and managers can identify environmental, societal and financial systems-level issues relevant to their investment processes. Integration of these systems-level considerations can help investors manage long-term risks and rewards while seeking competitive portfolio-level returns.

The primary questions addressed in this post are:

- What are the characteristics of environmental, societal and financial systems-level issues that make them relevant to long-term investors for integration into investment processes?

- What are examples of these systems-level issues that rise to the level of significance for such consideration and how in practice can that level of significance be determined?

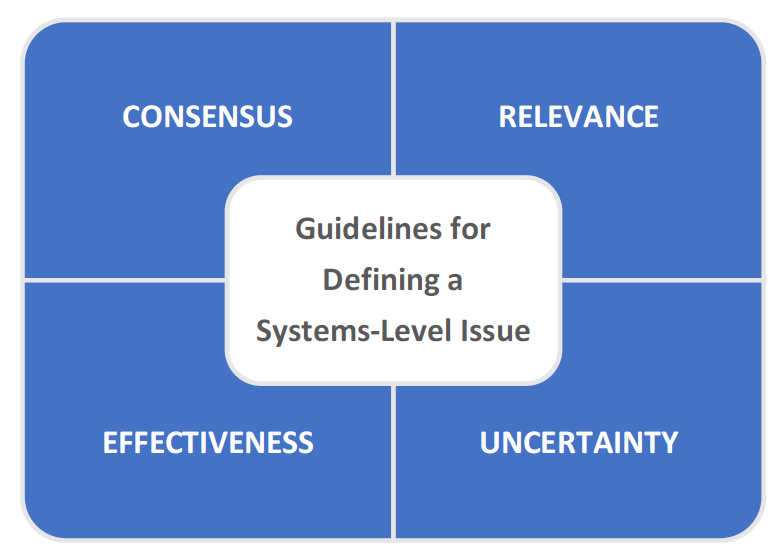

Four guidelines that can help long-term investors determine the relevance of systems under consideration are proposed:

- Breadth of consensus as to the importance of the system under consideration

- Potential of the feedback loops from the system to impact the investor’s portfolios positively or negatively

- Potential for the investor’s policies and practices to impact the system positively or negatively

- Degree of uncertainty about the potential outcomes that would ensue from fundamental disruptions at the systems level

The post examines six examples of systems-level issues that share these characteristics.

Within broad environmental systems, the paper looks at the issues of:

- Climate change

- Access to fresh water

Within broad societal systems, it looks at the issues of:

- Well-being: poverty alleviation and access to healthcare

- Dignity: human and labor rights

Within broad financial systems, it looks at the issues of:

- Stability and credibility

- Transparency of sustainability data

Resolution of the question of which issues do and do not appropriately rise to the level of systems-level consideration is crucial for institutional investors because issues with too narrow a focus may prove irrelevant, ineffective or even potentially detrimental to their management of long-term risks and rewards.

Introduction

Asset owners and their managers striving for long-term value creation and matching today’s assets with tomorrow’s liabilities benefit from the stability and predictability of the environmental, societal and financial systems within which investment takes place and upon which they depend for profitable long-term returns. Economic crises, financial boom and bust cycles, ecosystems under stress, societies rocked by unrest and turmoil—all can disrupt these systems and the best-laid plans of investors, and cost them dearly.

The global financial crisis of 2008 starkly demonstrated how instabilities in the highly sophisticated, globalized financial systems of today can bring this carefully constructed infrastructure to the brink of collapse and cause dramatic losses across all asset classes. The looming investment uncertainties of climate change are a contemporary reminder that fundamental disruptions in our environmental systems can raise the specter of “unhedgeable” financial risks across the board.

Long-term investors have increasingly come to recognize the importance of environmental, social and governance risk management (so called “ESG factors”) in security selection and portfolio construction. They are also beginning to make corresponding progress in understanding the broader context of their investment impacts—that is, how their investment policies and practices minimize risks and maximize rewards at the systems level, while simultaneously generating competitive returns.

This post identifies ways in which institutional investors with long investment time horizons can relevantly engage in systems-level thinking and identify systems-level issues that will help manage the risks and increase the rewards at these levels. Specifically, this post addresses the question of what constitutes systems-level issues significant enough for integration into the investment process.

The primary questions addressed in this post are:

- What are the characteristics of environmental, societal and financial systems-level issues that make them relevant to long-term investors for integration into investment processes?

- What are examples of these systems-level issues that rise to the level of significance for such consideration and how in practice can that level of significance be assessed?

Many issues are encompassed in considerations of environmental sustainability, the creation of a just and prosperous society, and the maintenance of a smoothly functioning financial system. For institutional investors, however, not all of these can—or should—rise to the level of “relevant for consideration.”

Too narrowly conceived, an issue may be an expression of personal or political preference with no true impact at the systems level; may blind investors to important financial considerations; may introduce market distortions or inefficiencies; or may entail conflicts of interest or the appearance of such conflicts.

It is therefore crucial to establish guidelines for identifying those issues that are relevant—that is, are broadly agreed upon to play a key role in well-functioning systems; may affect the systems’ potential to impact investor’s long-term returns; may potentially have impact on these systems; and may reduce the general scope of systemic uncertainty that investors face.

