Print

PrintMelissa Sawyer and Marc Treviño are partners, and Lauren Boehmke is an associate at Sullivan & Cromwell LLP. This post is based on a Sullivan & Cromwell memorandum by Ms. Sawyer, Mr. Treviño, Ms. Boehmke, and Nathan Ludewig. Related research from the Program on Corporate Governance includes The Long-Term Effects of Hedge Fund Activism by Lucian Bebchuk, Alon Brav, and Wei Jiang (discussed on the Forum here); Dancing with Activists by Lucian Bebchuk, Alon Brav, Wei Jiang, and Thomas Keusch (discussed on the Forum here); and Who Bleeds When the Wolves Bite? A Flesh-and-Blood Perspective on Hedge Fund Activism and Our Strange Corporate Governance System by Leo E. Strine, Jr. (discussed on the Forum here).

A. Pandemic’s Impact On Activism Strategies And Responses

Shifting Focus of Activism Campaigns

The impact of the COVID-19 pandemic on U.S. businesses has extended to shareholder activism—not only have activism levels decreased so far this year, but the strategies deployed by activists, and the ways issuers respond to these strategies, have also changed. After several years of activists focusing on M&A theses, this year we have observed activists shifting their focus towards board change, operational improvements and management change in higher proportions than previous years.

According to Lazard, 34% of global activism campaigns launched during the first half of this year had M&A objectives, compared to approximately 47% of campaigns last year. Almost one-third of the M&A-focused campaigns were initiated prior to the onset of the pandemic in March. In addition, a number of activist-initiated sale processes were delayed by the pandemic. Interestingly, one of the few big ticket M&A deals that signed in the first half of this year, Chevron’s $5 billion acquisition of Noble Energy, drew Elliott’s attention; in September, Elliott revealed a stake in Noble and unsuccessfully encouraged the company’s stockholders to vote against the transaction.

Anecdotally, we have also observed fewer instances of activists urging issuers to explore stock buybacks so far this year. This is likely because fewer issuers have excess cash to use for buybacks, and those issuers that do have excess cash are focused on conserving liquidity in order to manage the uncertainty caused by the pandemic. In fact, one high-profile campaign this year took the opposite approach, with Dan Loeb urging Disney to end its $3 billion annual dividend and invest in its streaming business. Buybacks have become the subject of criticism in the political arena, with members of both major political parties supporting limits on buybacks and the Federal Reserve imposing prohibitions on share buybacks for the largest banks through the end of 2020.

In place of M&A objectives and buybacks, activists increasingly turned their focus to board change (34% of campaigns), operational improvements (20%) and management change (7%) through the first half of this year as compared to prior years. Notable examples include Starboard’s successful proxy contest at chemical company GCP Applied Technologies for eight board seats, Ancora and Macellum’s push for retailer Big Lots to refresh its board and Elliott’s campaign for Twitter to replace CEO Jack Dorsey. Of course, campaigns focused on board change typically also have underlying objectives aside from board refreshment—for example, Starboard’s above-mentioned campaign to replace the GCP board of directors was aimed at driving operational, strategic and financial improvements.

Breaking with the trends observed during the first half of 2020, there was a shift back towards M&A objectives in the third-quarter of this year as deal volume also increased. This trend is likely to continue if M&A activity levels stay elevated through the end of 2020 and into 2021.

Return of the Rights Plan Defense

The onset of the pandemic also led some issuers to shift their strategies in responding to activism, albeit by returning to a familiar tactic. Shareholder rights plans, commonly known as poison pills, were briefly back in vogue this year as a number of issuers felt more susceptible to takeovers and activism due to pandemic-related stock price drops and volatility. Rights plans are a tool used by issuers since the 1980s to prevent stock accumulations above a stated threshold by diluting the acquiring shareholder. In the activism context, rights plans may give a board time to react in the face of potential activist approaches, stop the activist from accumulating a bigger stake, and discourage coordination among shareholders that might trigger the rights or discourage an opportunistic bidder from launching a hostile takeover in the midst of the disruption caused by the activist’s campaign. However, a rights plan will not prevent an activist from launching an activism campaign or running a proxy contest (and then potentially eliminating the rights plan after taking control of a majority of the board).

