Print

PrintArthur H. Kohn is a partner and Katy Yang is an associate at Cleary Gottlieb Steen & Hamilton LLP. This post is based on a Cleary Gottlieb memorandum by Mr. Kohn and Ms. Yang. Related research from the Program on Corporate Governance includes The Case for Shareholder Access to the Ballot by Lucian Bebchuk (discussed on the Forum here), and Private Ordering and the Proxy Access Debate by Lucian Bebchuk and Scott Hirst (discussed on the Forum here).

When the staff (the “Staff”) of the Division of Corporation Finance of the Securities and Exchange Commission (“SEC”) released Staff Legal Bulletin No. 14I (“SLB 14I”) last fall, it seemed that the Staff was potentially signaling that it would be taking a more issuer-friendly approach in its review of no-action letter requests (“NALs”). In particular, the language in SLB 14I regarding the role of the board of directors suggested that the Staff may defer to the board’s determination of whether a shareholder proposal focuses on a significant policy issue, in the case of the “ordinary business” exception (Rule 14a-8(i)(7)), and whether the shareholder proposal is significantly related to the issuer’s business, in the case of the “economic relevance” exception (Rule 14a-8(i)(5)), as long as the NALs provided a sufficiently detailed discussion of the board’s analysis and the “specific processes employed by the board to ensure that its conclusions are well-informed and well-reasoned.” For example, SLB 14I stated that these types of “determinations often raise difficult judgment calls that the Division believes are in the first instance matters that the board of directors is generally in a better position to determine.” One could read that language to mean that including a well-developed board analysis could significantly influence the outcome for a NAL based on the “ordinary business” exception and/or the “economic relevance” exception.

However, as further described below, our analysis of the results of this past proxy season does not seem to evidence that kind of deference to an issuer’s board. Instead, our analysis indicates that a complete board analysis may only make a difference in certain limited scenarios and the factor primarily driving the outcome of a NAL is the Staff’s perception of the extent to which, on its face, the shareholder proposal seeks to micromanage the issuer as opposed to raising a significant policy issue. In other words, certain topics seem to the Staff to be so clearly micromanaging on their face that no board analysis is needed for a favorable outcome, whereas other topics so obviously implicate significant policy issues on their face that even the most complete board analysis cannot persuade the Staff to grant those NALs.

Research Methodology and Scatterplot

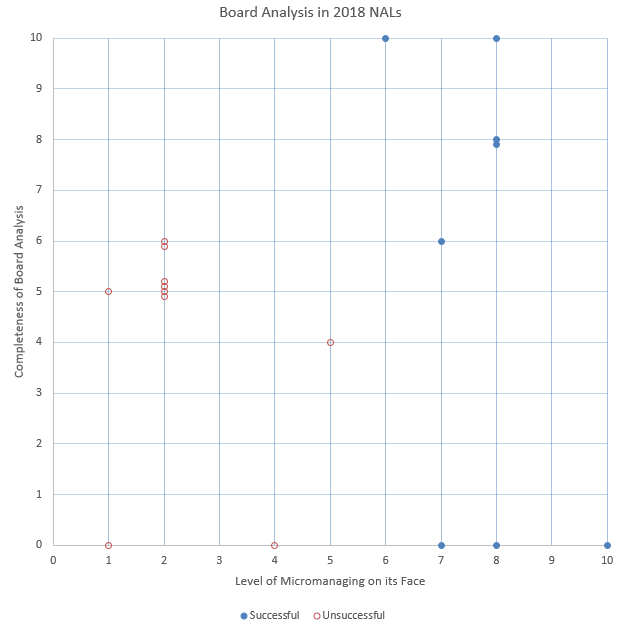

To better understand the Staff’s approach to board analysis, we analyzed the NALs from this past proxy season that received an SEC response citing the “ordinary business” argument and/or the “economic relevance” argument, which resulted in a sample size of 18—eight of which were successful and ten of which were unsuccessful. In our initial review, we noticed that the discussion of board analysis in the successful NALs ranged from very complete to no board analysis at all, with the NALs in the “no board analysis” group addressing proposals that were very obviously micromanaging the issuer (e.g., requesting particular actions regarding specific products being sold by the issuer).

Based on that observation, we thought that perhaps the impact of board analysis on a NAL’s outcome was not so much determined by the completeness of the discussion of board analysis but instead depended on how clearly, in the Staff’s view, the topics addressed by the proposal and supporting statement sought to micromanage the issuer as opposed to raise significant policy issues. To explore this theory, we created a scatterplot to see if there was a relationship between those two factors by assigning each NAL a value from 0 to 10 for each factor.

