Print

PrintAnthony Garcia is a Policy Advisor at ISS Custom Research, Kosmas Papadopoulos is Managing Editor and John Roe is Head of ISS Analytics. This post is based on their publication for ISS Analytics.

Peer groups form the bedrock of many company pay-setting exercises. Benchmarking CEO pay to a target value, typically the median pay of a group of “peer” companies, is a standard practice used by compensation committees; more than 97 percent of S&P 500 companies disclose benchmarking peer groups. And while there was once significant skepticism among the investor community due to perceived peer group manipulation (typically companies selecting many larger companies or “aspirational peers,” leading to escalating executive pay), most companies seem to have reformed their peer group selection practices.

In this post, we provide an alternative look at peer groups using the “wisdom of the crowd”—that is, the network of companies formed by examining the peer selections that other companies are making (and specifically ignoring the peer selections made by the target company itself). This is not meant to be a suggestion of peers for each company to use—but rather, a comparison to see how often the “wisdom of the crowd” arrives at decisions similar to the company’s own.

In our analysis, we find:

- Most companies—83 percent of the S&P 500—have a relatively high degree of overlap between their peer group and the “wisdom of the crowd” peer group;

- Sixty-three percent of the peers that companies didn’t select from the “wisdom of the crowd” peer group would have served to reduce the company’s peer group median pay; and

- Companies that deviate significantly from the “wisdom of the crowd” peer group are correlated with higher levels of pay and more significant say-on-pay opposition.

Using the “wisdom of the crowd” to build an alternative peer group

There is no magic formula for how to choose what constitutes an appropriate peer group. The most frequently cited characteristics for identifying a peer are: industry, financial size (revenue, market cap, or assets), and physical size (employee headcount/corporate footprint). Very few companies have a sufficient number of competitors that meet all the criteria to construct a complete peer group. In fact, forming a company’s peer group requires in-depth quantitative and qualitative familiarity with a company, its industry, competitive positioning, and strategic direction—knowledge that the company, its directors, and outside advisors may have better than anyone else.

We arrive at a “wisdom of the crowd” peer group for a target company by evaluating the network of companies formed by the peer group disclosures of all other companies. In their most recent disclosures, S&P 500 companies named 7,998 total peers, with 1,180 unique companies cited. Overall, 78 percent of the peer selections chosen by S&P 500 companies were fellow S&P 500 companies.

In our analysis, we attempt to define a reasonable group of peer companies with three key factors: the company’s peer network, company size, and the company’s industry. From a peer network standpoint, we identify companies that have selected the company as their peer, as well as second- and third-degree peers who chose peers of the company or were chosen by peers of the company. Firms with a closer network connection are deemed to have a greater connection strength. In this ranking methodology, the company’s own peer selections are ignored, so the network connection strength is primarily based on other firms’ peer selections. In terms of company size, companies with revenues, market cap, or assets closer to the company (the comparison metric depends on the company’s industry) rank higher in terms of connectedness. Finally, companies are ranked based on whether they operate in same or similar industries. A combination of these three factors offers a measure and ranking of “wisdom of the crowd” peers for each S&P 500 company.

To form this network-implied peer group, we select the 15 most highly ranked peers. We select 15 peers because that is approximately the median number of peers selected by S&P 500 companies themselves.

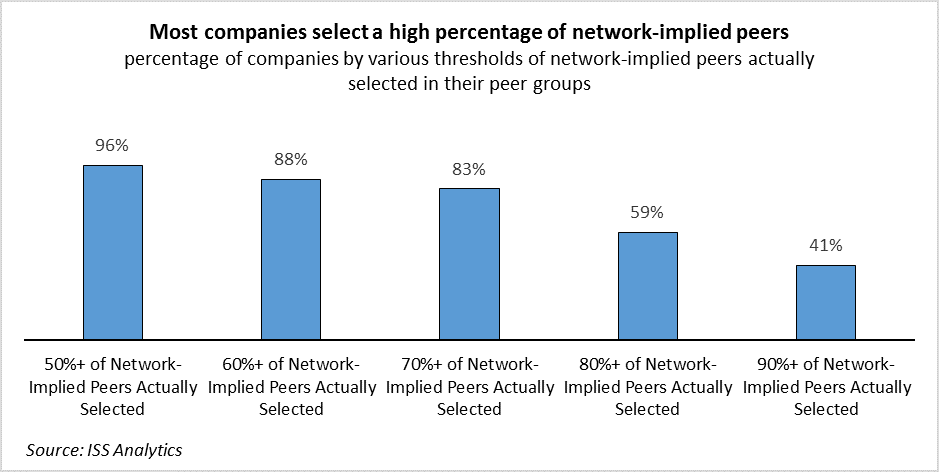

Most companies gravitate towards network-implied peers

The chart below looks at the frequency a company selects peers from its network-implied peers. The various groups are cumulative based on the percentage of the network-implied peers included in a company’s peer group. Since a company may have an actual peer group that includes more than 15 companies, companies are given full credit so long as all network-implied peers are included within their peer group. So, if a company selected 20 peers, and 15 of those peers were from the network-implied group, the company would be analyzed as having selected 100 percent of its network-implied peers. On the other hand, for companies who selected fewer than 15 peers, we measure the percentage of the company-selected peers who belong in the “wisdom of the crowd” peer group.

For the purposes of this analysis, we consider the selection of fewer than 70 percent of network-implied peers as significantly deviating from the wisdom-of-the-crowd peer selection model, and approximately 17 percent of companies under review (80) belong to this group.

