The Society for Corporate Governance (the “Society” or “we”) appreciates the opportunity to provide comments to the U.S. Securities and Exchange Commission (the “SEC” or the “Commission”) on the proposed changes to the reporting threshold for Form 13F reports by institutional investment managers (the “Proposed Rules”). We respectfully submit this letter in opposition to the Proposed Rules.

Founded in 1946, the Society is a professional membership association of more than 3,500 corporate and assistant secretaries, in-house counsel, outside counsel, and other governance professionals who serve approximately 1,600 entities, including 1,000 public companies of almost every size and industry. Society members are responsible for supporting the work of corporate boards of directors and the executive managements of their companies on corporate governance and disclosure matters.

I. Introduction

Congress enacted Section 13(f) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), to increase the public availability of information regarding the securities ownership of institutional investors and to increase investor confidence in U.S. securities markets. When the final rules relating to the filing and reporting requirements of institutional investment managers were announced in 1979, the SEC made clear that “[t]he reporting system required by Section 13(f) is intended to create in the Commission a central repository of historical and current data about the investment activities of institutional investment managers, in order to improve the body of factual data available and to facilitate the consideration of the influence and impact of institutional investment managers on the securities markets and the public policy implications of that influence.” Accordingly, as the SEC has recognized, the goals of the Section 13(f) disclosure program are to (i) aggregate data in respect of the investment activities of institutional investment managers, (ii) improve public insight into the holdings of institutional investment managers in order to facilitate the assessment of such managers’ impact on the securities markets, and (iii) increase investor confidence in the integrity of the U.S. securities markets.

In significant part because of public companies’ limited visibility to their shareholders’ identities, Form 13F filings today make up the primary data input for their “shareholder lists.” These disclosures are a primary source for market participants to understand the ownership profile of an issuer’s securities and, in the view of the Society’s membership, are essential to the functioning, growth, and clarity of the U.S. securities markets.

The Proposed Rules would undermine the express purposes of Section 13(f), run contrary to the Commission’s stated objectives with respect to regulating the securities markets, and harm investors, issuers, regulators, and academics alike. In particular, the Proposed Rules would substantially reduce market visibility into public company holdings—a burden that will be borne by issuers of all sizes and that would have the perverse effect of privileging the voices and influence of the already large, growing, and further concentrating index funds and larger asset managers at the expense of smaller institutional investors. In addition, the Proposed Rule’s massive reduction in 13F data will—in the context of the significant increase in investor activism since Section 13(f)’s enactment— dramatically reduce confidence in the integrity of U.S. markets. Accordingly, we respectfully submit this letter in opposition to the Proposed Rules.

Nonetheless, we support the Commission’s goals of modernizing the information reported on Form 13F and increasing the information provided by institutional investment managers. To that end, in connection with a broader overhaul of the shareholder reporting framework, we would be supportive of an increase to the Section 13(f) reporting threshold from $100 million to $450 million to reflect a consumer price inflation adjustment from 1976 to 2019, as previously considered by the Commission and proposed by another commentator. However, the Society believes the SEC should only revise the current 13F reporting threshold as part of a comprehensive modernization of shareholder reporting. As part of such a comprehensive modernization exercise, the Society reiterates its belief that it would be appropriate for the SEC to shorten the quarterly reporting deadline for 13F filings to two business days after the end of the calendar quarter.

This letter proceeds as follows. Section II outlines how the Proposed Rules would significantly reduce market transparency, materially reduce shareholder engagement, hamper capital formation, increase the costs of shareholder activism, and conflict with the policy rationale underlying Section 13(f). Section III provides a cost-benefit analysis, demonstrating that any potential cost savings as a result of the Proposed Rules is more than outweighed by the substantial costs resulting from the decline in market transparency. Section IV outlines the Society’s alternative to the modernization of Form 13F reporting regime, proposing to increase the existing threshold to $450 million and reducing the reporting period to two business days, as part of a comprehensive modernization of Section 13 shareholder reporting.

II. Loss of Transparency

In 1971, the SEC released the Institutional Investor Study Report that was commissioned by Congress three years prior (the “Institutional Investor Report”). There, the Commission recognized that “[t]he importance of a regularized, uniform and comprehensive, scheme of institutional reporting cannot be minimized in light of the demonstrated growth of institutional investment and its impacts on the structure of securities markets, corporate issuers and individual investors.” Accordingly, the SEC concluded in the Institutional Investor Report that “gaps in information about the purchase, sale and holdings of securities by major classes of institutional investors should be eliminated” and recommended that the Commission be granted the “general authority to require reports and disclosures of such holdings and transactions from all types of institutional investors.”

As currently contemplated, the Proposed Rules would eliminate access to information about discretionary accounts managed by more than 4,500 institutional investment managers, representing approximately $2.3 trillion in assets. This means that nearly 90% of institutional investment managers would be relieved from reporting on Form 13F.

In other words, increasing the reporting threshold to $3.5 billion and eliminating the Form 13F filing requirement for nearly 90% of filers widens—not closes—the very same gaps that the SEC was concerned with in the 1970s. Accordingly, the Society expects that the Proposed Rules would materially reduce the ability of issuers to satisfy investors’ increasing demand for engagement and would complicate the ability of all issuers (but particularly smaller issuers) to access working capital. Implementation of the Proposed Rules would also eliminate disclosure by the vast majority of activist investors of positions below 5%, potentially resulting in an increase in stealth shareholder activist activity and value destruction for both issuers and activist investors.

Market Change Has Reduced Transparency Under Existing 13F Regime

In 1978, when Form 13F was adopted, the distribution of market capitalizations among public companies was more uniform than it is today. In the current market, valuations are markedly more concentrated, with the top five publicly traded U.S. companies constituting approximately 23.1% of the S&P 500. The shareholder bases of larger issuers are also typically dominated by larger investors that accumulate sizable positions in such issuers. In 2020, the “big three” index funds, BlackRock, Vanguard, and State Street, controlled approximately 20% of the S&P 500, representing a radical departure from the historically dispersed ownership of the U.S. stock market.

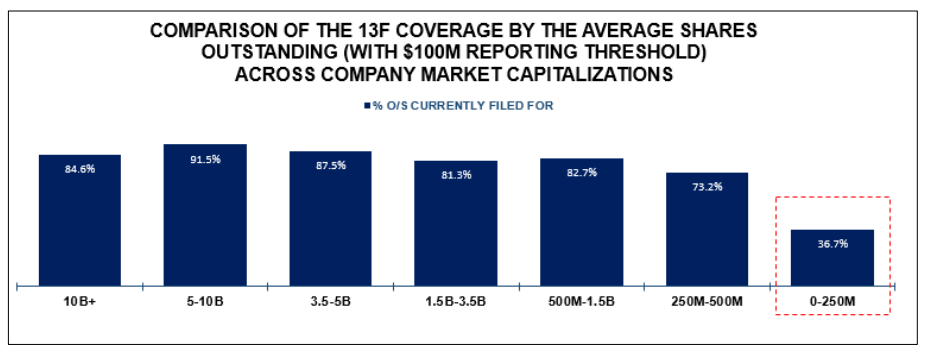

As demonstrated in Table 1 below, market changes over the past 42 years have led to an outdated disclosure regime under Section 13(f). For example, smaller issuers with market capitalizations of up to $250 million have relatively poor visibility into their shareholder base under the existing 13(f) regime: only 36.7% of their shares outstanding (on average) are reported on Form 13F. On the other hand, mid-and large-capitalization issuers have greater visibility today: over 80% of their shares outstanding (on average) are reported on Form 13F.