Framing the Issue

Momentum of Responsible Investment

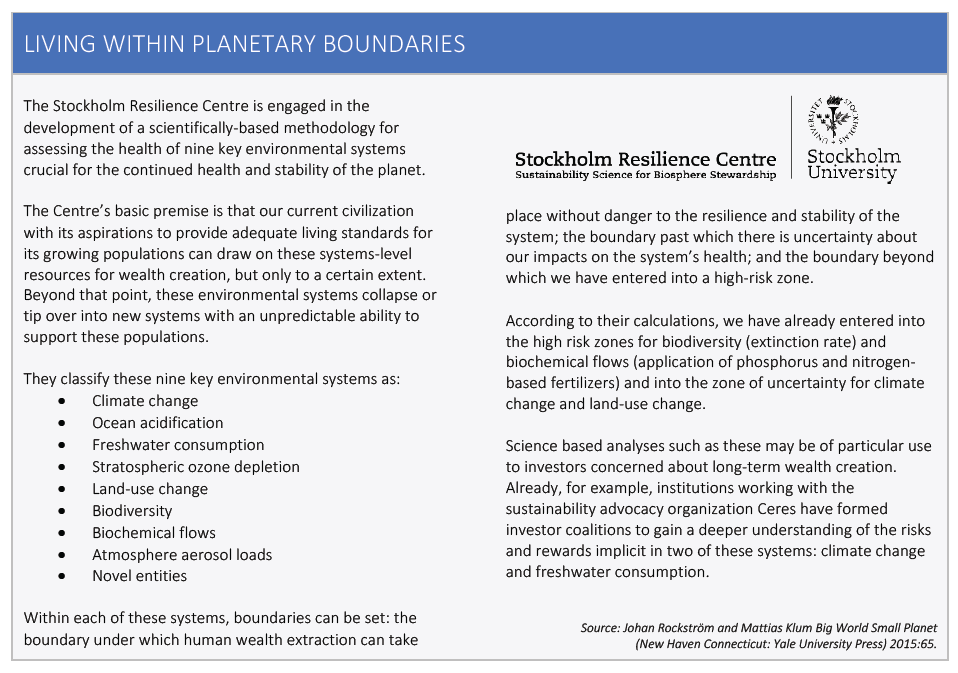

We never expected to destabilize the Greenland ice sheet, West Antarctic glaciers, tropical coral reefs, or the Siberian tundra simply by the way we ran our local economies.”

—Johan Rockström and Mattias Klum

Big World Small Planet

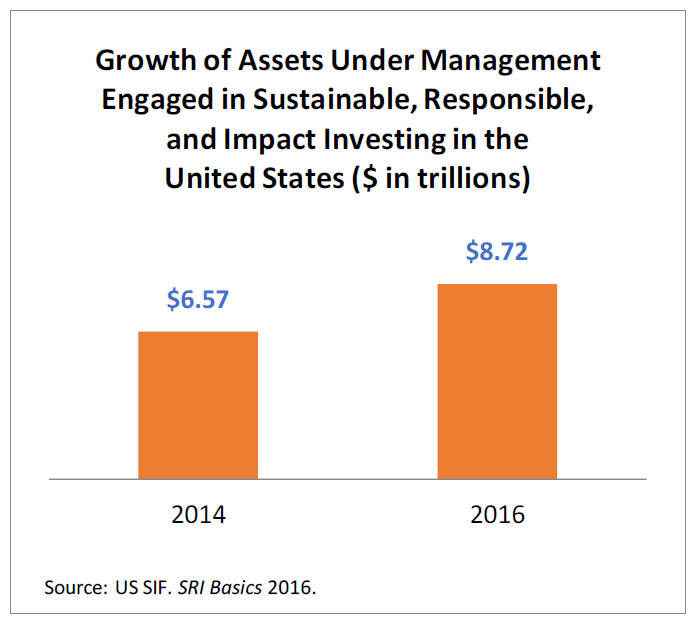

As we continue to be concerned about the state of our environment, progress in human well-being and the stability of our financial systems, interest in the constructive role that investment can play in their support is increasing. Responsible investment is currently one of the fastest growing segments of the financial markets, with assets under management engaged in sustainable, responsible and impact investing in the United States increasing from $6.57 trillion in 2014 to $8.72 trillion in 2016. Asset owners, managers and service providers who are signatories to the UN Principles for Responsible Investment totaled more than 1,600 as of late-2016. And an ever-increasing number of mainstream managers now incorporate ESG factors into their security valuation, portfolio construction and engagement with corporations.

Organizations such as the Global Reporting Initiative have developed robust methods to promote disclosure of corporate ESG data. The Sustainability Accounting Standards Board and others have identified industry-level sustainability key performance indicators. These ESG data points have proven particularly valuable in portfolio-level stock selection and asset allocation.

Similarly, in the realm of investment products, many, if not most, mainstream asset managers now offer an ever-broadening range of products with an ESG tilt. In 2013 Morgan Stanley launched its Institute for Sustainable Investing. In 2015 Blackrock introduced its Impact Equity Funds and Goldman Sachs acquired the impact investment boutique firm Imprint Capital. In 2016 the private equity firm Bain Capital launched its Double Impact fund, targeting companies with a focus on sustainability, health and wellness, and community building; and Eaton Vance acquired long-time responsible investment leader Calvert Investments.

Responsible investment has earned its place at the table, but the question remains as to whether it will progress beyond the niche market status it has attained.

From Portfolio to Systems and Back Again

Increasingly, institutional investors are being called upon to manage risks and rewards at systems levels. In May 2016, for example, the International Corporate Governance Network issued its Global Stewardship Principles, stating, among other things, that:

Investors should build awareness of long-term systemic threats, including ESG factors, relating to overall economic development, financial market quality and stability and should prioritize mitigation of system-level risk and respect for basic norms (e.g. anti-corruption, human rights) over short-term value.

Similarly, in September 2016 the Principles for Responsible Investment published Sustainable Financial System: Nine Priority Conditions to Address, a comprehensive overview of fundamental considerations for aligning our financial system with the long-term interests of investors and society. This study follows the series of papers published under the banner of The Financial System We Need through the United Nations Environmental Program’s Financial Initiative (UNEP FI). These reports lay out a program for reform of the financial system aimed at “aligning the financial systems with sustainable development.”

More particularly, progress is being made in developing practical and theoretical tools for measuring and analyzing the effects of investment policies at systems levels. In November 2016, in conjunction with Demos (a public policy organization focused on issues of democracy and reducing inequality, among others), UNEP FI published Towards a Performance Framework for a Sustainable Financial System, which proposed five principles for evaluating a market’s sustainability and inclusiveness. These principles focus on capital requirements, financial flows, resiliency, efficiency and effectiveness.

In its Winter 2017 issue, the Stanford Social Innovation Review published two articles documenting progress made by the Omidyar Network and Root Capital in conceptualizing investment frameworks that allow for the integration and measurement of two factors simultaneously. In Root Capital’s vocabulary they are “expected return” and “expected impact”; in Omidyar’s they are “financial impact” and “market impact”.

These studies follow on work relating environmental and societal systems-level crises to portfolio impacts. In October 2014, the Center for Risk Studies at the University of Cambridge published Social Unrest: Stress Test Scenario—Millennial Uprising Social Unrest Scenario, which ties the impact of various scenarios for social unrest in the 21st century to potential portfolio-level impacts. In November 2015, the Cambridge Institute for Sustainability Leadership published Unhedgeable Risk: How Climate Change Sentiment Impacts Investment, which projected the impacts of varying climate change scenarios on portfolios of varying risk tolerances.

