Print

PrintJohn Roe is Head of ISS Analytics and Managing Director at Institutional Shareholder Services, Inc. This post is based on an ISS publication by Mr. Roe.

One criticism frequently leveled against boards of directors is that, when it comes to filling vacant board seats, they don’t cast the net widely enough. The numbers clearly show that boards often fill seats with candidates that have previous board experience—it’s even written right into the job description given to search firms in some cases. And, for many boards, that’s an understandable request—bringing on a “proven” director can side-step some of the concerns that shareholders and other board members may have.

But the flip side of the coin is that the seeming preference for directors with previous board experience may hamper efforts to bring new and diverse views into the boardroom. Some cynics wonder, if companies are simply cycling through the same individuals again and again to fill vacant seats, how many new views are companies actually bringing into the boardroom?

To add some substance to the conversation, we thought it appropriate to see exactly how experienced directors are, starting with S&P 500 companies. Our Director Data database contains information on directors and the public company boards where they currently sit, as well as all directorships the director has held in the past, going back more than thirty years.

For this analysis, when we’re talking about experience, we’re not talking about how old they are, or how many years they’ve been working—but rather, how many board seats those directors have held. We count both present directorships held, as well as those held in the past, across all companies that ISS covers. Note, this analysis does not include directorships held at private companies or non-profit organizations.

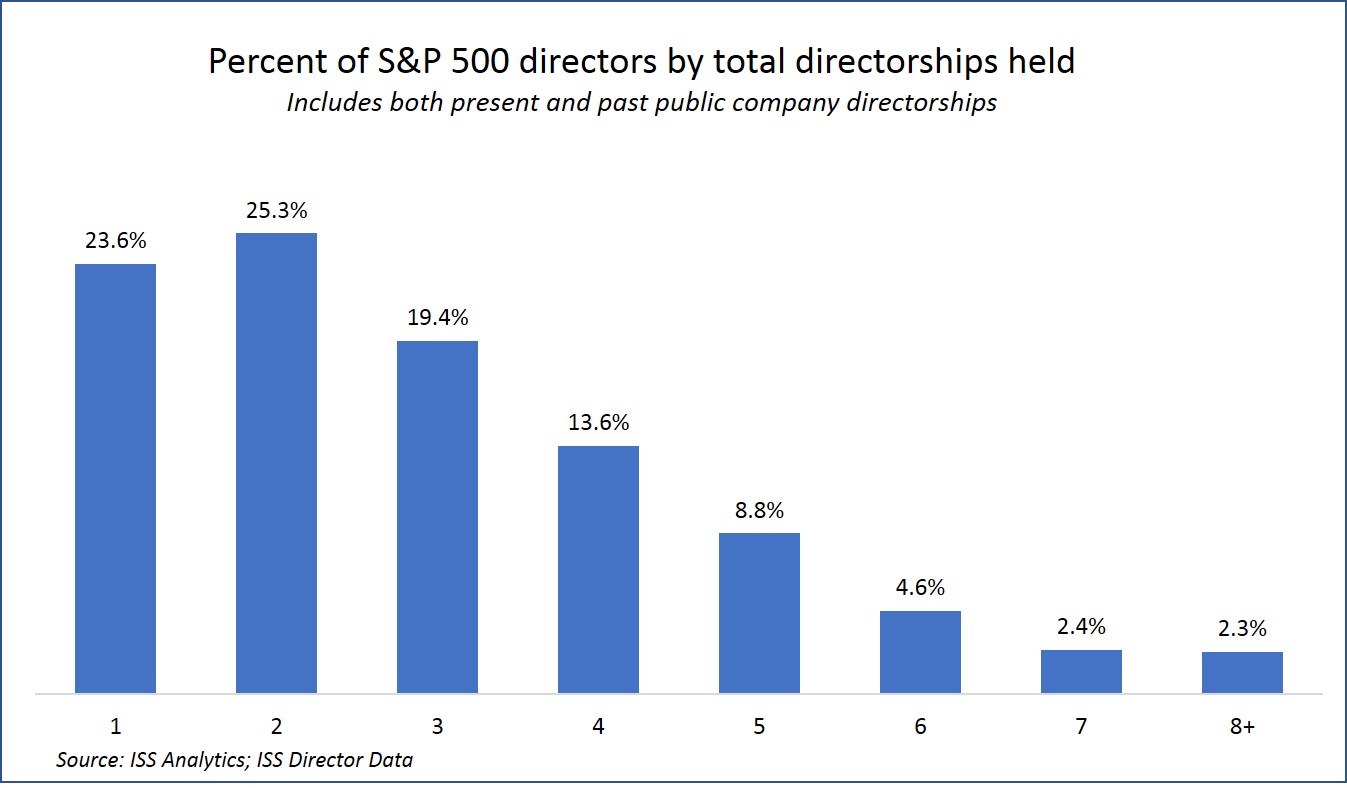

Fewer than one quarter of S&P 500 directors have held only one directorship

In the U.S., fewer than one in four directors in the S&P 500 has held only one directorship—more than three-quarters have held, or still currently hold, at least one additional board seat. And there are examples of directors that have had more than a dozen board seats over their career. Several of those are directors affiliated with active investors—although there are examples of those who are not, as well.