Table 1 (Source: Innisfree M&A Incorporated, as of August 18, 2020)

Impact of the Proposed Rules

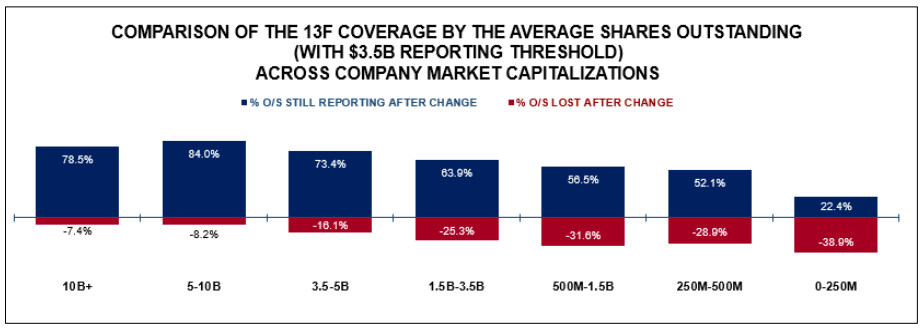

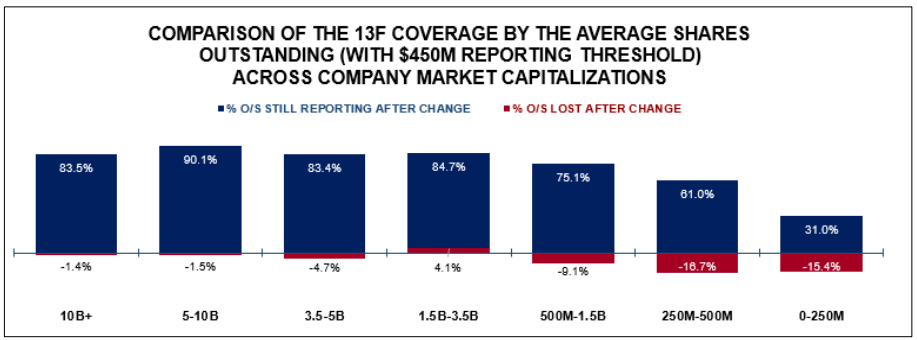

Under the Proposed Rules, the gap in visibility into the shareholder bases of large- versus small-capitalization issuers is likely to widen substantially. As demonstrated in Table 2 below, issuers with market capitalizations below $250 million would lose visibility into approximately 38.9% of their shares outstanding (on average), while issuers with market capitalizations of $10 billion or greater would lose visibility into approximately 7.4% of their shares outstanding (on average). The Society is also aware of members representing larger issuers who expect substantially greater reductions in transparency with respect to their shares outstanding than the average reported in the Survey.

Table 2 (Source: Innisfree M&A Incorporated, as of August 18, 2020)

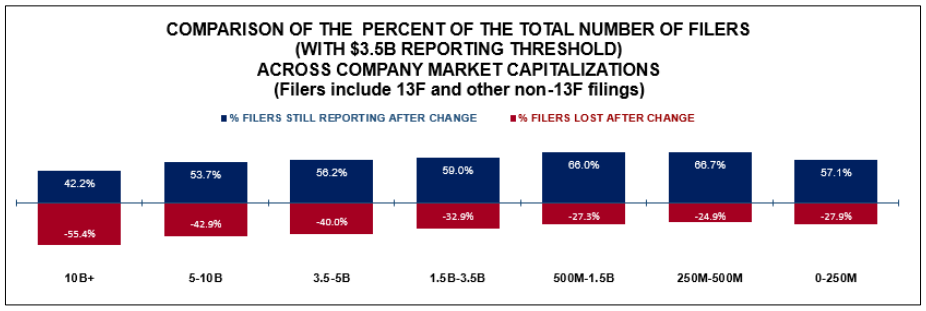

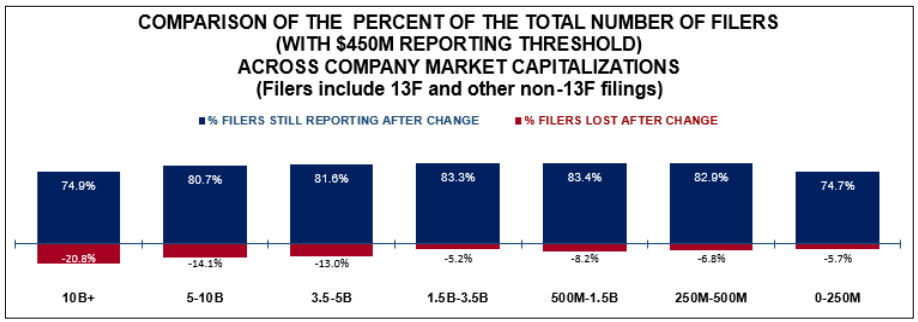

The Proposed Rules would also have a differential effect on issuers by market capitalization with respect to each issuer’s visibility in the number of filers of Form 13Fs holding its stock. As demonstrated in Table 3 below, issuers with market capitalizations of $10 billion or greater would lose visibility into approximately 55.4% of their filers (on average), while issuers with market capitalizations below $250 million would lose visibility into approximately 27.9% of their filers (on average). In other words, although smaller issuers would lose visibility into substantially more shares than larger issuers under the Proposed Rules, the larger issuers are expected to lose visibility into substantially more filers than smaller issuers. The Society expects the impact of these changes to significantly affect the ability of issuers across all market capitalizations to identify and engage with their shareholders. Even if those smaller investors who will no longer be visible to issuers only hold a small percentage of an issuer’s shares outstanding, such investors may still have a significant influence on issuers (e.g., hedge funds and activists). Moreover, the net effect of privileging the voices of larger investors over smaller investors is antithetical to the Commission’s mission and to the preferences of issuer and the investment community.

Table 3 (Source: Innisfree M&A Incorporated, as of August 18, 2020)

As discussed in Section IV, the Society believes that increasing the existing threshold to $450 million would have a less harmful effect on issuers across all market capitalizations, while still advancing the Commission’s goals of modernizing the information reported on Form 13F and increasing the information provided by institutional investment managers.

Impact of the Proposed Rules on Shareholder Engagement

As Chairman Clayton has noted, “[s]hareholder engagement is a hallmark of our public capital markets” and one of the “key principles” of our securities laws. Further to such suggestions, the Commission has, in recent years, taken steps to enhance shareholder engagement in the corporate governance of public companies and attempted to modernize SEC rules around such engagement. The Society fears that the Proposed Rules would lead to a stark regression in shareholder engagement.

Since the adoption of Section 13(f) more than 40 years ago, there has been a meaningful increase in shareholder engagement by issuers, including engagement with respect to long-term strategy, M&A, environmental, social, corporate governance and other matters, establishing a foundation for communications with shareholders and increasing shareholder confidence. To that end, issuers commonly hire and retain investor relations professionals to ensure that the concerns of investors are heard, conveyed to management, and acted on.

According to a survey of 157 issuers conducted by the Society in September 2020 (the “Survey”), approximately 94% of the respondents stated they use Form 13F to identify institutional ownership, approximately 89% of the respondents stated they use Form 13F to monitor accumulations of holdings, and approximately 68% of the respondents stated they use Form 13F to identify, prepare and respond to activist attacks. In response to the Survey’s question regarding how the issuer monitors investor movements in the issuer’s stock, approximately 14% of the respondents stated they use Form 13F reports, approximately 10% of the respondents stated that they use either a stock surveillance program or a stock watch firm (who in turn use Form 13F reports), and approximately 75% of the respondents stated they use a combination of Form 13F reports and stock watch. In the absence of comprehensive Form 13F data, the members of the Society fear that they would be left without an adequate source to track their shareholders, especially if they may not be able to afford costly stock surveillance programs to assist in the verification of investor ownership. Even if they could afford stock surveillance programs, or are currently using such programs, all stock surveillance programs rely on the disclosures provided on Form 13F to form the initial basis of their analysis. Accordingly, the Proposed Rules would render stock surveillance services substantially less effective. Further, the inability of issuers to identify their investors by relying on the quarterly ownership information set forth in Form 13F filings is particularly problematic in light of misrepresentation by investors of their positions in issuers. According to the Survey, approximately 15% of the respondents stated they have experienced misrepresentation by investors of their holdings while seeking engagement with issuers’ management or board of directors.

As general counsel, corporate secretaries, and other governance professionals, the Society’s members are frequently tasked with managing their company’s shareholder meeting processes, including facilitating the exercise of shareholder voting rights, and spearheading shareholder engagement efforts. According to the Survey, approximately 86% of the respondents stated that they are using Form 13F reports in formulating their shareholder engagement strategy and meetings, and virtually all (98%) of the respondents stated that the Proposed Rules do not facilitate shareholder engagement. Moreover, given the loss of visibility into the shareholder bases of issuers across all market capitalizations, compliance, monitoring and shareholder engagement costs are likely to increase substantially.

