Print

PrintSubodh Mishra is Executive Director at Institutional Shareholder Services, Inc. This post is based on an ISS Analytics publication by Kosmas Papadopoulos, Managing Editor at ISS Analytics.

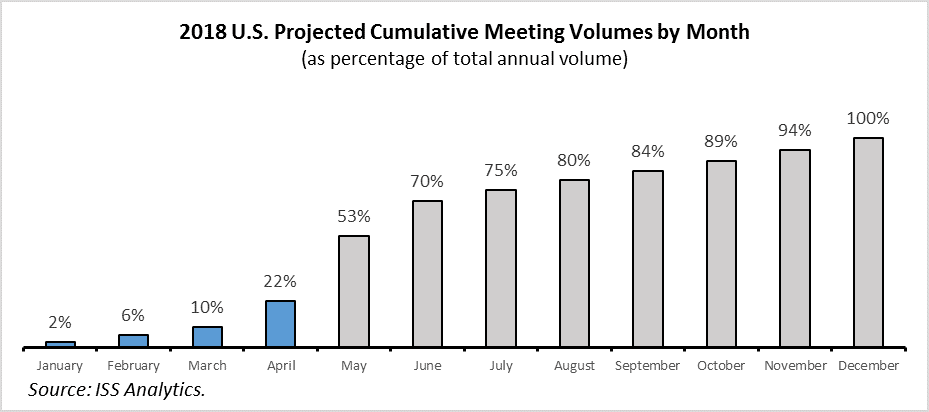

The U.S. proxy season is in full swing, with about 4,000 general meetings (or approximately 60% of annual meeting volume covered by ISS research) taking place in the months of April, May, and June. As we reach the end of April, investors are making voting decisions about the highest volume of meetings, which take place in May (not to mention all other markets in the Americas, Europe, and Asia that are also in peak season). As a meaningful number of meetings have already taken place, we take a look at some emerging trends forming in the beginning of proxy season 2018. While we have a long way to go for a complete picture to develop, the trends we observe now can serve as indicators of potential changes in the governance landscape.

Virtual-only meetings are on the rise

In the first five months of the year, we observe a growing number of companies favoring virtual shareholder meetings, continuing a trend from the past three years. A review of ISS Analytics data identified 127 virtual-only U.S. meetings taking place from January to May of 2018, compared to 99 virtual-only meetings during the same period last year. Virtual meetings present a number of advantages to both shareholders and the company, such as wider participation, lower costs, and ease of submission of questions. However, companies and investors will have to also consider and manage potential risks, such as less direct communication and lack of transparency in filtering or pre-screening of questions.