One significant source for these one-directorship directors are sitting CEOs of S&P 500 companies. More than one hundred and fifty CEOs of S&P 500 companies sit only on their own public company board (again, not including private and non-profit organizations). Others are “specialty” role players, such as emerging cyber risk experts—although the numbers suggest that, once identified, these specialists are often asked to join other boards, as well.

S&P 500 companies seem increasingly willing to take on “new” directors

Overall, out of that 23.6 percent of directors with only one directorship, S&P 500 companies have added nearly 200 new individuals to the boardroom in that timespan—and even more, counting those directors who are new to the boardroom since 2015 and have already been seated on multiple boards. Putting that into more tangible terms, about one in three S&P 500 companies has seated new first-time directors since the beginning of 2015. That number is trending up, perhaps in part reflecting the drive to increase diversity and fill critical skill gaps in the boardroom.

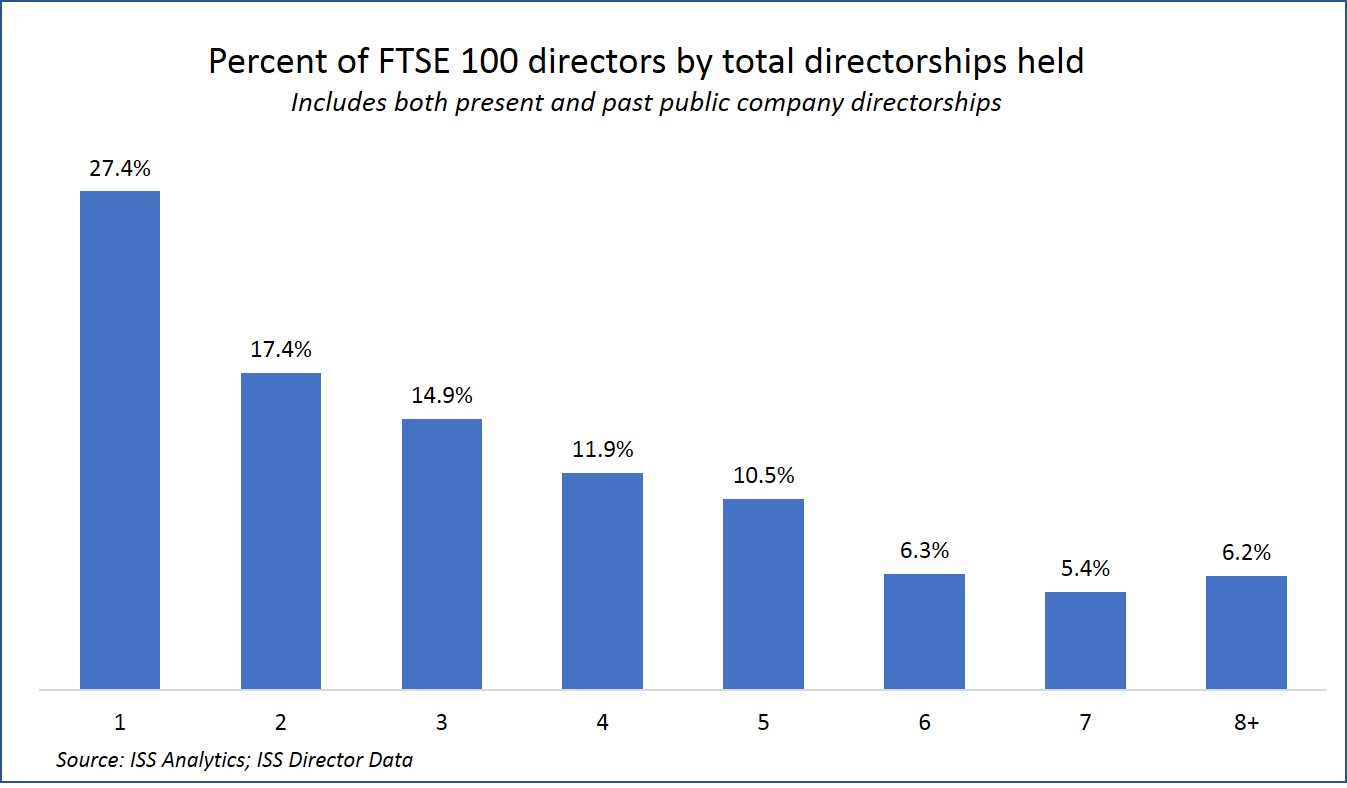

Not just an American phenomenon: FTSE 100 directors roughly the same

Among large-cap UK companies, we see a similar phenomenon, with the difference being that both ends of the distribution are elevated slightly. In other words, there are a slightly higher proportion of single-directorship directors at FTSE 100 companies, as well as a slightly higher proportion of directors that have held at least 8 directorships.

