Print

PrintHolly J. Gregory is partner, Rebecca Grapsas is counsel, and Claire H. Holland is special counsel at Sidley Austin LLP. This post is based on a Sidley memorandum by Ms. Gregory, Ms. Grapsas, Ms. Holland, John P. Kelsh, Thomas J. Kim, and Kai H.E. Liekefett. Related research from the Program on Corporate Governance includes Private Ordering and the Proxy Access Debate by Lucian Bebchuk and Scott Hirst (discussed on the Forum here) and Does Shareholder Proxy Access Improve Firm Value? Evidence from the Business Roundtable Challenge by Bo Becker, Daniel Bergstresser, and Guhan Subramanian (discussed on the Forum here).

Pressure from large institutional investors, including public and private pension funds, and other shareholders has led to the widespread adoption of proxy access by large U.S. public companies in the past few years. Proxy access is now mainstream at S&P 500 companies (71%) and is nearly a majority practice among Russell 1000 companies (48%). Proxy access gives shareholders the power to nominate a number of director candidates for inclusion in the company’s proxy materials.

As a follow-up to our Sidley Corporate Governance Report titled Proxy Access—Now a Mainstream Governance Practice from February 2018, this post provides an overview of the state of proxy access in the U.S. as of the end of 2018. Topics covered include:

- The rapid rise of proxy access at U.S. companies since 2015

- Management and shareholder proposals relating to proxy access

- Institutional investor support for proxy access

- Proxy advisory firm policies on proxy access

- Typical parameters of proxy access provisions

- The fact that proxy access has never been used in the U.S. (though a second attempt is pending)

- Practical guidance for companies considering whether and when to adopt proxy access

The Rapid Rise of Proxy Access

For decades, the Securities and Exchange Commission (SEC) unsuccessfully sought to adopt a market-wide proxy access rule. Most recently, in August 2010, the SEC adopted a proxy access rule (Exchange Act Rule 14a-11) that would have given shareholders holding 3% of the company’s shares for at least 3 years the ability to nominate candidates through the company’s proxy materials. In September 2010, Business Roundtable and the U.S. Chamber of Commerce challenged the validity of Rule 14a-11. In 2011, the U.S. Court of Appeals for the District of Columbia Circuit vacated Rule 14a-11 on the grounds that the SEC had acted “arbitrarily and capriciously” in promulgating the rule without adequately assessing its economic impact. The SEC did not appeal the court’s decision and has not re-proposed any proxy access rule; however, a related amendment to Rule 14a-8 became effective in September 2011, opening the door to shareholder proposals seeking proxy access.

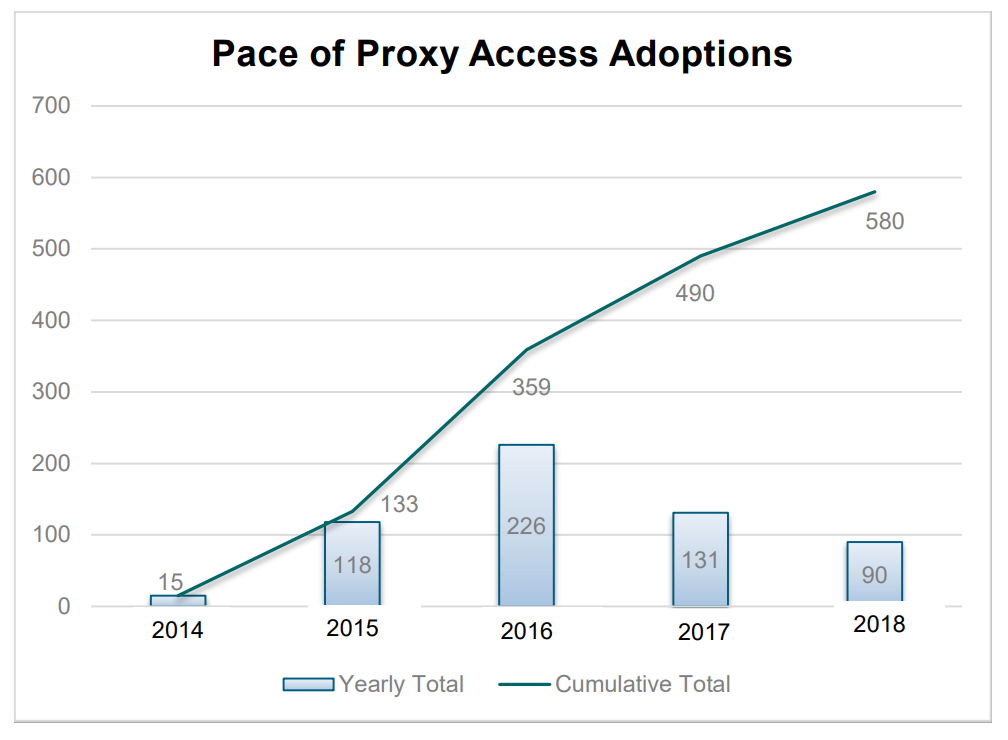

Prior to 2015, proxy access initiatives had limited success and only 15 U.S. companies had adopted proxy access. Shareholder support started to increase in 2014 as proponents began to focus on the “3% for 3 years” ownership requirement adopted by the SEC in its 2010 rulemaking efforts. With a major initiative from public pension funds led by the New York City Comptroller and with encouragement from major investors and the Council of Institutional Investors (CII), a large institutional investor industry group, proxy access quickly took hold. The 2015 proxy season saw a significant increase in the number of shareholder proxy access proposals and shareholder support for such proposals as well as an increased frequency of negotiation and adoption of proxy access via board action. Institutional investors and proxy advisory firms adopted policies supporting proxy access, which added to the momentum.

Through its Boardroom Accountability Project, the New York City Comptroller and New York City Pension Funds targeted over 70 companies with non-binding proposals to adopt proxy access during each of the 2015, 2016 and 2017 proxy seasons. Targeted companies were selected due to concerns about three priority issues: climate change, board and C-suite diversity and excessive executive compensation. Most of the proposals were withdrawn after successful negotiations with the companies. Just four proposals to adopt proxy access filed by the New York City Pension Funds were voted on in 2018, two of which passed. By the end of 2018, more than 150 companies targeted by the New York City Pension Funds since 2015 had adopted proxy access.