The Proposed Rules would make effective and efficient interactions between issuers and investors much more difficult. As detailed above, increasing the reporting threshold for institutional investment managers from $100 million to $3.5 billion would reduce issuers’ insight into their investor base, making it more difficult to discern the appropriate amount of time and resources necessary for direct engagement with shareholders that have requested to speak with management and/or board of directors. According to the Survey, approximately 67% of the respondents stated that they believe the Proposed Rules would result in a decrease in engagement with investors with less than $3.5 billion assets under management. Additionally, such limited insight would potentially make it more difficult for issuers’ boards of directors to ascertain to whom (and to what type of investors) they owe their fiduciary duties. Further, another likely result of the reduced insight is that large institutional investors (i.e., those that will continue to provide Form 13F disclosure) will be further prioritized and therefore exert even greater influence over issuers at the expense of smaller investors, a result both contrary to the Commission’s efforts to improve participation in corporate processes by smaller investors and detrimental to the securities markets as a whole.

Negative Impact on Capital Formation

As issuers and academics have noted, the Proposed Rules’ attempt at preventing front running and copycatting comes at the cost of significant “market opacity,” which, in turn, results in a reduction in capital formation. On the one hand, Form 13F data is essential to the ability of issuers to identify potential investors and attract new long-term investments necessary for growth. The opaqueness of an issuer’s investor base will likely cloud fundraising activities, as certain issuers will suffer from an inability to pinpoint new capital sources (e.g., investors that have made investments in the issuer’s industry) and monitor the efficacy of certain interactions with prospective shareholders. This is especially true for newly public issuers who may regularly access the securities market. Such issuers rely on information from Form 13F to monitor their shareholder base and engage with potential investors on an ongoing basis. This engagement is critical, as equity offerings are typically conducted with only one or two days of public marketing. With the adoption of Rule 163B, which allows “testing-the-waters” for all issuers, the SEC has validated the need for such engagement. On the other hand, the visibility provided by Form 13F disclosures encourages investments from smaller investors (i.e., through the assessment of crowdedness of trades). The Proposed Rules, and the attendant loss of visibility, introduce uncertainty for investors, potentially yielding fewer investments that facilitate capital formation and growth for issuers and making the securities offering process disproportionately burdensome for all issuers.

Promotion of Activist Activity

Increasing the ownership threshold from $100 million to $3.5 billion would result in many of the most influential activist hedge funds no longer filing Form 13F reports altogether. In the wake of the Proposed Rules, out of a total of 123 activist hedge funds that are currently required to file, only 25 (20%) would continue reporting on Form 13F. That is, other than the largest activists (e.g., Carl Icahn, Elliott Management, and Third Point), even prolific and vocal activists, such as Starboard Value, JANA Partners, Greenlight Capital, Engaged Capital, Land and Buildings, and Marcato, would generally not be required to disclose their sub-5% positions on a quarterly basis on Form 13F.

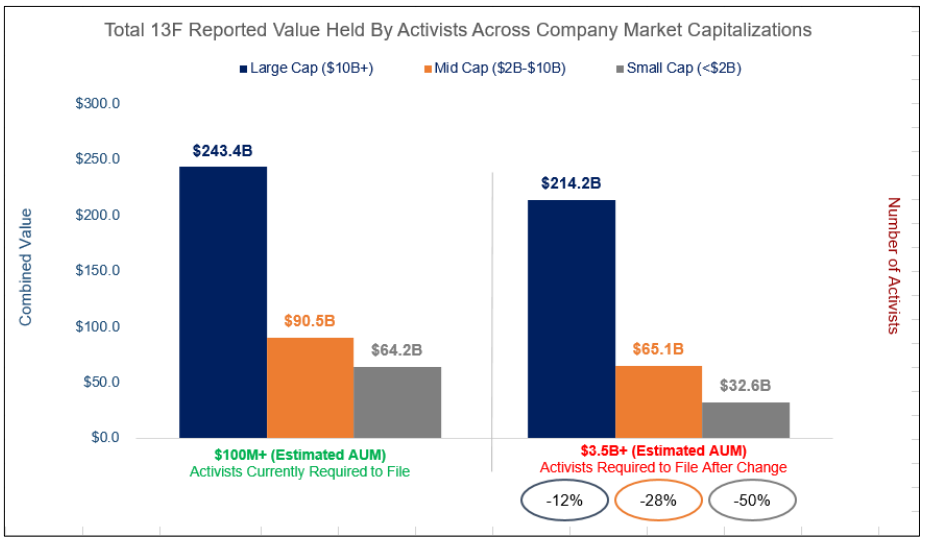

Eliminating Form 13F disclosure for most activist investors will affect issuers across all market capitalizations but will have an especially significant impact on smaller issuers, which are already more vulnerable to activism and hostile takeover activity than their larger peers. As shown in Table 4 below, under the current $100 million reporting threshold, activists hold a combined value of $64.2 billion worth of stock in small-capitalization issuers. As a result of the Proposed Rules, activists will continue reporting only $32.6 billion worth of stock in small-capitalization issuers. In other words, roughly 50% of activist equity holdings ($31.6 billion worth of stock) in smaller issuers would “go dark”.

To compare, as a result of the Proposed Rules, mid-and large-capitalizations issuers would lose visibility of 28% and 12%, respectively, of activists’ positions.

Table 4 (Source: Innisfree M&A Incorporated, as of August 30, 2020)

As a result of reduced disclosure by activist investors, issuers will no longer have key existing tools to identify, monitor, and prepare themselves for activist campaigns that frequently seek to influence the management, control, and boards of directors of issuers. In recent years, shareholder activists have become more numerous and diverse than they were in the past, both in their agendas and their methods. While in the 1980s corporate control and takeovers were activists’ primary goals, today’s shareholder activism is more focused on attempting to manufacture short-term value without a change in control, and doing so by leveraging a small ownership percentage, often no more than three to five percent. These changes in activism trends have led issuers’ boards of directors, together with management, to engage with shareholder activists proactively. The Proposed Rules will inhibit the ability of issuers, particularly smaller issuers, to effectively prepare for, identify, and respond to activist attacks, potentially facilitating the short-term investment objectives of a small subset of investors at the expense of the broader shareholder base.

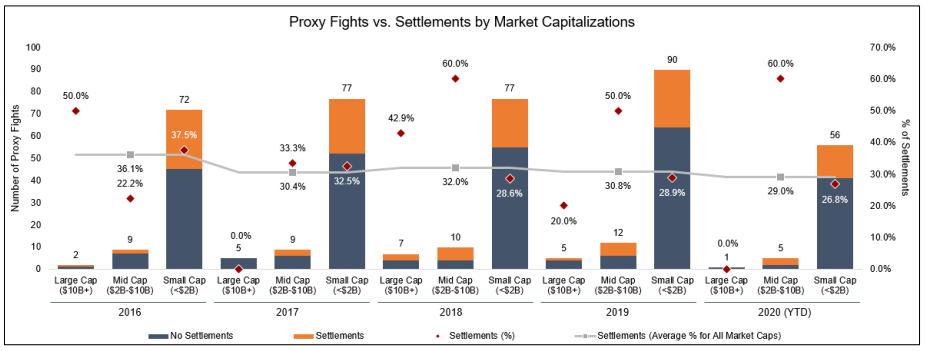

Additionally, the inability to identify activist investors is likely to increase the cost of shareholder activism activity for both issuers and investors while simultaneously reducing trust and transparency between them. Activists and issuers frequently reach settlements on the basis of an implicit understanding of how shareholders are likely to vote on a given issue, thereby negating the necessity of prolonged and expensive shareholder solicitation processes. Table 5 below shows the total number of proxy fights against U.S. issuers (across market capitalizations) between the years 2016 and 2020 (YTD) and the percentage of reported settlements reached in each of these years out of the total number of proxy fights. On average, the percentage of settlements across all issuer market capitalizations was approximately 32 percent between the years 2016 and 2020 (YTD), with a higher percentage of settlements occurring at small- and mid-capitalization issuers. The Proposed Rules would make settlements and other informal, non-public discussions (such as “quiet” campaigns where an activist engages with the issuer behind the scenes) with activists significantly more challenging because it would be more difficult to gauge investor sentiment, predict shareholder voting outcomes, and quantify the value of preempting proxy contests.

