Print

PrintJoseph Kieffer is a Research Analyst at Equilar. This post is based on an Equilar memorandum by Mr. Kieffer.

Since the introduction of Say on Pay, shareholders have maintained a larger degree of influence over CEO compensation. The ability to vote in an advisory capacity on CEO compensation strengthened the voice of shareholders. However, a particularly interesting case arises when the CEO occupies the position of the chair of the board. Potentially, this could create a conflict of interest between the board and management, where the CEO-chair has significant leverage over compensation decisions. It is partly for this reason, in combination with the board’s desire for independent oversight of management, that shareholders often take an active stance in making decisions about CEO-chairs.

For example, The Washington Post recently reported the CEO-Chair of Tesla Inc., Elon Musk, managed to continue to occupy both roles, despite attempts at separation. A single investor proposed the separation of the two positions, but the proposal was eventually rejected with 83.3% of shareholders voting against it. Similarly, Allergan investors pushed for independent occupants of the CEO and chair roles after a year in which the company saw its stock price drop 20.3%. A survey of the Equilar 500—the 500 largest companies by revenue trading on one of the major U.S. stock exchanges—suggests that such proposals are generally unsuccessful, with a single individual typically retaining the position of CEO-chair.

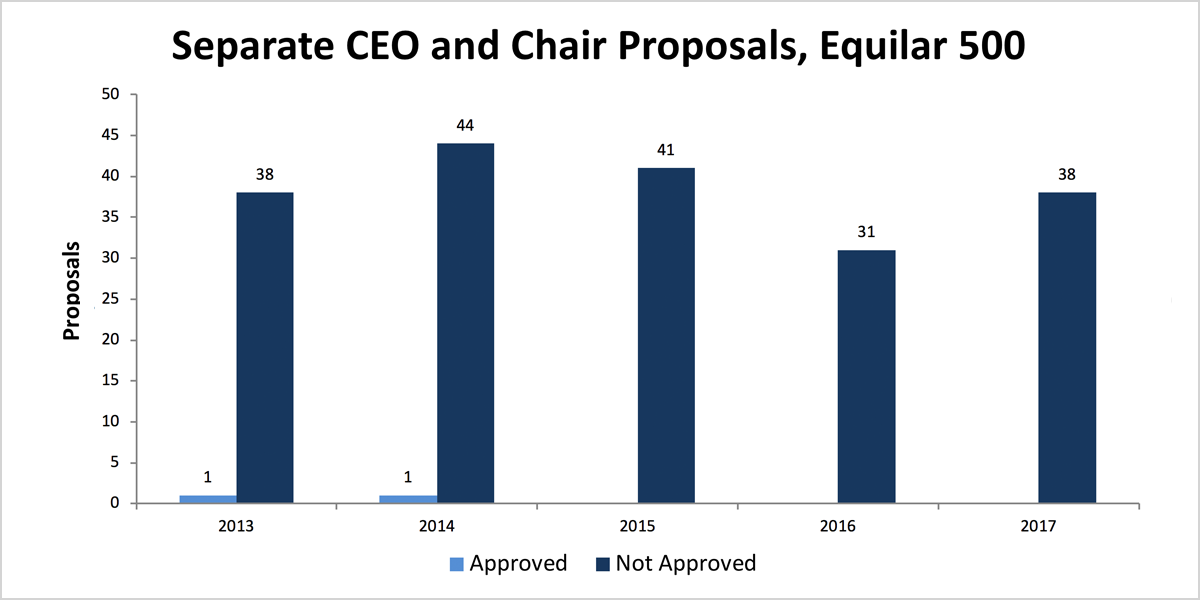

In 2017, 38 companies in the Equilar 500 received a shareholder proposal regarding the implementation of an independent chair—all 38 proposals were rejected. Additionally, many of the 2017 proposals, like those at Chevron, Walmart and Exxon Mobil, are similar to those submitted in previous years, which call for separation of the two positions. In fact, there has been a shareholder proposal requesting an independent chair of the board at Walmart for the past five years.