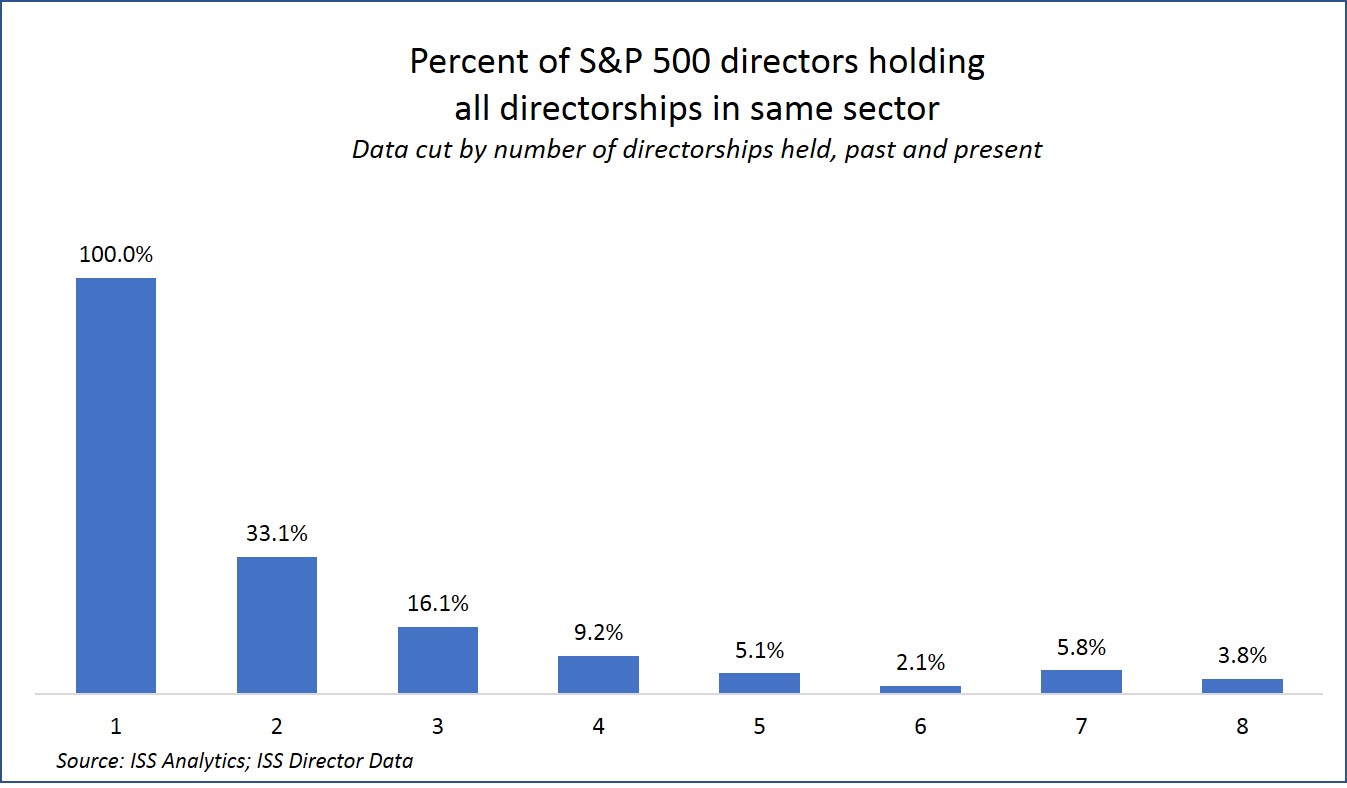

Directors seldom industry-exclusive

A second interesting dimension to the question is around industry concentration for directors that hold multiple directorships. We looked at this through the angle of the two-digit S&P GICS sector, looking to see what percentage of directors with multiple directorships held all of their directorships in a single sector. We cut the analysis by the number of directorships held—clearly, the more directorships held, the likelier a director is to diversify the sectors that they serve.

The results show that industry concentration (both past and present) isn’t nearly as important for directors as it might be for executives. Of course, some of this may be due to competitiveness issues, particularly for active directorships—companies will often not want their directors to sit on boards of potentially competitive companies.

The focus on skill & expertise breadth, rather than industry depth, is frequently reinforced when boards lay out their director qualification matrices, where they often focus on executive experience, complex and global management responsibilities, and financial acumen over industry-focused knowledge.

