Print

PrintLaura E. Simmons is Senior Advisor, Elaine M. Harwood is Vice President, and Frank T. Mascari is a Principal at Cornerstone Research. This post is based on their Cornerstone memorandum.

Executive Summary

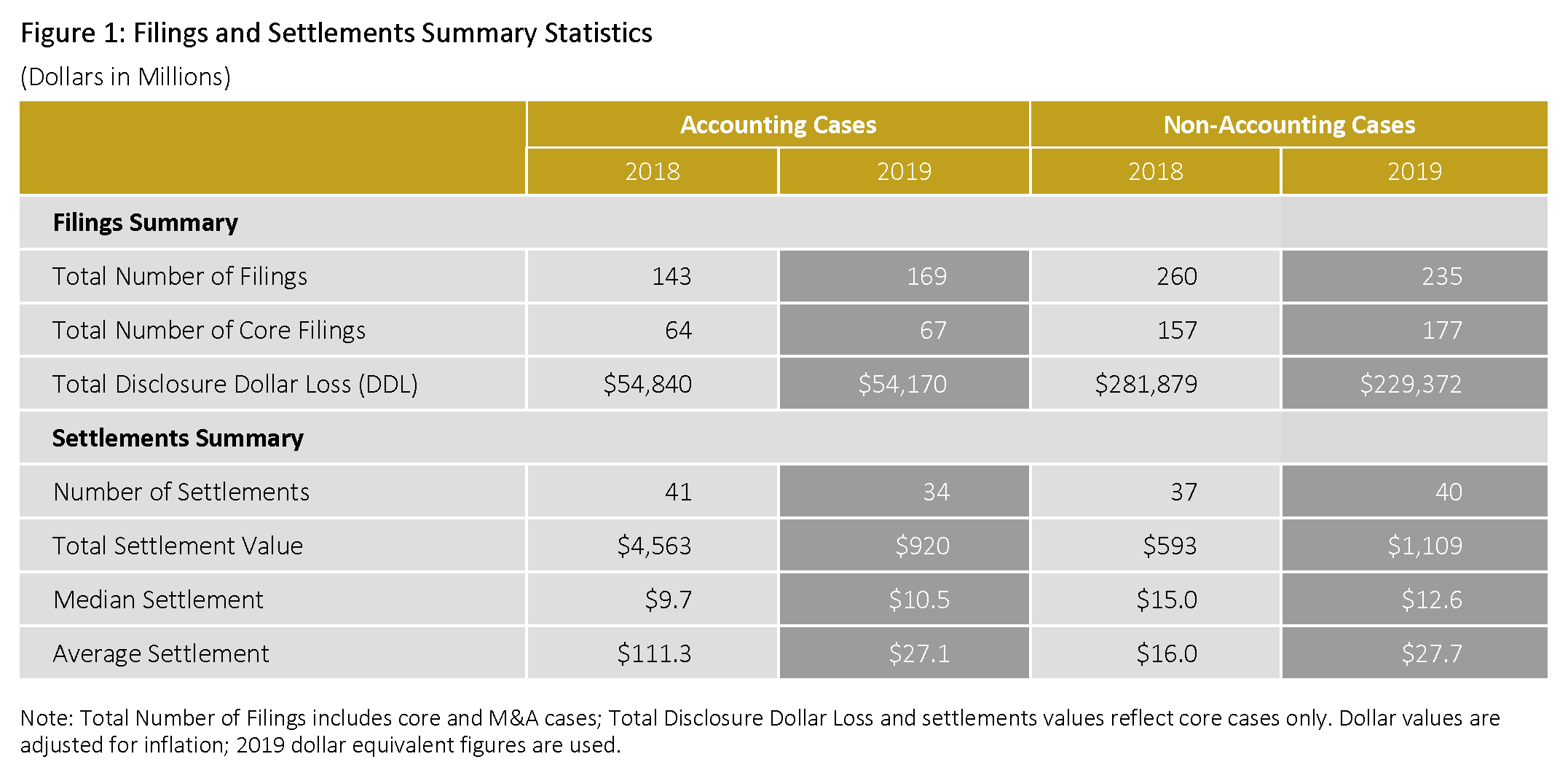

Securities class action filings involving accounting allegations reached a record level as the overall trend of core filings against larger defendant firms continued.

