Print

PrintKiran Vasantham is Director of Investor Engagement and David Shammai is Corporate Governance Director—Cross Border at Morrow Sodali. This post is based on their Morrow Sodali memorandum. Related research from the Program on Corporate Governance includes The Agency Problems of Institutional Investors by Lucian Bebchuk, Alma Cohen, and Scott Hirst (discussed on the Forum here).

This is the fifth consecutive year that we have conducted a global institutional investor survey and reported the findings and our observations. In this publication we focus on the ESG risks and opportunities that investors factor into their investment decisions with our report exploring these themes in greater detail.

As anticipated, it was clear that 2019 marked a turning point in incorporating ESG factors into mainstream investing as investors recognize the growing risks of non-financial factors. This correlates with the top risks facing the world in 2020 as reported by the World Economic Forum which found that for the first time, environmental issues are the dominant concern. The rate of ESG-oriented investing has risen significantly, and we continue to see mainstream institutional investors, both active and passive, shifting capital in this direction. Whilst maintaining the overall structure of the survey, we decided to explore these themes in more-depth.

The survey findings were resounding. Respondents unanimously agreed that ESG risks and opportunities played a greater role for them in 2020 when investing and engaging with companies. Unsurprisingly climate change was at the top of the ESG agenda. Whilst understanding the physical and transitional climate-related impacts were formerly limited to high-emitting sectors such as energy and industrials, this is no longer the case. All companies, regardless of their sector, should expect to be questioned on how they are managing and responding to these risks and opportunities. Boards and companies should also be prepared to face investor scrutiny on how they approach and report on their exposure to ESG-related issues.

Some of the trends identified in our 2019 survey have continued into 2020. Once again, investors reinforced how important it is for them to understand the Board’s thinking and attitude across a range of topics, re-iterating the importance of board engagement. In a recent publication on this topic by Morrow Sodali, the firm’s Chairman John Wilcox identifies this overarching theme as ‘the supremacy of the board’. Boards are now expected to clearly demonstrate oversight on a broad range of issues, including financial and non-financial (ESG) risks. Consequently, investors are increasingly seeking direct access to boards, so they can gauge the ‘tone at the top’ to assess the credibility of formal messaging around culture for example, or corporate purpose and how it links with the company’s stated strategic objectives.

Morrow Sodali’s survey explores how ESG, as a very broad concept, can transpose itself to the pragmatic issues of shareholder meetings, voting ballots, and to other forms of stewardship measures. The survey covers areas from activism through to reporting and whether there is an appetite for a separate vote on sustainability. However, our overall impression is that whilst investors are certainly embracing their role as active stewards of capital, there remains plenty of work to be done for companies on how best to report and manage environmental and social issues. The key here is to chart a path where investors drive effective stewardship but enable companies to retain autonomy in managing the business. A case in point is the desire a majority of respondents (70%) expressed to have greater say over the company’s non-financial information. At this formative time for ESG reporting, most see this as a vote over the robustness of the figures rather than the appropriateness of the performance. Likewise, we are seeing more clarity on the direction of corporate reporting, with progress made in reporting against frameworks such as the Sustainability Accounting Standards Board (SASB) and the Task Force on Climate-related Financial Disclosures (TCFD) recommendations.

Finally, we hope readers find beneficial the specific survey questions on investor priorities. After climate, pay-forperformance continues to dominate, but increasingly, the emphasis is on identifying and addressing cases where companies and boards appear to be unresponsive to shareholder concerns. It is critically important for companies to understand their investors’ expectations around ESG, sustainability and the growing list of other non-financial factors. This publication is presented with these facts front of mind and we invite readers to engage with us by providing feedback, thoughts and opinions either online or in person.

Key Findings—Voting & Engagement

Q.1 All respondents state that ESG risks and opportunities played a greater role in their investment decisions during the last 12 months, with climate change being top of investors’ list (86%).

Q.3 Continuing the trend identified last year, 91% of respondents say engagement at board level is the most effective way for investors to influence board policies and engagement. Notably, almost half of investors would consider voting against a director to influence outcomes.

Q.7 Climate change (91%) and human capital management (64%) are cited as the top sustainability topics that investors will focus on when engaging with boards in 2020.

Q.8 Activism: investors are more likely to support activists’ case if the company portrays weak governance practices (64%) and less surprisingly, if it can be shown that there is a track record of misallocation of capital (50%). Notably, investors now prioritize presence of ESG risks (32%) before a credible activist business strategy when deciding whether to support ESG activists.

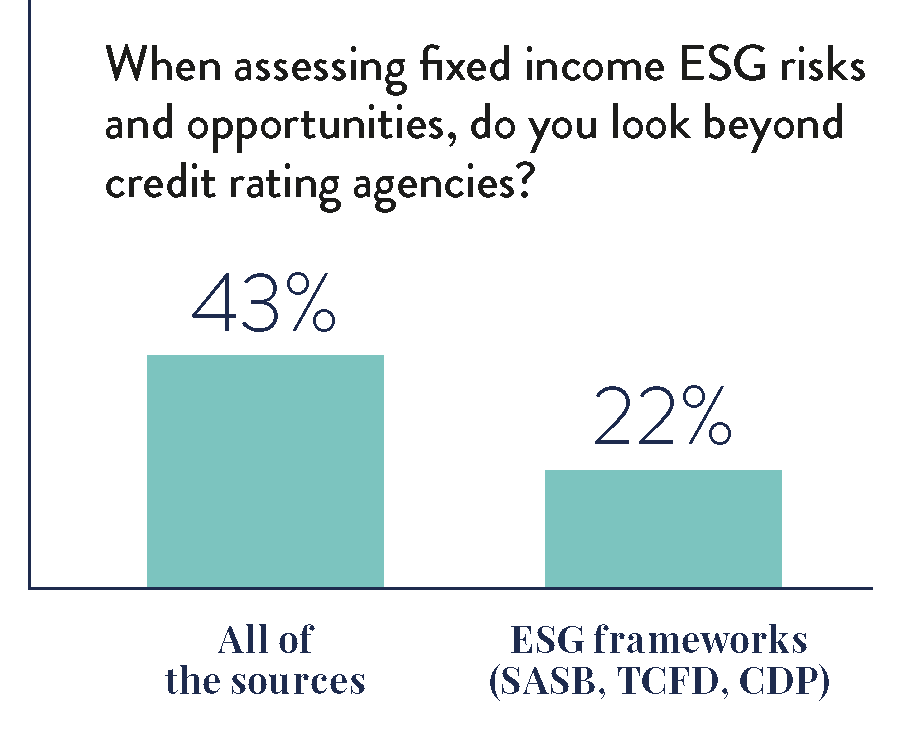

Q.13 ESG is playing a more concrete role in fixed income. ESG rating agencies established themselves as a key factor in analyzing risks and opportunities. Almost half of the respondents (43%) utilize all sources over the traditional credit rating agencies. A further 22% focus only on ESG frameworks or ESG rating agencies.

Q.14 ‘Say on sustainability’ is a concept that investors did not strongly agree or disagree on. 30% said there are sufficient routes for shareholders to express their views on non-financial matters whilst equally 30% supported ‘say on sustainability’.

Key Findings—Disclosure

Q.2 Overwhelmingly 91% of respondents expect companies to demonstrate a link between financial risks, opportunities and outcomes with climate-related disclosures. A total of 68% respondents believe that greater detail around the process to identify these risks and opportunities would significantly improve companies’ climaterelated disclosures.

Q.5 81% of investors indicate that poor disclosure of performance targets may lead to a vote against executive remuneration-related resolutions.

Q.10 Investors widely agree (81%) that stakeholder engagement approach and outcomes should be included in companies’ disclosure when they explain their corporate purpose.

Q.12 Last year, a total of 83% of respondents indicated that the key ESG topic that needed an improvement in disclosures was human capital. This year, the prime topics for disclosure improvements included board involvement in setting the culture (95%) and health and safety indicators (71%).

Q.15 When it comes to the company’s ESG performance and approach, investors recommend SASB (81%) and TCFD (77%) as best standards to communicate their ESG information.

Looking Forward

The results of this year’s survey confirm the global trends that are rapidly transforming the relationship between corporations and their institutional investors. Issues relating to ESG, sustainability, corporate purpose, culture and stakeholder interests have joined corporate governance at the center of the dialogue between investors and portfolio companies.

The momentum behind these issues is not yet fully realized internationally. As indicated by recent public statements from major asset managers, we can expect to see investors deepening the integration of ESG issues into their investment decision making, becoming more involved in collective engagement initiatives and generally dedicating more resources to assessing the ESG performance and sustainability of portfolio companies. These issues are now at the core of investors’ stewardship activities and central to their dialogue with management and boards of directors.

