Print

PrintUmit G. Gurun is the Ashbel Smith Professor at the University of Texas at Dallas Naveen Jindal School of Management. This post is based on a paper, forthcoming in the Journal of Financial Economics, by Professor Gurun; Huaizhi Chen, Assistant Professor of Finance at the University of Notre Dame’s Mendoza School of Business; Lauren Cohen, the L.E. Simmons Professor in the Finance & Entrepreneurial Management Units at Harvard Business School; and Dong Lou, Associate Professor at the London School of Economics.

With the proliferation of information signals in both quantity and dimensionality in recent decades, investors face an increasingly complex portfolio choice problem. These forces create a classic signal-to-noise problem, in which an agent must dig through an ever-larger information set to decipher and to create profitable signals. In a Grossman-Stiglitz world, an agent will be happy to collect information up to their private marginal value of expected return from that activity. However, with hundreds of thousands of information signals being produced in any given day, how does an investor reduce the dimensionality of the investment problem sufficiently to know even which subset (or class) of signals have the potential to be informative and provide this return in expectation?

Exactly how investors approach this foundational problem has remained largely a black box to researchers. In our paper, we offer a novel window into—as well as providing micro-level foundations with regard to—exactly what large portfolio managers do in the search process. We explore how it is conducted and what impact this has on their observable portfolio choices. In particular, using rich, proprietary data provided by the Securities and Exchange Commission (SEC) on every document downloaded from their online site—including the exact timing and IP address of the agent downloading—we provide new evidence on the search process in delegated portfolio management. We show that fund managers follow, and download, information on a very particular subset of firms and this set of firms stays highly constant over time. Further, their trades on these “tracked” firms (i.e., firms where the fund manager downloads a key filing) are significantly more informative for future operations and future firm performance, relative to their other trades.

The key innovation in our paper is that we can explicitly link the monitoring behavior of individual institutional investors (through their download behavior on the SEC’s website) to specific events on the stocks in their own portfolios. No prior study has been able to examine search behavior at the level of a specific institutional investor. In particular, we focus on how institutional fund managers track the trades of corporate insiders in the stocks they own.

We examine this laboratory for a number of reasons. First, compensation and hiring/firing decisions of fund managers are often determined by managers’ performance relative to their peers. In fact, many of the industries’ highest profile rankings (e.g., Morningstar, Kiplinger, Barron’s, etc.) are relative rankings amongst fund managers competing within a mandate. Given this tournament setup, a natural argument in a fund manager’s maximization function would be to find a signal (or set of signals) on which they have a comparative advantage relative to other managers. This begins to put some structure on the information acquisition problem that managers face.

Turning to insider trades, these are a potentially attractive candidate for relative comparative advantage signals for mutual fund managers. First, insiders are, by definition, a class of agents with privileged access to private information regarding their firms. Second, of all the factors of production—and all the information signals on a firm—insider trades are likely amongst the most valuable for unlocking a powerful (and legal) comparative advantage for a given fund manager. For instance, if a firm announces a new product launch, outside of the explicit transmission of material non-public information, it might be difficult (or prohibitively costly in any scalable manner) for an institution to gain a comparative advantage in interpreting this signal relative to other institutions.

However, contrast this with an insider trade within the same firm. The trade itself is public information, a sell, for instance. However, following the publicly disclosed sell, an institutional fund manager who owns the stock, and hence has a connection to that firm could feasibly contact someone at the firm, and inquire whether the sell was for personal liquidity reasons (for instance, to purchase a vacation home.) Once having determined that the sell was related to personal liquidity needs—information that the insider is perfectly legally free to tell her connection (i.e., it is not considered material non-public information to speak about vacation home purchases)—the fund manager can more accurately interpret this public signal of the tracked stock and trade accordingly. Importantly, this is an advantage of a connected manager—in that her competitor funds without a connection to the given insider may have a more costly process in gathering the same private information.

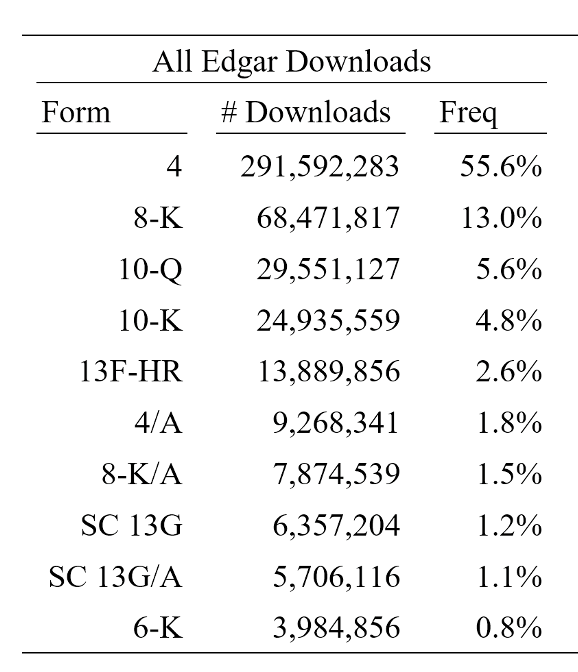

Given all of this, it is perhaps not surprising that insider filings are amongst the most in-demand company filings by investors:

Our results suggest that fund managers are able to know precisely which of their tracked insiders’ trades (e.g., Jamie Dimon’s trades) to follow and which not to, as the trades they track and choose to act upon significantly outperform those that they track and choose not to trade along with. This tracked-trade outperformance holds broadly across firm characteristics (e.g., small and large firms, value and growth firms, high and low past return firms); additionally, it holds considering only the most information-rich subsets of insider trades (e.g., opportunistic insider trades and trades by top executives). Last, the abnormal returns that follow these tracked trades continue to accrue for the quarters following the trades and do not reverse, suggesting that the information contained in the trades is important for fundamental firm value, and is revealed and incorporated into firm value only following the information-rich tracked trades.

We then explore the mechanism at work behind our results in a variety of ways. First, we show that institutional managers tend to track members of the top management teams of firms (CEOs, CFOs, presidents, and board chairs) and accountants and shy away from tracking outside directors. Next we take our institutional holdings data and isolate the fund managers within each institutional investment firm whose holdings correlate most with the insider trades tracked by their fund company and explore these “cherry–picking” fund managers in greater depth. We find that these cherry–picking fund managers are more likely to have an educational or location-based link to the insider in question. These findings are consistent with the idea that fund managers choose to track and mimic the trades of the specific insiders who not only possess the most valuable information but also those with whom they have lower-cost channels for obtaining private information.

Stepping back, as the costs of producing, disseminating, collecting, and processing information continue to fall, signal proliferation will only accelerate. This will make dimensionality reduction a growing problem facing investors for the foreseeable future. We believe that our study—using novel, rich, detailed data on fund manager tracking and trading behavior—is a first step to micro-founding and understanding successful attempts to do precisely this. Future research should push ahead even further to establish alternate ways that investors can solve this problem and engage as important information collectors and price setters in modern capital markets.

The complete paper is available for download here.