Systems-Level Considerations

The concept of incorporating systems-level considerations into investment decision-making complements, but is distinguishable from, that of ESG integration into portfolio management, which has recently gained considerable currency. Systems, as the term is used here, refers to the vast set of what are essentially common-pooled environmental and societal resources upon which investors draw to create long-term wealth—with the public benefits that the effective management of these resources brings. ESG integration, by contrast, typically refers to integration of environmental, social and governance factors into the efficient management of the risk and reward profile of portfolios’ investment strategies, resulting in essentially private, rather than public, benefit.

As the 21st century progresses, investors will likely find it increasingly necessary to operate with both goals in mind—the private and the public, the portfolio and the systems. Our assumption in this post is that investors can indeed help preserve and enhance the wealth-creating potential of these systems, as they efficiently manage the risks and rewards of their portfolios.

Preservation is a concept particularly useful for environmental systems whose physical resources we have inherited. Enhancement is helpful for societal and financial systems, which are constantly in flux as we debate, innovate, regulate and disrupt in ongoing efforts to increase their long-term value-generating potential.

This focus on preservation and enhancement will be driven by a variety of relatively predictable factors in this century. The world’s population will grow to between 9 and 11 billion by its end; will be more prosperous, with better access to communications, transportation and technology; and will have legitimate aspirations for ever-higher standards of living. The societal systems necessary to house, feed, clothe and employ that population will be ever-more complex and interconnected and will place ever-greater demands on our environmental systems—that is, the air, land and water on which we depend for survival.

Finance, and institutional investors in particular, can play a substantial role in the preservation and enhancement of these systems, a role that is likely to increase as the century progresses. It is in their self-interest to do so because their ability to generate long-term returns ultimately depends on the health and stability of these systems.

By elaborating the basic characteristics of systems-level considerations relevant to investment, this post attempts to take a concrete, practical step toward creation of processes applicable to the management of system-level issues—ones that help maximize long-term value creation and minimize value destruction in an increasingly complex and interconnected world.

Guidelines for Issue Selection

A crucial initial step for long-term institutional investors focusing on systems-level issues is to determine which issues are in fact worthy of their attention. This post offers four guidelines for making that selection. These are consensus, relevance, effectiveness and uncertainty. The choice of issues that can be considered relevant might seem on one level so simple as to not require serious thought. Of course we want stable and thriving environmental, societal and financial systems in order to make investments: consequently, any issues involving their preservation or enhancement should be legitimate.

In practice, however, the possibility for confusion and even abuse exists. “Systems-level considerations” is a broad concept capable of multiple interpretations. Issues proposed for consideration might be idiosyncratic and without broad-based agreement as to their relevance; might be widely agreed-upon but have little of implication for investments; might be too narrowly conceived to have substantive impact at a systems level; or might simply be covers for personal or political gain and hence involve conflicts of interest.

Four Guidelines

We offer here four guidelines as tools to assist long-term investors in assuring that a given systems-level issue can be viewed as legitimate and worthy of consideration. These guidelines focus attention on a relatively limited number of issues of overriding systems-level relevance with substantial long-term financial implications.

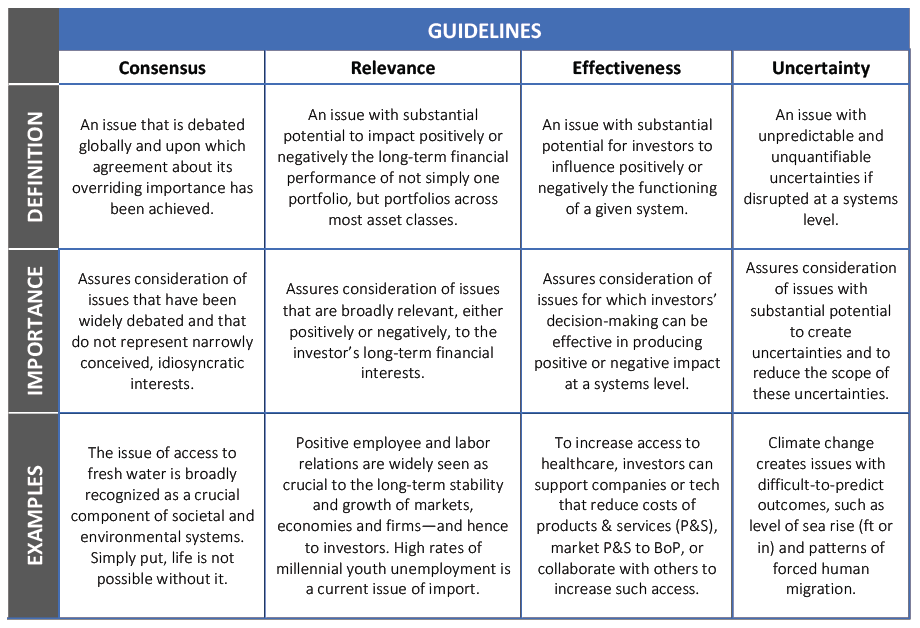

Guideline 1: Consensus

An issue can be judged as reasonable for consideration if it has achieved a broad consensus as to its legitimacy and general importance, whether positive or negative. The broader that consensus the stronger the case for its consideration. Because these issues have achieved consensus as to their legitimacy among a broad range of stakeholders, they can be viewed as involving a shared good, not simply the private good of self-interested rationality.

This guideline is intended to assure that institutional investors consider issues that have been widely debated and do not represent narrowly conceived, idiosyncratic interests.

For example, the issue of access to fresh water is broadly recognized as a crucial component of societal and environmental systems. With about one-fifth of the world’s population, or 1.2 billion persons, living in regions of water scarcity as of 2007, the availability of fresh water in the 21st century is emerging as a systems-level issue of overriding importance. Exemplifying consensus on this issue was the 2010 declaration by the United Nations that access to water is a human right. In its 2015 annual Water World Development report, the UN highlighted water’s critical role in poverty reduction, economic growth and environmental sustainability affecting the lives and livelihoods of billions. Without water, life itself is not possible.

Guideline 2: Relevance

An issue can be judged relevant for consideration if it has a substantial potential to impact positively or negatively the long-term financial performance of not simply one portfolio or asset class, but portfolios across most investors and asset classes. The greater that potential relevance, the stronger the case for its consideration. Because such issues impact portfolios across multiple asset classes and investors, they can be viewed as favoring not simply the interests of individual investors, but investors in general and hence the broader public.