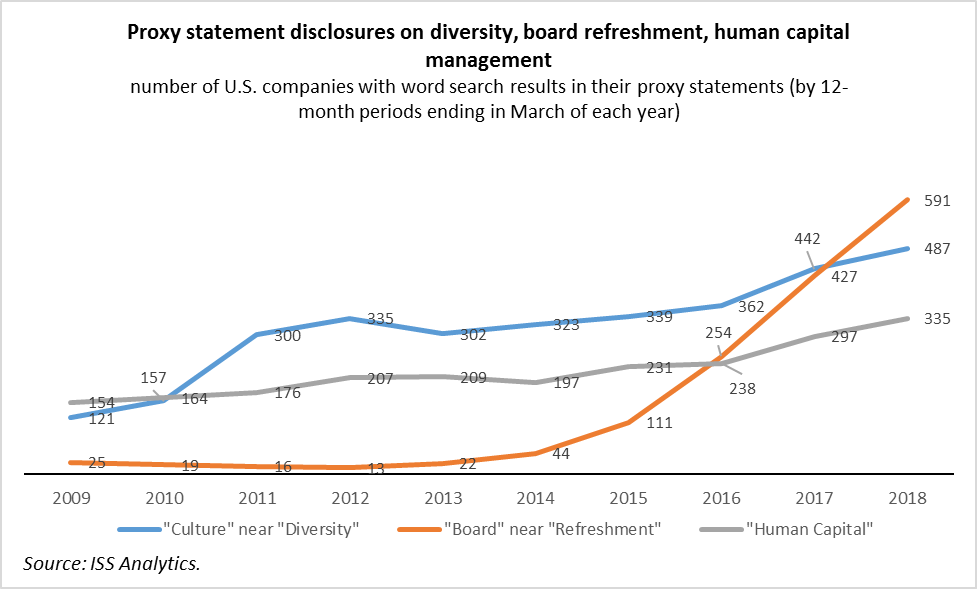

More proxy disclosures feature culture, refreshment, and diversity

An analysis of proxy filings from the past decade suggests that proxy disclosures continue to evolve, as discussions about culture, diversity, board refreshment, and human capital management reach record highs. This trend is not surprising, considering the increased focus on board diversity and renewal by many institutional investors. Moreover, companies appear to proactively address areas of potential concern, in light of several high-profile cases where questions of culture or problematic human capital management were identified as key points of failure at firms dealing with governance crises and reputational risks.

Director Elections and Board Practices

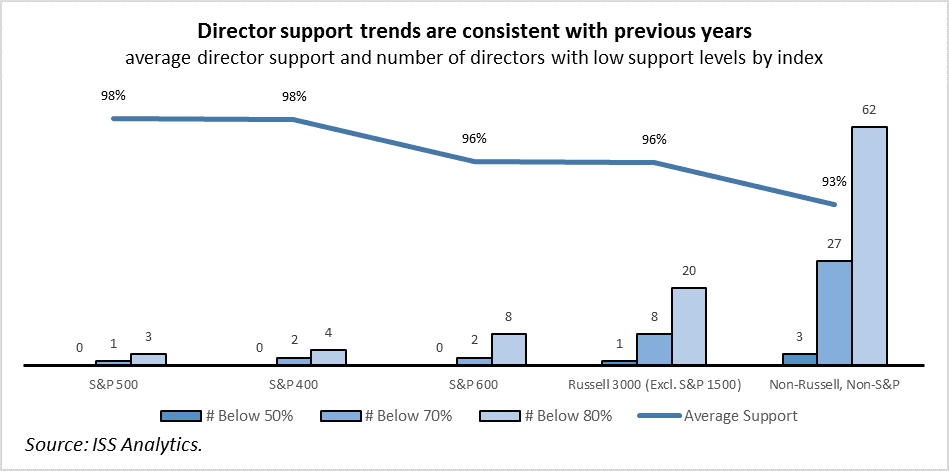

Director elections proposals have so far received similar levels of support as in previous years, with directors at small-cap firms generally seeing higher levels of opposition compared to directors at large-cap firms. In total, 40 directors at 19 companies received shareholder support below 70% of votes cast, and only four directors have failed to receive majority support. An analysis of potential reasons for concerns shows that about half of the boards that received low support rates (below 70% of votes cast) had structural issues, such as poor director attendance at board meetings and board and committee independence concerns, while the other half dealt with board accountability concerns, such as poison pill adoptions, unilateral bylaw amendments, and compensation concerns.