While the total value of accounting class action settlements declined, the median accounting case settlement amount rose in 2019.

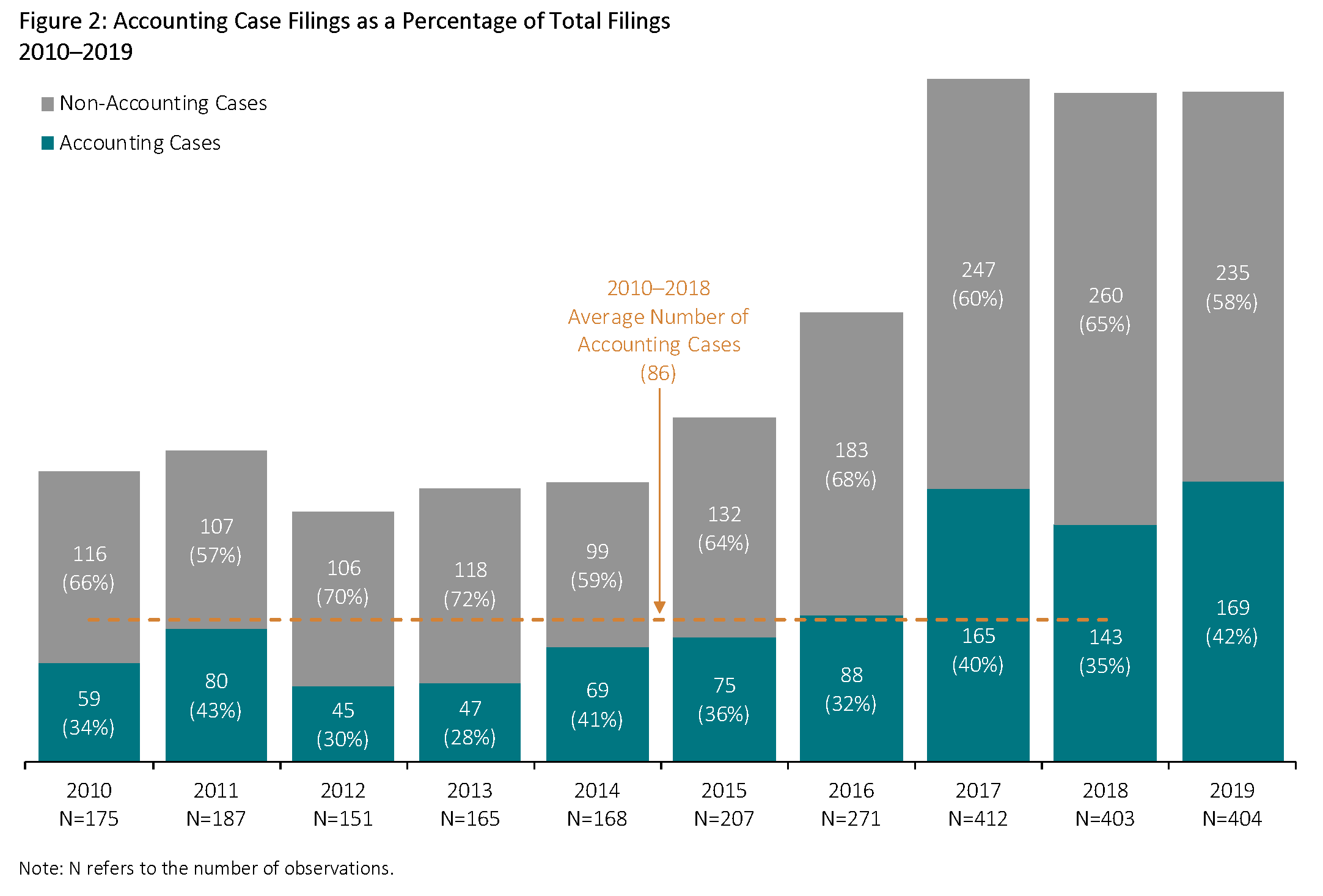

- There were 169 securities class actions involving accounting allegations (accounting case filings) during 2019, nearly double the historical average.