The findings of our survey make clear that investors expect to see improvement in corporate reporting generally, with a specific focus on climate change and other issues related to long-term performance and sustainability. We know that companies are struggling with a disharmonized array of reporting standards.

At the same time, we are seeing several initiatives to coalesce the key frameworks for disclosure and communication, or at least to achieve a shared understanding of the relationships among them. Examples of this global effort include the Corporate Reporting Dialogue, the “Compact for Responsive and Responsible Leadership” recently unveiled by the IBC at the World Economic Forum.

Tension between the tailored use of the data by both companies and investors and the need to establish common standards and metrics to facilitate global comparability will no doubt persist. Whilst it is possible to observe investor preferences on several of these points, and our survey certainly attempts to do so, a radical simplification in standard-setting and reporting requirements is unlikely to emerge in the short term. Until then, companies must engage individually with their shareholders.

We strongly believe that companies must proactively manage this important two-way communication with their investors, listening carefully, engaging in a substantive dialogue about business performance and strategy and shaping their response to meet investor expectations.

With the exponentially growing pools of new sustainable funds as well as mainstream funds integrating ESG, successful engagement programs will assist companies not only in improving their relationship with institutional investors, but furthermore make it easier for them to achieve lower cost capital over the long term.

Survey Results

1. Have ESG Risks and Opportunities Played a Greater Role in Your Investment Decisions During the Last 12 Months?

Setting the Scene

This unequivocal result confirms the growing importance to investors of ESG factors, whether risks or opportunities, in their investment decisions. The fact that 100% of the respondents answered ‘yes’ undeniably reinforces that ESG integration has become an integral part of mainstream investment decision making.

Results

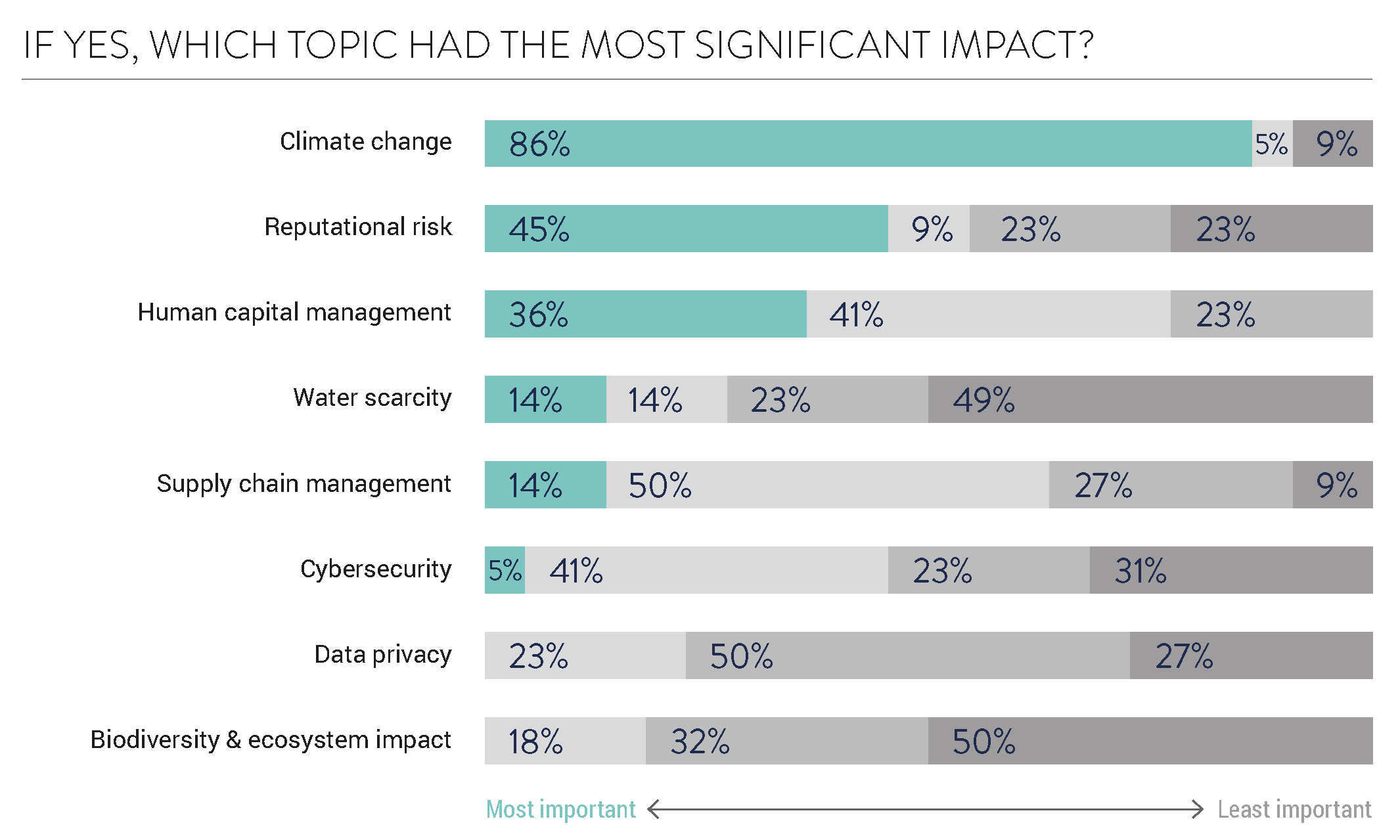

Unsurprisingly, climate change was overwhelmingly named as having the most significant impact on investment decisions by 86% of respondents. This correlates with the acceleration of investor action on a global basis that is focused on delivering climate solutions and mitigating the financial impacts presented by climate change.

After climate change, main topics were the reputational risk named by almost one in two respondents (45%), followed by human capital management which was stated by more than one in three (36%) investors. Other main ESG topics noted as having a significant impact on investment decisions, albeit on a smaller scale, were water scarcity and supply chain management that each rated 14% and cybersecurity that rated 5%. The fact that reputational risk is amongst the top 3 issues identified by respondents indicates the significant impact that a company’s management of ESG issues is having on investment decision making.

Further, we note that human capital management has been highlighted as one of the key engagement topics by the world’s largest three index funds over the last two years.

Key Takeaways

• Climate change had the highest ESG impact on investment decisions (86%)

• Reputational risk was the next most important ESG risk impact (45%)

2. How Could Companies Improve Their Climate-Related Disclosures?

Setting the Scene

Morrow Sodali’s 2019 Institutional Investor Survey highlighted the importance of a company’s disclosure and dialogue around sustainability and climate change strategy for investment decision making. The results from our 2020 survey continue to emphasize that the majority of investors view climate change as the most important sustainability topic. Historically companies have reported their environmental footprint (including energy, emissions, waste and water data) to report their impact on climate change. With the introduction of the TCFD recommendations in 2017, companies are now expected to refine their climate-related disclosures by considering governance, risk management, strategy, and metrics and targets, and linking these to financial impacts and performance.