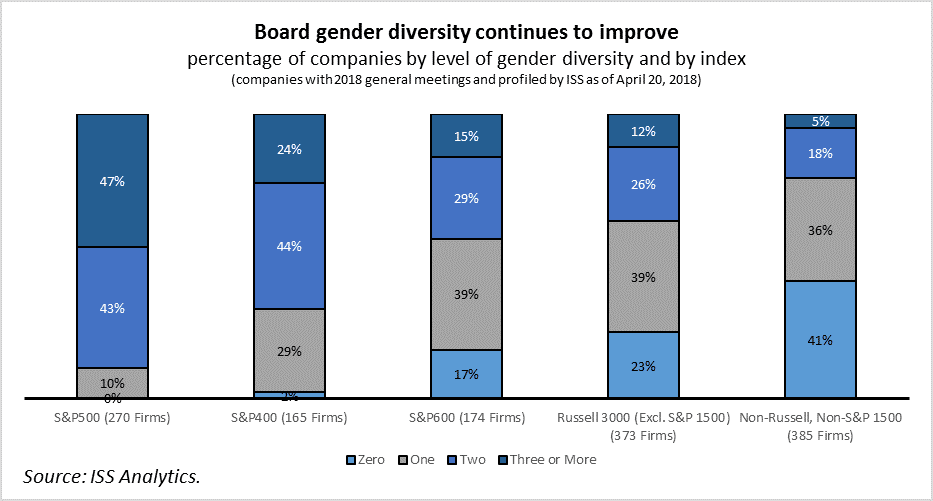

Companies continue to make strides in the area of board gender diversity, as the percentage of new directors who are female reaches a record high of 35% in the Russell 3000 and close to 39% in the S&P 500. By now, approximately 90% of S&P 500 and 58% of Russell 3000 companies have at least two female directors. As expected, board gender diversity practices differ significantly by company size, with smaller companies having fewer women on their boards despite recent improvements.

CEO pay increases, raising concerns about quantum and performance rigor

On the compensation front, support levels for say-on-pay proposals are at similar levels as in previous years. Unlike director election proposals, say-on-pay opposition is equally distributed between large and small firms, with the exception of micro-cap firms, which appear to gain higher support levels so far this year. Five proposals failed to receive majority support, among them one S&P 500 firm, the high-profile case of Walt Disney Company. The other four companies are Nuance Communications Inc., AECOM, Commercial Metals Company, and Sanmina Corporation. Among the S&P 500, four other companies received levels of support below 70% of votes cast: Schlumberger Limited, Transdigm Group Incorporated, Broadcom Limited, and Johnson Controls International plc. In most of the cases above, the key concerns constituted a combination of lack of rigor in performance criteria and high quantum of pay, as four of the five S&P 500 companies that received low support levels made payouts to individual executives exceeding $40 million, approximately four times the median CEO pay in the index.

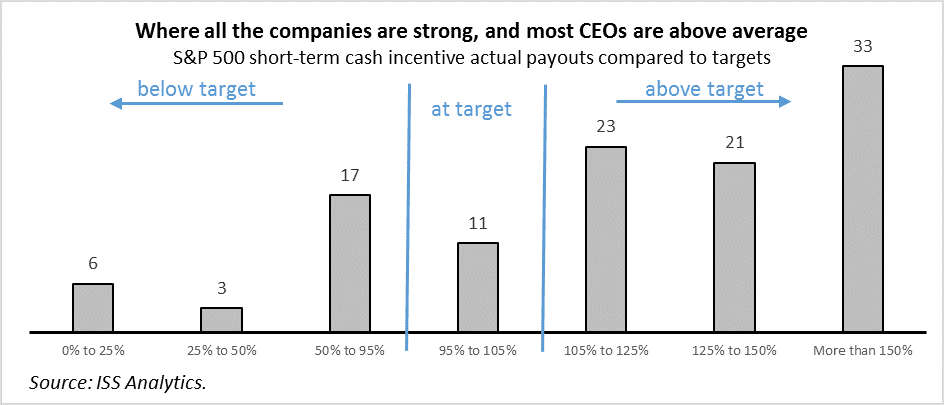

As discussed in our early look at the status of U.S. CEO pay, CEO compensation levels see some of the highest increases in the past decade, with an average increase of approximately 10% compared to the previous year. Stock awards and annual incentives make up 90% of these increases in pay, while base salaries and discretionary bonuses remain fairly stable, and option grants are in decline. Strong 2017 results have resulted in more than two-thirds of S&P 500 CEOs receiving annual incentive payouts above targets, raising concerns about a potential Lake Wobegon effect in CEO pay (i.e. companies overestimating their achievements in relation to the rest of the market).

Farewell to most 162(m) proposals

The recent U.S. tax reform eliminated certain tax deductibility provisions for performance-based pay, including most stock-based awards granted under equity compensation plans. Among other criteria, section 162(m) of the code required companies to request shareholder approval to gain tax deductibility status for awards under equity compensation plans at least every five years. As companies are no longer required to request this approval, we already see fewer firms submitting equity compensation plan requests on ballot. While many investors did not consider 162(m)-related requests material, the rule forced a regular check on the state of the plan and its provisions. The loss of 162(m) proposals raises the question of whether companies will opt for requesting higher volumes of shares, while returning to shareholder for approval once every ten years per the minimum regulatory requirement.

