Print

PrintJongha Lim is Assistant Professor of Finance at California State University Fullerton Mihaylo College of Business and Economics; Michael Schwert is Assistant Professor of Finance at The Ohio State University Fisher College of Business; and Michael S. Weisbach is Ralph W. Kurtz Chair in Finance at The Ohio State University Fisher College of Business, and Research Associate at the National Bureau of Economic Research. This post is based on their recent paper.

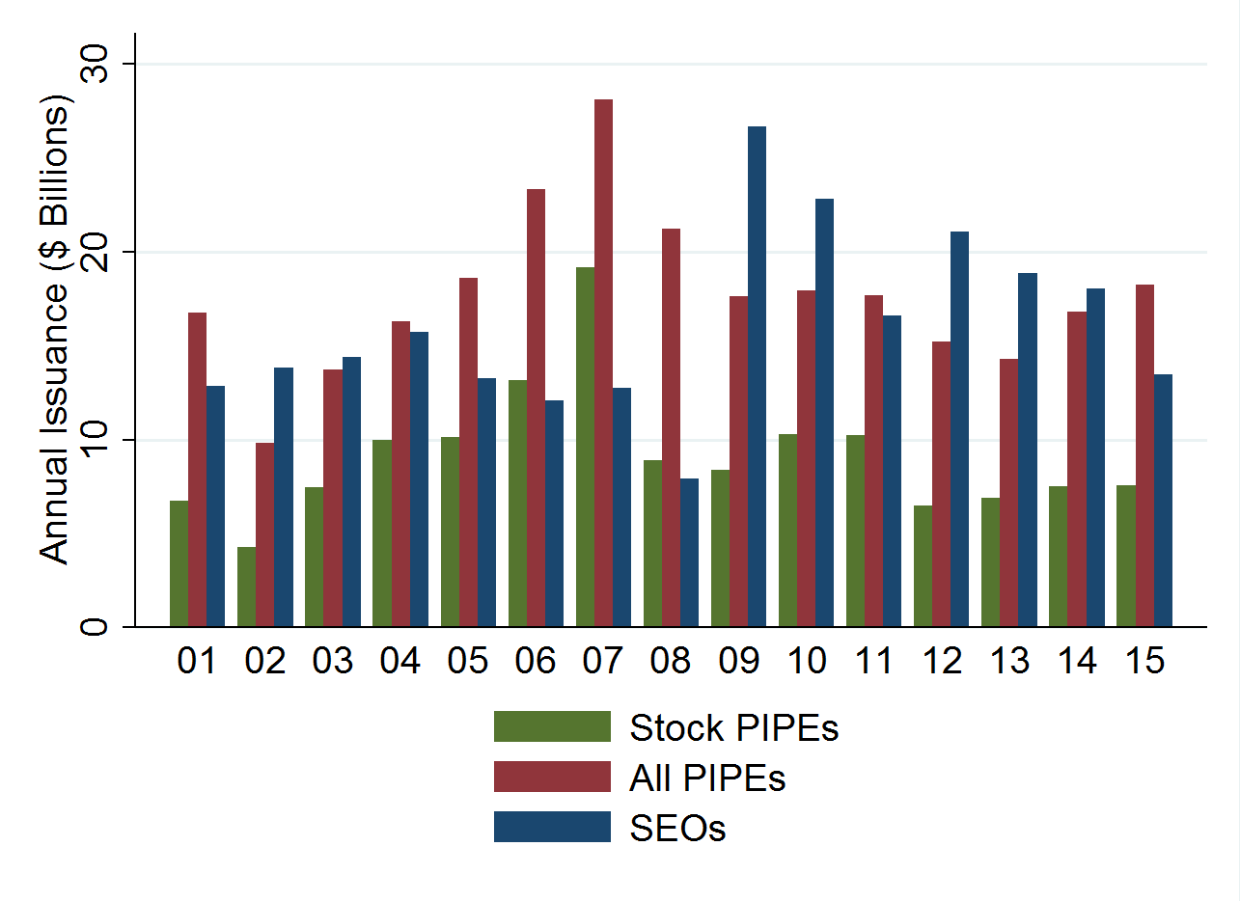

Private placements of equity, commonly referred to as “PIPEs,” are an important source of financing for many public corporations. According to PrivateRaise, a leading database on PIPE transactions, between 2001 and 2015, there were 11,296 private placements of common stock by U.S. listed firms that raised $243.9 billion. Firms raising funds through PIPEs tend to be small, with 93% of common stock PIPE issuers having market capitalization below $1 billion. As a point of comparison, U.S. firms with market capitalization below $1 billion raised $240.3 billion in SEOs over the same period.