- Accounting class actions as a percentage of total class action filings reached the highest level since 2011.

- Merger and acquisition (M&A) accounting cases alleging failure to reconcile a non-GAAP measure to a GAAP measure increased 29 percent.

- Market capitalization losses for core accounting case filings 3 were 58 percent higher than the historical average as the trend of filings against larger defendant firms continued.

- In 2019, 19 percent of core accounting filings involved allegations of improper revenue recognition.

- The number and proportion of securities class action settlements involving accounting allegations (accounting case settlements) continued to decline, with the proportion of accounting settlements relative to all case settlements at the lowest level over the past decade.

- The median settlement for accounting cases increased over 2018, reflecting a shift in the size of the typical case.

- The total value of accounting case settlements can fluctuate substantially from year to year due to the presence or absence of very large settlements. In 2019, the total value declined, reflecting a lack of any settlements exceeding $500 million, as well as only two mega settlements (settlements above $100 million) involving accounting allegations.

Filings

Number of Accounting Case Filings

- Plaintiffs filed 169 accounting cases in 2019, the highest number on record.

- Accounting case filings increased by 18 percent over 2018, driven by increases in both core accounting case filings (5 percent) and M&A-related accounting case filings (29 percent).

- The proportion of accounting case filings to total case filings (42 percent) was the second highest over the last 10 years.

- The total number of accounting case filings in 2019 was nearly double the 2010–2018 average of 86.