Proxy access is now a mainstream bylaw provision at S&P 500 companies—71% at the end of 2018 compared to less than 1% in 2014—and it is extending significantly into the Russell 1000. Reflecting this shift, of the 90 companies that adopted proxy access during 2018, only 46% were S&P 500 companies. Adoption by smaller companies, however, remains relatively rare. According to data from SharkRepellent.net, 48% of Russell 1000 companies but just 4% of Russell 2000 companies have adopted proxy access.

Management and Shareholder Proposals Relating to Proxy Access

Management Proxy Access Proposals

Nine management proposals to adopt proxy access were voted on in 2018, averaging support of 97% of votes cast. Seven proposals passed while two did not because they fell short of the companies’ 80% supermajority vote requirements. Institutional Shareholder Services (ISS) recommended votes for all nine proposals. The number of management proxy access proposals voted on in 2018 was down from 12 in 2017 and 25 in 2016. There were no instances of competing management and shareholder proxy access proposals during the 2018 proxy season.

Shareholder Proxy Access Proposals

Shareholder proposals seeking proxy access were the defining feature of the 2015 and 2016 proxy seasons but their prevalence has declined now that most S&P 500 companies have adopted proxy access. The number of shareholder proposals to adopt proxy access going to a vote has also declined as more companies have adopted proxy access in exchange for potential withdrawal or exclusion of the proposals. The focus has shifted from shareholder proposals to adopt proxy access to shareholder proposals seeking to amend existing proxy access bylaws.

The table below shows the key highlights of voting results on shareholder proxy access proposals over the past five years.

Key Highlights of Shareholder Proxy Access Proposal Voting Results

| Shareholder Proposals to Adopt Proxy Access | 2014 | 2015 | 2016 | 2017 | 2018 |

|---|---|---|---|---|---|

| • Voted On | 18 | 91 | 77 | 36 | 14 |

| • Passed | 5 (28%) | 55 (60%) | 40 (52%) | 19 (53%) | 4 (29%) |

| • Average Support | 34% | 55% | 51% | 54% | 42% |

| Shareholder Proposals to Amend Proxy Access Provisions | 2014 | 2015 | 2016 | 2017 | 2018 |

|---|---|---|---|---|---|

| • Voted On | – | – | 8 | 21 | 27 |

| • Passed | – | – | 2 (25%) | 0 (0%) | 0 (0%) |

| • Average Support | – | – | 44% | 28% | 28% |

*Data points in this post with respect to proxy access proposals are derived from SharkRepellent.net, last accessed on January 5, 2019. All voting results in this report are calculated on the basis of votes cast “for” the proposal divided by the sum of votes cast “for” and “against” that proposal (not taking into account abstentions).

Fourteen shareholder proposals to adopt proxy access were voted on in 2018, averaging support of approximately 42.2% of votes cast. Four of the proposals received majority support, while ten did not pass. Average support at the four companies where proxy access proposals passed was 79%. ISS supported all of the proposals. Management recommended against all but one of the shareholder proposals, for which it provided no recommendation. The fact that only four of fourteen proposals to adopt proxy access passed in 2018 marks a significant shift from 2015, 2016 and 2017 where the majority of shareholder proposals to adopt proxy access passed. Furthermore, average support decreased from 54% in 2017 to 42% in 2018. Possible explanations are that two companies adopted proxy access prior to the vote at their 2018 annual meetings and others are controlled companies or otherwise have concentrated share ownership.

Of the four companies where shareholder proposals to adopt proxy access passed at the 2018 annual meeting, only one has since adopted proxy access. The other three companies each had majority-supported proxy access proposals in previous years as well. One of the companies disclosed in Form 8-Ks in both 2018 and 2017 that the board of directors considered the vote results on the proposals (which received 77% and 75% support) but “concluded that the Company’s governance structure is appropriately designed to promote managing the business for the long term and no change to the Company’s By-Laws is warranted.” These companies may face negative vote recommendations against directors from ISS and Glass, Lewis & Co. (Glass Lewis) under their board responsiveness policies.

Fix-It Proposals

Following the flood of shareholder proposals asking companies to adopt proxy access, a few individual shareholder proponents began submitting proposals in 2016 requesting that companies make specific revisions to their existing proxy access bylaws. These so-called “fix-it” proposals requested some combination of the following amendments:

- An ownership threshold of 3%.

- Loaned shares counting toward the ownership threshold so long as they are recallable.

- Number of proxy access nominees capped at the greater of 25% or 2 directors.

- No limit on the size of the nominating group.

- No restriction on the re-nomination of a proxy access nominee based on the number or percentage of votes received in a prior election.

- No requirement to hold shares after the annual meeting (e.g., for one year) or to express any intention to do so.

- No board authority to amend the proxy access bylaw.

Of the eight fix-it proposals voted on in 2016, two passed (in each case where the proponent requested a reduction of the ownership threshold from 5% to 3%, among other amendments) and average shareholder support was approximately 44%.

Based on SEC Staff determinations discussed below, certain individual shareholder proponents began refining their shareholder proxy access proposals or fix-it proposals to limit them to one or two issues, making it less likely for a company to be able to exclude them. For example, for the 2017 proxy season, certain proponents asked companies solely to increase (to 40 or 50) or remove the nominating group size limit in their proxy access bylaws.

For the 2018 proxy season, certain proponents asked companies to remove the nominating group size limit as well as increase the cap on the number of proxy access nominees.

Twenty-seven shareholder fix-it proposals were voted on in 2018. Average support was 27.8% and none of the proposals passed. ISS supported all of the proposals and management recommended against all of them. Institutional investors generally support shareholder proposals to adopt proxy access but vote against fix-it proposals. The fact that no fix-it proposals passed in 2017 or 2018 despite favorable recommendations from ISS suggests that most shareholders are satisfied with proxy access on terms that have become market standard through private ordering as discussed below.

Appendix A accessible here sets forth the specific proxy access bylaw amendments requested in the fix-it proposals submitted to date as well as details about voting results on the proposals and responses from the SEC Staff to no-action requests to exclude such proposals where applicable.

Grounds for Exclusion of Shareholder Proposals Relating to Proxy Access

A company may seek no-action relief from the SEC Staff to exclude a shareholder proxy access proposal from its proxy materials if the proposal fails to meet any of the procedural and substantive requirements of Exchange Act Rule 14a-8. The primary substantive basis relied on by companies seeking to exclude a shareholder proxy access proposal is that the company has already substantially implemented the proposal (Rule 14a-8(i)(10)). Previously companies also argued that the shareholder proposal directly conflicts with a management proposal (Rule 14a-8(i)(9)), but the SEC Staff issued guidance in 2015 that effectively eliminated companies’ ability to obtain no-action relief on that basis.