Why do so many firms turn to PIPEs for financing? Conventional wisdom is that it is relatively expensive source, or as Brophy, Ouimet, and Sialm (2009) put it, a “last resort” form of financing. But how expensive is it? To calculate the cost to issuers, it is important to consider a number of attributes of the package purchased by PIPE investors. In addition to common stock, issuers often offer investors warrants and other securities. In most transactions, the common stock is unregistered and cannot be immediately sold by investors. The cost of capital for the issuing firms is a function of the expected return and risk of these securities. Since the equity in PIPEs tends to be discounted, the expected return to holding them varies inversely with the expected holding period, which depends on the time it takes to register the securities as well as the thinness of the secondary market for trading these securities after they are registered. Therefore, to calculate the cost of financing through PIPEs, one must control for the time it takes to register the securities and to sell them.

Our paper evaluates the cost to issuers and the benefits to investors in PIPE transactions. We rely on a comprehensive sample of 3,001 common stock PIPE transactions by U.S. firms listed on NYSE or NASDAQ between 2001 and 2015. In this sample, the median investment is $10 million, which equals 9.1% of the market value of the median issuing firm’s equity. In 80.9% of the transactions, the firm issues unregistered equity, meaning that investors cannot sell their positions until the issuing firm registers the equity, on average 100 days following the closing date of the offering. PIPE investors purchase shares at an average discount of 6.3% to the market price. In addition, investors receive warrants in 39% of the transactions in our sample. If one values the warrants using standard techniques, these warrants are worth an average of 17.5% of the value of the equity purchased. Including the value of the warrants, PIPE investors receive an effective average discount of 11.2% relative to the value of the package of securities they acquire.