This guideline is intended to assure that institutional investors are considering systems-level issues that are broadly pertinent to their long-term financial interests. Matters of the price-related financial performance of specific investments can be addressed through risk analysis at the portfolio level. For issues with longer-term investment impacts across multiple asset classes—particularly those that result from secular changes, long-tail disruptions or scientific or geopolitical uncertainties—a systems-level view can be helpful.

For example, the issue of dignity in the workplace as expressed in employee and labor relations and opportunities to work is widely recognized as crucial to the long-term stability and growth of markets, economies and individual firms—and hence to investors. The International Labor Organization, founded in 1919 after World War I, developed labor-related principles endorsed by a wide spectrum of countries to prevent unfair labor practices “involving such injustice, hardship and privation to large numbers of people as to produce unrest so great that the peace and harmony of the world are imperiled.”

Highlighting the current investment relevance of employment concerns, the 2014 study Millennial Uprising Social Stress Scenario by the University of Cambridge Centre for Risk Studies examined the potential impacts across a variety of portfolios under various scenarios of global social unrest stemming from lack of employment opportunities for millennial youth. In addition, various academic studies have documented the correspondence between positive employee relations and the long-term stock performance of individual corporations.

Guideline 3: Effectiveness

An issue can be considered effective if institutional investors have the ability to influence the functioning of a given system, either minimizing potential risks or maximizing rewards. The greater the potential of influence on that system, the stronger the case for consideration. Because risks and rewards are being managed at a systems level, investors are providing a common benefit as well as an individual one.

This guideline is intended to assure that institutional investors are considering issues for which their time and resources expended can be effective in producing positive impact upon the systems of relevance to them or in minimizing negative impacts on these systems.

For example, institutional investors can have a positive impact on access to healthcare through a variety of policies and practices. They can invest in specific companies or technologies that bring down the costs of healthcare products and services. They can invest in those marketing healthcare products and services to individuals and families at the bottom of the pyramid. They can collaborate with governmental, non-governmental and corporate organizations working to increase such access. Multiple avenues can provide investors with effective inputs with regards to this systems-level issue.

Guideline 4: Uncertainty

An issue can be judged reasonable for consideration if it involves difficult-to-assess uncertainties in the event of systems-level disruption, whether the trends of these uncertainties are positive or negative. The greater the potential for uncertainty due to systems-level disruptions, the stronger the case for consideration of these issues. Because systems-level uncertainties have implications for all portfolios and investors, not simply one, this characteristic relates to shared, rather than individual, value.

This guideline is intended to assure that institutional investors consider those issues with substantial potential to create uncertainties and to reduce the scope of these uncertainties. It reflects the fact that long-term investors must always contend with what John Maynard Keynes called “the dark forces of time and ignorance which envelop our future.” It is crucial for long-term investors to understand if their actions are increasing the unpredictability and future uncertainty for potential systems-level disruption —and to decrease it whenever reasonably possible within the constraints of prudent investment decision-making.

For example, the looming issue of climate change involves unpredictabilities of such broad scope that incorporating them into today’s investment policies and practices becomes a major challenge. Today scientists have difficulty in predicting something as relatively straightforward as the rate that sea levels around the world will rise during the 21st century. Even greater are uncertainties such as predicting the migration patterns that will be caused by these increases in sea levels and the social and political impact of this migration. Such basic questions as whether major coastal centers of civilization will survive or whether nations around the world will accept climate-change refugees are virtually impossible to incorporate into today’s stock valuations. To the degree that investors’ decision-making can minimize the likely severity of climate change, it will also minimize the unpredictabilities that climate change is likely to bring.

Issues that share these four characteristics—consensus, relevance, effectiveness and uncertainty—are those that will be of sufficient concern that long-term investors can reliably treat them as credible.

Examples of Systems-Level Issues

The following are six examples of systems-level issues that long-term institutional investors might consider as relevant. For each example, an explanation is provided as to why it may be viewed as aligned with the four general guidelines proposed above. The purpose of these examples—two each for environmental, societal, and financial systems—is to provide a sense of when an issue generates broad consensus, impacts long-term investments, can be influenced by investors, and involves substantial unpredictability—all to a degree sufficient to rise to a level of a relevant consideration.

Environmental Systems

The environment, broadly speaking, can be viewed as the overarching physical network that makes up the biosphere of the Earth: that is, the complicated ecology of natural phenomena that constitutes the physical surroundings in which we live. Our investments assume the continued existence of this environment as a source of wealth generation necessary for future prosperity.

The environment writ large is made up of a number of interrelated systems: the atmosphere, the oceans, fresh water, arable land, the biodiversity of life on land and in the seas, and the geological features of the Earth’s crust and resources that can be extracted from them, among others. By way of example, we illustrate how two of those systems—climate change (in the atmosphere) and access to fresh water—possess the fundamental characteristics outlined in the guidelines above.

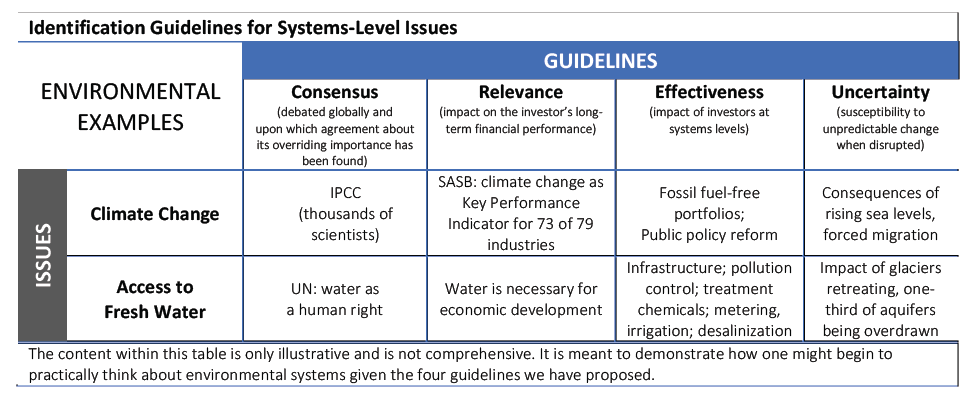

Climate Change

Guideline 1: Consensus

A global consensus as to the importance of preserving the stability of the current chemical make-up of our atmosphere has been established by the Intergovernmental Panel on Climate Change (IPCC), a network of several thousand atmospheric and oceanic scientists. The IPCC’s reports, issued every five to seven years since 1990, have documented on-going changes in the chemistry of the atmosphere and the uncertain consequences of those changes.