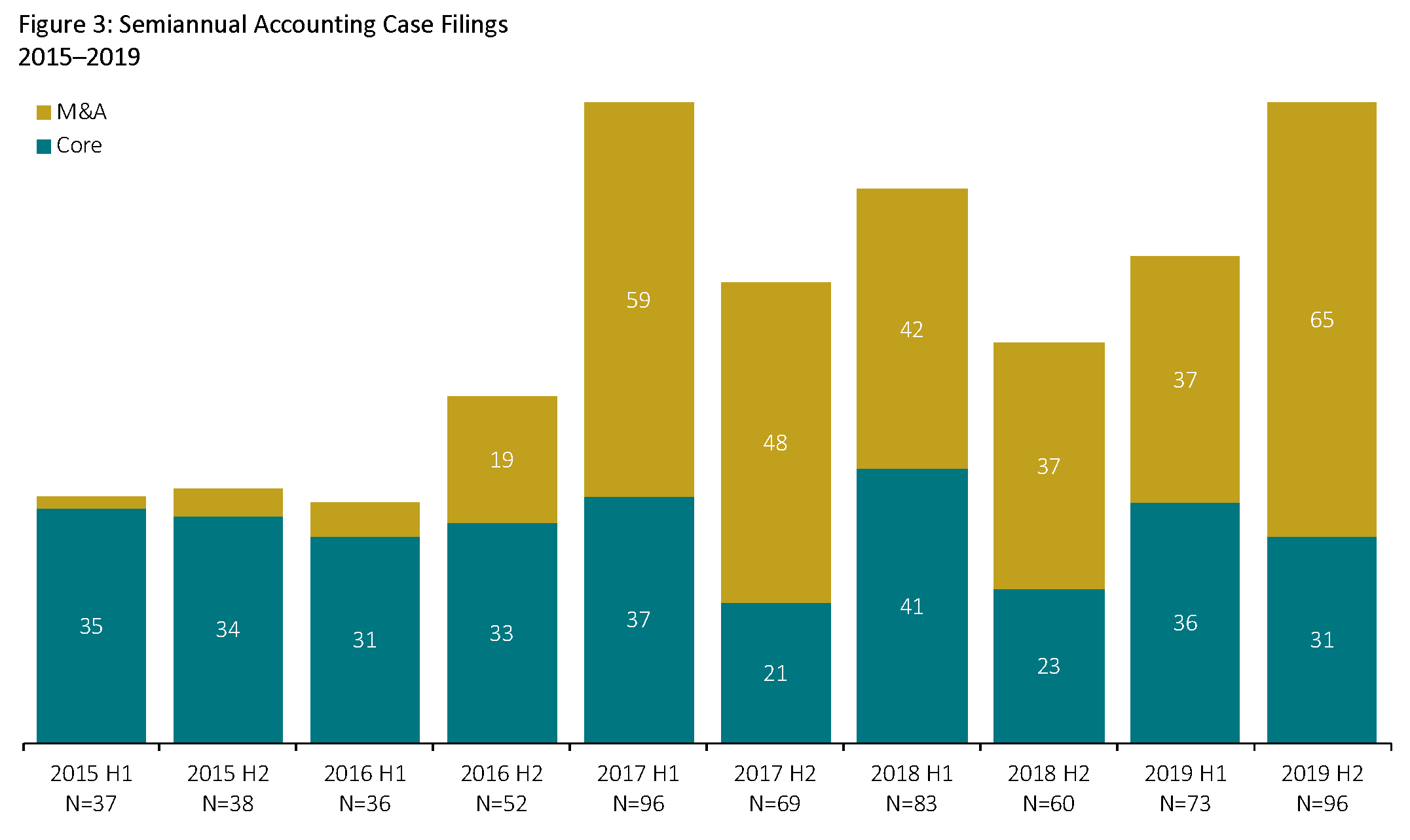

Semiannual Accounting Case Filings

- Total accounting case filing activity increased by 32 percent in the second half of 2019 compared to the first half of the year.

- More M&A accounting cases were filed in the second half of 2019 than in any other semiannual period in the last five years.

- For the third consecutive year, the pace of core accounting case filings slowed in the second half of the year.

- M&A accounting cases constituted 75 percent of all M&A cases in the second half of 2019 compared to approximately 50 percent in the first half of the year. This is the highest proportion for any half-year period.