Table 5 (Source: FactSet, as of September 13, 2020)

III. The SEC’s Cost Benefit Analysis is Incomplete and Warrants Reconsideration

Purported Savings Do Not Justify The Reduction In Transparency

We believe that the Commission’s economic analysis related to these proposed amendments requires further study by the Commission of the cost and benefit impacts on market participants, including public company issuers represented by the Society. Particularly, while we believe there are opportunities to improve the timeliness and transparency of this data, further economic analysis by the Commission of the substantial costs of the lost transparency of 13F data on public company issuers is needed, as the 13F filings remain the only publicly-available source for public companies for quarterly data on the “street name” investors who are buying or selling their shares.

As mentioned above, the Society’s members heavily rely on 13F data to make determinations regarding capital formation activities and shareholder engagement strategies, including increasing their understanding as to whether shareholders are invested in them for the long-term. While the Commission’s economic analysis stresses the availability of other data sources, such as the Schedules 13D and 13G, and the Form N-PORT, these reports are not adequate substitutes, as Schedules 13D and 13G only become applicable if a person acquires beneficial ownership of 5 percent or more of an issuer’s outstanding shares. Likewise, Form N-PORT data is only publicly available on a delayed basis and is limited to registered management investment companies, which are more likely to be the largest firms, which would continue to be identified through 13F filings and Schedules 13D and 13G.

Therefore, without the 13F reports, Society members would be limited in tracking ownership changes or verifying how much of their respective stock is owned by investors who may refuse to disclose their stakes—even after those investor reach out to issuers, request meetings with issuer management, or launch activist campaigns against issuers. However, the Commission’s proposal does not provide a more specific analysis of the value of this lost transparency.

Without access to 13F data, the Society’s members, as discussed above, would need to further rely on stock surveillance firms for capital formation activities and shareholder engagement. In 2016, Bloomberg estimated the annual cost of stock surveillance was $25,000 to $50,000 and in the experience of the Society’s members these annual costs are currently far higher and potentially prohibitive for smaller issuers. With the competitive force of freely available 13F data removed, stock surveillance firms would likely be able to charge more for their services (even as the services would become less effective due to the absence of this 13F data) and become more cost prohibitive for smaller issuers.

In addition, the Society believes further study by the Commission is required on the cost consequences to issuers and shareholders on capital formation activities and reduced and less effective shareholder engagement. As discussed above, less engagement would ultimately lead to more proxy contests and less effective engagement processes with respect to activists’ campaigns and shareholders generally. Activist campaigns are costly for management, both in direct expenses and in the significant time and attention diverted from running the business. The Society believes ongoing shareholder engagement and bringing activists shareholders and issuers together to the negotiating table sooner allows public company issuers to achieve better outcomes for shareholders overall, including through negotiated settlements and costs avoided. The data provided by 13F filings is a key tool for issuers to continue positive engagement strategies that allow them the opportunity to proactively avoid these costs and achieve negotiated outcomes that benefit its shareholders at large.

The expenses of responding to activists’ campaigns are substantial to the Society members and ultimately are passed through to shareholders. A 2014 study found that a contested activist campaign costs a company between $10 million and $20 million—plus weeks of management time to develop plans and meet with investors. Furthermore, Society members are more frequently being asked for reimbursements of expenses from activists’ campaigns with U.S. public company issuers spending an average $431,831 to cover activists’ campaigning costs in 2018. Without 13F data, the Society would expect that these costs would grow significantly as public company issuers would have less information to create proactive engagement strategies that can avoid distracting protracted activist campaigns and proxy contests and would experience substantially increased costs in identifying investors through such campaigns. Analysis on the potential increase in these costs, which are already substantial for public company issuers, along with the negative impact on capital formation, is absent from the Commission’s current analysis and merits further consideration.

IV. 13F Changes To Be Considered As Part of a Comprehensive Modernization of Shareholder Reporting

The Society welcomes the SEC’s efforts to modernize the reporting regime applicable to institutional investment managers but does not believe modernization can be accomplished in a piecemeal fashion. The Society believes that efforts to modernize the Form 13F reporting regime should only be made in a holistic manner as part of a comprehensive modernization of shareholder reporting. Such a holistic approach would update the regime to provide for more current information, reflect the reality of modern investment practices so that reports do not present a distorted and inaccurate view of investment activities and, because those reforms could impose some incremental costs on institutional investment managers, the Society would support an increase in the threshold for Form 13F reporting to $450 million to reduce burdens on smaller managers.

New $450 million Threshold

The Society appreciates that the reporting threshold for Section 13(f) has not been increased since it was first implemented and that the reforms discussed below would impose some incremental costs on some institutional investment managers. As a result, if the SEC is amenable to modernizing Form 13F holistically, the Society would be supportive of a modest increase in the 13F reporting threshold. However, for the reasons noted above, any small cost savings that might be realized by some incremental investment managers by increasing the reporting threshold from $100 million to $3.5 billion are wildly disproportionate to the substantial deleterious effects of the Proposed Rules. As an alternative to such a dramatic increase in the reporting threshold and associated reduction in information made available to the public, issuers, and the SEC, the Society believes that an increase of the threshold to $450 million, reflecting inflation, would have a less harmful effect on issuers across all market capitalizations.

As demonstrated in Table 6 below, under the proposed $450 million threshold, issuers with market capitalizations below $250 million would lose visibility into approximately 15.4% of their shares outstanding (on average) (versus a loss of approximately 38.9% under the Proposed Rules), while issuers with market capitalizations of $10 billion or greater would lose visibility into approximately 1.4% of their shares outstanding (on average) (versus a loss of approximately 7.4% under the Proposed Rules). Additionally, as demonstrated in Table 7 below, under the proposed $450 million threshold, issuers with market capitalizations of $10 billion or greater would lose visibility into approximately 20.8% of their filers (on average) (versus a loss of approximately 55.4% under the Proposed Rules) and issuers with market capitalizations below

$250 million would lose visibility into approximately 5.7% of their filers (on average) (versus a loss of approximately 27.9% under the Proposed Rules).

Table 6 (Source: Innisfree M&A Incorporated, as of August 18, 2020)

Table 7 (Source: Innisfree M&A Incorporated, as of August 18, 2020)

Further, under the proposed $450 million threshold, issuers across all market capitalizations would lose visibility into approximately 7.5% of their shares outstanding (on average) (versus a loss of approximately 22.3% under the Proposed Rules). Additionally, issuers across all market capitalizations would lose visibility into approximately 10.5% of their filers (on average) (versus a loss of approximately 36% under the Proposed Rules). To that end, the Society believes that a proportional increase of the existing threshold to $450 million would have a less harmful effect on issuers across all market capitalizations by allowing them to maintain greater visibility into their shareholder bases as well as to identify their investors, while still advancing the Commission’s goals of modernizing the information reported on Form 13F and increasing the information provided by institutional investment managers. This approach would be consistent with the recommendation of the SEC’s Office of Inspector General (the “OIG”).

Reduce Reporting Period to Two Business Days

The Society believes reducing the significant lag between the date triggering Form 13F disclosure and the filing date would provide substantial benefits to issuers and the market as a whole, while imposing only limited additional costs on institutional investment managers. Currently, the Form 13F reporting regime can allow for over a year—up to 382 days—between when an institutional investment manager first becomes subject to the requirement to file Form 13F and when that manager’s first filing is due. That first report would include information as of the end of the fourth calendar quarter of the year during which the institutional investment manager crosses the filing threshold and be filed 45 days after that quarter end. Subsequent reports are due 45 days after the end of each calendar quarter and present information as of the end of that calendar quarter.

The six-and-a-half weeks between quarter end, the time as of which a Form 13F presents information, and the date a Form 13F is required to be filed has long been the subject of criticism. In 2013, the Society, together with NYSE Euronext and the National Investor Relations Institute, petitioned the SEC to reduce the reporting deadline to two business days after the end of the calendar quarter. The Society continues to believe that a shorter reporting cycle is appropriate. As noted in its 2013 petition, the month-and-a-half-long gap between the date of the information and when it is published inhibits the ability of issuers to identify, communicate with and engage with their shareholders in real time and results in outdated information being provided to the market and the SEC. The Society believes that institutional investment managers track their portfolios on a daily, if not more frequent, basis, and would be able to produce the limited information—consisting primarily of a list of holdings and their value—required by Section 13(f), within two business days of a reporting date without undue hardship, especially because the date as of which the information need be presented and the date on which it would be required to be filed would be set by regulation and known in advance.