Shareholder Proposals

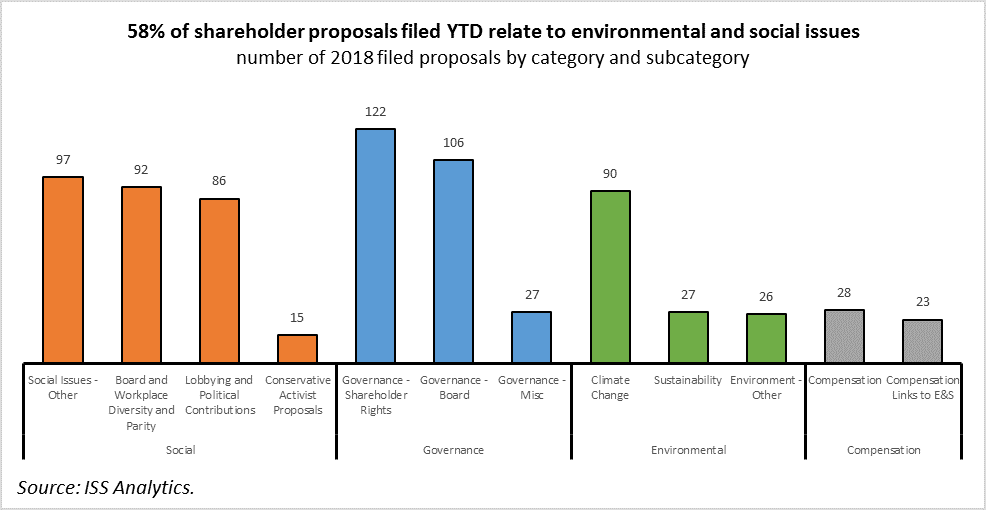

To date, ISS has identified 739 shareholder proposal filings at U.S. companies, with 123 proposals omitted and 114 proposals withdrawn from ballots, while 55 have been voted. This leaves 447 pending proposals. Social issues take the lead in terms of the number of filed proposals, as several campaigns have increased their efforts in 2018: lobbying and political contribution disclosures (86 proposals), board diversity (29 proposals), and disclosures on the gender pay gap (22 proposals). New types of requests include three pending proposals on gun safety and gun violence at American Outdoor Brands Corporation, Dick’s Sporting Goods Inc., and Sturm, Ruger & Company Inc., as well as three pending proposals on content management and “fake news” at social media giants Alphabet Inc., Facebook Inc., and Twitter Inc.

However, the majority of voted proposals dealt with governance issues, with resolutions seeking to reduce the ownership threshold for the right to call a special meeting and requests to establish an independent chair on the board featuring as the most common shareholder requests. In fact, requests regarding the right to call a special meeting are the most numerous filed so far this year, led by campaigns by John Chevedden and James McRitchie.

| Proposal Type | Proposals Filed |

|---|---|

| Right to Call Special Meeting | 68 |

| Lobbying Disclosure | 48 |

| Independent Chair | 41 |

| Carbon Emissions | 39 |

| Political Contributions Disclosure | 38 |

| Right to Act by Written Consent | 30 |

| Board Diversity | 29 |

| Sustainability | 27 |

| Pay Inequality | 24 |

| Amend Proxy Access | 23 |

Source: ISS Analytics.

Environmental proposals also have a very strong presence, with approximately 90 proposal filings related to climate change, including requests for carbon emissions targets and disclosures, 2-degree scenario reporting, and renewable energy reporting.

Support levels for shareholder proposals are relatively high, as approximately 54% of voted proposals received support above 30% of votes cast. This is true for environmental and social proposals also, with 11 of 23 voted E&S proposals receiving support levels above 30% of votes cast, and five proposals receiving support of more than 40% of votes cast. Four governance-related proposals have received a majority votes cast, as listed in the table below.

| Company Name | Proposal Type | Support (F/(F+A)) |

|---|---|---|

| Applied Energetics, Inc. | Amend Articles | 94% |

| Nuance Communications, Inc. | Amend Bylaws—Call Special Meetings | 94% |

| Costco Wholesale Corporation | Adopt Simple Majority Vote | 87% |

| Kaman Corporation | Eliminate Supermajority Vote Requirement | 59% |

Source: ISS Analytics.