Results

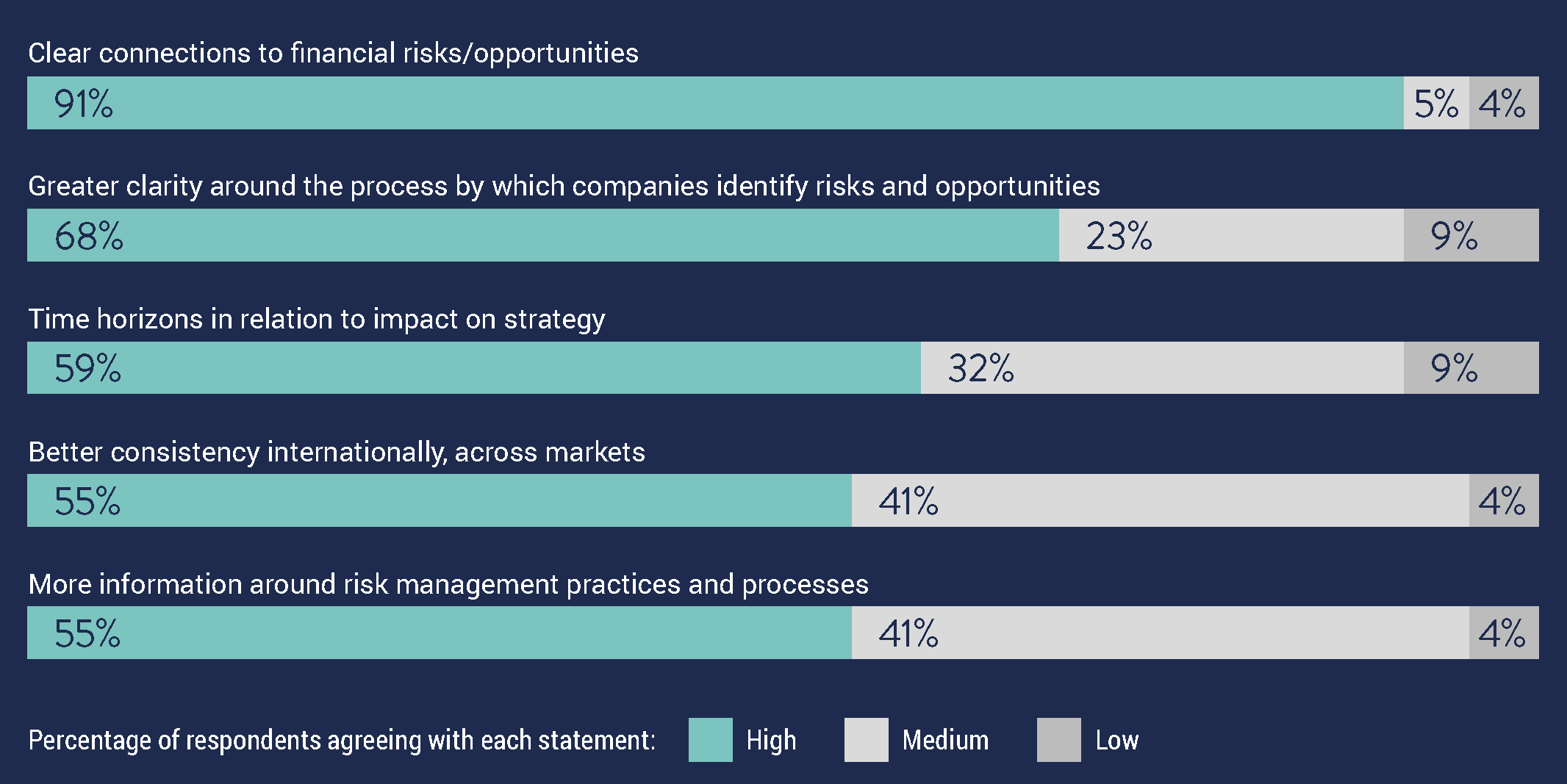

In terms of potential improvements to current climate-related disclosures, an overwhelming majority of respondents (91%) suggested clear connections between the climate-related data and financial risks and opportunities. Although climate change will have an impact for every business, different companies will be affected by climate change in different ways. As a result, they will need to tailor their disclosures to their own circumstances mainly with regard to increases in cost and potential negative influence on revenue. A total of 68% respondents believe that greater detail around the process to identify these risks and opportunities would significantly improve companies’ climate-related disclosures.

Climate-related risks are foreseeable and to a large extent are manageable. Details about the process to manage the risks and opportunities related to climate will assist investors in making informed decisions about capital allocation and enable them to better price risks and opportunities over both the short and longer term.

Key Takeaways

- Clear connections to financial risks/opportunities (91%)

- Greater clarity around the process by which companies identify risks and opportunities (68%)

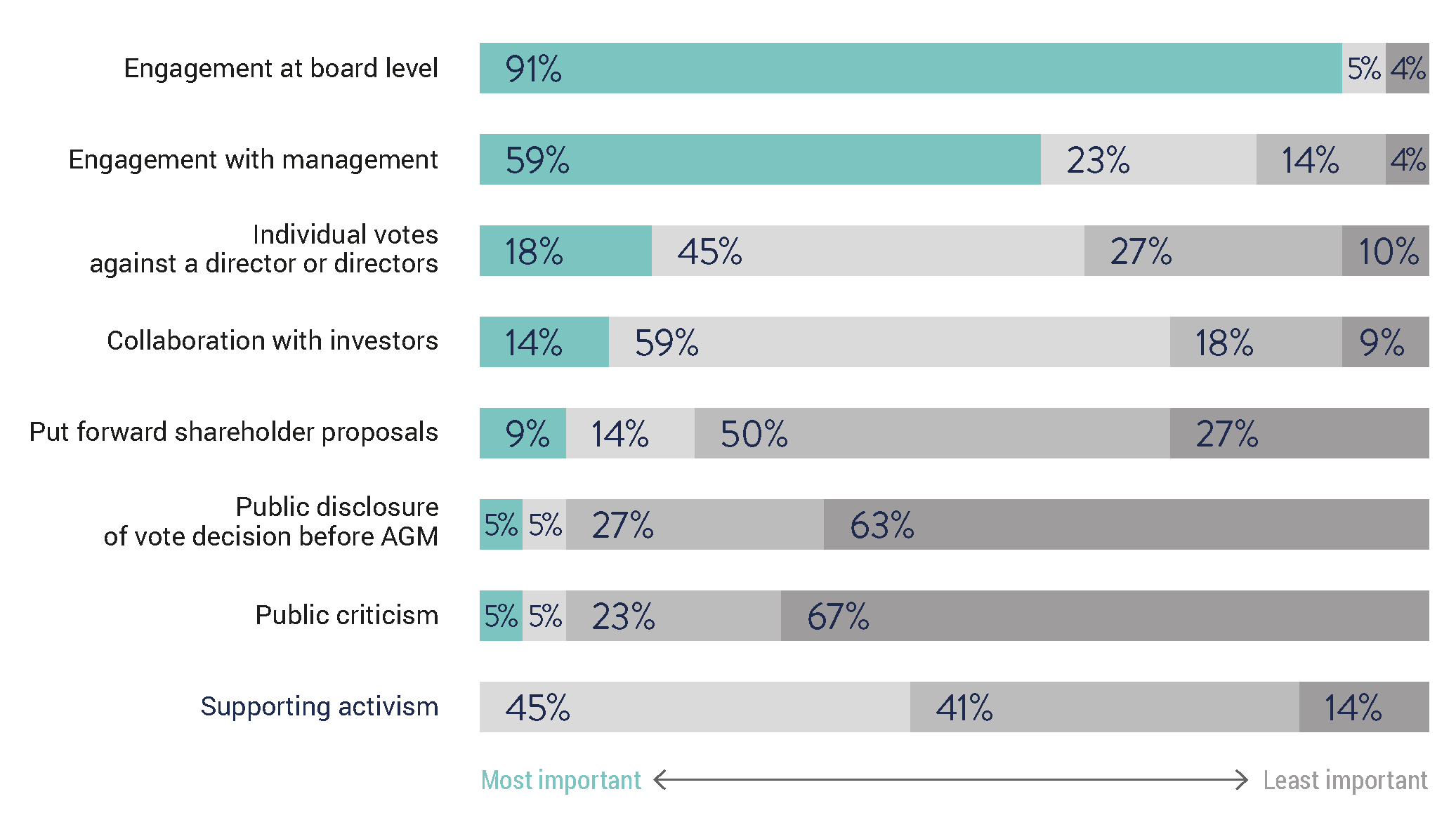

3. What Do You Think is the Most Effective Way for Investors to Influence Board Policies and Decisions?

Setting the Scene

We have witnessed a continued focus on board accountability with large investors signalling their preparedness to ‘put their mouth where there money is’ where a boards policies and decisions are not aligned with investor or market expectations. Investor interest in ESG has grown exponentially and both passive and active funds are forensically scrutinizing how companies are disclosing and managing various ESG risks and opportunities. Investors want to ensure boards clearly understand how they are prioritizing the materiality of sustainability-related issues and the impact this is having on capital allocation.

Results

There is no question about the importance investors attach to direct engagement between companies and their shareholders. In response to this question, an overwhelming 91% of respondents selected ‘engagement at the board level’ as the most effective way to influence board policies and decisions.

This is reflective of boards being held increasingly accountable for the performance of their companies and whether they can demonstrate achievement of sustainable wealth creation. Reinforcing the thematic of board accountability, almost one in five respondents, 18% believe the most effective way to influence board decisions is by voting against individual directors.

A majority of respondents, 59% selected ‘engagement with management’ as their first choice to influence the board. Further, investors expect to be more collaborative with each other with 14% stating it as the most effective way to influence board policies and decisions. With some collective engagement initiatives gaining public traction, for example Climate Action 100+, the lesson for issuers is to engage actively and be prepared to face collective action or votes against directors.