Similarly, current technology allows the period of time between when an institutional investment manager becomes subject to reporting under Section 13(f) and the first reporting deadline to be substantially shortened. While the Society acknowledges that the filing of an initial Form 13F may require more effort than subsequent filings, we believe it is appropriate to require an institutional investment manager to file a Form 13F with information as of the end of quarter subsequent to the quarter during which that manager crosses the Section 13(f) threshold (e.g., if a manager crosses the threshold on January 2, its first filing would include information as of June 30 and be filed in early July) and that such period should provide adequate time to prepare that filing.

In 1979, the SEC focused on the following benefit to justify changing Form 13F filing obligations from annual to quarterly: “Both corporations and financial reporting services asserted that quarterly reporting is needed to provide corporate treasurers with current information concerning institutions owning their stock. They pointed out that many stockholders take ownership in nominee or street name, making it difficult to trace such information and making it difficult to secure proxies on important corporate matters.” That remains at least as relevant—if not more relevant—today as it was in 1979 given the massive increase in beneficial ownership of equity securities.

In addition, since 1979, the frequency and depth of engagement between issuers and their respective shareholders has expanded dramatically. However, the fact that Form 13F reports contain only outdated information substantially reduces the ability of issuers and market participants to actually engage with shareholders in real time with the benefit of that information. Although a long period between the end of a quarter and when information was required to be filed under Form 13F may have been necessary to accommodate systems used by institutional investment managers in 1979, technological advancements have made it so that is no longer the case, nor is it consistent with shareholders’ expectations regarding issuer engagement.

The Society acknowledges that a shortened reporting cycle may lead to calls from hedge funds regarding greater copycatting and front running, and the frequency of confidential treatment requests. As noted in the Society’s 2013 rulemaking petition, these concerns are unpersuasive and rest on the argument that “the 45-day delay period works to the advantage of Managers at the cost of other investors.” We would add that for first-time 13F filers, the “delay period” is frequently far longer. To the extent there are specific positions for which institutional investment managers have particular concerns, those can be addressed through the Commission’s process for handling confidential treatment requests. In connection with a potential increase in confidential treatment requests, the Society would encourage the Commission and its staff (“Staff”) to adopt guidelines to the effect that the Staff will review, approve, reject or comment on confidential treatment requests within 30 days of receipt.

The scope of Form 13F reporting should be enhanced to avoid reporting of incomplete and potentially misleading information

The Society agrees with the finding of the OIG that “[t]he current Form 13F does not provide for the disclosure of all significant investment activities of institutional investment managers, and it could be improved to be more useful to the public.” The 13F reporting regime presents an incomplete picture of both long positions in 13F securities held by institutional investment managers and the overall economic exposure of those managers to 13F securities.

Currently, Form 13F generally does not address reporting of derivative positions other than listed options. As a result, the treatment of positions that are economically equivalent to purchases of 13F securities remains unclear. The limited guidance that is available sheds little light on that matter. For example, in a letter issued to the New York State Teachers’ Retirement System, the Staff made clear that institutional investment managers that lend securities should report those securities on Form 13F—even though the borrower (and not the lender) holds title to those securities during the term of the loan.

The Staff reasoned that: “[t]he Reporting Manager still has investment discretion over the loaned securities because he has the authority to sell the loaned securities, even though such transactions typically may not be consummated until the conclusion of the loan. In addition, the non-reporting of the loaned securities could render the data base created by Form 13F filings incomplete and therefore unsuitable for analyses of trading activities of Reporting Managers…. If Reporting Managers do not report loaned securities, it would be difficult to analyze the data of different reporting periods of a given Reporting Manager because no one will be able to determine whether the difference in holdings is caused by the lending of securities or the purchase or sale of securities. Thus, for example, one could improperly infer greater trading activity by a Reporting Manager when in actuality the Manager only lent securities. … Finally, if institutional investment managers are not required to report loaned securities, they could avoid the reporting requirements of Rule 13f-1 by lending enough securities on the last trading day of each month to bring the total amount of investments they manage under $100 million.”

However, other transactions that result in an institutional investment manager having economic exposure to a 13F security without directly holding that security are not addressed. For example, an institution that holds the long position in a physically-settled total return swap that references a 13F security is in an economic position similar to that of a securities lender—it remains economically exposed to the security, has a right to obtain the security at maturity of the transaction and does not currently have title to the security. If an institutional investment manager was not required to report the position held through that total return swap, on maturity of the total return swap, it would report an increase in its position in the relevant 13F security even though it may

have acquired economic exposure to that position in a prior period—giving an inaccurate view of its trading activities. Similarly, it could use total return swaps or similar instruments to avoid 13F reporting requirements.

The Society believes that the SEC should clarify the treatment of derivative securities under Section 13(f), making clear that positions that are substantially equivalent economically to direct ownership of a 13F security should be reported. Equally importantly, the Society believes that the SEC should generally provide detailed guidance as to the treatment of derivative securities under the 13F reporting regime to ensure that all market participants are reporting on a like basis and that reports can be accurately interpreted. Additionally, the current 13F reporting regime does not present a full picture of the trading activities of institutional investment managers because it does not require disclosure of short positions. Reporting of short positions would provide substantial value to issuers by allowing them to better identify holders that have a significant economic position in the company—facilitating their ability to identify persons with whom the issuers should communicate and engage. The Society believes that institutional investment managers often utilize short positions as part of their investment strategy, both for hedging and speculative purposes. It is difficult to see how Form 13F can serve its primary goals—“[f]irst, to create a central repository of historical and current data about the investment activities of institutional investment managers. Second, to improve the body of factual data available regarding the holdings of institutional investment managers and thus facilitate consideration of the influence and impact of institutional investment managers on the securities markets and the public policy implications of that influence. Third, to increase investor confidence in the integrity of the U.S. securities markets”—while requiring reporting that distorts the economic position and trading activities by institutional investment managers by excluding short positions.

The Society believes that institutional investment managers track their short positions on a daily basis, if not more frequently, and that the incremental burden of including those positions on a Form 13F together with long positions would be minimal. To the extent that specific short positions give rise to material concerns regarding front running or copycatting, those concerns are better addressed through the SEC’s process for confidential treatment requests than a blanket exclusion of those positions from public reporting.

* * *

We appreciate the opportunity to provide comments on this proposal. We would be happy to provide you with further information to the extent you would find it useful.

The complete publication, including footnotes, is available here.

Reporting Threshold for Institutional Investment Managers

More from: Granville Martin, Society for Corporate Governance

Granville J. Martin is General Counsel at the Society for Corporate Governance. This post is based on a comment letter by the Society for Corporate Governance to the U.S. Securities and Exchange Commission. Related research from the Program on Corporate Governance includes The Law and Economics of Blockholder Disclosure by Lucian Bebchuk and Robert J. Jackson Jr. (discussed on the Forum here).

The Society for Corporate Governance (the “Society” or “we”) appreciates the opportunity to provide comments to the U.S. Securities and Exchange Commission (the “SEC” or the “Commission”) on the proposed changes to the reporting threshold for Form 13F reports by institutional investment managers (the “Proposed Rules”). We respectfully submit this letter in opposition to the Proposed Rules.

Founded in 1946, the Society is a professional membership association of more than 3,500 corporate and assistant secretaries, in-house counsel, outside counsel, and other governance professionals who serve approximately 1,600 entities, including 1,000 public companies of almost every size and industry. Society members are responsible for supporting the work of corporate boards of directors and the executive managements of their companies on corporate governance and disclosure matters.

I. Introduction

Congress enacted Section 13(f) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), to increase the public availability of information regarding the securities ownership of institutional investors and to increase investor confidence in U.S. securities markets. When the final rules relating to the filing and reporting requirements of institutional investment managers were announced in 1979, the SEC made clear that “[t]he reporting system required by Section 13(f) is intended to create in the Commission a central repository of historical and current data about the investment activities of institutional investment managers, in order to improve the body of factual data available and to facilitate the consideration of the influence and impact of institutional investment managers on the securities markets and the public policy implications of that influence.” Accordingly, as the SEC has recognized, the goals of the Section 13(f) disclosure program are to (i) aggregate data in respect of the investment activities of institutional investment managers, (ii) improve public insight into the holdings of institutional investment managers in order to facilitate the assessment of such managers’ impact on the securities markets, and (iii) increase investor confidence in the integrity of the U.S. securities markets.