Guideline 2: Relevance

Through the mechanism of climate change, the ecosystem can profoundly affect investments. A study by the University of Cambridge Institute for Sustainability Leadership, for example, has projected considerable range of the unhedgeable—that is to say, unavoidable—consequences for portfolios of climate change under various scenarios. Similarly, a study by the Sustainability Accounting Standards Boards found climate change to be a “systemic risk”—that is to say, a material sustainability key performance indicator—for 73 of 79 industries that make up the economy.

Guideline 3: Effectiveness

A wide range of investment vehicles are currently being developed with the aim of reducing greenhouse gas emissions and thereby reducing the likely impacts of climate change. These include fossil fuel-free portfolios, portfolios with reduced exposure to carbon emissions and specialty funds investing in clean technologies and alternative energy. Institutional investors also have opportunities to support global public policy initiatives to reduce greenhouse gas emissions or to mandate disclosure of climate change-related data and risks; to contribute to sustainability initiatives within the financial system; and, to partner with peers and non-governmental organizations to promote industry standard-setting aimed at achieving climate-change risk reduction.

Guideline 4: Uncertainty

The uncertainties surrounding climate change and its long-term implications for investment are substantial. Scientists have difficulty predicting something as straightforward as the timing and levels of anticipated rises in sea levels, let alone the societal impacts—including those of forced migration—that will result. It is challenging to make reasonable long-term investment decisions when as investors we don’t know such basics as whether major coastal centers of civilization will survive or whether basic weather patterns will change in fundamental ways. Steps taken to lessen that uncertainty are in the long-term interest of investors.

Access to Fresh Water

Guideline 1: Consensus

With about one-fifth of the world’s population, or 1.2 billion persons, living in regions of water scarcity as of 2007, it is not surprising that the availability of fresh water in the 21st century is emerging as a systems-level issue of both overriding economic and environmental importance. Fresh water plays an essential role in systems supporting life on land as well as many crucial aspects of our economy. In 2010, the United Nations declared water a human right. In its 2015 annual Water World Development report, the UN highlighted its essential roles.

Water resources, and the range of services they provide, underpin poverty reduction, economic growth and environmental sustainability. From food and energy security to human and environmental health, water contributes to improvements in social well-being and inclusive growth, affecting the livelihoods of billions.

Guideline 2: Relevance

Numerous studies have documented the importance of the availability of high-quality fresh water to economic development and hence to long-term investment opportunity. Water capacity constraints can limit the growth of industry. The pollution of rivers and ground water can cause health problems and impact food and beverage production. Drought can devastate economies and kill through famine when crops wither and die. Workforce productivity can be lost to illness from contaminated drinking water and to the demands on domestic time in obtaining water in many regions.

Guideline 3: Effectiveness

A wide array of investment opportunities that can positively impact water-related challenges has materialized in recent years. Investment opportunities abound for increasing the availability of water, improving its efficiency and assuring its quality. These include water infrastructure systems, wastewater treatment systems, pollution control devices, water usage metering, irrigation equipment, desalinization technologies, and filtration and pumping products, among many others. In addition, as the importance of water as an investment theme gains recognition, opportunities for investors to work collaboratively to effect positive change, such as the Ceres Investor Water Hub, are taking shape.

Guideline 4: Uncertainty

The long-term social and economic consequences of the fact that glaciers worldwide are in retreat and an estimated one-third of aquifers worldwide being overdrawn are fundamentally unpredictable. If the resilience and stability in access to water accounted for by glaciers and aquifers are lost, the consequences will be highly unpredictable.

An estimated two billion persons living in a dozen Asian countries depend on rivers such as the Ganges, Indus, Yangtze and Mekong, which are fed in large part by the dependable runoff from thousands of glaciers in the high Tibetan plateau. California’s fruitful farms depend on the reliability of the Sierra Nevada snowpack for much of their summer water supply. Midwestern farmers draw upon the vast aquifers of that region.

Societal Systems

Societies are made up of the historical, cultural and legal structures that constitute the systems within which communities operate and human interactions take place. These systems consist of a complex network of institutions, goals, standards, beliefs and customs. They have evolved to serve certain broadly agreed-upon purposes including the assurance of well-being, dignity, equality, health, opportunity, fair working conditions, impartiality of the law, and transparent markets, among others.

By way of example, we will illustrate how two of those systems—well-being (focused on poverty alleviation and access to healthcare) and dignity (focused on human and labor rights)—possess the fundamental characteristics outlined in the guidelines above.

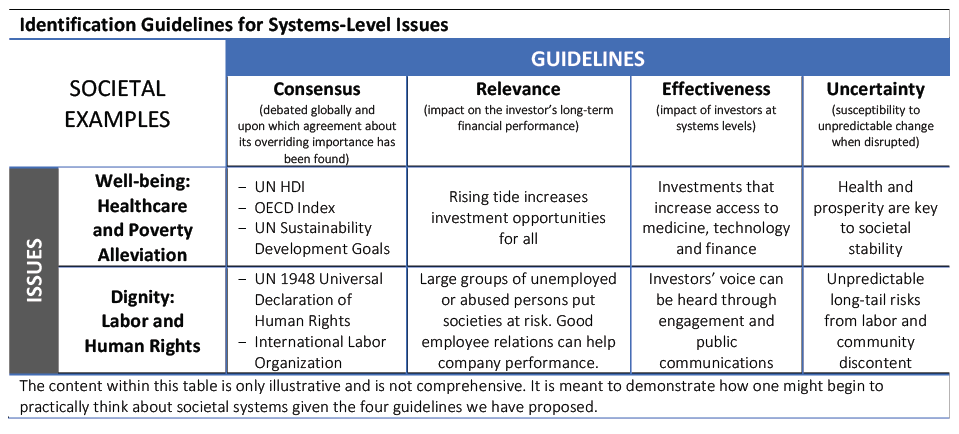

Well-Being (Poverty Alleviation and Access to Healthcare)

Guideline 1: Consensus

It is widely agreed that providing for the well-being of its members is a primary function of a well-ordered society. Well-being can be measured in many different ways. Freedom from extreme poverty and the provision of adequate healthcare are typically considered key components of this well-being.

The United Nations Human Development Index (HDI) states that “people and their capabilities should be the ultimate criteria for assessing the development of a country, not economic growth alone.” It measures such factors as people’s ability to have “a long and healthy life” and have “a decent standard of living.” The Organization for Economic Cooperation and Development’s Better Life Index rates countries on 11 factors including income and health. The first of the UN’s Sustainable Development Goals, is to “end poverty in all its forms everywhere” and the third is to “ensure healthy lives and promote well-being for all at all ages.”