Companies that adopted proxy access argued substantial implementation when seeking to exclude proxy access proposals from their 2016, 2017 and 2018 proxy statements and were generally successful. The SEC Staff granted no-action relief to companies that adopted a proxy access bylaw with a “3% for 3 years” ownership threshold mirroring the threshold requested by the proponent, even though the company-adopted bylaw deviated from the specific terms of the proposal in other respects. The SEC Staff determinations suggest that companies have some flexibility to adopt proxy access bylaws tailored to their particular circumstances so long as they track the ownership threshold and duration set forth in the proposal. Presumably, no-action relief will be available even if the company’s proxy access bylaw (1) includes a limit on the number of shareholders that may aggregate to form a nominating group (e.g., 20 versus an unlimited number per the terms of the proposal) or (2) includes a lower percentage or number of board seats available to proxy access nominees than specified in the proposal (e.g., 20% versus “the greater of 25% of the board or two” per the terms of the proposal).

The SEC Staff takes a different approach when evaluating whether a company has substantially implemented a fix-it proposal requesting that specific revisions be made to an existing proxy access bylaw. In 2016, the SEC Staff denied no-action relief to six companies that sought to exclude fix-it proposals under Rule 14a-8(i)(10) where they made no amendments to their existing 3%/3 years/20%/20 proxy access bylaws in response to the proposals. These determinations suggested that companies would not be able to rely on substantial implementation under Rule 14a-8(i)(10) as a basis to exclude fix-it proposals if they do not make any changes to the bylaws in response to the shareholder proposal. In other words, the SEC Staff would not consider the company’s original adoption of proxy access as substantially implementing the essential objective of the fix-it proposal.

In contrast, later in 2016, the SEC Staff granted no-action relief to a company that sought to exclude a fix-it proposal under Rule 14a-8(i)(10) when the company implemented three of the six revisions to the proxy access bylaw sought by the proponent. The board amended the bylaw to (1) reduce the ownership threshold from 5% to 3%, (2) eliminate the requirement for the nominating shareholder to state an intention to maintain ownership for one year beyond the meeting and (3) delete the 25%/2 years re-nomination restriction but did not (1) increase the number of proxy access nominees to the greater of 25% or 2 (rather than the greater of 20% or 2 per the existing bylaw), (2) specify that loaned shares would count toward the ownership threshold so long as they are recallable (rather than recallable on five business days’ notice and recalled upon notice that the nominating shareholder’s proxy access nominee will be included in the proxy statement) and (3) remove the 20-person limit on the size of the nominating group. It is unclear what revisions, alone or in combination, would have been sufficient to persuade the SEC Staff that the company had substantially implemented the proposal, but we believe that the reduction of the ownership threshold from 5% to 3% was critical to the determination.

In early 2017, the SEC Staff granted dozens of requests to exclude fix-it proposals solely seeking to increase the limit on the size of the nominating group from 20 to 50 (or in two cases, 40) shareholders. The SEC Staff granted requests from 31 of 33 companies seeking to exclude such proposals from their 2017 proxy statements on the basis of substantial implementation without making any amendments to their proxy access bylaws. Nearly all of the companies successfully demonstrated in their no-action requests that the existing nominating group size limit achieved the proposal’s goal of providing a meaningful proxy access right. The reason two companies were denied relief appears to be that their no-action requests failed to include specific information regarding the ownership of the company’s institutional holders—as opposed to all holders or large holders—when arguing that the existing proxy access bylaw already provides a meaningful proxy access right. These determinations provided helpful guidance to companies as to how to frame the arguments to obtain no-action relief in future requests to exclude shareholder proposals to increase the limit on the size of the nominating group.

However, uncertainty returned in July 2017 when the SEC Staff denied H&R Block’s request to exclude a fix-it proposal from John Chevedden solely seeking to remove the limit on the size of the nominating group. The SEC Staff was “unable to conclude that H&R Block’s proxy access bylaw compares favorably with the guidelines of the proposal” based on the information presented. The proposal received 33% support at H&R Block’s annual meeting in September 2017 despite a favorable recommendation from ISS. Following this development, John Chevedden and associated proponents submitted eight fix-it proposals for the 2018 proxy season solely seeking to remove the limit on the size of the nominating group, each of which failed (average support was 27%).

In several shareholder proposals for 2018, John Chevedden and associated proponents sought to remove the nominating group size limit as well as increase the cap on the number of proxy access nominees. Four companies requested no-action relief to exclude these proposals on the basis of substantial implementation and the SEC Staff denied such relief.

The SEC Staff granted no-action relief with respect to only one fix-it proposal in 2018. John Chevedden submitted a shareholder proposal at Delta Air Lines, Inc. asking the board to amend the bylaws to provide proxy access for shareholders with seven specified features. Delta’s existing proxy access bylaw already included five of the specified features. It did not, however, provide for (1) the number of proxy access nominees to be the greater of 25% or 2 (rather than the greater of 20% or 2) or (2) no limit (rather than a 20-person limit) on the size of the nominating group. Nevertheless, the SEC Staff found that the existing proxy access bylaw addresses the proposal’s “essential objective” and granted no-action relief on the basis of substantial implementation under Rule 14a-8(i)(10). Interestingly, the SEC Staff may have denied no-action relief if the proposal had been more limited (i.e., if it solely sought to increase the cap on the number of proxy access nominees and remove the nominating group size limit).

Even though average support for shareholder proxy access proposals has declined, we expect that a small number of proponents will continue to submit proposals asking companies to adopt proxy access or amend their proxy access bylaws. We expect the amendments sought in fix-it proposals to be narrow to reduce the likelihood that companies may exclude them. For example, the SEC Staff recently denied no-action relief to Apple Inc. when it sought to exclude a shareholder proposal to amend a proxy access bylaw to provide for the number of proxy access nominees to be the greater of 20% or 2 rather than 20% (rounding down).

Fortunately for companies, even if these fix-it proposals are not able to be excluded from annual meeting ballots, they are unlikely to be majority-supported by shareholders if the existing proxy access bylaw has standard terms (e.g., 3%/3 years/20%/20).

