Print

PrintSubodh Mishra is Executive Director at Institutional Shareholder Services, Inc. This post is based on an ISS publication.

In early September, ISS published its annual post-season report on compensation vote results and practices, which revealed a continuation of many trends identified last year. Shareholder support for management say-on-pay remains stronger than ever, while failures are exceedingly rare; average support for equity plan proposals was consistent with prior years. While CEO pay at larger companies has increased, the composition of CEO pay packages has trended towards more strongly performance based incentives. Interestingly, median golden parachute payments rose considerably, while golden parachute vote rates dropped and failure rates more than doubled. Shareholder proposals on compensation topics remained on the decline, and for the second consecutive proxy season no proposals received majority support.

Say-on-Pay Votes

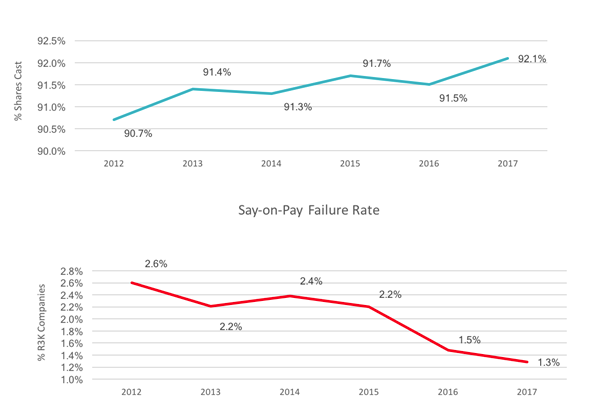

Say-on-pay support reached its highest levels. Since the introduction of say-on-pay, average support levels have remained consistently high. The 2017 proxy season was no exception, with average vote support of 92.1 percent, the highest to date. Failed votes remained a rare occurrence and the failure rate of 1.3 percent for 2017 was the lowest yet.

Votes Cast For / Votes Cast For + Against. Unless otherwise indicated, charts represent companies in the Russell 3000 Index (R3K), inclusive of the S&P 500 Index (S&P 500), with annual meetings held between January 1 and June 30.

ISS Recommendation Trends

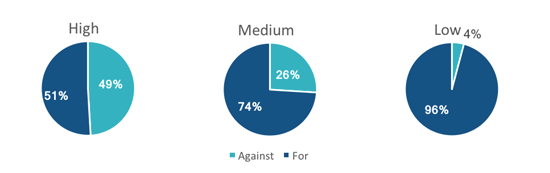

The severity of pay-for-performance misalignment correlates with ISS vote recommendations. During the first half of 2017, ISS recommended “against” votes for nearly half of the companies where there was a “High” quantitative concern, which indicates a severe misalignment between pay and performance. ISS recommended against slightly more than one-quarter of companies with a “Medium” concern level. Only 4 percent of companies that yielded a “Low” quantitative concern level (indicating quantitative alignment) received “Against” recommendations, usually as a result of problematic contractual provisions or poor board responsiveness. The initial screens identify quantitative outliers, while the ultimate say-on-pay vote recommendation is based on an in-depth qualitative assessment of pay programs and practices.

ISS’ Say-on-Pay Recommendations by Quantitative Concern Level 2017

CEO Pay Trends

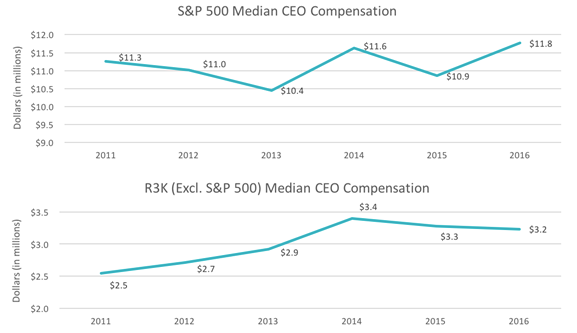

Median S&P 500 CEO pay reached its highest point since the say-on-pay rule took effect in 2011, pay at smaller companies was flat. Median CEO compensation in the S&P 500 grew nearly 8 percent over 2015 (including the impact of cash, stock awards, pensions, and other compensation), driven primarily by increases in stock compensation. Median CEO pay in the Russell 3000 (exclusive of the S&P 500) declined slightly from $3.28 million to $3.24 million. For these smaller companies, CEO total pay has remained relatively steady over the past three years.