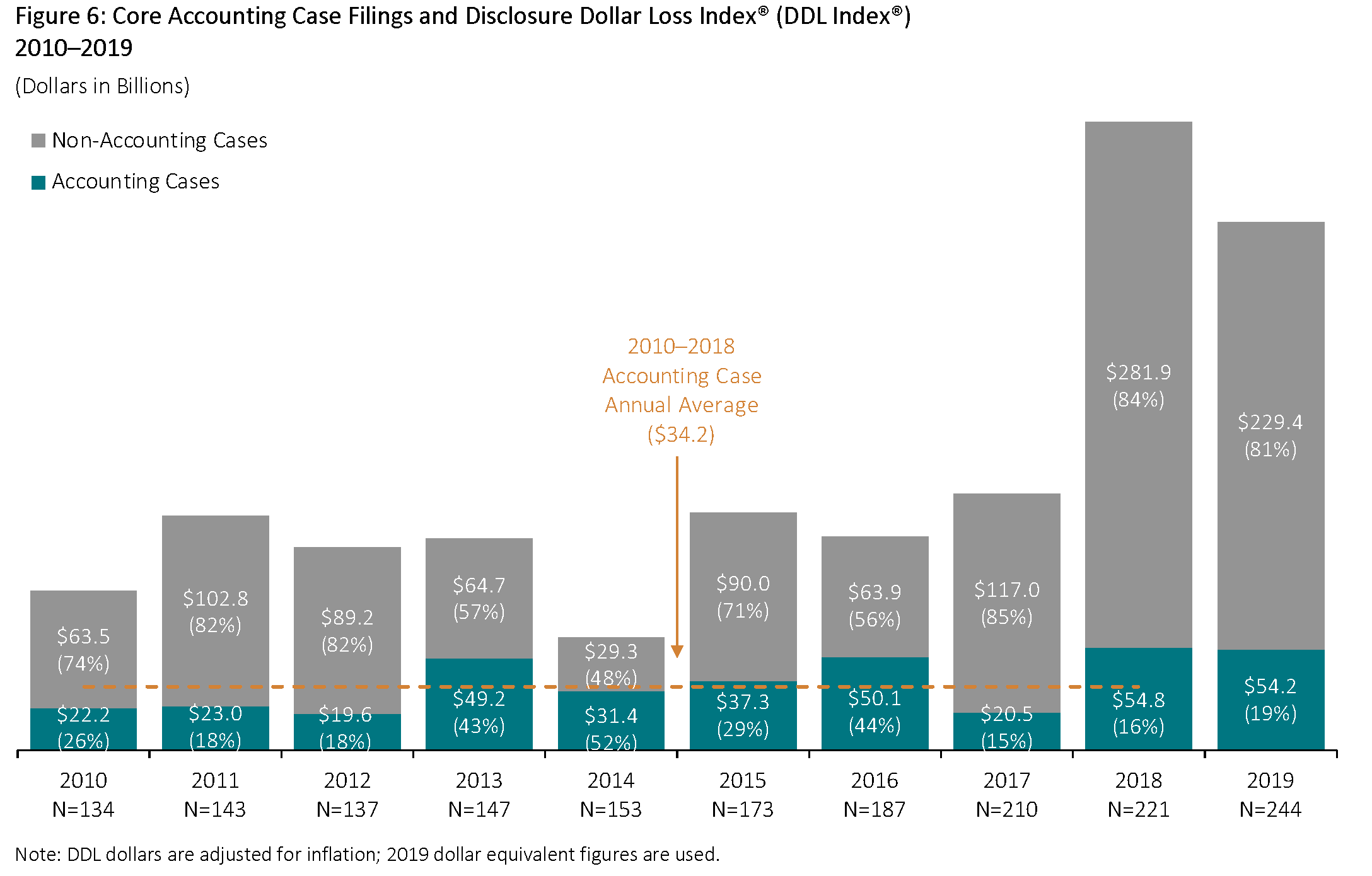

Core Accounting Case Filings and Market Capitalization Losses

Disclosure Dollar Loss Index® (DDL Index®)

This index measures the aggregate annual DDL for all filings. DDL is the dollar value change in the defendant firm’s market capitalization between the trading day immediately preceding the end of the class period and the trading day immediately following the end of the class period. DDL should not be considered an indicator of liability or measure of potential damages.

- The DDL Index for core accounting cases in 2019 was 58 percent greater than the 2010–2018 annual average DDL for accounting cases.

- In 2019, there were two core accounting cases with a DDL of at least $5 billion (mega DDL cases). The two mega DDL cases accounted for approximately half of the total accounting case DDL in 2019.

- Excluding mega DDL cases, the DDL Index for core accounting cases reached its third-highest level in the last 10 years. This is consistent with a continued trend of filings against larger issuer defendants as measured by market capitalization.