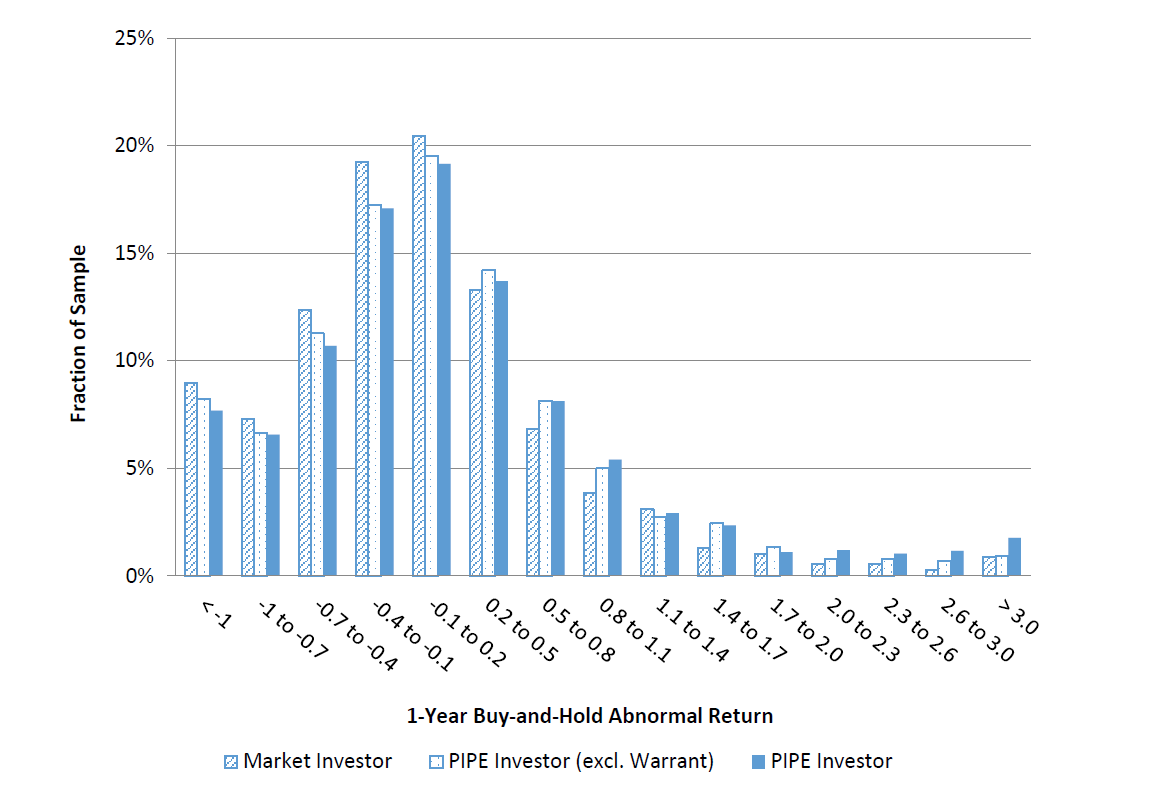

Because of these discounts and warrants, PIPE investors earn substantially higher returns than investors who buy and sell stocks of issuing firms’ or comparable firms at market prices. Over the year following the issuance, PIPE investors average a 12.1% abnormal return relative to firms with similar characteristics. These returns are highly skewed, with the median PIPE investor earning an abnormal return of only 1.7% over the year after issuance. The large difference between mean and median returns occurs because the returns of the issuing firms’ stocks are skewed and in addition the warrants amplify the right tail of the return distribution while having no effect on the losing deals. This highly skewed return distribution suggests that PIPE investing is like venture capital investing in that the key drivers of returns are the “home run” investments.

It is, however, not clear if PIPE investors in practice could achieve the above mentioned buy-and-hold returns. An important factor affecting investors’ returns is the time they hold the investments. The returns PIPE investors receive decline with the time they hold the investment. This pattern occurs because the offering discount accrues to investors immediately when the transaction closes. After that point, the long-run performance of issuing firms tends to be poor. Therefore, PIPE investors have an incentive to exit their stock positions as quickly as possible to capture the discount and mitigate exposure to the issuer’s downside risk.

There are two factors that limit the ability of PIPE investors to exit their positions quickly. First, most PIPE shares are unregistered at issuance and cannot be sold to the public until they are registered with the SEC. Second, the shares of PIPE issuers tend to be illiquid, so they cannot be sold immediately after registration without putting substantial downward pressure on the stock price. At the time of registration, the typical deal exhibits an increase in trading volume and a decrease in the stock price, suggesting that PIPE investors begin to exit their positions as soon as the securities can be sold. However, considering both the size of the investments (18% of the pre-offering shares outstanding, on average) and the limited trading volume in the issuers’ shares, we estimate that investors in unregistered PIPEs retain stock exposure for at least one year after registration. In contrast, investors in registered PIPEs are exposed to the issuer’s stock for at least six months.

We estimate the returns to PIPE investors controlling both for registration status and the limited ability of investors to exit their positions given the thinness of trading in the underlying stocks. To calculate these “holding period adjusted” returns, we assume that investors sell a constant fraction of the daily volume each trading day from the day the stock is registered until they liquidate their portfolio. The returns from this strategy, which presumably could be executed with a minimal effect of the PIPE investors’ trading on price pressure, leads to returns that are nonetheless still noticeably higher than investments in comparable firms at market prices. Assuming that investors sell 10% of the daily trading volume after registration, PIPE investors average a 21.2% return, compared to 4.9% for market investors, over an average holding period of 384 days.

Why do public firms raise capital under such costly terms? Examining the characteristics of PIPE issuers, it appears that their options are limited. Even though these firms are publicly traded, they are relatively small, with median book assets of $51 million. Their operating performance in the year prior to the PIPE issuance tends to be very poor, with a median EBITDA-to-Assets ratio of -22%. They likely do not have access to public debt markets and appear to have limited access to bank loans, as the median firm has a leverage ratio of only 7.2%. Finally, these are firms for which information asymmetry is likely severe, suggesting that the issuance cost of an SEO would be substantial.

We examine the hypothesis that the abnormal returns earned by PIPE investors represents compensation for the risk associated with providing capital to such poorly performing firms. Consistent with this view, when issuing firms appear to be more risky, the capital in the PIPE is more likely to be provided by relatively risk tolerant investors such as hedge funds and private equity funds, as opposed to the insiders and strategic partners who tend to supply capital to the other PIPEs in our sample. In addition, the returns from the PIPEs issued by riskier firms are higher and more volatile. The PIPE market appears to be one in which PIPE investors provide financing to companies that cannot obtain financing from alternative sources.

The complete paper is available for download here.