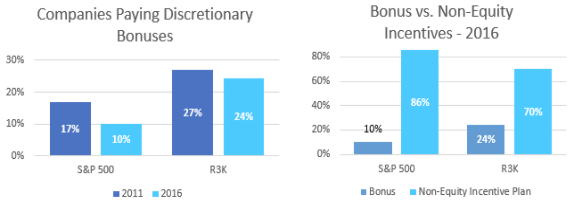

Discretionary bonuses continued to decline. Companies paying discretionary cash bonuses to the CEO (as disclosed in the “Bonus” column of the Summary Compensation Table) made up an even smaller minority in both the S&P 500 and the Russell 3000. In 2016, just 10 percent of the S&P 500 and less than a quarter of R3K companies paid discretionary cash bonuses. Concurrently, more companies are moving to formulaic non-equity incentive programs. In 2016, 86 percent of the S&P 500 and 70 percent of the R3K reported payments to the CEO through non-equity incentive plans.

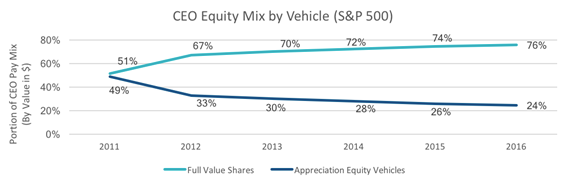

Appreciation awards continue to decline in popularity. The use of appreciation awards (options and SARs) for CEOs in the S&P 500 continued to decline in 2016, and these were increasingly replaced with full value share awards (restricted stock and RSUs, both time- and performance-vested).

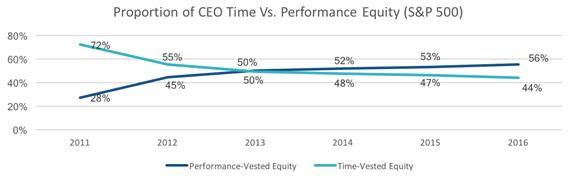

Performance-conditioned equity is the prevailing practice. Among the S&P 500, most companies deliver the majority of CEO equity awards in performance-conditioned vehicles. The percentage of CEO performance equity increased further in 2016 to an all-time high of 56 percent.

Say-on-Frequency Votes

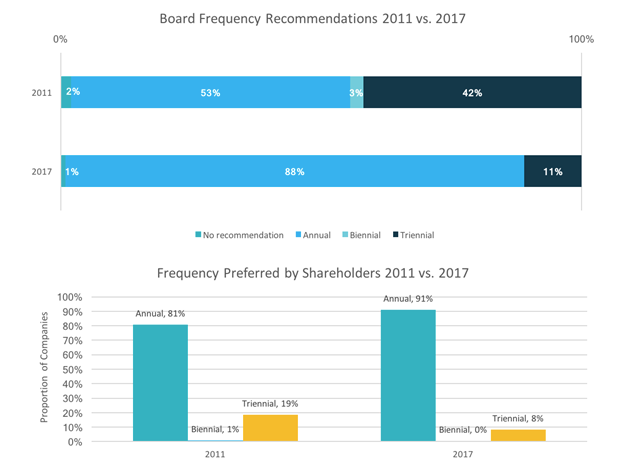

Say-on-pay frequency votes returned; annual frequency favored by boards and investors. Say-on-pay frequency votes are required at least once every six years, and most companies held their second say-on-pay frequency vote during the 2017 proxy season. In this second wave of frequency votes, significantly more boards supported an annual frequency. During the 2017 proxy season, 88 percent of boards recommended annual votes, compared to 53 percent in 2011. Shareholders’ strong preference for an annual frequency was even more pronounced in 2017, as they endorsed an annual frequency at 91 percent of companies in 2017, compared to 81 percent in 2011.