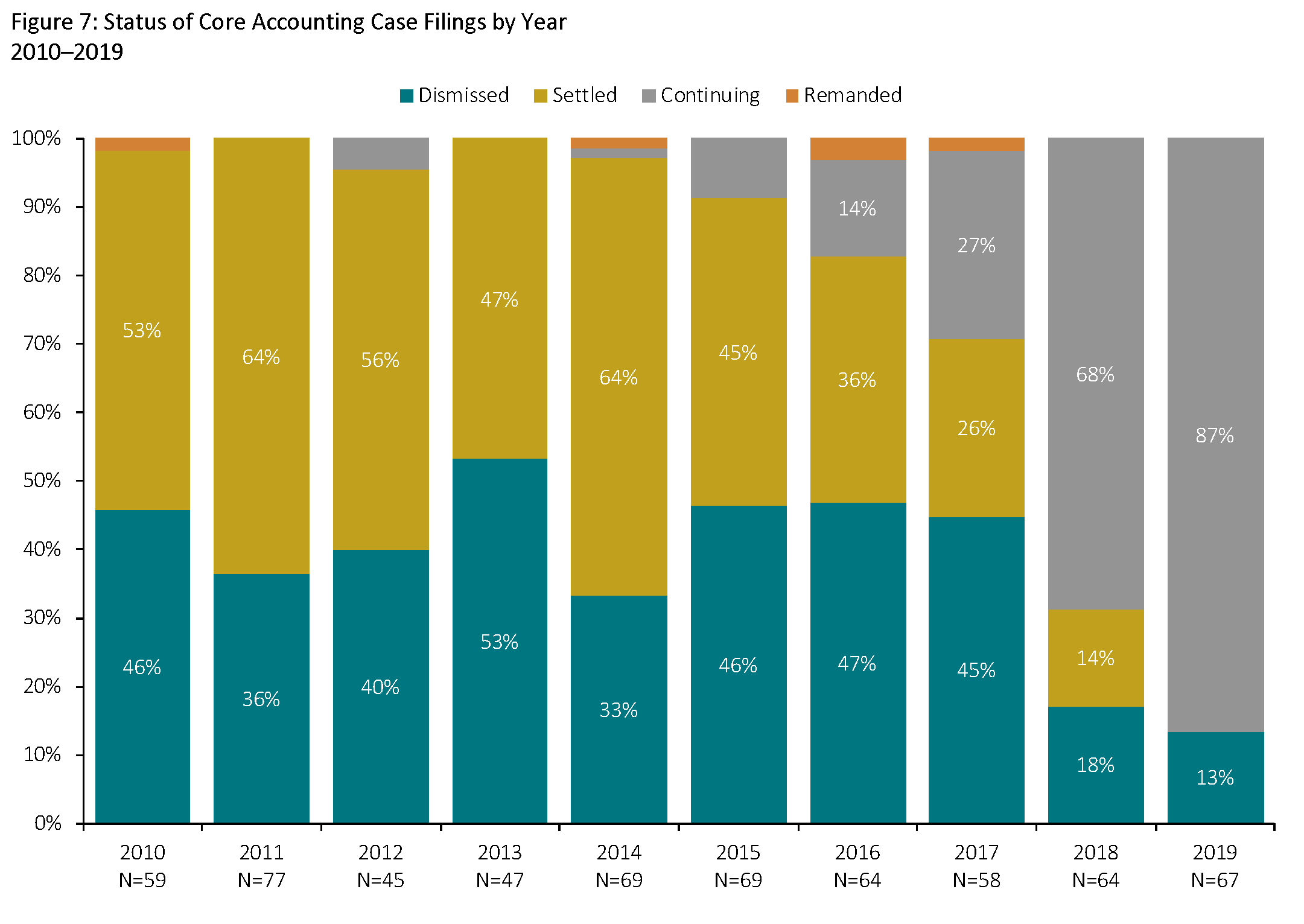

Status of Core Accounting Case Filings

This analysis compares filing groups to determine whether filing outcomes have changed over time. As each cohort ages, a larger percentage of filings are resolved—whether through dismissal, settlement, remand, or trial verdict.

- From 2010 through 2018, 45 percent of core accounting cases settled, 40 percent were dismissed, 14 percent are continuing, and 1 percent were remanded.

- Dismissal rates for M&A accounting cases filed in the past three years have been significantly higher than the rates for core accounting cases. Over the last three years, 84 percent of M&A accounting cases have been dismissed.

- More recent cohorts have too many ongoing cases to determine their ultimate dismissal rates. However, the 2016 cohort will end up having a dismissal rate of at least 47 percent.