Our rating of the first factor, the completeness of the board analysis described in the NAL, took into account the level of detail, form, content and what the Staff’s response said about the board analysis. Successful NALs where the Staff cited the board analysis as part of the basis for its concurrence received a 10, whereas the NALs (successful or not) with no board analysis received a 0. The NALs where the Staff said the board analysis was insufficient in some way (i.e. insufficient detail or the failure to address the results of the prior year’s shareholder vote on a similar proposal) were somewhere in the middle, between 4 to 6. In addition, many NALs seemed to follow a similar form in describing board analysis, so those were consistently rated.

Our rating of the second factor, the extent to which the shareholder proposal “on its face” sought to micromanage the issuer as opposed to raise a broader policy issue, took into account the topics addressed, the specific drafting of the proposal and the content of the supporting statement. Proposals in which micromanaging was more obvious and/or that were more narrowly focused (e.g., regarding specific products, grant recipients, or environmental considerations) received higher scores, whereas proposals raising broader policy issues (particularly those topics that the Staff has previously identified as raising significant policy issues, like executive compensation) received lower numbers. However, this rating represents our inference as to the SEC’s perception of the level of micromanagement with respect to the topics raised by each proposal and as such is inherently a subjective assessment.

The results of our analysis are displayed in the scatterplot below:

Observations

General observations. Overall, the successful NALs seemed to involve proposals with a more obvious level of micromanagement regardless of the level of completeness of the board analysis provided, as evidenced by the blue dots clustering towards the right while also spanning the full range of the vertical axis from 0 to 10. The NALs with no board analysis also had higher scores for micromanaging, suggesting that despite the language in SLB 14I to the contrary, no board analysis is actually needed when the proposal and/or supporting statement clearly micromanages the issuer. Conversely, the unsuccessful NALs tended to address proposals that did not as obviously micromanage the issuer on their face and instead were more likely to raise policy concerns, as evidenced by the red dots clustering towards the left. In addition, some NALs were denied despite having the same or similar levels of board analysis as a successful NAL—in particular, note the distribution of red vs. blue dots for no board analysis and for board analysis at levels 5 to 6—with the difference being that the blue dots all fall further right on the horizontal axis measuring the level of micromanagement. This distribution suggests that the SEC’s perception of a proposal’s level of micromanagement has a greater impact on the outcome of the NAL than the completeness of the board analysis provided in connection with an economic relevance or ordinary course argument.

Political topics and prior shareholder support. This year’s results suggest that it may be difficult for issuers to convince the SEC that proposals on lobbying and/or political activity micromanage the issuer and do not raise significant policy issues. Half of the unsuccessful NALs addressed proposals about lobbying, political contributions or political activities, and the board analysis in these NALs had a level of detail, completeness and format that was consistent with one of the successful NALs (around level 5 or 6), suggesting that the description of board analysis was not the dispositive factor. In addition, we note that the Staff responses to these NALs addressing political activity all specifically cited the prior year’s shareholder voting results on a similar proposal as a reason for denial, suggesting that the Staff’s refusal to exclude these proposals may also be due to the fact that they have garnered a critical mass of shareholder support in prior years instead of, or in addition to, the subject matter of political activity. Some SEC responses stated that the board analysis failed to sufficiently address these voting results because although the NAL set forth a number of factors considered by the board, including an apparent lack of investor interest, a similar proposal received more than 25% support in recent years. Other SEC responses remained silent as to the adequacy of the board analysis but noted that it could not concur in the exclusion of the proposal because approximately 40% of the issuer’s shareholders supported a similar proposal last year. This suggests that for proposals garnering lower levels (e.g., ~25%) of shareholder support in prior years, a strong board analysis specifically addressing this fact could make a difference in the Staff’s response, whereas proposals receiving higher levels (e.g., ~40%) of prior shareholder support will not be excluded regardless of the completeness of board analysis.

Environmental topics. In addition, this year’s results suggest that board analysis could potentially make a difference with proposals falling in the middle of the micromanaging/policy issue spectrum. The four NALs falling between 4 through 7 on the micromanaging axis all raised environmental topics (the “Environmental NALs”). Of the Environmental NALs, other than the successful NAL with no board analysis (the “Verizon NAL,” which is further discussed below), the one unsuccessful Environmental NAL had the least complete board analysis of the group, and the Staff’s response to that NAL stated that although the discussion of board analysis set out several factors the board considered, it did not provide a sufficient level of detail for the Staff to determine that exclusion would be appropriate. On the other hand, the successful Environmental NALs generally had more complete board analyses and in fact, the Staff’s response to the NAL with a 10 on board analysis cited the board analysis as part of its basis for concurring with the issuer (the “Apple NAL”). The exception to the foregoing is the Verizon NAL, which was successful despite not including any board analysis. Interestingly, the Verizon NAL cited the Staff’s decision in the Apple NAL in support of its ordinary business argument that the proposal sought to micromanage the issuer’s operations, and was presumably granted on that basis, which reinforces the notion that no board analysis is necessary if the Staff perceives the proposal to be sufficiently micromanaging.