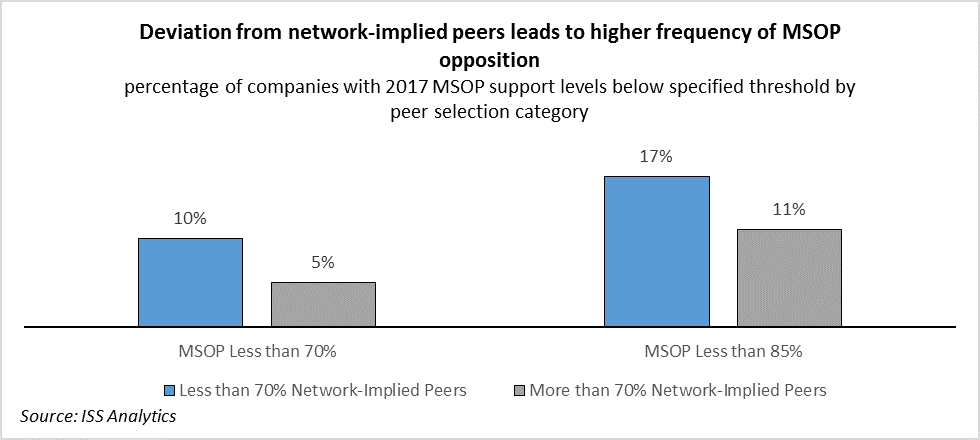

Deviation from the network-implied peer group correlates with lower MSOP support

The chart below examines the percentage of companies that received low levels of support on their say-on-pay votes. There were 27 companies that received less than 70 percent support out of 454 companies that had both a disclosed peer group and an MSOP proposal on ballot in 2017. Companies that deviated from the network-implied peer group were more likely to receive support rates below 70 percent of votes cast compared to companies with higher percentages of network-implied peers. We observe the same trend for support levels below 85 percent of votes cast.

These vote results trends raise interesting questions concerning peer selection and actual compensation practices. In the next section, we explore potential drivers for the higher frequency of say-on-pay vote opposition.

Network-implied peer selection and CEO pay

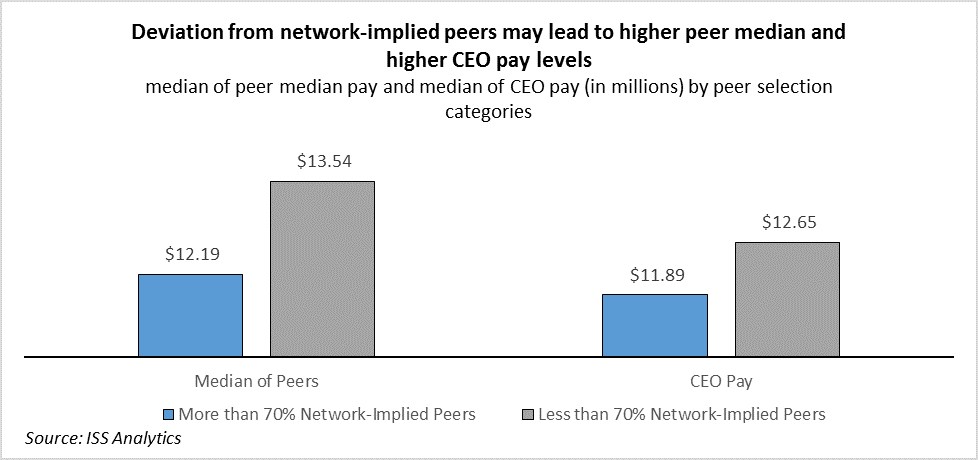

One potential explanation for the higher frequency of say-on-pay opposition for companies that deviate from the network-implied peer group may be quantum of pay. Companies whose peer groups include a lower proportion of wisdom-of-the-crowd peers tend to have higher levels of CEO compensation, while the pay levels of their median peer also tend to be higher compared to firms whose peer selections are more aligned with the network-implied model.

Overall, the peer median of CEO pay of the company-selected peers is greater than the median of the wisdom-of-the-crowd peers for 53 percent of companies. This number jumps to 59 percent of firms when isolating companies that significantly deviated from the network-implied peer group, while it drops to 51 percent of firms for the rest of the universe. These trends suggest that a deviation from the network-implied peer group tends to result in higher pay targets, which materialize in higher levels of pay. Furthermore, we observe slightly higher rates of pay-for-performance misalignment among firms that significantly deviate from the network-implied peer group (10.1 percent of firms, compared to 8.9 percent of firms for the control group).

On a peer-specific level, only 47 percent of the peers chosen by companies that were outside of the network-implied peer group had pay that was higher than the network-suggested median. Therefore, companies are not necessarily adding peers with higher CEO pay values, but rather companies are likely excluding network-implied peers whose CEO pay is in the bottom half of the group. Overall, 63 percent of the optimal peers that were not included in the company’s peer group would have lowered the median CEO pay value of the company peer group if added.

Crowd-sourced peer groups: where to go next?

This academic exercise of picking an alternative group of peers based primarily on peer network data has real-world implications for both companies and investors.

For companies, crowd-sourced peer networks can provide a powerful tool to identify prospective peers, as well as to identify peers that may have weaker connections to the company. The goal isn’t to radically alter a company’s peer group—but rather, to understand where improvements might be sourced, and to prepare for questions about the justification for including certain peers in the peer set. As investors become increasingly sophisticated in their compensation analyses, we see these questions coming up more often.

And for investors, crowd-sourced peer groups can provide an additional viewpoint to compare compensation practices for a portfolio of companies. The goal isn’t to judge the appropriateness of any individual company’s peer group, or to replace ISS’s existing peer group construction methodology—but rather to provide a comparator group, implied by the “wisdom of the crowd,” to base additional pay analyses upon.