Print

PrintNick Dawson is Co-Founder and Managing Director of Proxy Insight. This post is based on a Proxy Insight memorandum by Mr. Dawson. Related research from the Program on Corporate Governance includes The Powerful Antitakeover Force of Staggered Boards: Theory, Evidence, and Policy by Lucian Bebchuk, Charles C. Coates, and Guhan Subramanian; The Costs of Entrenched Boards by Lucian Bebchuk and Alma Cohen; and Reexamining Staggered Boards and Shareholder Value by Alma Cohen and Charles C. Y. Wang (discussed on the Forum here).

Classified or staggered boards may be the norm in some markets, but they are generally not seen as part of corporate governance best practice. In the US, in particular, the tide of opinion is turning against them. Their opponents argue that, by only putting a part of the board up for re-election each year, they serve to entrench management, make it harder to replace underperforming directors and insulate board members from the consequences of poor conduct.

Many asset managers state in their voting policies that they will support the declassification of boards and oppose proposals to classify them. In practice, however, it seems that the larger part of investors will be happy either way.

Down for Whatever

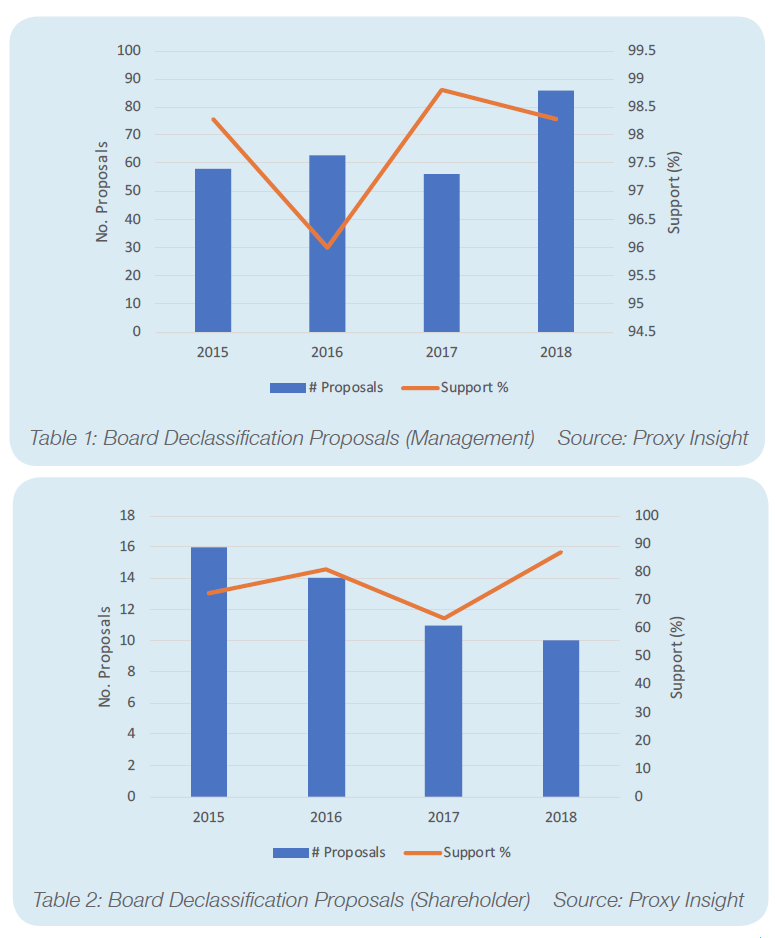

It should come as no surprise that resolutions seeking to declassify them tend to receive solid levels of support. In fact, whether they come from management or shareholders, they tend to be backed overwhelmingly. Management proposals received 98.3 percent support last year on average. While those put forward by shareholders were less successful, they still received very high levels of support. On average, they were backed by a decisive 87.1 percent of shareholders.

Our database contains voting results for 80 management declassification proposals and a further seven from shareholders last year. Not one of these failed to receive a majority of the vote. In fact, only one received less than 70 percent support; a shareholder proposal at Axon Enterprise Inc which was backed by 67.3 percent of shareholders. Tables 1 and 2 show support for management and shareholder declassification proposals over the past few years. As you can see, average support for shareholder proposals has been varied—which could simply be a result of small sample sizes—but has never dipped below 60 percent. For management resolutions, average support was almost invariably above 98 percent.