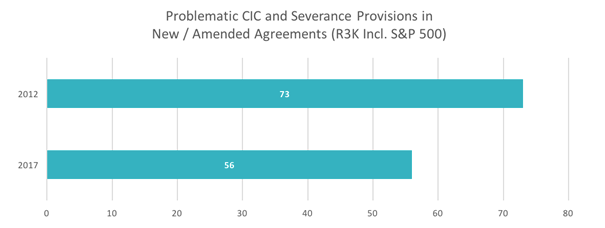

Problematic Pay Practices

Problematic pay practices are generally declining. The number of problematic severance and change-in-control provisions (per ISS policy) that were included in new or materially amended executive agreements has declined each year, as illustrated below. However, the decline has recently slowed: this year 56 companies included such provisions in new or amended agreements, compared to 58 in 2016. Excise tax gross ups were the exception to this trend, and actually grew more prevalent in 2017.

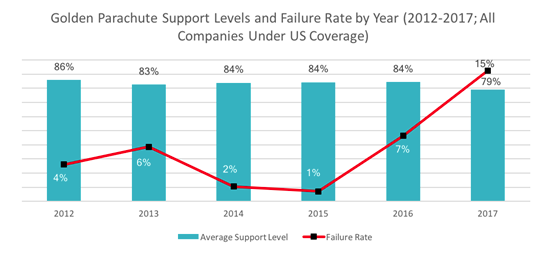

Say-on-Golden Parachute Votes

Golden parachute failure rate doubled as average shareholder support fell. Shareholder support for golden parachute proposals has typically trended lower than say-on-pay support. Average support for golden parachute proposals fell to an all-time low of 79 percent in 2017. The number of failed proposals doubled from six proposals in the first half of 2016 (7 percent of all proposals) to 12 proposals (15 percent) in 2017. As companies continue to incorporate performance equity awards, ISS and shareholders are more closely scrutinizing vesting treatment upon a change in control, particularly for recent grants. Moreover, the median CEO golden parachute payment rose by close to 75 percent, from $5.2 million in 2016 to $9 million in 2017.

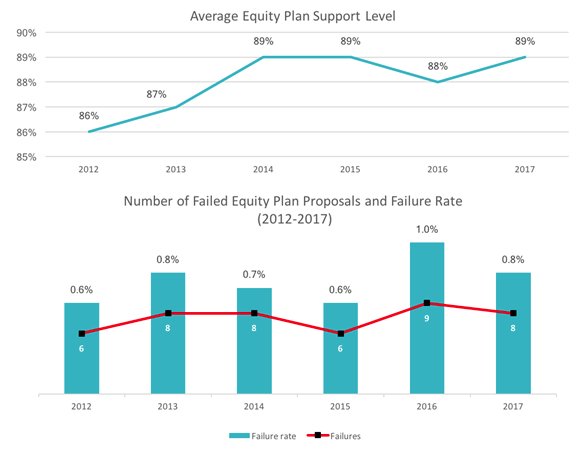

Equity Plan Proposals

Equity plan support levels were essentially flat. For the 2017 proxy season, average equity plan support was 89 percent, consistent with recent years. ISS supported 70 percent of the equity plan proposals analyzed under U.S. policy in 2017, a slight increase from 68 percent in 2016. Eight equity plan proposals failed, just below the five-year high of nine failures seen in the 2016 season. While there was no single common factor resulting in the failed proposals, many of the evaluated plans showed a relatively high shareholder value transfer (plan cost).

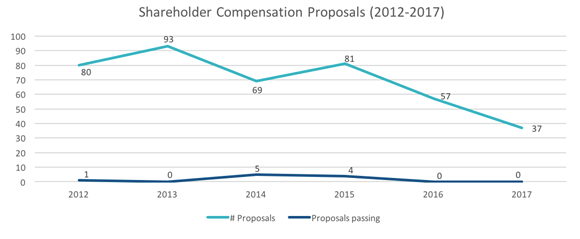

Shareholder Proposals on Compensation

The number of shareholder proposals on compensation plummeted. Shareholders voted on 37 compensation-related proposals during the 2017 proxy season, the lowest number since the first full year of say-on-pay. Compensation shareholder proposals rarely receive majority support and, similar to last year, none did during the 2017 proxy season. The steadily declining number of compensation-related shareholder proposals is likely impacted by the introduction of say-on-pay, which provides shareholders an alternative channel to voice their concerns.