Print

PrintEd Batts is partner, Isabella Fu is a summer associate, and Sara Gates is an associate at Orrick, Herrington & Sutcliffe LLP. This post is based on their Orrick memorandum. Related research from the Program on Corporate Governance includes Socially Responsible Firms by Alan Ferrell, Hao Liang, and Luc Renneboog (discussed on the Forum here).

On August 6, a group of three individual plaintiffs represented by Judicial Watch, Inc. filed suit in Los Angeles County Superior Court against California’s Secretary of State seeking to block the provisions of SB 826, which was signed into law in September 2018 and provides that:

- By December 31, 2019, every publicly traded company on a major securities exchange (e.g. Nasdaq, NYSE) with its headquarters in California is required to have at least 1 female board director; and

- By December 31, 2021, a public company board with 5 board members will need at least 2 female members, and those boards with 6 or more members will need at least 3 female members.

As the Judicial Watch lawsuit notes, at the time of the law’s enactment in September 2018, many commentators questioned its constitutionality and enforceability, irrespective of its public policy goal.

Due to the “private ordering” initiatives described below from large index and pension fund investors and proxy advisory firms, the potential incremental impact of the law itself, however, may be more limited than first appears. Almost all of these other constituencies are advocating for boards to have at least 1 female member, and many are advocating for 2 (or more).

Thus, the law itself really is limited in additionally having

- a formal requirement for 3 (instead 2) female members be required on boards with 6 or more members, and

- specified required adoption deadlines and an associated enforcement system of state-imposed fines, rather than relying alone on the “private ordering” threat of annual election voting.

Each of the “Big 3” rules-based index investing fund families—BlackRock, Vanguard and State Street—are vocal. BlackRock expects at least two board members to be female and already is voting against the re-election of nominating committee members on companies where it sees shortfalls in board diversity. Vanguard has joined the “30% Club” (https://30percentclub.org). State Street formally has announced that beginning in 2020, it will vote against the entire nominating committee of any company without at least one female director—thus mirroring the first step in California’s requirement.

And proxy advisors, whose policies remain controlling in the voting decisions of many institutional investors, are likewise adopting similar stances. ISS issued a new 2019 policy, which is effective in 2020, to vote against re-electing the nominating committee chairperson where no female is on the board. Glass Lewis issued an identical policy in 2017, which took effect already in 2019 and extends further in that Glass Lewis reserves the right to vote against the re-election of more than just the nominating committee chair. These efforts stand on their own and U.S. public company boards should be cognizant that irrespective of California’s law, Judicial Watch’s challenge thereto or their company’s location, there are independent reasons to pay heed in earnest to increasing board gender diversity.

Against this background, we thought it would be useful to benchmark the data on where California public companies stand today on board gender diversity.

Sample Size to Benchmark Board Gender Diversity

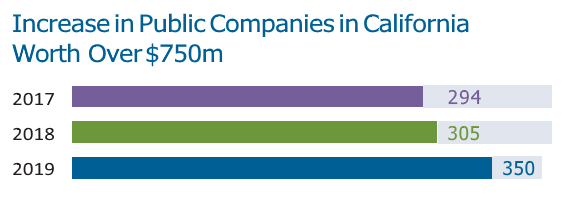

For meaningful trends in board gender diversity, of the approximately 750 public companies in California, we looked in 2019 at 350 companies, with two criteria: headquarters in California, and (2) over $750 million market capitalization, as follows:

| 122 companies between $750 million – $2 billion | 93 companies between $2 billion – $5 billion | 135 companies with over $5 billion |

These 350 companies—representing just under half of the public companies in California—are the most material from an economic standpoint. Interesting to note, despite the contraction in the number of public companies in the United States—from approximately 8,100 in 1996 to 4,300 today—the population of public companies headquartered in California with above $750 million in market capitalization has grown in the past three years: from 294 in 2017 to 305 in 2018 to 350 in 2019. No doubt this is both because equity market values have continued appreciating in a bull market, and, relatedly, the IPO “window” has reopened and numerous companies have gone public.

Trends in Board Gender Diversity

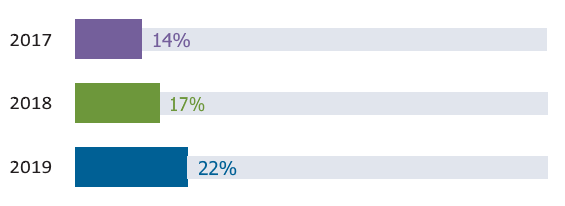

The median percentage of female directors at the sample companies has increased.