Although shareholder activism has substantially increased, none of the polled respondents selected it as their first preference when it comes to influencing the board. Investors continue to seek better access and constructive engagement with the board and tend to use shareholder activism as an opportunity for a robust dialogue. However, the results also show that investors are prepared to consider shareholder activism where board and management engagement fails to deliver adequate responsiveness.

Key Takeaways

- Engagement at board level (91%)

- Engagement with management (59%)

- Individual votes against a director or directors is ‘somewhat important’ (45%)

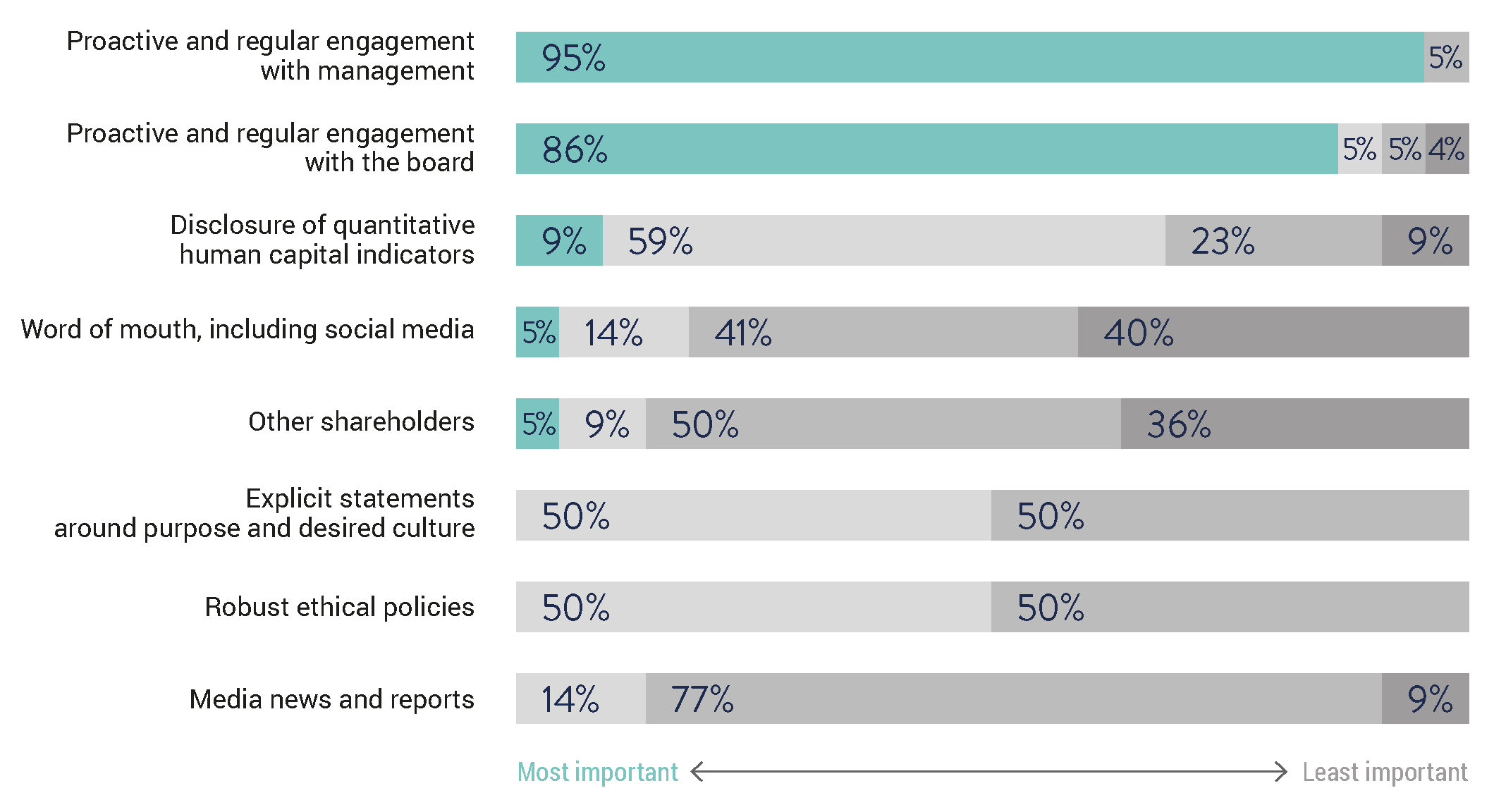

4. Which of the Following Sources of Information Helps You Best Evaluate Corporate Purpose and Corporate Culture?

Setting the Scene

With the publication of the Business Roundtable’s statement and the Davos principles 2020 on the purpose of a corporation last year, the world’s top businesses and financial leaders most visibly acknowledge that companies must serve the interests of their wider stakeholders as well as their shareholders. This position has been adopted by major institutional investors who have urged companies to pay more attention to long-term success and recognize that ESG topics represent material risk and opportunities directly impacting financial performance. Connecting this with shareholder engagement, the logical consequence of this purpose-led mindset is increased investor focus on how boards and management define and articulate corporate purpose. And furthermore, how companies effectively use corporate purpose to promote a high-performing culture.

Results

To meet expectations around articulating corporate purpose and culture, explicit statements or disclosure of quantitative human capital indicators are not sufficient. Investors are overwhelmingly united in their responses that proactive and regular engagement with both management and the board, 95% and 86% respectively, informs their evaluation of a company’s corporate purpose and corporate culture. Investors are sending a very clear message that it is not what a company says on paper, but rather how its top representatives communicate their purpose and culture that sets the ‘tone at the top’ and filters through all levels of the organization.

We note that one in two respondents ranked explicit statements and robust ethical policies as the third or fourth sources of information that they consider when evaluating a company’s corporate purpose and culture; however they do not rely on these as primary sources of information. Boards and management should therefore expect a greater number of questions from investors about purpose and culture and should be well prepared to provide a coherent and well articulated response that is consistent between management and the board. A failure to effectively respond to these types of questions will be considered by investors as a potential ‘red flag’ that may influence voting and investment decisions.

Key Takeaways

- Proactive and regular engagement with the board (86%)

- Proactive and regular engagement with management (95%)

- It’s ‘somewhat important’ to have disclosure of quantitative human capital indicators (59%)