In significant part because of public companies’ limited visibility to their shareholders’ identities, Form 13F filings today make up the primary data input for their “shareholder lists.” These disclosures are a primary source for market participants to understand the ownership profile of an issuer’s securities and, in the view of the Society’s membership, are essential to the functioning, growth, and clarity of the U.S. securities markets.

The Proposed Rules would undermine the express purposes of Section 13(f), run contrary to the Commission’s stated objectives with respect to regulating the securities markets, and harm investors, issuers, regulators, and academics alike. In particular, the Proposed Rules would substantially reduce market visibility into public company holdings—a burden that will be borne by issuers of all sizes and that would have the perverse effect of privileging the voices and influence of the already large, growing, and further concentrating index funds and larger asset managers at the expense of smaller institutional investors. In addition, the Proposed Rule’s massive reduction in 13F data will—in the context of the significant increase in investor activism since Section 13(f)’s enactment— dramatically reduce confidence in the integrity of U.S. markets. Accordingly, we respectfully submit this letter in opposition to the Proposed Rules.

Nonetheless, we support the Commission’s goals of modernizing the information reported on Form 13F and increasing the information provided by institutional investment managers. To that end, in connection with a broader overhaul of the shareholder reporting framework, we would be supportive of an increase to the Section 13(f) reporting threshold from $100 million to $450 million to reflect a consumer price inflation adjustment from 1976 to 2019, as previously considered by the Commission and proposed by another commentator. However, the Society believes the SEC should only revise the current 13F reporting threshold as part of a comprehensive modernization of shareholder reporting. As part of such a comprehensive modernization exercise, the Society reiterates its belief that it would be appropriate for the SEC to shorten the quarterly reporting deadline for 13F filings to two business days after the end of the calendar quarter.

This letter proceeds as follows. Section II outlines how the Proposed Rules would significantly reduce market transparency, materially reduce shareholder engagement, hamper capital formation, increase the costs of shareholder activism, and conflict with the policy rationale underlying Section 13(f). Section III provides a cost-benefit analysis, demonstrating that any potential cost savings as a result of the Proposed Rules is more than outweighed by the substantial costs resulting from the decline in market transparency. Section IV outlines the Society’s alternative to the modernization of Form 13F reporting regime, proposing to increase the existing threshold to $450 million and reducing the reporting period to two business days, as part of a comprehensive modernization of Section 13 shareholder reporting.

II. Loss of Transparency

In 1971, the SEC released the Institutional Investor Study Report that was commissioned by Congress three years prior (the “Institutional Investor Report”). There, the Commission recognized that “[t]he importance of a regularized, uniform and comprehensive, scheme of institutional reporting cannot be minimized in light of the demonstrated growth of institutional investment and its impacts on the structure of securities markets, corporate issuers and individual investors.” Accordingly, the SEC concluded in the Institutional Investor Report that “gaps in information about the purchase, sale and holdings of securities by major classes of institutional investors should be eliminated” and recommended that the Commission be granted the “general authority to require reports and disclosures of such holdings and transactions from all types of institutional investors.”

As currently contemplated, the Proposed Rules would eliminate access to information about discretionary accounts managed by more than 4,500 institutional investment managers, representing approximately $2.3 trillion in assets. This means that nearly 90% of institutional investment managers would be relieved from reporting on Form 13F.

In other words, increasing the reporting threshold to $3.5 billion and eliminating the Form 13F filing requirement for nearly 90% of filers widens—not closes—the very same gaps that the SEC was concerned with in the 1970s. Accordingly, the Society expects that the Proposed Rules would materially reduce the ability of issuers to satisfy investors’ increasing demand for engagement and would complicate the ability of all issuers (but particularly smaller issuers) to access working capital. Implementation of the Proposed Rules would also eliminate disclosure by the vast majority of activist investors of positions below 5%, potentially resulting in an increase in stealth shareholder activist activity and value destruction for both issuers and activist investors.

Market Change Has Reduced Transparency Under Existing 13F Regime

In 1978, when Form 13F was adopted, the distribution of market capitalizations among public companies was more uniform than it is today. In the current market, valuations are markedly more concentrated, with the top five publicly traded U.S. companies constituting approximately 23.1% of the S&P 500. The shareholder bases of larger issuers are also typically dominated by larger investors that accumulate sizable positions in such issuers. In 2020, the “big three” index funds, BlackRock, Vanguard, and State Street, controlled approximately 20% of the S&P 500, representing a radical departure from the historically dispersed ownership of the U.S. stock market.

As demonstrated in Table 1 below, market changes over the past 42 years have led to an outdated disclosure regime under Section 13(f). For example, smaller issuers with market capitalizations of up to $250 million have relatively poor visibility into their shareholder base under the existing 13(f) regime: only 36.7% of their shares outstanding (on average) are reported on Form 13F. On the other hand, mid-and large-capitalization issuers have greater visibility today: over 80% of their shares outstanding (on average) are reported on Form 13F.

Table 1 (Source: Innisfree M&A Incorporated, as of August 18, 2020)

Impact of the Proposed Rules

Under the Proposed Rules, the gap in visibility into the shareholder bases of large- versus small-capitalization issuers is likely to widen substantially. As demonstrated in Table 2 below, issuers with market capitalizations below $250 million would lose visibility into approximately 38.9% of their shares outstanding (on average), while issuers with market capitalizations of $10 billion or greater would lose visibility into approximately 7.4% of their shares outstanding (on average). The Society is also aware of members representing larger issuers who expect substantially greater reductions in transparency with respect to their shares outstanding than the average reported in the Survey.

Table 2 (Source: Innisfree M&A Incorporated, as of August 18, 2020)

The Proposed Rules would also have a differential effect on issuers by market capitalization with respect to each issuer’s visibility in the number of filers of Form 13Fs holding its stock. As demonstrated in Table 3 below, issuers with market capitalizations of $10 billion or greater would lose visibility into approximately 55.4% of their filers (on average), while issuers with market capitalizations below $250 million would lose visibility into approximately 27.9% of their filers (on average). In other words, although smaller issuers would lose visibility into substantially more shares than larger issuers under the Proposed Rules, the larger issuers are expected to lose visibility into substantially more filers than smaller issuers. The Society expects the impact of these changes to significantly affect the ability of issuers across all market capitalizations to identify and engage with their shareholders. Even if those smaller investors who will no longer be visible to issuers only hold a small percentage of an issuer’s shares outstanding, such investors may still have a significant influence on issuers (e.g., hedge funds and activists). Moreover, the net effect of privileging the voices of larger investors over smaller investors is antithetical to the Commission’s mission and to the preferences of issuer and the investment community.

Table 3 (Source: Innisfree M&A Incorporated, as of August 18, 2020)

As discussed in Section IV, the Society believes that increasing the existing threshold to $450 million would have a less harmful effect on issuers across all market capitalizations, while still advancing the Commission’s goals of modernizing the information reported on Form 13F and increasing the information provided by institutional investment managers.

Impact of the Proposed Rules on Shareholder Engagement

As Chairman Clayton has noted, “[s]hareholder engagement is a hallmark of our public capital markets” and one of the “key principles” of our securities laws. Further to such suggestions, the Commission has, in recent years, taken steps to enhance shareholder engagement in the corporate governance of public companies and attempted to modernize SEC rules around such engagement. The Society fears that the Proposed Rules would lead to a stark regression in shareholder engagement.

Since the adoption of Section 13(f) more than 40 years ago, there has been a meaningful increase in shareholder engagement by issuers, including engagement with respect to long-term strategy, M&A, environmental, social, corporate governance and other matters, establishing a foundation for communications with shareholders and increasing shareholder confidence. To that end, issuers commonly hire and retain investor relations professionals to ensure that the concerns of investors are heard, conveyed to management, and acted on.