Institutional Investor Support for Proxy Access

Institutional investors, including BlackRock, CalPERS, CalSTRS, Fidelity, J.P. Morgan, the New York City Pension Funds, State Street Global Advisors, TIAA, T. Rowe Price, the United Brotherhood of Carpenters and Vanguard, universally support proxy access. This widespread support affects companies’ ability to defeat proposals to adopt proxy access.

In October 2018, a group of 21 prominent business and investment leaders published Commonsense Principles 2.0, an update to its 2016 predecessor, the Commonsense Principles of Corporate Governance. The revised principles are a set of corporate governance best practices designed for “sound, long-term-oriented corporate governance.” While the 2016 version did not take a position on proxy access, the principles now recommend that public companies allow for some form of proxy access.

CII has long supported proxy access, favoring a broad-based SEC rule imposing proxy access. Absent such a rule, CII’s Corporate Governance Policies state that a company should provide access to management proxy materials for an investor or group of investors that has held in the aggregate at least 3% of the company’s voting stock for at least 2 years, to nominate less than a majority of the directors.

In July 2017, CII issued an update to its guidelines, originally published in August 2015, that set forth what it considers best practices for companies adopting proxy access provisions. The guidelines identify provisions that, if drafted otherwise, could “significantly impair shareholders’ ability to use” proxy access. CII suggests the following proxy access terms, among others:

- A minimum ownership threshold of 3%.

- A requirement that shareholders own stock for at least 2 years before using proxy access (however CII recognizes that a 3-year holding period is standard).

- Providing shareholders with the option to nominate at least 2 proxy access candidates.

- No limitation on the number of shareholders that may aggregate their shares to form a nominating group (however CII recognizes that a cap of 20 is standard).

- No requirement that nominators must continue to hold the required percentage of stock after the annual meeting.

- Counting loaned securities toward the ownership threshold and providing at least a 5-day window if nominating shareholders must recall loaned shares to count them.

- Treating as one shareholder two or more funds that are (1) either under common management and investment control, (2) under common management and funded primarily by the same employer or (3) considered a group of investment companies as defined by the Investment Company Act of 1940.

- No adjustment to the shareholder nominee cap for directors previously elected through proxy access, unless proxy access nominees from the current and previous 2 annual meetings would constitute a majority of the board (look-back period should not exceed 2 years).

- No re-nomination restrictions if a proxy access nominee fails to obtain a specified minimum percentage of votes in a previous election.

- No automatic suspension of proxy access for all shareholders in the event of a proxy contest (although CII does not oppose provisions that bar the concurrent use of a proxy contest and proxy access).

Three provisions that CII finds objectionable are very commonly included in the proxy access bylaws that have been adopted to date: (1) a limit on the size of the nominating group, (2) a reduction in the shareholder nominee cap for directors elected through proxy access in the past 2 years and (3) re-nomination restrictions based on a failure to obtain a specified minimum percentage of votes in the past 2 years.

Some institutional investors that favor proxy access coordinated their efforts during the 2015 proxy season in an attempt to increase investor support for the proxy access proposals they sponsored. Specifically, the New York City Pension Funds, CalPERS and other large labor-affiliated pension funds each filed Form PX14A6Gs with the SEC enabling them to communicate in support of their proxy access proposals (but not collect actual proxies) without such communications being subject to the proxy solicitation rules. The New York City Pension Funds partnered with CalPERS again in 2016, 2017 and 2018 to conduct exempt solicitations in support of proxy access proposals.

According to a report on the 2018 proxy season by Broadridge and PricewaterhouseCoopers, institutional investors are nearly three times more likely to support shareholder proxy access proposals than are individual investors: 35% of votes cast by institutional investors were in favor of shareholder proxy access proposals in the first half of 2018, compared with only 13% of those cast by individual retail investors. (Institutional investors supported 61% of proxy access proposals in 2015—the reason for the sharp decline in the level of support from institutional investors is that most 2018 proposals sought to amend existing proxy access provisions rather than adopt proxy access and institutional investors generally do not support fix-it proposals.) The report also indicated that retail investors voted only 28% of the shares they own (compared with 91% of institutional investors). These findings suggest that companies facing a shareholder proxy access proposal should seek out opportunities to engage with retail investors and encourage them to vote.

Proxy Advisory Firm Policies on Proxy Access

Both ISS and Glass Lewis generally favor proxy access for significant, long-term shareholders.

ISS

ISS policy does not address the unilateral adoption or amendment of proxy access bylaws. ISS generally recommends in favor of shareholder and management proxy access proposals with all of the following features:

- An ownership threshold of not more than 3% of the voting power.

- A holding period of no longer than 3 years of continuous ownership for each member of the nominating group.

- Minimal or no limits on the number of shareholders that may form a nominating group.

- A cap on the number of available proxy access seats of generally 25% of the board.

ISS will review any additional restrictions for reasonableness and will generally recommend a vote against proposals that are more restrictive than the ISS guidelines. In 2018, ISS recommended votes for all shareholder and management proposals to adopt proxy access or amend proxy access bylaws.

ISS may issue negative vote recommendations against directors of companies that do not implement a majority-supported shareholder proxy access proposal substantially in accordance with its terms. ISS FAQs set forth what ISS will examine when evaluating a board’s response to a majority-supported proposal. ISS has issued negative vote recommendations against directors at a limited number of companies where they adopted proxy access bylaws with secondary provisions that ISS deemed “significantly more restrictive than the shareholder proposal” without providing adequate disclosure regarding the rationale for the additional restrictions or engagement with shareholders regarding the proxy access bylaw.

ISS will vote case-by-case on proxy access nominees considering various factors specific to the nominee/nominator, company and election (such as whether there are more candidates than board seats).

ISS’ QualityScore corporate governance rating tool includes five scored questions relating to proxy access:

- Does the company provide proxy access to shareholders? (ISS will not award credit if the proxy access bylaw includes “problematic provisions” specified by ISS that nullify the proxy access right.)

- What is the ownership threshold for proxy access? (ISS notes that most companies have adopted a 3% threshold.)

- What is the ownership duration for proxy access? (ISS considers a holding period of longer than 3 years to be excessive.)

- What is the cap on shareholder nominees to fill board seats from proxy access? (ISS notes that generally investors have approved a range of 20-25% of the board, and that many companies have adopted a “greater of 2 directors or 20% of the board” standard.)

