Print

PrintSteve W. Klemash is America’s Leader, Jamie C. Smith is Associate Director, and Kellie C. Huennekens is Associate Director, all at EY Center for Board Matters. This post is based on their EY memorandum.

The EY Center for Board Matters took a close look at independent directors newly elected in 2018 by investors to Fortune 100 boards, and we are pleased to present the findings of our analysis of this “new class of 2018.”

The report analyzes what these directors bring to the boardroom and how companies are showcasing those strengths, based on a review of corporate disclosures highlighting the skills, expertise and backgrounds associated with these new nominees. In the third year of this series, we also reviewed the same 83 companies’ entering class of directors in prior years to enable consistent year-on-year comparisons. What follows is our perspective on the changes and trends we identified.

Our perspective: gradual change is underway

Given the limited number of board seats in the Fortune 100, and that newly added independent directors represent only around 10% of all independent Fortune 100 directors serving each year, boards appear to be making the most of these valuable board refreshment opportunities. We observe a continuing shift of attention from the more traditional director candidates (current and former CEOs) to individuals with a wider range of skills, expertise, backgrounds and personal characteristics—diversity across multiple dimensions. Nearly one-quarter of new directors were recognized for their experience in innovation, transformation and in navigating change, and 10% were highlighted for their ability to bring an investor perspective to the boardroom, including through experiences in asset management or active investment funds. Still, the limited opportunities for adding new directors mean that change continues to be gradual.

Given the limited number of board seats in the Fortune 100, and that newly added independent directors represent only around 10% of all independent Fortune 100 directors serving each year, boards appear to be making the most of these valuable board \refreshment opportunities. We observe a continuing shift of attention from the more traditional director candidates (current and former CEOs) to individuals with a wider range of skills, expertise, backgrounds and personal

Corporate statements that recognize the importance of board diversity appear increasingly common, but we continue to observe an opportunity for greater consistency and comparability in disclosures around board diversity, particularly across gender, race and ethnicity. We find, too, that companies are continuing to expand and refine disclosures to clarify how the disclosed director qualifications align with the company’s strategy. The quality and extent of disclosure varies, and we estimate that 14% of the directors’ qualifications language and reasons for nominations were clearly linked to company strategy, suggesting that this is an emerging disclosure trend. In one of the stronger examples, we saw a company highlight its nominee’s areas of expertise, explain how these experiences contribute to the company’s future strategy and link these elements to a brief description of broader industry transformations underway.

Boards are thinking differently about what makes an effective board candidate, and the supply of possible candidates is expanding significantly. This larger pool means boards can be even more selective about their short lists. At the same time, the responsibilities of being a public company director are continuing to increase and become more complex, and boards are setting the expectation that directors must be fully committed to being engaged and active. There is greater concern over the possibility of being “over-boarded” and “over-committed.”

Observations on skills and demographics

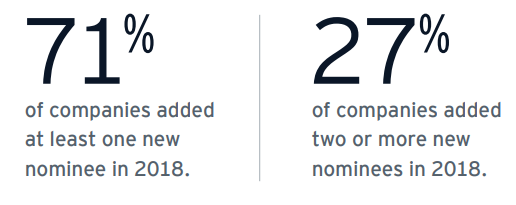

In 2018, 71% of the reviewed companies added at least one new nominee and 27% added two or more. This represents an increase from prior years when the levels were generally steady at around 56% and 21%, respectively. For companies that added at least one new nominee in 2018, our review yielded the following observations.

Top 10 areas of expertise for the new class

For a look at the skills being added to boards, we found that the areas of expertise most frequently cited in new nominations were: international business; corporate finance, accounting; and industry expertise. Around half of the new class was recognized for expertise in at least one of these categories. The next most common areas—technology; operations, manufacturing; and board service, corporate governance—were cited in 40% to 45% of new nominations. On average, 35% was recognized for experience in government, public policy, regulatory; risk oversight; strategy; or marketing, business development.