This is consistent with many major investors’ voting policies. For example, BlackRock’s US guidelines state: “We believe that directors should be re-elected annually and that classification of the board dilutes shareholders’ right to promptly evaluate a board’s performance and limits shareholder selection of directors.”

Proxy adviser Glass Lewis agrees. Its US guidelines argue that “staggered boards are less accountable to shareholders than boards that are elected annually” and that studies have associated them with lower company valuations.

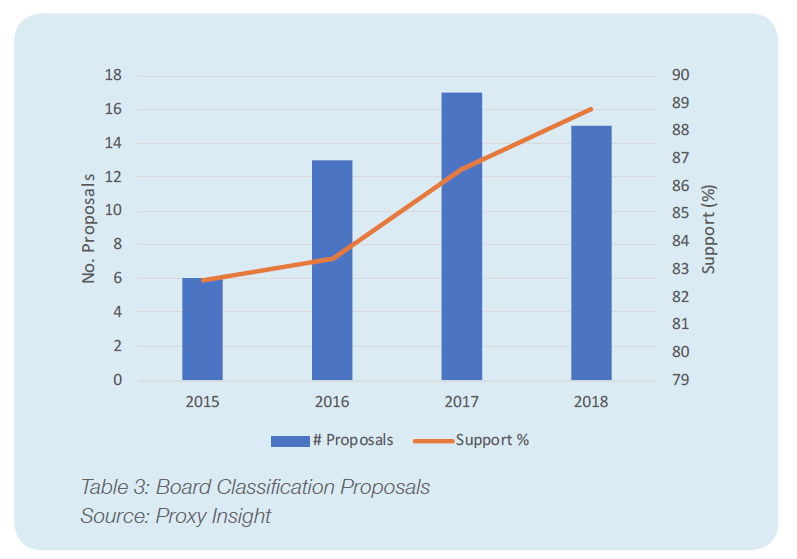

Given the enthusiastic support investors have for the declassification of boards, you might expect that proposals to classify them would prove somewhat controversial. However, the truth is that these resolutions also enjoy comfortable backing. Last year, we picked up 15 of these proposals and the average support level was 88.8 percent.

Explaining the Paradox

While support for classifying boards is certainly lower than support for declassifying them, and on the low side for something that is invariably a management proposal, 88.8 percent is still pretty decisive. What’s more, support has been trending upwards over the past few years, despite classified boards falling out of favor. As you can see from Table 3, these proposals received 82.6 percent of votes on average in 2015 but the figure has been ticking up every year since.

At first glance, a possible explanation might be the fact that management proposals almost always receive far higher levels of support than

shareholder proposals. All proposals to classify boards and most proposals to declassify them come from management, so both enjoy this advantage. While this likely goes some way towards accounting for the apparent paradox, it certainly does not explain everything.

For one thing, by that same token shareholder proposals are at a disadvantage, yet have a very hard time failing. The level of success they enjoy is exceptionally high for a shareholder proposal. While the success of classification proposals is unspectacular for a management resolution, it remains high. It seems investors are far more willing to buck the trend in order to support declassification than to oppose classification. This still leaves us with the odd situation where investors are highly supportive of two opposite moves.

This explanation also fails to explain the fact that support for board classification is increasing. At a time when these structures are increasingly being seen as an example of poor governance, one would expect the opposite even if support ultimately remained high.

Proposals to classify boards are relatively rare. While the sample sizes are not small enough to easily dismiss the strange trends as a quirk of chance, perhaps this lack of volume can help explain the paradox. It is possible that, knowing classified boards are unpopular, managements are reluctant to propose such a potentially troublesome item unless they are confident of success. This would mean the high level of support simply shows that their confidence is generally not misplaced.

Conclusion

Whatever their reasons, it seems that investors are very much inclined to support switching between classified and declassified board structures, whichever direction the company is heading in. They are, however, near-universal in their support for declassification when proposed by management, while classification generally only wins over around 90 percent of voters. Even so, the fact that support for classifying boards has been slowly but steadily rising for several years seems difficult to account for, and is the polar opposite of what most would expect.