- What is the aggregation limit on shareholders to form a nominating group for proxy access? (ISS notes that an aggregation limit of 20 shareholders has generally been considered a minimal restriction.)

Glass Lewis

Glass Lewis evaluates shareholder proposals to adopt proxy access on a case-by-case basis, taking into consideration the minimum ownership and holding period requirements, company size and performance, responsiveness to shareholders and several other factors set forth in Glass Lewis’ proxy voting policies.

Glass Lewis evaluates proxy access fix-it proposals on a case-by-case basis, considering the company’s existing proxy access provisions to assess whether they unnecessarily restrict shareholders’ ability to use proxy access. If the existing proxy access provisions “reasonably conform with broad market practice,” Glass Lewis will generally recommend against fix-it proposals. However, Glass Lewis may recommend in favor of a fix-it proposal if the company has an unnecessarily restrictive proxy access provision and the proposal directly addresses areas of the provision that Glass Lewis believes warrant shareholder concern.

Under a revised policy for 2019, if a company has adopted a special meeting right of 15% or lower and a reasonable proxy access bylaw, Glass Lewis will generally recommend voting against any shareholder proposal asking the company to provide shareholders with the right to act by written consent.

Typical Parameters of Proxy Access Provisions

Over the past four years, proxy access provisions have progressively converged on market standard terms. The majority of proxy access provisions adopted since the beginning of 2015—including 84% of the proxy access bylaws adopted in 2018—have the following terms: 3% for 3 years for up to 20% of the board (at least 2 directors) with a nominating group size limit of 20.

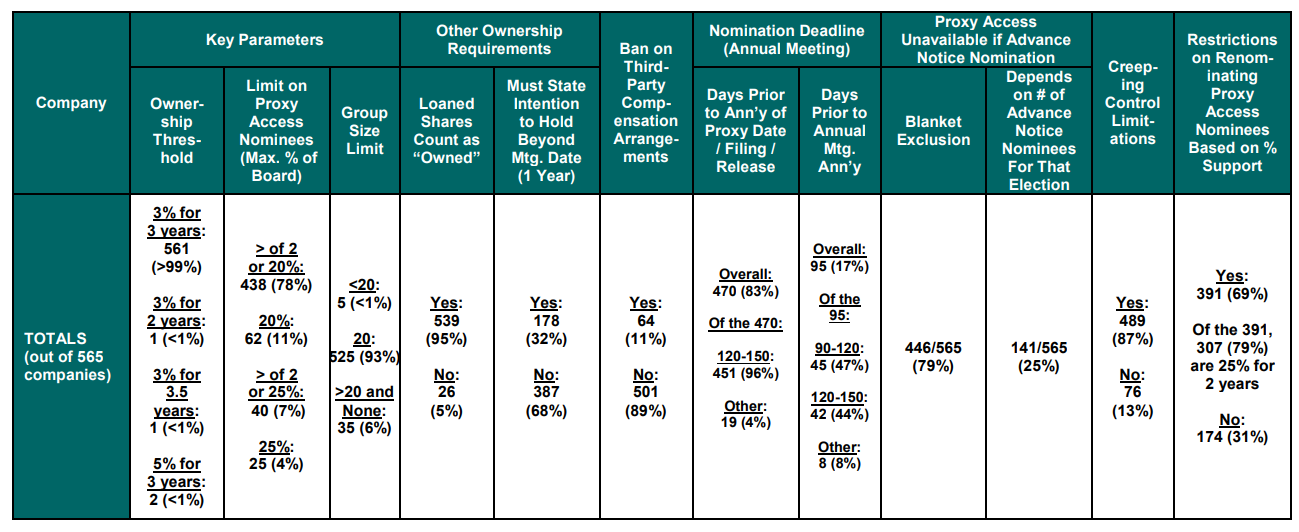

Appendix B accessible here highlights, on a company-by-company basis, the various detailed terms of proxy access provisions adopted by 565 companies since the beginning of 2015. The chart lists the key parameters of the proxy access provisions, including the minimum ownership threshold, maximum percentage of board seats open to proxy access nominees and maximum number of shareholders that can comprise a nominating group. It also covers select terms relating to the treatment of loaned shares, representations regarding intentions with respect to post-meeting ownership, third-party compensation arrangements, nomination deadlines, exclusion of proxy access nominees if a director has been nominated under the advance notice provision, “creeping control” limitations and re-nomination restrictions. The table below highlights the prevalence of the various terms of the proxy access provisions adopted to date.

Notably, certain of the terms that have become standard do not match the terms sought by shareholder proponents or set forth in CII’s proxy access best practice recommendations. In addition to the terms covered in the table above, proxy access provisions delineate various procedural and informational requirements, proxy access nominee eligibility conditions and circumstances in which a company will not be required to include a proxy access nominee in its proxy materials.

Typical Provisions

Net Long Beneficial Ownership of 3% or 5%

3% for 3 years is the nearly universal ownership threshold (561 out of 565 companies (>99%)). Fourteen companies that initially adopted proxy access at a 5% ownership threshold subsequently amended their bylaws to decrease the required ownership percentage to 3%.

A nominating shareholder is typically deemed to own only those outstanding common shares of the company as to which the shareholder possesses both the full voting and investment rights and the full economic interest in such shares. For example, shares subject to any derivative arrangement entered into by the shareholder or any of its affiliates would not qualify as eligible ownership for proxy access purposes. Loaned shares explicitly count as “owned” for purposes of meeting the ownership threshold in the vast majority of proxy access provisions (539 out of 565 companies (95%)), subject to certain conditions. Where loaned shares count toward ownership, most provisions require that the nominating shareholder has the power to recall the loaned shares within a specified

time frame (most commonly, on 3 or 5 business days’ notice). Several provisions require that the nominating shareholder has actually recalled the loaned shares within a specified time frame or prior to a specified time (e.g., by the record date or prior to submission of the nomination notice).

Holding Period

All of the proxy access provisions adopted since January 1, 2015 provide that the nominating shareholder must own the requisite percentage of shares for at least 3 years with two exceptions that have 2-year and 3.5-year holding periods. A nominating shareholder is typically required to continue to own the requisite percentage of shares until the nomination date, the record date and annual meeting date and, at 178 out of 565 companies (32%), is required to represent whether or not it intends to, or in some cases will, continue to own the requisite shares for at least one year after the annual meeting.