According to a survey of 157 issuers conducted by the Society in September 2020 (the “Survey”), approximately 94% of the respondents stated they use Form 13F to identify institutional ownership, approximately 89% of the respondents stated they use Form 13F to monitor accumulations of holdings, and approximately 68% of the respondents stated they use Form 13F to identify, prepare and respond to activist attacks. In response to the Survey’s question regarding how the issuer monitors investor movements in the issuer’s stock, approximately 14% of the respondents stated they use Form 13F reports, approximately 10% of the respondents stated that they use either a stock surveillance program or a stock watch firm (who in turn use Form 13F reports), and approximately 75% of the respondents stated they use a combination of Form 13F reports and stock watch. In the absence of comprehensive Form 13F data, the members of the Society fear that they would be left without an adequate source to track their shareholders, especially if they may not be able to afford costly stock surveillance programs to assist in the verification of investor ownership. Even if they could afford stock surveillance programs, or are currently using such programs, all stock surveillance programs rely on the disclosures provided on Form 13F to form the initial basis of their analysis. Accordingly, the Proposed Rules would render stock surveillance services substantially less effective. Further, the inability of issuers to identify their investors by relying on the quarterly ownership information set forth in Form 13F filings is particularly problematic in light of misrepresentation by investors of their positions in issuers. According to the Survey, approximately 15% of the respondents stated they have experienced misrepresentation by investors of their holdings while seeking engagement with issuers’ management or board of directors.

As general counsel, corporate secretaries, and other governance professionals, the Society’s members are frequently tasked with managing their company’s shareholder meeting processes, including facilitating the exercise of shareholder voting rights, and spearheading shareholder engagement efforts. According to the Survey, approximately 86% of the respondents stated that they are using Form 13F reports in formulating their shareholder engagement strategy and meetings, and virtually all (98%) of the respondents stated that the Proposed Rules do not facilitate shareholder engagement. Moreover, given the loss of visibility into the shareholder bases of issuers across all market capitalizations, compliance, monitoring and shareholder engagement costs are likely to increase substantially.

The Proposed Rules would make effective and efficient interactions between issuers and investors much more difficult. As detailed above, increasing the reporting threshold for institutional investment managers from $100 million to $3.5 billion would reduce issuers’ insight into their investor base, making it more difficult to discern the appropriate amount of time and resources necessary for direct engagement with shareholders that have requested to speak with management and/or board of directors. According to the Survey, approximately 67% of the respondents stated that they believe the Proposed Rules would result in a decrease in engagement with investors with less than $3.5 billion assets under management. Additionally, such limited insight would potentially make it more difficult for issuers’ boards of directors to ascertain to whom (and to what type of investors) they owe their fiduciary duties. Further, another likely result of the reduced insight is that large institutional investors (i.e., those that will continue to provide Form 13F disclosure) will be further prioritized and therefore exert even greater influence over issuers at the expense of smaller investors, a result both contrary to the Commission’s efforts to improve participation in corporate processes by smaller investors and detrimental to the securities markets as a whole.

Negative Impact on Capital Formation

As issuers and academics have noted, the Proposed Rules’ attempt at preventing front running and copycatting comes at the cost of significant “market opacity,” which, in turn, results in a reduction in capital formation. On the one hand, Form 13F data is essential to the ability of issuers to identify potential investors and attract new long-term investments necessary for growth. The opaqueness of an issuer’s investor base will likely cloud fundraising activities, as certain issuers will suffer from an inability to pinpoint new capital sources (e.g., investors that have made investments in the issuer’s industry) and monitor the efficacy of certain interactions with prospective shareholders. This is especially true for newly public issuers who may regularly access the securities market. Such issuers rely on information from Form 13F to monitor their shareholder base and engage with potential investors on an ongoing basis. This engagement is critical, as equity offerings are typically conducted with only one or two days of public marketing. With the adoption of Rule 163B, which allows “testing-the-waters” for all issuers, the SEC has validated the need for such engagement. On the other hand, the visibility provided by Form 13F disclosures encourages investments from smaller investors (i.e., through the assessment of crowdedness of trades). The Proposed Rules, and the attendant loss of visibility, introduce uncertainty for investors, potentially yielding fewer investments that facilitate capital formation and growth for issuers and making the securities offering process disproportionately burdensome for all issuers.

Promotion of Activist Activity

Increasing the ownership threshold from $100 million to $3.5 billion would result in many of the most influential activist hedge funds no longer filing Form 13F reports altogether. In the wake of the Proposed Rules, out of a total of 123 activist hedge funds that are currently required to file, only 25 (20%) would continue reporting on Form 13F. That is, other than the largest activists (e.g., Carl Icahn, Elliott Management, and Third Point), even prolific and vocal activists, such as Starboard Value, JANA Partners, Greenlight Capital, Engaged Capital, Land and Buildings, and Marcato, would generally not be required to disclose their sub-5% positions on a quarterly basis on Form 13F.

Eliminating Form 13F disclosure for most activist investors will affect issuers across all market capitalizations but will have an especially significant impact on smaller issuers, which are already more vulnerable to activism and hostile takeover activity than their larger peers. As shown in Table 4 below, under the current $100 million reporting threshold, activists hold a combined value of $64.2 billion worth of stock in small-capitalization issuers. As a result of the Proposed Rules, activists will continue reporting only $32.6 billion worth of stock in small-capitalization issuers. In other words, roughly 50% of activist equity holdings ($31.6 billion worth of stock) in smaller issuers would “go dark”.

To compare, as a result of the Proposed Rules, mid-and large-capitalizations issuers would lose visibility of 28% and 12%, respectively, of activists’ positions.

Table 4 (Source: Innisfree M&A Incorporated, as of August 30, 2020)

As a result of reduced disclosure by activist investors, issuers will no longer have key existing tools to identify, monitor, and prepare themselves for activist campaigns that frequently seek to influence the management, control, and boards of directors of issuers. In recent years, shareholder activists have become more numerous and diverse than they were in the past, both in their agendas and their methods. While in the 1980s corporate control and takeovers were activists’ primary goals, today’s shareholder activism is more focused on attempting to manufacture short-term value without a change in control, and doing so by leveraging a small ownership percentage, often no more than three to five percent. These changes in activism trends have led issuers’ boards of directors, together with management, to engage with shareholder activists proactively. The Proposed Rules will inhibit the ability of issuers, particularly smaller issuers, to effectively prepare for, identify, and respond to activist attacks, potentially facilitating the short-term investment objectives of a small subset of investors at the expense of the broader shareholder base.

Additionally, the inability to identify activist investors is likely to increase the cost of shareholder activism activity for both issuers and investors while simultaneously reducing trust and transparency between them. Activists and issuers frequently reach settlements on the basis of an implicit understanding of how shareholders are likely to vote on a given issue, thereby negating the necessity of prolonged and expensive shareholder solicitation processes. Table 5 below shows the total number of proxy fights against U.S. issuers (across market capitalizations) between the years 2016 and 2020 (YTD) and the percentage of reported settlements reached in each of these years out of the total number of proxy fights. On average, the percentage of settlements across all issuer market capitalizations was approximately 32 percent between the years 2016 and 2020 (YTD), with a higher percentage of settlements occurring at small- and mid-capitalization issuers. The Proposed Rules would make settlements and other informal, non-public discussions (such as “quiet” campaigns where an activist engages with the issuer behind the scenes) with activists significantly more challenging because it would be more difficult to gauge investor sentiment, predict shareholder voting outcomes, and quantify the value of preempting proxy contests.

Table 5 (Source: FactSet, as of September 13, 2020)

III. The SEC’s Cost Benefit Analysis is Incomplete and Warrants Reconsideration

Purported Savings Do Not Justify The Reduction In Transparency

We believe that the Commission’s economic analysis related to these proposed amendments requires further study by the Commission of the cost and benefit impacts on market participants, including public company issuers represented by the Society. Particularly, while we believe there are opportunities to improve the timeliness and transparency of this data, further economic analysis by the Commission of the substantial costs of the lost transparency of 13F data on public company issuers is needed, as the 13F filings remain the only publicly-available source for public companies for quarterly data on the “street name” investors who are buying or selling their shares.

As mentioned above, the Society’s members heavily rely on 13F data to make determinations regarding capital formation activities and shareholder engagement strategies, including increasing their understanding as to whether shareholders are invested in them for the long-term. While the Commission’s economic analysis stresses the availability of other data sources, such as the Schedules 13D and 13G, and the Form N-PORT, these reports are not adequate substitutes, as Schedules 13D and 13G only become applicable if a person acquires beneficial ownership of 5 percent or more of an issuer’s outstanding shares. Likewise, Form N-PORT data is only publicly available on a delayed basis and is limited to registered management investment companies, which are more likely to be the largest firms, which would continue to be identified through 13F filings and Schedules 13D and 13G.