Guideline 2: Relevance

Poverty alleviation can create powerful sources of investment opportunity. For companies and investors creating markets for the four billion people at the bottom of the pyramid “the prospective rewards include growth, profits and incalculable contributions to mankind.” Increased access to healthcare can spur local economies and create investment opportunities. The link between healthcare and poverty reduction, for example, has been extensively documented and with improved healthcare services come new investment opportunities. As the World Health Organization puts it:

Better health is central to human happiness and well-being. It also makes an important contribution to economic progress, as healthy populations live longer, are more productive, and save more.

Guideline 3: Effectiveness

Investors are well-positioned to identify opportunities that directly impact the health and economic well-being of societies including those most in need. Investments in vaccines can prevent diseases that not only keep citizens from leading productive lives but cost society dearly in their treatment. Similarly, investment in low-cost generic pharmaceuticals can keep the healthcare costs of societies under control. Investments in mobile telephone firms can contribute to wealth creation in poor, rural regions. Unilever has taken on investments in poverty reduction as a basic business strategy in the consumer products area. Such strategies can generate a rising tide of investment opportunities across multiple asset classes.

Guideline 4: Uncertainty

A healthy population free from extreme poverty is an essential component of a resilient economy capable of withstanding the unpredictable, but inevitable, exogenous shocks that will occur. For example, without a strong, local healthcare infrastructure in place, the 2014 outbreaks of Ebola in Western Africa led to crises that effectively shut down national economies.

Dignity (Human and Labor Rights)

Guideline 1: Consensus

Since the end of the 18th century, national governments have placed an increasing emphasis on the expectation that their citizens are entitled to live lives of basic human dignity. In 1948, the United Nations enshrined these expectations in its Universal Declaration of Human Rights. Broadly endorsed throughout the world, the declaration begins with a recognition “of the inherent dignity and of the equal and inalienable rights of all members of the human family” and goes on to spell out the conditions essential for a dignified life.

Similarly, in its 1919 founding document, the International Labor Organization addressed the globally destabilizing consequences of unfair labor practices “involving such injustice, hardship and privation to large numbers of people as to produce unrest so great that the peace and harmony of the world are imperiled.” Part of the mission of this widely recognized international tripartite organization under the guidance of representatives from labor, business and governments was to help assure peace in the wake of the economic and societal devastation of World War I.

Guideline 2: Relevance

In addition to fundamental concerns about economic stability and the maintenance of world peace, labor and human rights abuses can lead to damage to company and industry reputations, short- and long-term financial losses, and disasters as catastrophic as the 1984 release of toxic chemicals from a Union Carbide plant in Bhopal, India, which led to more than 3,700 deaths and an estimated 500,000 injuries. The 2014 study Millennial Uprising Social Stress Scenario by the University of Cambridge Centre for Risk Studies called attention to the potential impacts across portfolios under various scenarios of social unrest stemming from lack of employment opportunities for millennial youth around the world in the 21st century.

Conversely, numerous studies have documented the long-term benefits of positive employee relations. For example, a recent study found that in flexible labor markets such as the United States, “employee satisfaction is associated with positive abnormal returns,” although in more highly regulated markets where “legislation already provides minimum standards for worker welfare” the correlation is not strong.

Guideline 3: Effectiveness

Through their investment policies and practices, institutions can factor labor and human rights considerations into firm- and industry-level risk analysis; through engagement they can call corporations’ attention to long-term reputational risks from poor management of these issues; and through communications they can raise public awareness of the relevance of such abusive practices as child and bonded labor.

Guideline 4: Uncertainty

Abuses of labor and human rights can result in unrest of an unpredictable sort. In the short run, adverse consequences range from simple loss of productivity or shutdowns of operations due to strikes or community opposition. In the longer run, they can include widespread civil unrest and a company’s or industry’s loss of societal faith and license to operate. Even more fundamentally, labor and human rights abuses have the potential to undermine credibility in the legal corporate structure and that of markets in general. It is in the long-term interest of investors to incorporate policies and practices that minimize the likelihood of these unpredictable adverse effects.

Systems-Level Issues and the Sustainable Development Goals

In 2016, the United Nations announced its 17 Sustainable Development Goals (SDGs)—a “universal call to action to end poverty, protect the planet and ensure that all people enjoy peace and prosperity.” Since then a number of investors—including Aviva, PGGM and Sonen Capital, as well as the UNEP Financial Initiative and the Cambridge Institute for Sustainability Leadership—have begun to explore ways to align investment activities with specific SDGs. Although presented as goals, these ambitious targets for human well-being and environmental sustainability also have the characteristics of systems-level issues as outlined in this post, and can consequently serve as a resource for investors seeking to identify issues that help preserve and enhance the basic environmental, societal and financial frameworks within which long-term investment take place.

Financial Systems

Our financial system consists of a globally interlocking network of laws, regulations, institutions and customs that enable the smooth functioning of markets. Its stability and preservation are of essential importance to investors.

Finance is bound up with the cultural customs and political histories of national economies and manifests itself in diverse ways on local, national and regional levels. Nevertheless, certain interrelated fundamentals are generally agreed upon as underpinning efficient and effective financial systems, including stability, trust, credibility, inclusiveness and transparency.

By way of example, we illustrate how two of those systems—stability and transparency of sustainability data—possess the fundamental characteristics outlined in the guidelines above.

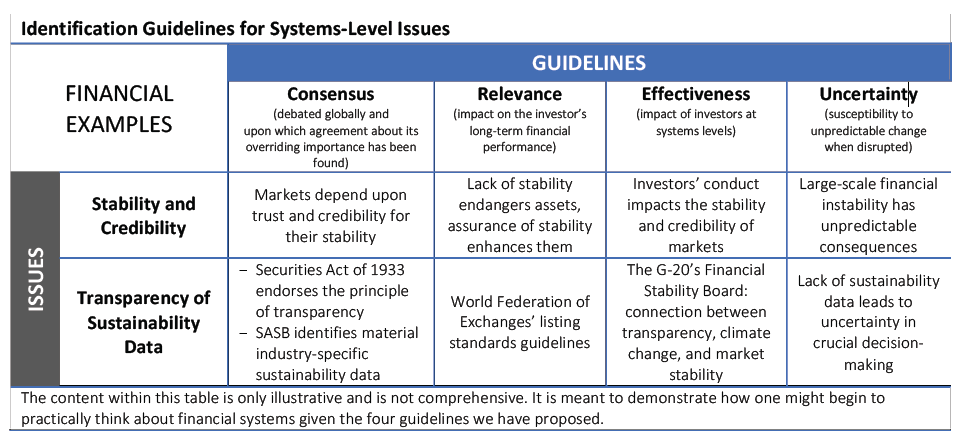

Stability and Credibility

Guideline 1: Consensus

It is a fundamental tenet of finance that stability—and the credibility and trust that makes that stability possible—is essential for the functioning of modern-day markets. For markets to function, one must believe that money will hold a relatively stable value, that governments will continue to assure that value, that those who enter into contracts to purchase today will have the means to do so tomorrow, and that banks that accept deposits can pay them back upon demand, among other things.