Nominee Limit and Procedure for Selecting Candidates if Nominee Limit is Exceeded

A significant majority of companies limit the number of board seats available to proxy access nominees to the greater of 2 or 20% of the board (438 out of 565 companies (78%)) and this has become standard in recent years. Some companies have limited the number of board seats available to proxy access nominees to 20% of the board, without specifying a minimum of at least two proxy access nominees (62 out of 565 companies (11%)). Dozens of companies have adopted a 25% cap (65 out of 565 companies (12%)), 40 of which provide for a minimum of 2 proxy access nominees.

In most cases, if the calculation of the maximum number of proxy access nominees does not result in a whole number, the maximum number of proxy access nominees that the company would be required to include in its proxy materials would be the closest whole number below the applicable percentage (e.g., 20% or 25%). Even though the greater of 2 or 20% of the board has become standard, companies that adopt proxy access at that threshold remain vulnerable to shareholder proposals seeking to increase (e.g., to 25%) or remove the limit. John Chevedden submitted a new variation of fix-it proposal at six companies for 2018 that requested the following nominee limit: not less than 2 directors when the board has less than 12 members and not less than 3 directors when the board has more than 12 members (note that the proposal does not specify what the minimum number of proxy access nominees would be if the board size is 12). None of the proposals received majority support from shareholders. For the 2019 proxy season, James McRitchie submitted a shareholder proposal at Apple Inc. to amend the company’s proxy access bylaw solely to provide for the number of proxy access nominees to be the greater of 20% or 2 rather than 20% (rounding down to the nearest whole number).

Nearly all proxy access provisions provide that if a vacancy occurs on the board after the nomination deadline but before the date of the annual meeting, and the board decides to reduce the size of the board in connection with the vacancy, the nominee limit would be calculated based on the reduced number of directors. Any proxy access nominee who is either subsequently withdrawn or included by the board in the proxy materials as a board-nominated candidate typically would count against the nominee limit (including, in some cases, for a specified number of future years). One-quarter of proxy access provisions provide that the maximum number of proxy access nominees that the company would be required to include in its proxy materials will be reduced by the number of director candidates nominated by any shareholder pursuant to the company’s advance notice provisions (141 out of 565 companies (25%)). A small number of companies with classified boards have limited the maximum number of proxy access nominees to no more than half of the candidates up for election at the annual meeting.

Any nominating shareholder that submits more than one nominee would be required to provide a ranking of its proposed nominees. If the number of proxy access nominees from all nominating shareholders exceeds the nominee limit, the highest ranking qualified person from the list proposed by each nominating shareholder, beginning with the nominating shareholder with the largest qualifying ownership and proceeding through the list of nominating shareholders in descending order of qualifying ownership, would be selected for inclusion in the proxy materials, with the process repeating until the nominee limit is reached.

Limitation on the Size of the Nominating Group

All but 14 companies limit the number of shareholders that are permitted to comprise a nominating group. A nominating group size limit of 20 is by far the most common (525 out of 565 companies (93%)); however, 5 companies set a lower limit (e.g., 5, 10 or 15) and 21 companies set a higher limit (e.g., 25, 30, 35 or 50). Even companies that adopt proxy access with a standard nominating group size limit of 20 remain vulnerable to shareholder proposals seeking to increase or remove the limit. Proxy access provisions often also provide that a shareholder cannot be a member of more than one nominating group. Many companies require that one group member be designated as authorized to act on behalf of all other group members. It is extremely common to provide that members of the same fund family count as one shareholder for purposes of this limit, particularly in light of current ISS policy that would deem “especially problematic” a provision that would treat such individual funds as separate shareholders.

Nomination Deadline; Limited to Annual Meetings

Requests to include proxy access nominees in the company’s proxy materials typically must be received within a window of 120 to 150 days before the anniversary of (1) the date on which the company released its proxy statement for the previous year’s annual meeting (451 out of 565 companies (80%)) or (2) the previous year’s annual meeting (42 out of 565 companies (7%)). Less commonly, the deadline is a window of 90 to 120 days before the anniversary of the previous year’s mailing date (13 out of 565 companies (2%)) or annual meeting date (40 out of 565 companies (7%)). Thirteen out of 565 companies (2%) require that requests be received prior to the date that is 120 days before the date the company released its proxy statement to shareholders in connection with the previous year’s annual meeting (i.e., the same as the deadline for shareholder proposals under Exchange Act Rule 14a-8, which does not incorporate a window). Proxy access provisions typically specify that proxy access may be used only with respect to director elections at annual meetings (but not special meetings) of shareholders. Several companies that have adopted proxy access specified that the right cannot be used until the following year’s annual meeting.

Information Required of All Nominating Shareholders

Each nominating shareholder is typically required to provide certain information to the company, including:

- Verification of, and information regarding, stock ownership as of the date of the submission and the record date for the annual meeting (including in relation to derivative positions).

- The Schedule 14N the shareholder filed with the SEC.

- Information regarding each proxy access nominee, including biographical and stock ownership information.

- The written consent of each proxy access nominee to be named in the proxy statement and serve as a director if elected as well as the public disclosure of the information provided by the shareholder regarding the proxy access nominee.

- A description of any arrangement with respect to the nomination between the shareholder and any other person.

- Any other information relating to the shareholder that is required to be disclosed pursuant to Section 14 of the Exchange Act, and the rules and regulations promulgated thereunder.

- The written consent of the shareholder to the public disclosure of the information provided to the company. Nominating shareholders are generally permitted to include in the proxy statement a 500-word statement in support of their nominees. The company may omit any information or statement that it, in good faith, believes would violate any applicable law or regulation.

Nominating shareholders are also typically required to make certain written representations to and agreements with the company, including in relation to:

- Lack of intent to change or influence control of the company.

- Intent to maintain qualifying ownership through the annual meeting date and, at 178 out of 565 companies (32%), for a specified timeframe (e.g., one year) beyond the meeting date.

- Refraining from nominating any person for election to the board other than its proxy access nominees.

- Intent to be present in person or by proxy to present its nominees at the meeting.

- Not participating in any solicitation other than that relating to its nominees or board nominees.

- Not distributing any form of proxy for the annual meeting other than the form distributed by the company.

- Complying with solicitation rules and assuming liability and providing indemnification relating to the nomination, if required.

- The accuracy and completeness of all information provided to the company.