Therefore, without the 13F reports, Society members would be limited in tracking ownership changes or verifying how much of their respective stock is owned by investors who may refuse to disclose their stakes—even after those investor reach out to issuers, request meetings with issuer management, or launch activist campaigns against issuers. However, the Commission’s proposal does not provide a more specific analysis of the value of this lost transparency.

Without access to 13F data, the Society’s members, as discussed above, would need to further rely on stock surveillance firms for capital formation activities and shareholder engagement. In 2016, Bloomberg estimated the annual cost of stock surveillance was $25,000 to $50,000 and in the experience of the Society’s members these annual costs are currently far higher and potentially prohibitive for smaller issuers. With the competitive force of freely available 13F data removed, stock surveillance firms would likely be able to charge more for their services (even as the services would become less effective due to the absence of this 13F data) and become more cost prohibitive for smaller issuers.

In addition, the Society believes further study by the Commission is required on the cost consequences to issuers and shareholders on capital formation activities and reduced and less effective shareholder engagement. As discussed above, less engagement would ultimately lead to more proxy contests and less effective engagement processes with respect to activists’ campaigns and shareholders generally. Activist campaigns are costly for management, both in direct expenses and in the significant time and attention diverted from running the business. The Society believes ongoing shareholder engagement and bringing activists shareholders and issuers together to the negotiating table sooner allows public company issuers to achieve better outcomes for shareholders overall, including through negotiated settlements and costs avoided. The data provided by 13F filings is a key tool for issuers to continue positive engagement strategies that allow them the opportunity to proactively avoid these costs and achieve negotiated outcomes that benefit its shareholders at large.

The expenses of responding to activists’ campaigns are substantial to the Society members and ultimately are passed through to shareholders. A 2014 study found that a contested activist campaign costs a company between $10 million and $20 million—plus weeks of management time to develop plans and meet with investors. Furthermore, Society members are more frequently being asked for reimbursements of expenses from activists’ campaigns with U.S. public company issuers spending an average $431,831 to cover activists’ campaigning costs in 2018. Without 13F data, the Society would expect that these costs would grow significantly as public company issuers would have less information to create proactive engagement strategies that can avoid distracting protracted activist campaigns and proxy contests and would experience substantially increased costs in identifying investors through such campaigns. Analysis on the potential increase in these costs, which are already substantial for public company issuers, along with the negative impact on capital formation, is absent from the Commission’s current analysis and merits further consideration.

IV. 13F Changes To Be Considered As Part of a Comprehensive Modernization of Shareholder Reporting

The Society welcomes the SEC’s efforts to modernize the reporting regime applicable to institutional investment managers but does not believe modernization can be accomplished in a piecemeal fashion. The Society believes that efforts to modernize the Form 13F reporting regime should only be made in a holistic manner as part of a comprehensive modernization of shareholder reporting. Such a holistic approach would update the regime to provide for more current information, reflect the reality of modern investment practices so that reports do not present a distorted and inaccurate view of investment activities and, because those reforms could impose some incremental costs on institutional investment managers, the Society would support an increase in the threshold for Form 13F reporting to $450 million to reduce burdens on smaller managers.

New $450 million Threshold

The Society appreciates that the reporting threshold for Section 13(f) has not been increased since it was first implemented and that the reforms discussed below would impose some incremental costs on some institutional investment managers. As a result, if the SEC is amenable to modernizing Form 13F holistically, the Society would be supportive of a modest increase in the 13F reporting threshold. However, for the reasons noted above, any small cost savings that might be realized by some incremental investment managers by increasing the reporting threshold from $100 million to $3.5 billion are wildly disproportionate to the substantial deleterious effects of the Proposed Rules. As an alternative to such a dramatic increase in the reporting threshold and associated reduction in information made available to the public, issuers, and the SEC, the Society believes that an increase of the threshold to $450 million, reflecting inflation, would have a less harmful effect on issuers across all market capitalizations.

As demonstrated in Table 6 below, under the proposed $450 million threshold, issuers with market capitalizations below $250 million would lose visibility into approximately 15.4% of their shares outstanding (on average) (versus a loss of approximately 38.9% under the Proposed Rules), while issuers with market capitalizations of $10 billion or greater would lose visibility into approximately 1.4% of their shares outstanding (on average) (versus a loss of approximately 7.4% under the Proposed Rules). Additionally, as demonstrated in Table 7 below, under the proposed $450 million threshold, issuers with market capitalizations of $10 billion or greater would lose visibility into approximately 20.8% of their filers (on average) (versus a loss of approximately 55.4% under the Proposed Rules) and issuers with market capitalizations below

$250 million would lose visibility into approximately 5.7% of their filers (on average) (versus a loss of approximately 27.9% under the Proposed Rules).

Table 6 (Source: Innisfree M&A Incorporated, as of August 18, 2020)

Table 7 (Source: Innisfree M&A Incorporated, as of August 18, 2020)

Further, under the proposed $450 million threshold, issuers across all market capitalizations would lose visibility into approximately 7.5% of their shares outstanding (on average) (versus a loss of approximately 22.3% under the Proposed Rules). Additionally, issuers across all market capitalizations would lose visibility into approximately 10.5% of their filers (on average) (versus a loss of approximately 36% under the Proposed Rules). To that end, the Society believes that a proportional increase of the existing threshold to $450 million would have a less harmful effect on issuers across all market capitalizations by allowing them to maintain greater visibility into their shareholder bases as well as to identify their investors, while still advancing the Commission’s goals of modernizing the information reported on Form 13F and increasing the information provided by institutional investment managers. This approach would be consistent with the recommendation of the SEC’s Office of Inspector General (the “OIG”).

Reduce Reporting Period to Two Business Days

The Society believes reducing the significant lag between the date triggering Form 13F disclosure and the filing date would provide substantial benefits to issuers and the market as a whole, while imposing only limited additional costs on institutional investment managers. Currently, the Form 13F reporting regime can allow for over a year—up to 382 days—between when an institutional investment manager first becomes subject to the requirement to file Form 13F and when that manager’s first filing is due. That first report would include information as of the end of the fourth calendar quarter of the year during which the institutional investment manager crosses the filing threshold and be filed 45 days after that quarter end. Subsequent reports are due 45 days after the end of each calendar quarter and present information as of the end of that calendar quarter.

The six-and-a-half weeks between quarter end, the time as of which a Form 13F presents information, and the date a Form 13F is required to be filed has long been the subject of criticism. In 2013, the Society, together with NYSE Euronext and the National Investor Relations Institute, petitioned the SEC to reduce the reporting deadline to two business days after the end of the calendar quarter. The Society continues to believe that a shorter reporting cycle is appropriate. As noted in its 2013 petition, the month-and-a-half-long gap between the date of the information and when it is published inhibits the ability of issuers to identify, communicate with and engage with their shareholders in real time and results in outdated information being provided to the market and the SEC. The Society believes that institutional investment managers track their portfolios on a daily, if not more frequent, basis, and would be able to produce the limited information—consisting primarily of a list of holdings and their value—required by Section 13(f), within two business days of a reporting date without undue hardship, especially because the date as of which the information need be presented and the date on which it would be required to be filed would be set by regulation and known in advance.

Similarly, current technology allows the period of time between when an institutional investment manager becomes subject to reporting under Section 13(f) and the first reporting deadline to be substantially shortened. While the Society acknowledges that the filing of an initial Form 13F may require more effort than subsequent filings, we believe it is appropriate to require an institutional investment manager to file a Form 13F with information as of the end of quarter subsequent to the quarter during which that manager crosses the Section 13(f) threshold (e.g., if a manager crosses the threshold on January 2, its first filing would include information as of June 30 and be filed in early July) and that such period should provide adequate time to prepare that filing.

In 1979, the SEC focused on the following benefit to justify changing Form 13F filing obligations from annual to quarterly: “Both corporations and financial reporting services asserted that quarterly reporting is needed to provide corporate treasurers with current information concerning institutions owning their stock. They pointed out that many stockholders take ownership in nominee or street name, making it difficult to trace such information and making it difficult to secure proxies on important corporate matters.” That remains at least as relevant—if not more relevant—today as it was in 1979 given the massive increase in beneficial ownership of equity securities.