Guideline 2: Relevance

Without credibility, the stability of the markets is endangered, placing at risk the assets of investors. In September 2008, the fate of the global financial system hung in the balance. Although total collapse was averted, estimates of investors’ losses in the fallout of that crisis range from $5 trillion to $15 trillion. This crisis came as a “wake-up call” to many long-term investors as to the importance of understanding and monitoring the risks of instability in the overall financial system as well as that of their portfolios. In the wake of that crisis, governments around the world have proposed a host of legislation and regulations to assure that credibility and stability, including the Dodd-Frank Wall Street Reform and Consumer Protection Act in the United States and the European Central Bank’s stress testing framework.

While they require stability, our financial systems also benefit from a certain degree of innovation, diversity of product, and adaptability that can provide the resilience needed in complex systems. This resilience allows finance to evolve in response to changes in technology, global economic conditions, and exogenous crises in ways that can preserve its stability while allowing for system-wide advances.

This combination of stability and resilience is essential for investors seeking reliable long-term returns.

Guideline 3: Effectiveness

That the practices of investors can undermine this stability was made clear in the 2008 crisis. The Financial Crisis Inquiry Report by the National Commission on the Causes of the Financial and Economic Crisis in the United States was explicit on the crucial causal role played by large financial institutions.

We conclude dramatic failures of corporate governance and risk management at many systematically important financial institutions were a key cause of this crisis…. We conclude a combination of excessive borrowing, risky investments, and lack of transparency put the financial system on a collision course with crisis…

That these same institutions, along with others, can play an effective role in assuring the stability and sustainability of these systems is the argument put forward by the UN Environmental Program’s Financial Initiative in its series of publications under the rubric of The Financial System We Need.

Guideline 4: Uncertainty

As with other complex systems, what happens when financial systems become unstable is highly unpredictable and uncertain. Even a potential breakdown as relatively simple as the prospect of default of Greece’s sovereign debt in 2010 provoked protracted speculation as to its implications for not only that country, but for the European Union as a whole. That uncertainty pales, however, in comparison to the uncertainty experienced during the near collapse of the global financial system in the dark days of September 2008.

Robert Skidelsky, the British economic historian and author of a three-volume biography of John Maynard Keynes, argues that economic collapses in current times are likely to be more frequent and more severe than in the past:

The increased importance of investment, the interconnectedness of today’s economies, the global reach of financial trading, technology-innovation, and the surfeit of distracting information produced by the media may well have rendered the scale and frequency of collapses generated by economic activities themselves, rather than by outside events, much greater than in the past.

Transparency of Sustainability Data

Guideline 1: Consensus

Transparency—in particular in the form of disclosure of security-specific data material to investors—is essential to the efficient functioning of financial markets.

Indeed, the primary objective of the Securities Act of 1933 was to ensure consistent public disclosure of financial data to enhance the trustworthiness of the public markets, a principle that has since found widespread acceptance. As the Securities and Exchange Commission describes this legislation, its twin objectives were to:

- require that investors receive financial and other significant information concerning securities being offered for public sale; and

- prohibit deceit, misrepresentations, and other fraud in the sale of securities.

The broadly accepted assumption today is that adequate disclosure is essential for trustworthy financial markets and that those lacking transparency will be less than efficient.

Guideline 2: Relevance

Transparency for transparency’s sake is not sufficient for financial markets—data disclosed must have material relevance to the functioning of these markets. The Sustainability Accounting Standards Board is engaged in research to document the most material, sustainability (i.e. related to environmental and social factors) data for the purposes of investment in various industries.

In October 2015 the World Federation of Exchanges (WFE) proposed guidance for stock exchanges around the world that would encourage voluntary adoption of a requirement that listed companies disclose key sustainability data. In order to assure consistency across exchanges, the WFE proposed standardized disclosure of 33 crucial environmental, social and governance indicators.

The assumption is that this data is relevant to today’s pricing of securities.

Guideline 3: Effectiveness

That the disclosure of data can help manage the impacts that investors have upon environmental systems is implicit in the work of the Task Force on Climate-Related Financial Disclosure created by the G-20’s Financial Stability Board. One of its fundamental assumptions is that climate-related disclosure by financial institution can positively impact management of the uncertainties of climate change at the systems level, and by implication can help assure the stability of financial markets.

Guideline 4: Uncertainty

Without disclosure of material environmental, social and governance data, not only are investors forced to make financial decisions in the relative dark on issues as crucial as climate change, but corporate managers, government officials and civil society organizations are at an equal disadvantage in assessing the impacts of corporations and finance in these arenas. Although unpredictability and uncertainty can never be entirely eliminated from investment, transparency helps reduce their scope and facilitates the management of investments with long-term timelines.

Note on the Specificity of Investment Choices

A disjunction can arise between a broad systems-level focus that an institutional investor has adopted and the specifics of the individual investments or related practices it undertakes. Inclusion of a broadly diversified range of investments and related activities can help manage this apparent discrepancy.

For example, healthy communities might be the systems-level issue on which an investor asserts it is focused. This investor points to its investment in a company manufacturing insulin used to control the diabetes that results from obesity. Taken by itself, this investment may appear to be a disproportionately narrow choice. Prevalence of obesity is simply a symptom of a dysfunction in a healthy community and insulin is no more than a treatment for that symptom. The investment addresses one symptom of poor health, but not its causes. This choice becomes problematic if obesity or insulin treatments are the sole focus of the investor’s program, but less so if it is part of a well-conceived diversified portfolio of health-related investments and practices.