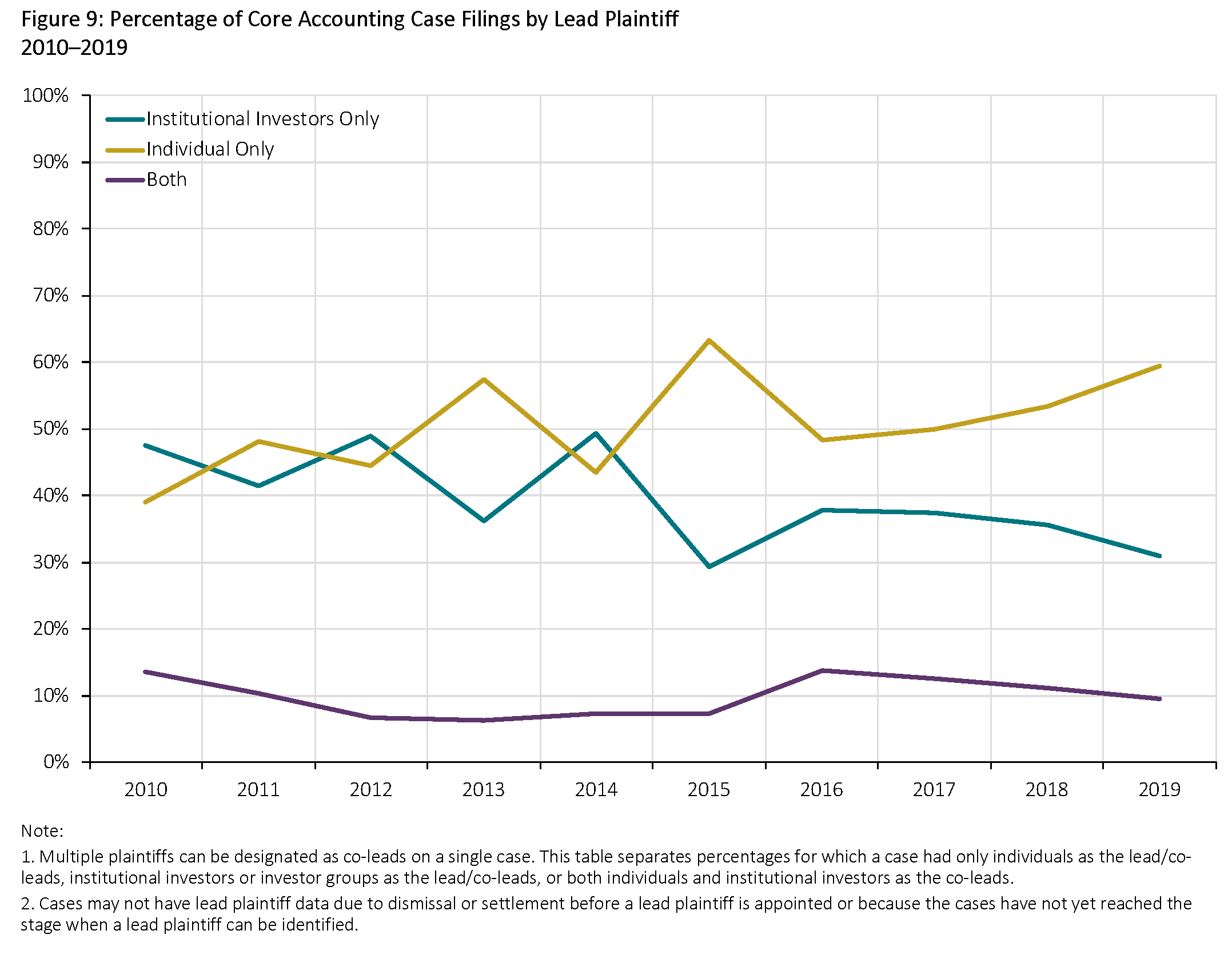

Core Accounting Case Filings by Lead Plaintiff

This analysis examines how frequently individual or institutional investors were appointed as lead plaintiffs in core accounting case filings.

- On average, individual investors were appointed as lead plaintiffs in 60 percent of core accounting case filings over the last 10 years.

- Institutional investors were appointed as lead plaintiffs more often than individual investors in only three of the last 10 years and not since 2014.