On the other hand, most S&P 500 boards do include a number of industry experts, along with a diverse representation of expertise and viewpoints from other industries. This is often seen as healthy and beneficial by most investors.

Some industries show a higher need for “specialty” directors

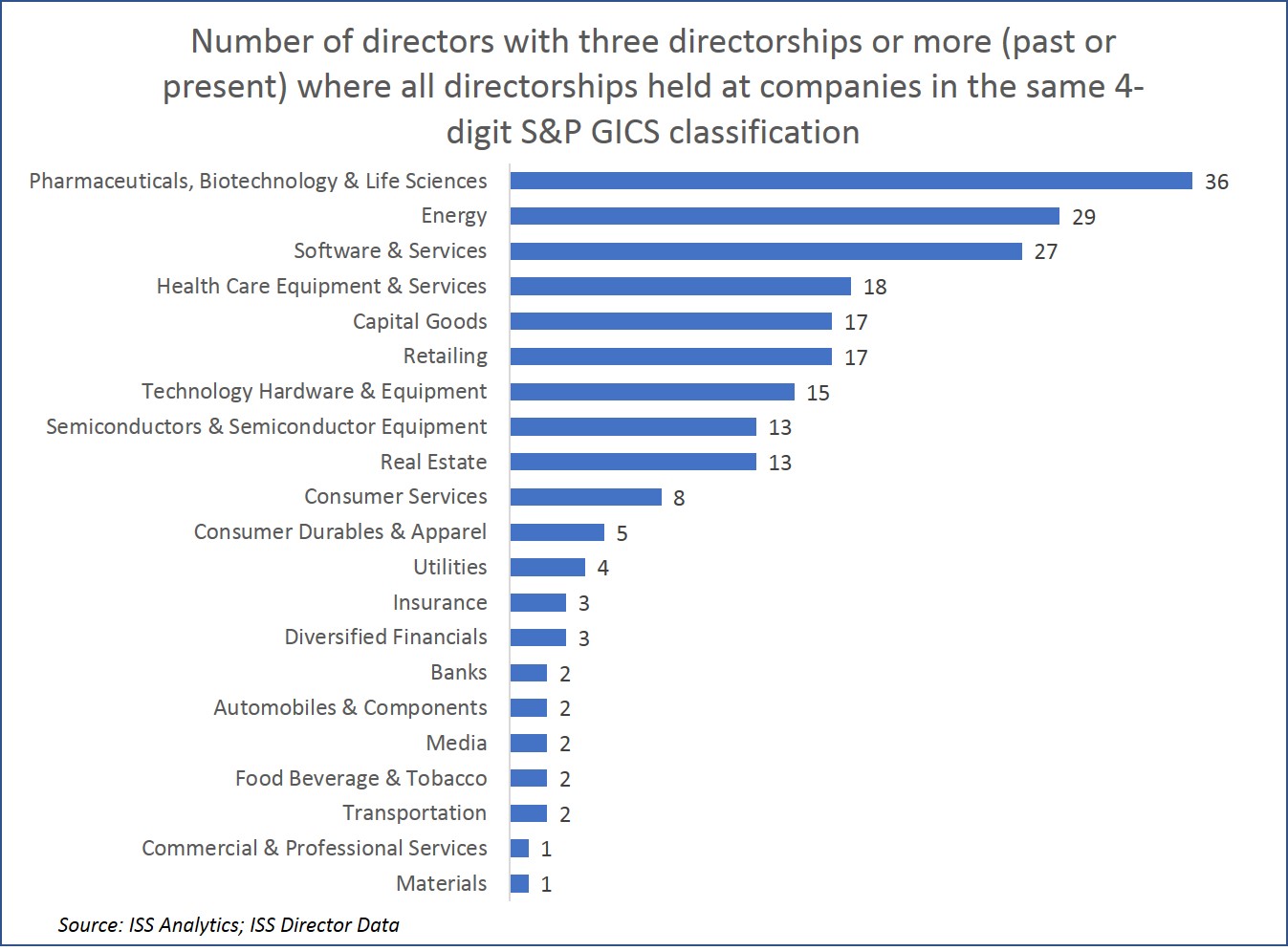

Among S&P 500 directors, there are approximately 2,200 directors who hold or have held at least three directorships. Among this group, almost exactly ten percent are “specialist” directors—meaning they have held all directorships in one industry (as defined by the four-digit S&P GICS classification). And there is some significant industry concentration among this group.

Pharma, energy, and software & services lead the way for industries where it appears S&P 500 companies are going after experienced industry experts to fill roles on the board—whereas other industries, such as materials and commercial & professional services, seem less inclined to seek out this expertise.

Finding the right balance

The right combination of directors is different for every company—new versus experienced directors, industry expertise versus broad knowledge, the right level of refreshment, and much more. The only sure thing in all of this analysis is that the level of scrutiny over the selection of directors will only increase.