In this case, the institution might also invest in companies producing healthy foods, promoting exercise, and helping with weight loss, as well as healthcare providers operating community-based clinics and health education programs. It might also engage their food producers and retailers to reduce sugar in products, increase organic food offerings, and address the overuse of antibiotics in animal feedstocks. In addition, it might collaborate with peers or enter into partnerships with non-governmental organizations to influence public policies that enhance community health at a broad level.

A second example involves an investor focusing on the systems-level issue of poverty alleviation. As part of that commitment, it makes investments in affordable housing. If these investments are narrowly focused in its headquarters city alone, it might appear to be using the issue simply as an excuse to make self-interested, suboptimal local investments. By contrast, if that local investment were part of a larger program of investments in affordable housing spread out over diverse geographic regions and accompanied by other broad poverty-alleviation investments in small business and community economic development, it would be less likely to appear inappropriate.

Constraints of Consistency and Imperfection

As Jon Elster points out in his essay Reason and Rationality, when it comes to the opportunities for conflict of interest,

[A]n agent would have to be either very inept or very unfortunate not to be able to find some combination of normative principles and causal chains that would allow him to present his passion or his particular interest in an impartial light.

Elster’s solution to this challenge relies on two concepts: what he terms the “constraint of consistency” and the “constraint of imperfection.”

To incorporate the concept of consistency, Elster proposes that “[O]nce the agent has adopted a certain normative principle or a certain causal theory, he cannot abandon it, even if it no longer allows him to satisfy his desires.” That is to say that once investors choose to focus on a particular systems-level consideration, they must incorporate it consistently. If investors focusing on climate change, for example, choose to divest from a coal company in a foreign country, they cannot then choose to invest in a local coal-mining firm.

To appear “perfect” in the execution of one’s duties as an investor, Elster also argues that “the coincidence between the professed motivation and the desire must not be too blatant.” In other words, one must avoid even the appearance of a conflict of interest. If the investor’s personal interest in a given decision appears “too blatant” it must be modified, qualified or avoided entirely. To continue the climate change example, investors would not adopt a policy of investing only in local renewable energy companies and no others elsewhere in the world because the appearance of favoritism to the local would be too great, irrespective of the merits of the specific investment decision.

The general principal of diversification, fundamental to finance today, is applicable to this challenge of managing risks and rewards for systems-level issues as well. The credibility of investment policies and practices made here should be assessed in the context of a fully diversified approach. Narrowly conceived approaches to systems-level impact will increase the chances of the perception of conflicts of interest. See the accompanying box for two general principles proposed by the philosopher Jon Elster. These principles rely on consistency in decision-making to assure that private interests do not overwhelm the larger public interest, or appear to do so.

Implications for Further Research

This post clarifies the types of definitions, principles, and specific tactics that institutional investors might find useful in managing systems-level risks and rewards as an intentional part of their investment practices.

A number of areas for further in-depth research would be useful to facilitate this undertaking. Three of the most pressing of these are the following.

Common-Pooled Resources and Collaborative Action

The tendency for the investment community to create unintended consequences through their collective but uncoordinated actions is poorly documented and understood. Although the investment community’s collective impact is often manifest, it is frequently assumed that individually investors could not, or even should not, influence the broader systems within which they operate.

Further research on the intentional collective-action potential of the investment community will help deepen investors’ understanding of how they might avoid “tragedy of the commons” situations and work toward the preservation and enhancement of systems. In particular, this research could draw on the work of Elinor Ostrom and others who explore the question of which systems could be considered common-pooled resources and how those attributes identified by Ostrom as encouraging trust and cooperation in the management of such public goods might be applied to investors contending with systems-level issues.

Risk and Reward Measurement

Increasingly effective tools have been developed to measure the environmental, social and governance (ESG) performance of corporations and the sustainability key performance indicators of industries. It is now possible to roll up indicators—for example, the carbon footprint of individual companies—from a security level to a portfolio-level score. In parallel, scientists and public policy institutions continue their refinement of indicators for measuring the value of ecosystems and the progress in human development and well-being.

Further research would be useful to survey these parallel systems of measurement and understand their differences and similarities. Building on those findings, work could be done to develop measurement tools to answer the question: to what degree have the policies and practices of specific investors impacted positively or negatively the health of the larger systems within which they operate? What are the metrics that would be most useful in assessing the individual or collective impacts of investors at these levels?

Systems-Level Reporting

An increasing number of asset owners and managers report on a variety of social and environmental initiatives including those that involve collective action (e.g., engagement with corporations, public policy advocacy) and systems-level thinking (e.g., development of investment belief statements, intentionality in the creation of long-term societal wealth). This reporting tends to be sporadic and anecdotal.

Further research would be useful in understanding what the key elements of reporting on these initiatives and their impacts at systems level would look like, how they could best be gathered into a coherent whole, and what range of options might be available to investors for such reporting. A crucial issue to be resolved is how would such systems-level reporting differ from today’s well-developed practices with regards to the portfolio-level reporting of investment returns and performance, particularly versus benchmarks, which is an essential part of investors’ communications and will continue to be so?

Research in these three areas could provide valuable tools for investors wishing to consider the legitimacy and practicalities of integrating systems-level considerations into their policies and practices.

Conclusion

With a 21st century population headed toward more than nine billion and the stresses that will be put on our environmental, societal and financial systems by that population’s growing wealth, technological capabilities and aspirations for higher standards of living, institutional investors with long-term time horizons will be well served to understand how they can intentionally manage the risks and rewards that their policies and practices create at the level of the systems in which they operate and upon which their decisions, individually and collectively, inevitably have impact. These decisions can stabilize or destabilize these systems, which in turn can have positive and negative impacts on investors’ portfolios, effects that cannot be prudently ignored.

One of the first steps for investors seeking to manage these impacts is to decide on which systems-level issues to focus. Issues are many and varied and impact is difficult to achieve. Even for the largest of investors, focus is necessary as they deploy necessarily limited resources. In addition, only a limited number of issues have achieved widespread consensus as to their systemic importance, are broadly relevant to long-term investment returns, are susceptible to substantive influence from investors, and have a broad range of uncertain implications and outcomes.

When investors intentionally manage risks and rewards at these systems levels they contribute to long-term wealth creation along with the responsible management of their portfolios. The more comprehensive investors’ understanding of systems-level preservation and enhancement, the greater their comprehension of how “doing the right thing” can encompass both prudent management of assets and the creation of rising tides of potential wealth creation that benefit investors as a whole.

The complete publication, including footnotes, is available here.