Settlements

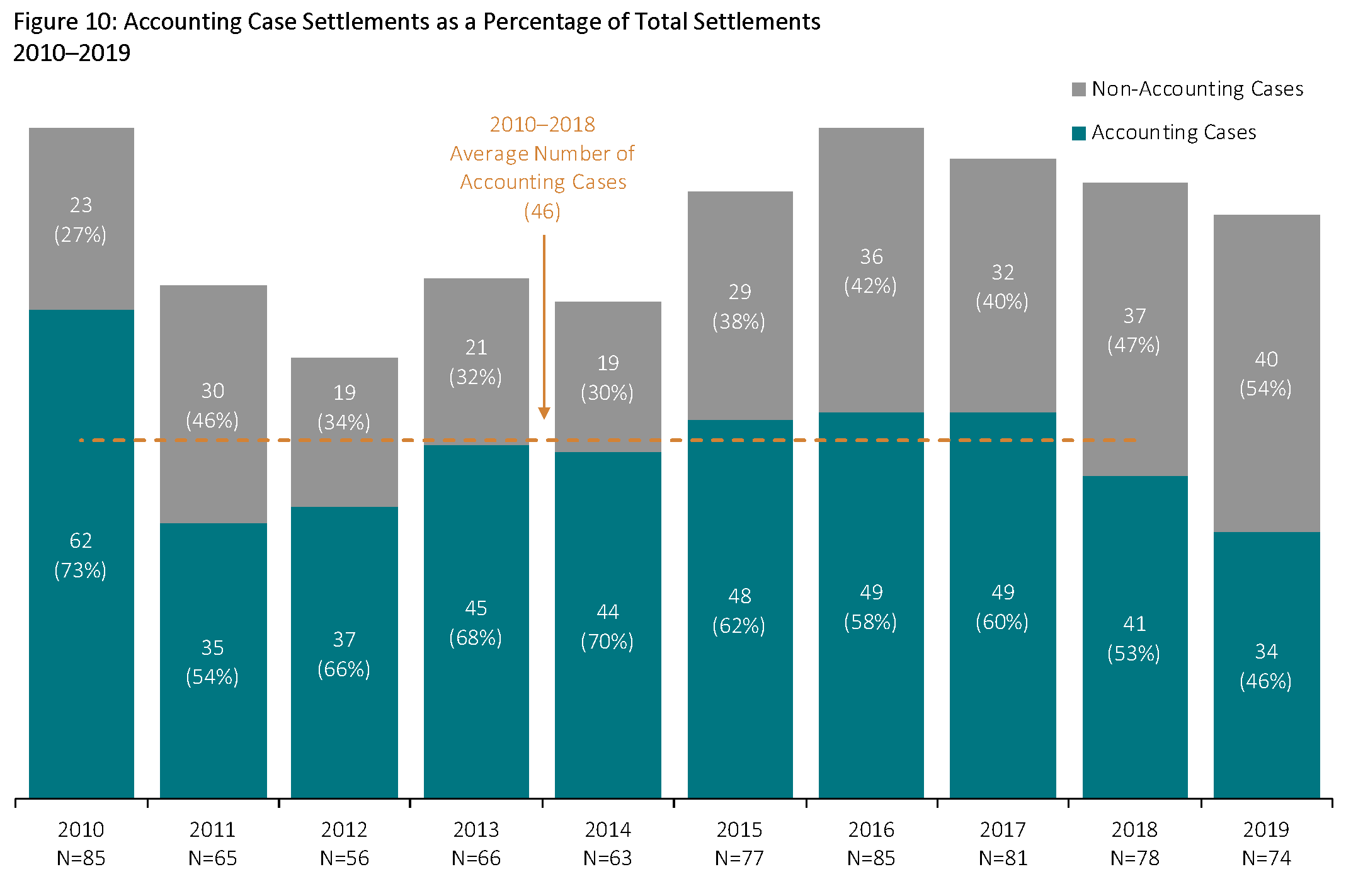

Number of Accounting Case Settlements

- As a percentage of all settlements, the proportion of accounting case settlements decreased in 2019 to the lowest level over the last 10 years.

- The median time from filing to settlement for accounting cases in 2019 was 2.8 years. Thus, the reduced number of accounting case settlements in 2019 in part reflected the relatively low number of core filings during 2016–2018.

- The proportion of settled accounting cases involving accompanying SEC actions increased in 2019 to 44 percent of all accounting cases—the highest proportion since 1998.

- Public pension plan involvement as lead plaintiffs in settled accounting cases fell to its lowest level in the past decade, representing 24 percent of all accounting case settlements.

Accounting Case Settlement Value

- Total settlement dollars continue to vary considerably from year to year depending on the presence or absence of very large settlements.

- The drop in the value of accounting case settlements in 2019 was largely due to a lack of any settlements over $500 million.

- Of the four mega settlements (settlements greater than or equal to $100 million) in 2019, two involved accounting allegations.

The complete publication, including footnotes, is available here.