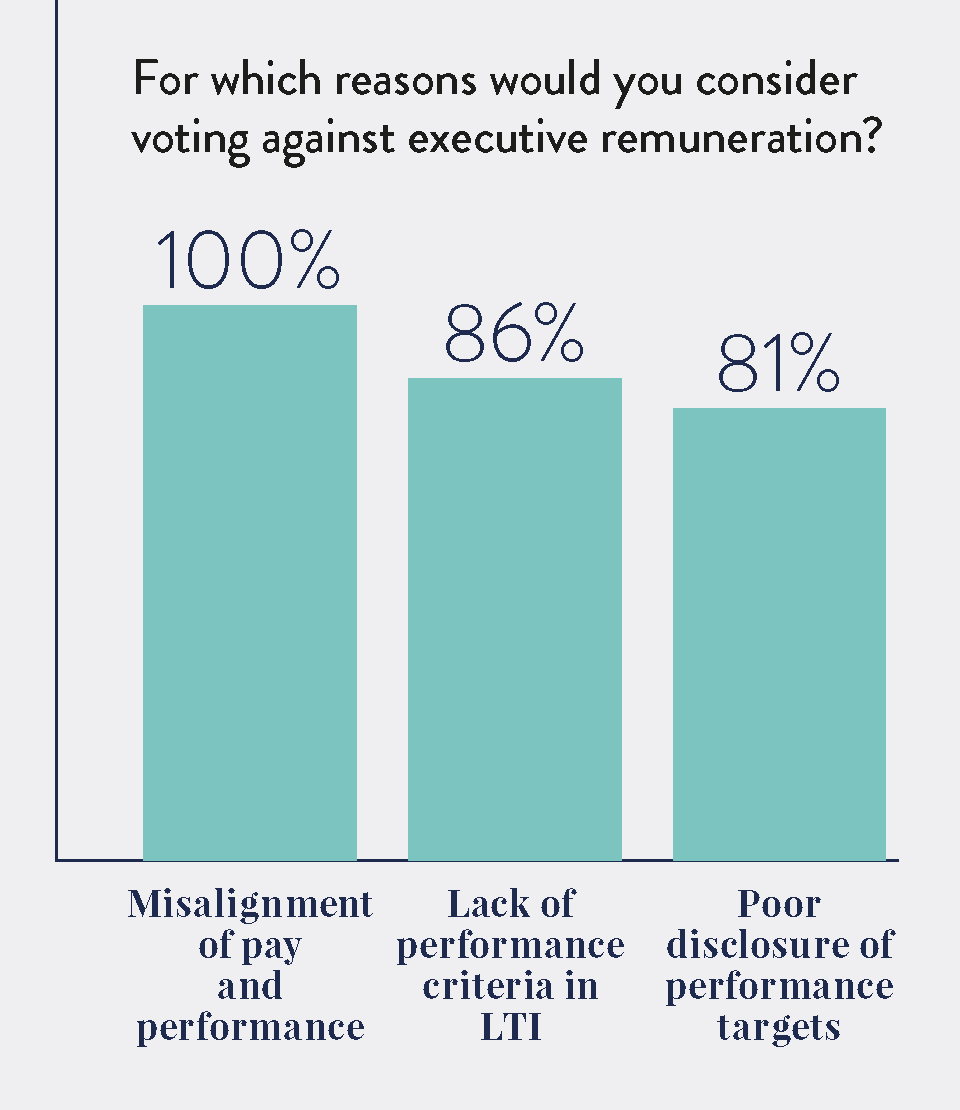

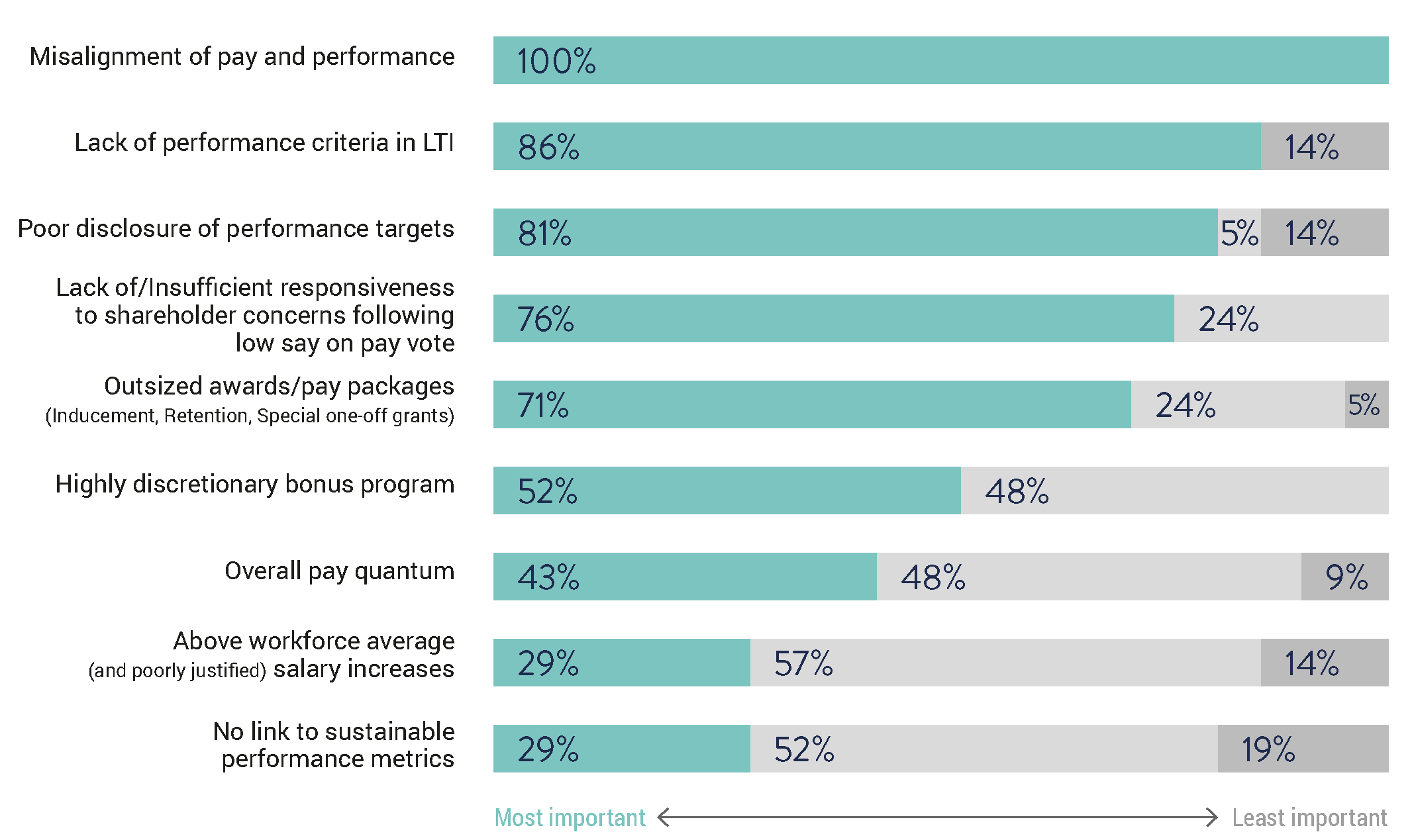

5. For Which Reasons Would You Consider Voting Against Executive Remuneration?

Setting the Scene

Investor concerns and attention on executive pay have not waned—spanning all markets. Pay remains a critical area for engagement between investors and portfolio companies as investors seek to better understand a company’s pay philosophy and how it creates a true pay-for-performance culture. This is being demonstrated through sound pay structures, practices and appropriate pay-related decisions that confirm the board’s understanding that remuneration outcomes are clearly aligned with the results achieved by individuals.

Recent investment association interventions have allowed investors to voice their concerns about a company’s executive remuneration report and/or policy by voting against the latter at the annual shareholder meeting. This has resulted in a greater emphasis on how companies at the very least respond or address these concerns.

Results

In our 2019 survey, 65% of investors said pay-for-performance remained the most important consideration when evaluating executive remuneration. This year, an overwhelming 100% of investors indicated that misalignment between pay and performance is the primary factor to consider voting against executive remuneration. For this reason, other factors that specifically tied to performance such as lack of criteria in the long-term incentive (LTI) (86%) and poor disclosure of targets (81%) were also rated as key reasons to vote against.

The findings also show how important a company’s responsiveness is to shareholder concerns about say on pay with 76% citing insufficient or lacking responsiveness as a reason to vote against executive remuneration. The onus therefore clearly sits with companies to be proactively engaging with their investors to ensure they are effectively addressing and responding to shareholder concerns and expectations about remuneration.

Outsized awards and discretionary bonus programs continue to draw the ire of shareholders with a majority (71% and 52% respectively) stating them as reasons to vote against remuneration. Other reasons include high salary increases and the absence of a link to sustainable performance metrics which equally rated at 29% of all responses.

Key Takeaways

- Misalignment of pay and performance (100%)

- Overall pay quantum (43%)