Information Required of All Proxy Access Nominees

Each proxy access nominee is typically required to make certain written representations to and agreements with the company, including in relation to:

- Acting in accordance with his or her duties as a director under applicable law.

- Not being party to any voting agreements or commitments as a director that have not been disclosed to the company.

- Not being party to any compensatory arrangements with a person or entity other than the company in connection with such proxy access nominee’s candidacy and/or service as a director that have not been disclosed to the company.

- Complying with applicable laws and stock exchange requirements and the company’s policies and guidelines applicable to directors.

- The accuracy and completeness of all information provided to the company.

Proxy access nominees are also typically required to submit completed and signed D&O questionnaires. Several companies have adopted a provision requiring each proxy access nominee to submit an irrevocable resignation to the company in connection with his or her nomination, which would become effective upon the board’s determination that information the proxy access nominee provided in connection with the nomination is untrue or misleading or that the nominee or the nominating shareholder breached any obligations to the company.

Exclusion or Disqualification of Proxy Access Nominees

It is typical for proxy access provisions to permit exclusion of proxy access nominees from the company’s proxy statement if any shareholder (or at some companies, specifically the nominating shareholder) has nominated any person (or at some companies, one or more of the proxy access nominees) to the board pursuant to the company’s advance notice provisions (446 out of 565 companies (79%)).

In addition, the company is typically not required to include a proxy access nominee in the company’s proxy materials if any of the following apply:

- The nominee withdraws, becomes ineligible or does not receive at least a specified percentage (most commonly 25%) of the votes cast at his or her election. Such person is typically ineligible to be a proxy access nominee for the 2 annual meetings following such vote. Re-nomination restrictions based on failed support in previous years appear in 69% (391 of 565) of the proxy access bylaws adopted since January 1, 2015, 79% (307 of 391) of which disqualify a proxy access nominee for 2 years for failure to receive at least 25% support. Companies that adopt proxy access bylaws with re-nomination restrictions remain vulnerable to shareholder proposals seeking removal of such restrictions.

- The nominating shareholder participates in the solicitation of any nominee other than its nominees or the board’s nominees.

- The nominee is or becomes a party to a compensatory arrangement with a person or entity other than the company in connection with such nominee’s candidacy or service as a director that has not been disclosed to the company or, at 64 out of 565 companies (11%), under any circumstances, whether or not disclosed.

- The nominee is not independent under any applicable independence standards. Many companies require nominees to meet heightened standards of independence applicable to audit committee and/or compensation committee members under SEC, stock exchange and/or IRS rules.

- The election of the nominee would cause the company to violate its charter or bylaws, any stock exchange requirements or any laws, rules or regulations.

- The nominee has been an officer or director of a competitor (often as defined in Section 8 of the Clayton Antitrust Act of 1914) within the past 3 years.

- For certain financial institutions subject to compliance with Section 164 of the Dodd-Frank Act, the nominee has been a director, trustee, officer or employee with management functions for any depository institution, depository institution holding company or entity that has been designated as a systemically important financial institution (each as defined in the Depository Institution Management Interlocks Act).

- The nominee is the subject of a pending criminal proceeding or has been convicted in a criminal proceeding within the past 10 years.

- The nominee is subject to any order of the type specified in Rule 506(d) of Regulation D promulgated under the Securities Act.

- The nominee or the nominating shareholder has provided false or misleading information to the company or breached any obligations under the proxy access provision.

Proxy access provisions at 489 out of 565 companies (87%) include “creeping control” limitations that take various forms. A proxy access nominee elected by shareholders will typically count toward the proxy access nominee limit in future years (most often 2 years and sometimes 3 years after election); this is the case at 481 out of 565 companies (85%). In addition, the limit is reduced at 226 out of 565 companies (40%) by the number of director candidates that will be included in the proxy statement as unopposed as a result of an agreement, arrangement or other understanding between the company and a shareholder. At a minority of companies, if a nominating shareholder’s nominee is elected to the board, then such nominating shareholder may not utilize proxy access for the following 2 or 3 annual meetings (other than with respect to the nomination of the previously elected proxy access nominee).

The board or the chair of the annual meeting may declare a director nomination by a shareholder to be invalid, and such nomination may be disregarded, if the proxy access nominee or the nominating shareholder breaches any obligations under the proxy access provision or the nominating shareholder does not appear at the annual meeting in person or by proxy to present the nomination.

Increasingly proxy access bylaws specify that the board has authority to interpret the proxy access provision and make related determinations in good faith. As discussed in a 2016 ISS report on proxy access and an update published in April 2017, ISS characterized any such provision as a “particularly contentious restriction.” In its Governance QualityScore Technical Document, ISS includes “providing the board with broad and binding authority to interpret the provision” as an example of a “problematic provision” in a proxy access bylaw that may “nullify it as a practical right for shareholders.” ISS indicated that including problematic provisions in a proxy access bylaw that are deemed sufficient to nullify the proxy access right would prevent a company from receiving “credit” for adopting proxy access for QualityScore purposes. Despite these statements from ISS, a review of the QualityScore reports of certain companies with proxy access bylaws that include broad board interpretation provisions revealed that such companies still received credit for adopting proxy access, suggesting that ISS may not view that provision alone as sufficient to nullify the proxy access right.

In the updated version of its Proxy Access: Best Practices report issued in July 2017, CII sets forth its position that the ability to interpret proxy access bylaws should be subject to judicial review rather than in the sole discretion of the board. In our view, ISS’s and CII’s concern is misplaced given that boards have the ability to interpret bylaws pursuant to Delaware law whether or not such an explicit interpretation provision is included in a proxy access bylaw.

Proxy Access Has Never Been Used in the U.S.—Second Attempt is Pending

To date, no shareholder has included a director nominee in the proxy materials of a U.S. company pursuant to a proxy access right. There have been only two attempts to use proxy access in the U.S.—one failed and the other is pending.