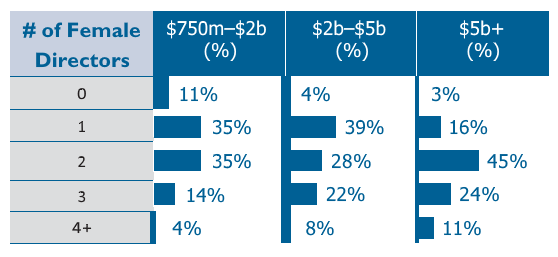

Moreover, there is a striking continued difference in gender balance between smaller cap and large cap companies.

Correlation of Number of Female Directors to Market Capitalization

- Smaller companies are more likely to have 0-2 female board members.

- Mid-size companies are more likely to have 1-3 female board members.

- Large cap companies have a definite bulge—45 percent of such companies have 2 female board directors and 35 percent of such companies have 3 or more female board directors.

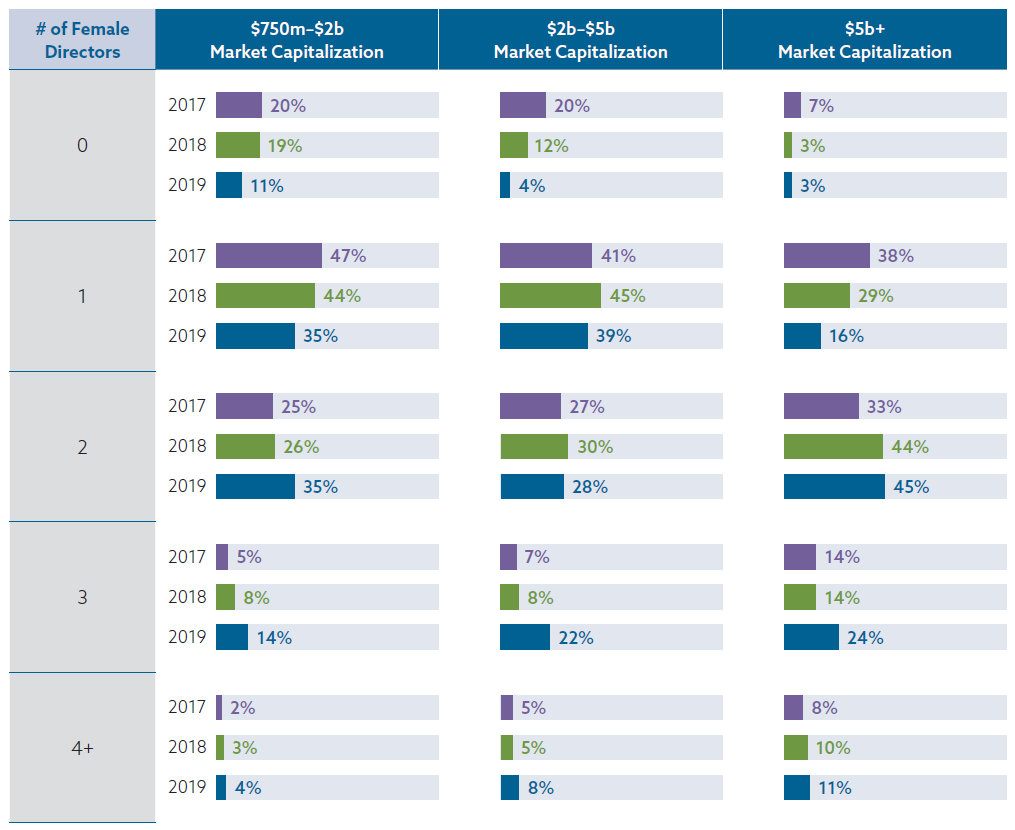

Over 10% of Companies Worth From $750m-$2b Still Do Not Have a Single Female Director

- The slope of companies with no female director clearly is correlated and goes down as market cap increases.

- 1 out of every 10 companies with market capitalization between $750m-$2b do not have any gender diversity in their boardrooms. However, that number still represents progress, as it is a roughly 50 percent drop from 2017—when 1 in 5 companies in that value band did not have a single female board director.

Acceleration of Female Directors in Large Cap Companies

- Whereas 1 in 3 companies over $5 billion in value had 2 female directors in 2017, in 2019 that number is just shy of 1 in 2.

- The percentage of large cap companies with 3 female directors increased from 14 percent in 2017 to 24 percent in 2019—and the percentage of such companies with more than 3 female directors ticked up slightly from 8 percent to 11 percent.

Mid-Size Companies Also Continue Acceleration of Adding Female Directors

- 7 percent had 3 female board members in 2017 and 22 percent have 3 female board members in 2019.

- The percentage of such companies with 0 female board members has precipitously dropped—from 1 in 5 companies in 2017 to under 5 percent in 2019.

In conclusion, there continues to be an unmistakable migration toward higher percentage of female board members among California’s most significant public companies. We clearly would expect this trend to continue as the deadlines at the end of this year and then in 2021 for mandated board gender diversity continue to grow closer.

Raw Data on California Board Gender Diversity