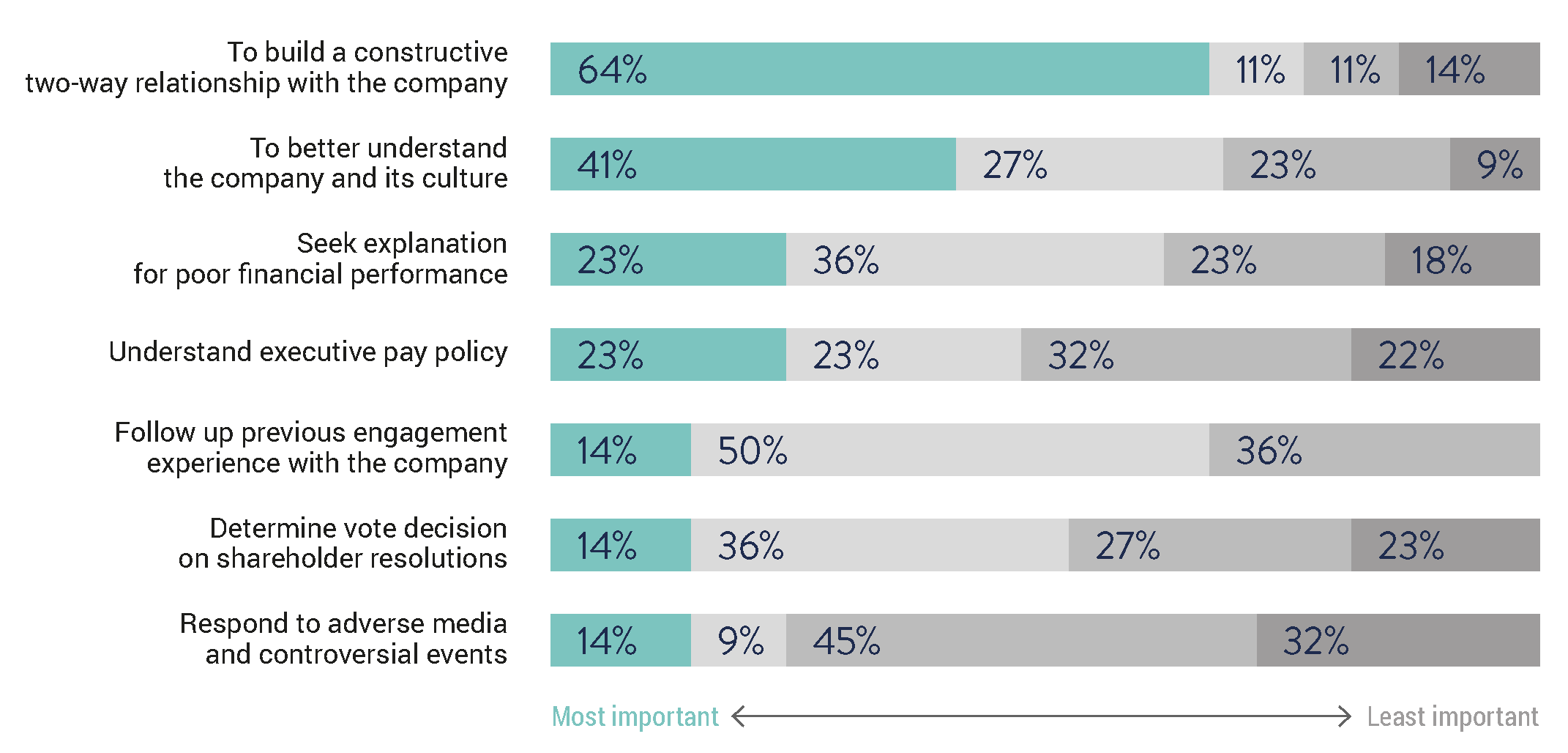

6. For What Purpose Do You Request Engagement with the Board?

Setting the Scene

Engagement continues to be an important avenue for investors to better understand the board’s thinking and risk management around non-financial factors that impact company strategy, performance and operational activities.

Until recently, investors in many markets did not necessarily expect board members to participate in engagement meetings and they were generally satisfied to speak to a company’s CEO, CFO, corporate secretaries and investor relations officers. In the last few years, this has changed dramatically as investor focus has shifted from engaging on financial performance to seeking engage across non-financial, ESG topics. In part, the shift has also been driven by the significant increase in company engagement from passive investors who are seeking direct access and dialogue with a board who they consider ultimately accountable.

Since 2016, we have continued to see a trend in our surveys where institutional investors are demanding greater transparency, including more contact and engagement with independent directors. Investors are seeking insights into the interactions between management and board members and understanding the key decision-making processes around setting and monitoring the business strategy and overall risk assessment including audit, remuneration, climate risk management and capital management decisions.

Results

A significant majority (64%) of respondents request engagement with the board for the purpose of building a constructive two-way relationship.

This is followed by 41% of respondents whose purpose when engaging with board members is to help them ‘to better understand the company and its culture’.

These responses are an encouraging sign that investors are seeking to work with the company in a positive way to achieve good outcomes rather than taking a combative approach. Other reasons why investors request engagement with the board is to seek explanations for poor financial performance (23%) and to understand executive pay policy (23%).

As financial performance and executive pay design are important matters for investors, boards should seek to proactively engage as appropriate if issues emerge to prevent adverse outcomes that may result from investor dissatisfaction. Especially when it comes to executive pay policy, investors believe that management is conflicted from independently discussing the rationale for pay design and they expect a dialogue with the board.

A minority of investors sought engagement with the board for the purpose of deciding how to vote on shareholder proposals (14%) and at times of adverse media or controversies.

Key Takeaways

- Build a constructive two-way relationship (64%)

- Better understand the company and its culture (41%)

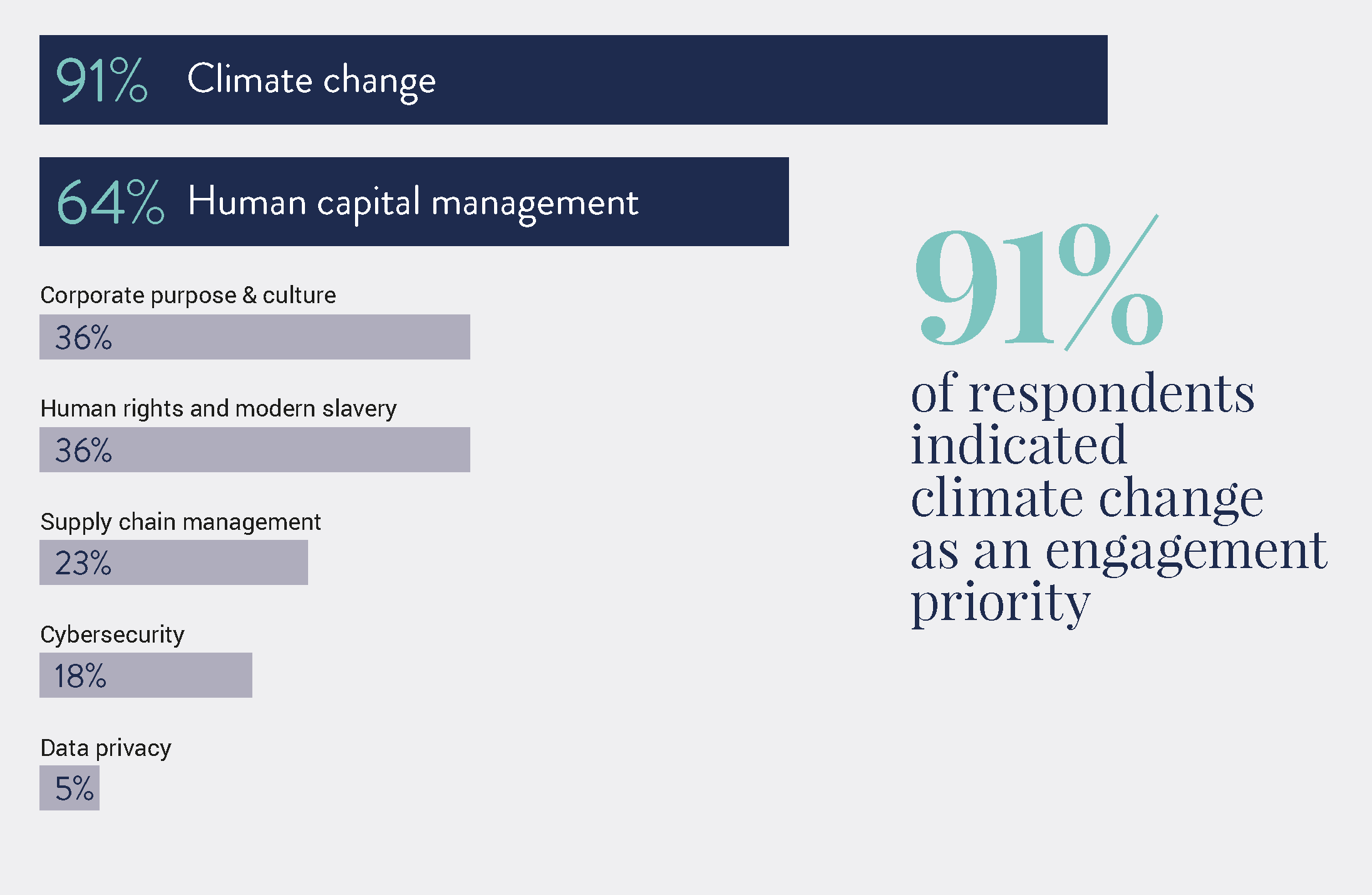

7. What Are the Top Three Sustainability Topics that You Will Focus on When Engaging with the Board in 2020?

Setting the Scene

Doubling down on the trends observed in recent years, investors continue to invest heavily in stewardship resources enabling them to influence corporate decisions relating to ESG and sustainability. Influential stakeholders including governments, NGOs and asset owners, and the endorsement of key initiatives such as Climate Action 100+ and TCFD have encouraged shareholders to intensify their engagement focus and even file shareholder resolutions specifically tackling ESG-related issues.

Results

In our 2019 survey, 85% of respondents indicated that climate change would be a key sustainability topic for board engagement followed by 54% who said they would engage on human capital management and corporate culture. In our 2020 survey, investors overwhelmingly continue to rank climate change (91%) as an engagement priority. Human capital management remains the second most important topic with 64% citing it as a focus (up from 54% in 2019).