The first attempt to use proxy access, in November 2016, was promptly withdrawn. GAMCO Asset Management Inc. and Gabelli Funds, LLC, entities affiliated with activist investor Mario Gabelli (collectively, GAMCO), attempted to use proxy access to nominate a director at National Fuel Gas Company’s 2017 annual meeting. National Fuel had adopted proxy access in March 2016 on standard terms. GAMCO, which disclosed ownership of 7.8% of National Fuel’s common stock in its Schedule 14N, had owned greater than 3% for more than 3 years. Two weeks after the Schedule 14N filing, National Fuel disclosed in a Form 8-K that it had rejected

GAMCO’s proxy access nominee on the grounds that GAMCO could not comply with the terms and conditions set forth in the proxy access bylaw. National Fuel’s proxy access bylaw included a typical requirement that the nominating shareholder acquired the shares “in the ordinary course of business and not with the intent to change or influence control of the Corporation, and does not presently have such intent.” National Fuel argued that GAMCO could not comply with that requirement because its Schedule 13D filings throughout its investment reflected a control intent and it had previously pressured the company to spin-off certain of its assets. Five days after the Form 8-K filing, GAMCO disclosed that its proxy access nominee had withdrawn his nomination at National Fuel and that “GAMCO will not pursue Proxy Access.” The following year GAMCO submitted a shareholder proposal requesting that National Fuel’s board take steps “to participate in the rapidly consolidating natural gas local distribution (“LDC”) sector.” The board recommended against the proposal, which received only 11.2% support at the company’s annual meeting in March 2018.

This first attempt to use proxy access at a U.S. company by a known activist was surprising given the nomination restrictions relating to control intent—although the result was not a surprise. It serves as a reminder to companies considering adopting proxy access bylaws to thoughtfully consider the eligibility requirements applicable to nominating shareholders and proxy access nominees.

More than two years later, the second attempt to use proxy access at a U.S. company surfaced. On December 27, 2018, The Austin Trust dated January 1, 2006 (with Steven Colmar as trustee) filed a Schedule 14N seeking to use proxy access to nominate a director at The Joint Corp.’s 2019 annual meeting. The Joint Corp. had adopted proxy access in August 2018 on standard terms after a shareholder proposal to adopt proxy access submitted by Colmar was approved (with 96.05% support) at the company’s annual meeting in June 2018. (The board had not made a recommendation for or against the proposal.) According to the Schedule 14N, Colmar co-founded The Joint Corp. and served on its board of directors from 2010 to 2017 and is the brother of The Joint Corp.’s corporate secretary. The Form 8-K filing disclosing Colmar’s resignation from the board in March 2017 stated that he had previously “expressed disagreements about the Company’s strategic direction and management’s ability to execute upon it.” Colmar reportedly met the director nominee, Glenn Krevlin, in connection with The Joint Corp.’s initial public offering in 2014. Krevlin, founder of the hedge fund Glenhill Capital, was listed as beneficially owning 16.6% of The Joint Corp.’s common stock in the most recent proxy statement filed in April 2018, but his beneficial ownership had decreased to 3.8% due to stock sales as of May 2018 according to a Schedule 13D filing. The Joint Corp. has not made any filings since the Schedule 14N was filed and likely will not file its proxy statement for the 2019 annual meeting until April.

Practical Considerations

Companies have several alternatives when considering whether and when to adopt proxy access. We expect that many companies will continue to follow a “wait-and-see” approach, particularly if they have not received a shareholder proxy access proposal. Some companies may choose to proactively adopt a proxy access bylaw by board action or file a management proxy access proposal to gauge shareholder support at the next annual meeting. A company that proactively adopts proxy access should ensure that it can justify any provision with thresholds that differ from the following terms which have become market standard: 3% for 3 years for up to 20% of the board (at least 2 directors) with a group size limit of 20 (e.g., by disclosing preferences of its shareholders as communicated to the company through engagement).

If faced with a shareholder proposal to adopt proxy access, counsel should be prepared to help the board and management consider the full range of options available given the company’s circumstances. A proxy access proposal with a 3% for 3 years ownership threshold is likely to receive majority shareholder support at a company that does not have a high degree of insider ownership and has not previously adopted proxy access. Therefore, a company may consider adopting proxy access on its own terms rather than putting the shareholder proposal up for a vote. Doing so may enable a company to negotiate a withdrawal from the proponent. Keep in mind that some shareholder proponents are more willing to withdraw proposals than others (e.g., generally, the New York City Comptroller will withdraw but certain individual proponents will not), and that the process to negotiate a withdrawal may be protracted.

Alternatively, in light of the SEC Staff’s grants of no-action relief on the basis of “substantial implementation,” a company will likely be able to exclude the shareholder proposal so long as the company’s proxy access bylaw tracks the proposal’s “3% for 3 years” ownership threshold, although this may not be the case if the proposal seeks a single specific provision that the company has not implemented (e.g., no limit on the size of the nominating group).

If a company is not able to have a shareholder proposal to adopt proxy access withdrawn or excluded, it may still consider adopting prior to the vote—or putting up a management proposal to adopt—proxy access on market standard terms, which would make it very unlikely that the shareholder proposal would pass.

Companies that have already adopted proxy access on market standard terms should bear in mind that shareholders are increasingly submitting proposals seeking to modify the terms of their proxy access bylaws. As discussed above, the ability to have such proposals withdrawn or excluded is far less certain than with respect to shareholder proposals seeking adoption of proxy access. Even if a company is unable to obtain no-action relief to exclude a fix-it proposal, such a proposal is very unlikely to receive majority support from shareholders.

As companies are considering these alternatives, they should:

- Follow developments in this area and keep the nominating and corporate governance committee and the full board generally apprised.

- Know the preferences of their shareholder base (as evidenced in proxy voting policies and other public statements, and voting history on proxy access proposals) and engage with shareholders with respect to proxy access.

- Keep abreast of proxy advisory firm policies and guidance relating to proxy access. Specifically, companies should consider the likelihood of negative vote recommendations against directors under the ISS FAQs discussed above if the board has failed to act on a majority-supported shareholder proxy access proposal.

- Stay apprised of the key parameters and other terms upon which companies are adopting proxy access.

- Be aware of the SEC Staff’s position with respect to requests to exclude shareholder proxy access proposals and fix-it proposals seeking to amend proxy access bylaws.

- Prepare a draft proxy access provision and thoughtfully consider its secondary features (e.g., eligibility restrictions applicable to nominating shareholders and proxy access nominees).

- Review the advance notice and director qualification provisions in their bylaws and consider whether and, if so, how such provisions may be aligned with a proxy access provision if implemented. In addition, companies that have cumulative voting in place may wish to consider eliminating (or requiring suspension of) cumulative voting if a proxy access nominee is included in the company’s proxy materials.

The complete publication, including footnotes and Appendix, is available here.