New class enhances career and gender diversity

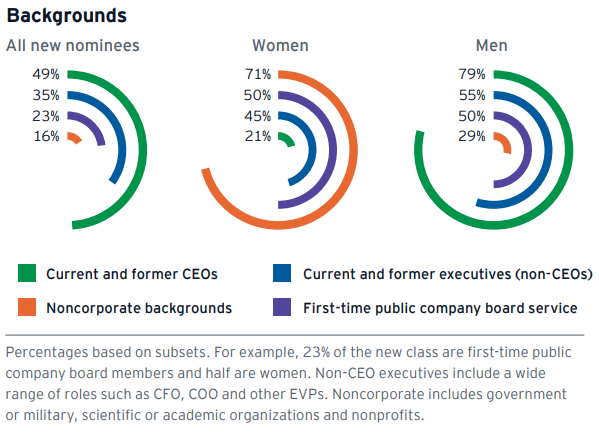

Women continued to represent around 40% of new nominees, contributing to a slight increase in overall board gender diversity; in 2018, 27% of existing independent directors were women, up from 25% in 2016. Slightly less than half of the new class fits the traditional model of independent directors in years past (current and former CEOs) and that group remained predominantly male. The slate of non-CEO new nominees represented a different picture: this group reflected relative gender balance. Further, of those directors with noncorporate backgrounds, most were women.

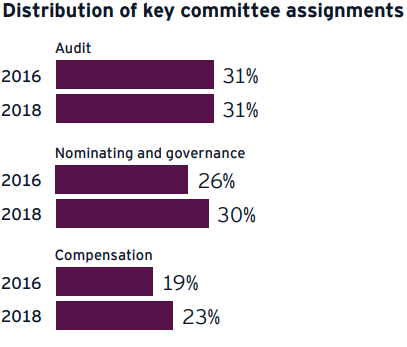

Audit and nominating and governance committee assignments most common

The most common committee assignments continue to be either the audit or nominating and governance committees. However, the 2018 entering class shows a more even distribution of committee assignments with growth apparent in the number of new appointments to nominating and governance committees, and in the number of new directors landing on compensation committees. A look at the portion of new nominees being designated audit committee financial experts found that while these “AC FEs” comprised 23% of the 2016 class, the level was lower in 2018 at 20%.

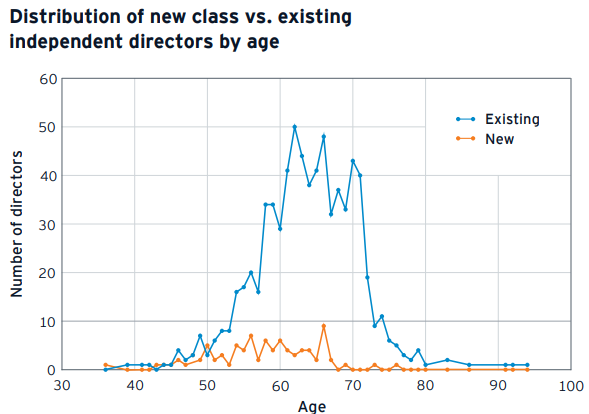

New class of directors getting younger

The average age of the new class of directors has been getting younger each year. While the changes have been gradual and the numerical differences very slight, a look at the new nominees by age group shows a clear trend. The portion of new nominees under the age of 60 grew from 51% in 2016 to 58% in 2018, while the portion of those under 50 grew from 8% to 14%. Although boards are adding more younger directors, the overall age of the boards remains high due to the portion of existing directors compared to the new class.

Questions for the board to consider

- Is the board proactively aligning director qualifications to the company’s strategy and risk oversight priorities, including for the company’s future state?

- Is the board considering board diversity across multiple dimensions, including skills and expertise, career background and personal characteristics (age, gender, race/ethnicity, geography, etc.)? In other words, does the board “refresh” or essentially “replace” perspectives? Does the board go beyond seeing diversity as a “check-the-box” concept?

- How effectively is the company communicating that its directors represent the best mix of individuals to guide the company? Would a third party read director qualifications disclosures in the way that the company intends?