Corporate purpose and culture remained a top three focus topic but declined to 36%, down from 54% last year. The reason for the decline is separating out corporate culture as a response and also adding human rights and modern slavery (36%) into our data set.

Overall, environmental (climate) and social (human capital management, corporate purpose and corporate culture, human rights) issues are the key sustainability topics that companies will engage with boards in 2020.

Engaging on the topics of cybersecurity (18% down from 39% in 2019) and data privacy (5% down from 11% in 2019) has declined since last year. Anecdotal feedback gathered from respondents indicates that the decline is a result of investors obtaining good information and establishing good lines of communication around these issues.

Key Takeaways

- Climate change (91%)

- Human capital management (64%)

- Corporate purpose & culture is the joint 3rd highest with (36%)

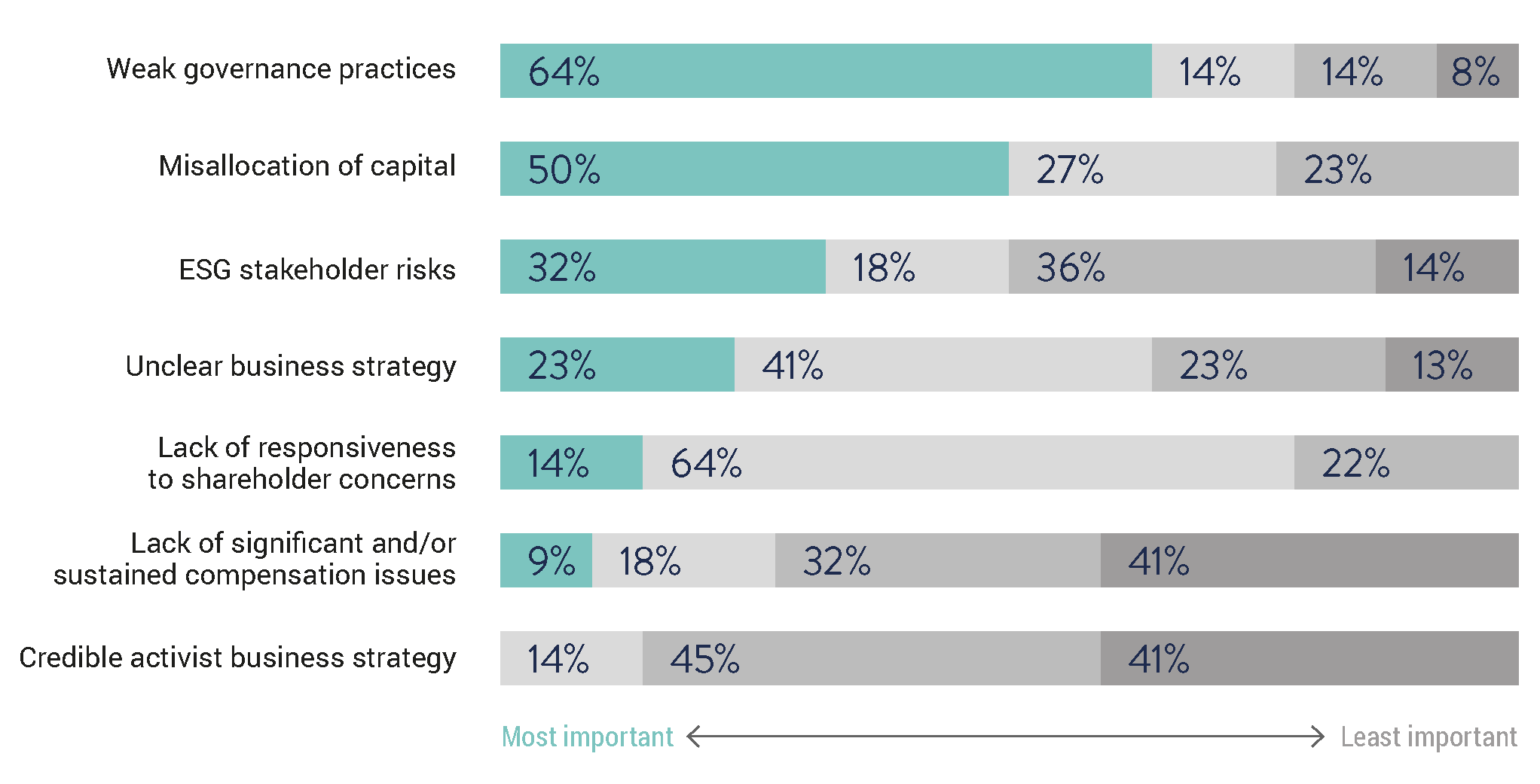

8. In Addition to Poor Financial Performance, What Factors Might Lead You to Support An Activist (Either a Corporate Activist or An ESG-Driven Civil Society Activist)?

Setting the Scene

While global shareholder activism saw a slight increase in the number of formal proxy contests in 2019, public companies experienced a sizable increase in various pressure points from shareholder activists over that same time.

According to FactSet research, the number of global proxy contests in 2019 was up to 258 from 251 the previous year. However, the total number of high-impact campaigns (e.g. seeking board representation/control, campaigns to remove directors, maximize shareholder value) reached 616, an increase of 31 campaigns from 2018. Shareholder activists were successful in roughly 46% of global proxy fights in 2019.

Understanding what is important to shareholders is critical in addressing concerns and securing their voting support. While poor financial performance is almost always the key component driving an activism event, institutional shareholders also consider other factors, such as governance and operational disruption, when voting.

Results

Our survey indicates that 64% of respondents would consider weak governance practices to be the most important factor in addition to poor financial performance when deciding to support an activist.

This was followed by 50% of respondents who cited misallocation of capital as the second most important criteria. In the current climate it is not surprising that 32% noted concern around ESG-related risks. Finally, rounding out non-financial factors to support an activist included an unclear business strategy (23%) and lack of responsiveness to shareholder concerns (14%).

These responses indicate that at the very least, boards should benchmark and monitor their governance practices to the market and peers so that they meet stakeholder expectations. This will help provide a buffer against an activist’s campaign and help minimize support for an activist.

Key Takeaways

- Weak governance practices (64%)

- Misallocation of capital (50%)

- ESG stakeholder risks (32%)