For a more in-depth analysis of these proposals and why they are brought to the forefront of annual meetings, Equilar examined the cases of a few companies. For the first case, Pfizer’s shareholder proposal, submitted by the Sisters of Philadelphia and other co-filers, suggests that a single person who serves as both the CEO and chair “weakens a corporation’s governance structure,” as found in Pfizer’s 2018 proxy statement. The proposal to separate the two positions cites Andrew Grove, Intel’s former chair, who posed the question, “is the company a sandbox for the CEO, or is the CEO an employee?” The purpose of separating the two roles is to prevent the “excessive management influence” that may unduly result from having a CEO participate in the corporate governance and oversight process. The response by the board highlights the need for a flexible leadership structure, in which the two positions are combined or separated based on the needs of the company at any particular time.

In the case of General Electric, activist investor Kenneth Steiner submitted the proposal, claiming that the lack of a strong lead director role creates an imbalance in the corporate governance structure. As is the case with GE, Steiner cites the examples of Caterpillar and Wells Fargo, which both recently appointed independent board chairmen. The board recommended shareholders vote against this proposal because it found that the current arrangement allows the CEO to lead the company without “any undesirable duplication of work and, in the worst case, lead to a blurring of the clear lines of accountability and responsibility, without any proven offsetting benefits.” In contrast to the position of Steiner, the board believes that its independent directors’ strength “minimize[s] any potential conflicts that may result from combining the roles of CEO and chairman.” The proposal was ultimately rejected.

The third example comes from Bank of America’s most recent proxy, a proposal that was also presented at the request of Kenneth Steiner. As was the case at GE, this proposal references Caterpillar and Wells Fargo as examples where 2016 independent chairmen proposals were strongly opposed, only to see both companies “change course” and elect to separate the two positions. Bank of America provides a lengthy response, mentioning both flexibility and evidence showing separation of the two positions does not result in improved financial performance of the company. Bank of America’s TSR has outperformed its peer group significantly in the past three years, and the board did not see a need to split the two positions. The board also cites a 2015 study, which found that only 4% of companies in the S&P 500 had adopted a policy of separation where a CEO-chair previously existed. A more recent survey, from the same surveyors, claims that only 28% of chairs at S&P 500 companies are independent. A recurring theme found in the 2018 proxies is that, in spite of the fact that particular shareholders see an apparent need for split positions, company performance is not noticeably affected by the joint position and companies ultimately choose to retain it.

A historical look at the results of shareholder proposals related to separating the CEO-chair position at Equilar 500 companies over the last five fiscal years shows that this year is right on trend. Only three companies have approved CEO-chair separation proposals.

While the diversification of power for governance is the main argument for separating the two positions, another potential negative outcome addressed by proponents is the sheer difficulty of shouldering the responsibilities of both positions. Verizon, for example, is preparing to launch a major digital media initiative that may occupy a large part of the CEO’s attention over the next few years, and shareholders may be concerned that this initiative will draw the CEO away from the duties associated with the chairman of the board. However, board responses tend to reference the significant governance capabilities of the lead independent directors, who collectively buttress the company against excessive CEO-chair influence.

Perhaps partly related to the desire to maintain stability and flexibility among the leadership, the board opposes the appointment of two separate individuals as a staunch, written policy. Additionally, a board of directors may have other reasons, such as length of CEO-chair tenure and industry influence, for consolidating the two positions among one individual. An example of the latter is the board of Gilead Sciences, which makes the case that their CEO-chair has a depth of knowledge about the industry and substantial relationships in the scientific and medical communities. The wide-spread rejection of these separation proposals suggests that, while these proposals may be trying to address genuine leadership concerns, shareholders seem to opt for stability and maintenance of consolidated leadership when it comes to actual votes. The need to ensure stability and have intricate knowledge and experience among the company’s leadership causes shareholders to often collectively reject proposals to separate the positions of CEO and chairperson.

* For this blog, 2017 refers to companies that filed proxies from 5/2/2017 to 5/1/2018.*