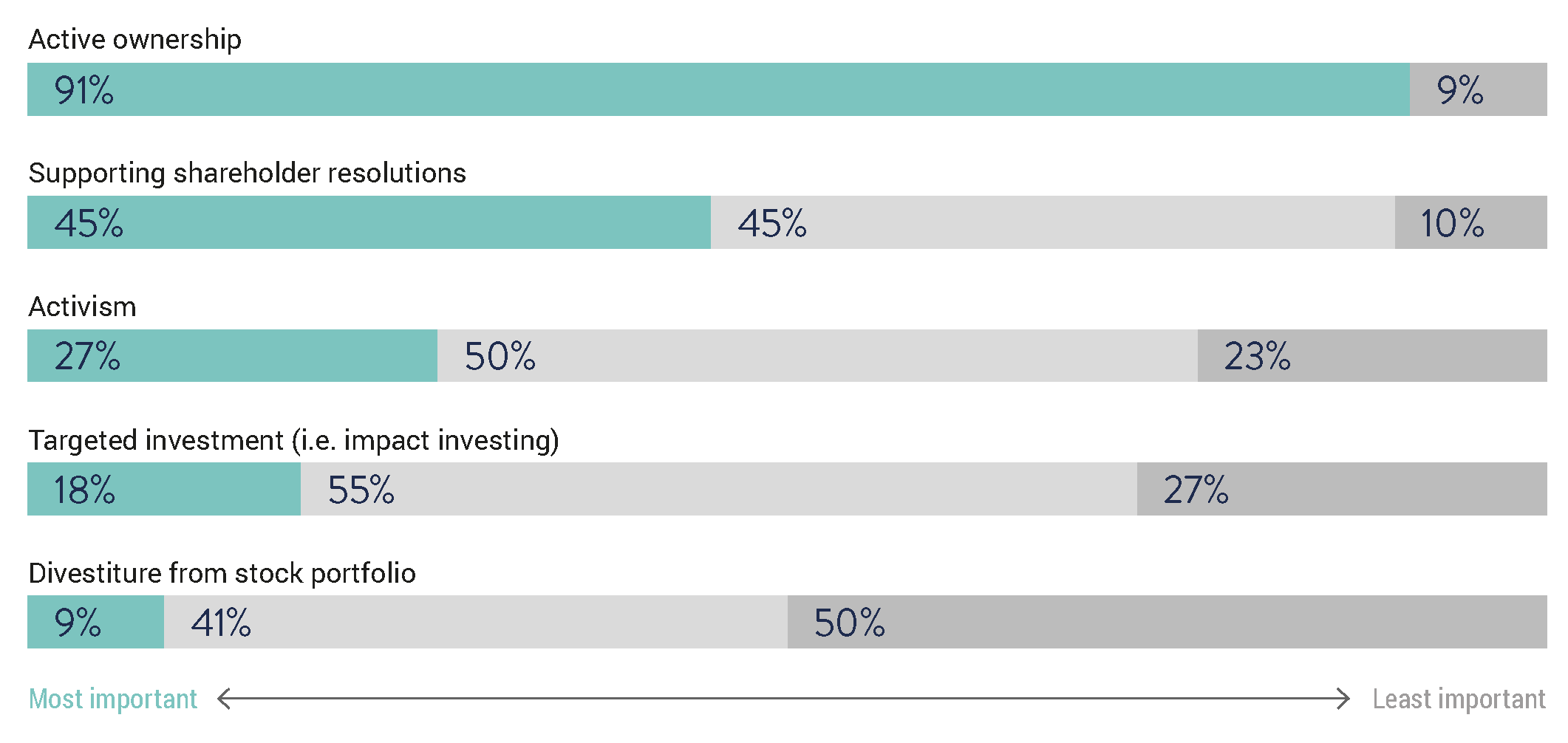

9. Which of the Following Shareholder Activities Are Most Effective for Influencing Companies to Adopt Positive Social or Environmental Policies?

Setting the Scene

The growing attention by investors in relation to material non-financial topics is a continued thread in this survey. In effect, investors may influence issuers to refine their policies, management approaches and disclosures to meet investor and stakeholder expectations on environmental and social issues.

Whilst market trends and peer group best practices may encourage companies to focus their efforts on adopting positive social or environmental policies, pressure from shareholders—through methods such as active ownership, shareholder resolutions, divestiture, activism, and targeted investments—can further encourage and lead to significant change in the adoption of more proactive environmental and social strategies.

Key Takeaways

- Active ownership (91%)

- Supporting shareholder resolutions (45%)

- Activism (27%)

- Targeted investment (18%)

Results

Respondents overwhelmingly believe that active ownership (91%) is the most effective way to help positively influence companies to adopt positive environmental and social policies. However support for shareholder proposals also rated highly (45%) as an effective method which indicates that many investors are prepared to force change.

Through active ownership, owners may focus on specific topics and engage with issuers to understand their approach to these topics. However, if engagements do not meet investor expectations, or, if there is a lack of engagement from either the company or the investor, then investors are not opposed to supporting shareholder proposals to encourage companies to take action.

As environmental and social topics increasingly become a focal area for engagement, issuers should be prepared to demonstrate a clear understanding of material risks and opportunities and provide meaningful disclosures that meet investor expectations.

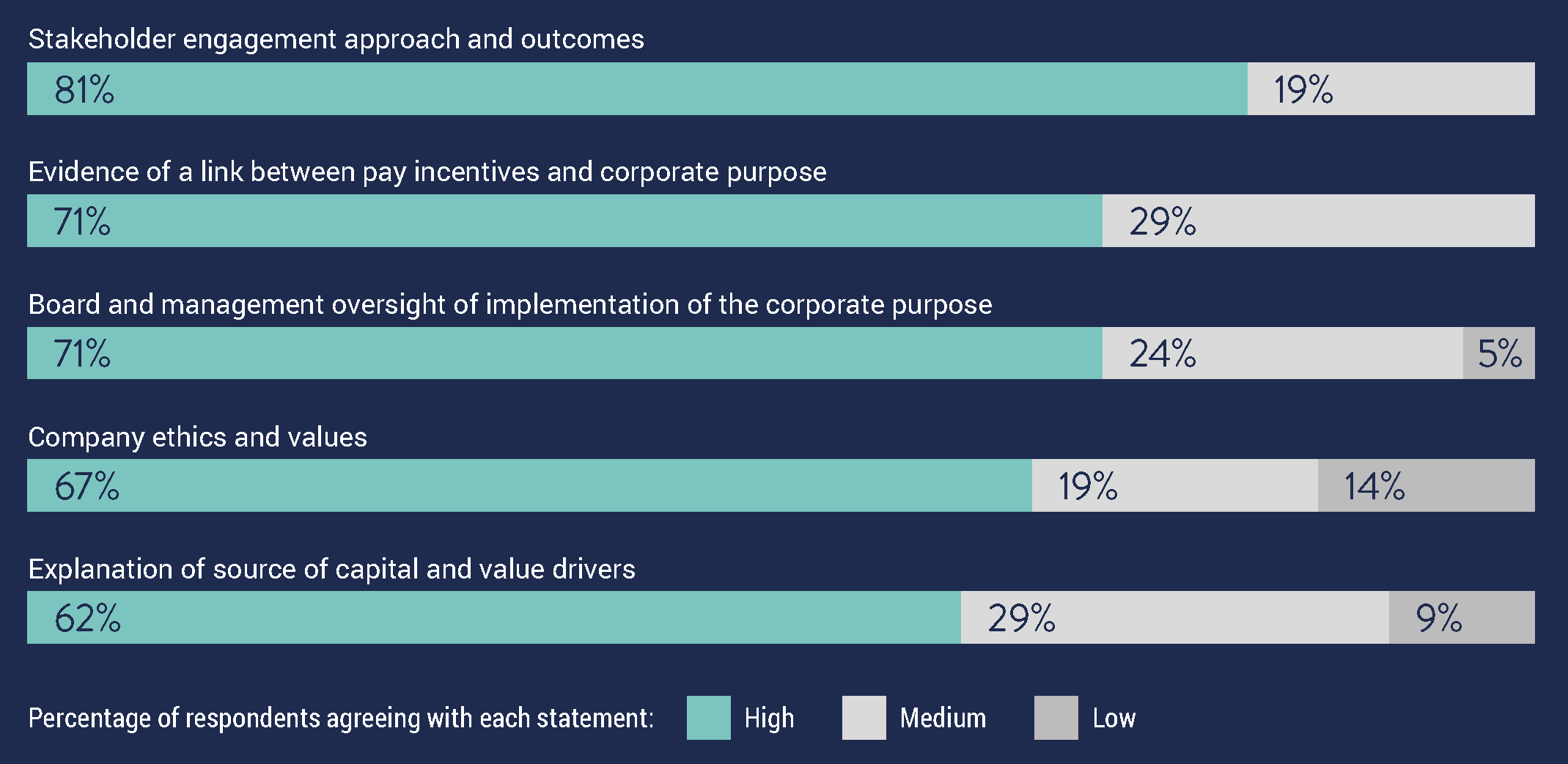

10. What Topics Should the Companies Include When Explaining Their Corporate Purpose?

Setting the Scene

While the concept of corporate purpose is not new, over the past 12 months it has gained momentum following significant value destruction and reputational damage over recent years as a result of corporate scandals. This concept has received new-found attention following the release Statement on the Purpose of a Corporation by the Business Roundtable.

Companies are still not fully clear on the exact implications and there has been little consistency in the use of the term. Nevertheless, focus on the topic of corporate purpose is becoming more common among major listed companies and a significant driver in strategic thinking among corporate executives. Boards are particularly aware that they need to maintain and build trust with their many stakeholders and that they are expected to demonstrate good corporate citizenship and positive impacts.

Results

Even if there is no consensus among investors on exact expectations, they generally recognize the benefit for a company in defining a corporate purpose that should be tied to its core business as well as delivering wider benefits to stakeholders. To that extent, respondents widely agree (81%) that stakeholder engagement approach and outcomes should be included in companies’ disclosures when explaining their corporate purpose.

Going forward, we anticipate investors’ expectations regarding the role, responsibilities and accountability of the board will be amplified. Hence, most investors (71%) expect companies to clearly disclose how the board and management were involved in the implementation of this corporate purpose. Further, companies will need to provide evidence that pay incentives are linked to corporate purpose as stated by 71% of respondents. The expectation that pay incentives are linked to corporate purpose indicates the importance that investors place on how management behavior is influenced and motivated by incentive design.

At the moment, we are experiencing a rapid evolution in the definition of common ESG sustainability standards. The concept of corporate purpose could emerge as a central theme, enabling companies to express their own uniqueness in sustainable value creation.

Key Takeaways

- Stakeholder engagement approach and outcomes (81%)

- Evidence of a link between pay incentives and corporate purpose (71%)

- Board and management oversight of implementation of the corporate purpose (71%)

The complete publication, including footnotes, is available here.