In recent years, there have been some instances in which issuers have adopted rights plans in response to an actual or perceived activism threat. From 2017 – 2019, we observed at least 26 instances of issuers explicitly adopting rights plans in such circumstances. Many more companies prepared “shelf ” rights plans behind the scenes prior to and during this period, readying the documentation and educating the board on rights plans proactively so that a rights plan could be implemented on short notice if deemed advisable by the board.

This year, rights plans have been adopted in much higher numbers than prior years—including 17 plans in March alone and a total of 60 plans through August. Notably, a number of 2020 rights plans have been adopted prophylactically, or without any disclosed threat by an activist or hostile acquiror. The terms of the rights plans adopted this year generally track market practice for rights plans in prior years, with many of the rights plans having one-year terms and not requiring shareholder approval, consistent with proxy advisor guidance. These plans typically had ownership thresholds of 10% to 15%. Notably, however, according to data from the Council of Institutional Investors, seven rights plans adopted this year had a 5% ownership threshold (not including Net Operating Loss-focused plans). The Williams Companies’ 5% rights plan is currently the subject of litigation in the Delaware Chancery Court focused on its low threshold, which is discussed in more detail below.

In the event there is another increase in market volatility due to health, economic, political or other conditions, additional issuers may wish to consider adopting rights plans. In addition, current issuers may consider whether it is in their shareholders’ best interests to adopt a second rights plan or extend the terms of their existing rights plans. In such case, it will be interesting to see whether proxy advisor guidance shifts to tolerate, in these circumstances, issuers maintaining rights plans beyond a one-year period without a shareholder vote.

B. Blurring Lines Between Activists and Other Investors

Recently, we have begun to observe a convergence of private equity and activism strategies as private equity funds and activist hedge funds have become increasingly willing to borrow from each other’s playbooks. On the private equity side, this is taking the form of sponsors making minority investments in public companies with the intention of engaging with management (rather than acquiring control). For example, in January, KKR announced a minority stake in entertainment and dining chain Dave & Busters. KKR has not expressed any interest in acquiring control of Dave & Busters; instead, it has stated that its intention is to engage constructively with Dave & Busters’ management team. In May, Dave & Busters agreed to add a KKR executive to its board.

Some private equity funds have even shown that they are willing to go hostile. In June, Cerberus launched a campaign at German bank Commerzbank, sending a letter to the bank’s Chairman criticizing the board and management team and demanding two board seats. In January, middle market private equity funds Atlas Holdings and Blue Wolf Capital launched a proxy contest against paper producer Verso Corporation, which ultimately ended in a settlement. It is worth noting, however, that while private equity funds have adopted activist strategies, private equity funds are typically careful not to launch fully hostile campaigns—in fact, some fund documents prohibit hostile activities.

On the activist side, activist investors are also adopting traditional private equity strategies such as full company acquisitions, private investments in public equity (PIPEs) and forming special purpose acquisition companies (SPACs). Elliott has perhaps been the most publicly active on the M&A and PIPE fronts, through its private equity arm, Evergreen Coast Capital, although other activists are beginning to join in these approaches as well. In November, Elliott made a proposal to acquire specialty foods company Aryzta and, in September, Elliott revealed a 15% stake in transportation and defense services company Cubic and said it was partnering with private equity fund Veritas Capital in a bid for the company. This follows a busy 2019, in which Elliott teamed up with Francisco Partners to acquire technology company LogMeIn for $4.3 billion in December and also agreed to take retailer Barnes & Noble private earlier in the year. More recently, as M&A activity slowed in the spring and early summer of this year, activists joined private equity funds in making PIPE investments to provide issuers with much needed liquidity. For example, in May, Elliott teamed up with Fidelity and Bluescape to invest $1.4 billion in utility CenterPoint Energy. ValueAct has invested at least $119 million in PIPEs in recent years and, in February 2019, Starboard announced a $200 million investment in restaurant chain Papa John’s. Activists are also experimenting with SPAC investment strategies. In January, Far Point, a SPAC formed by Third Point, agreed to acquire Swiss payments company Global Blue from Silver Lake. In August, Starboard announced the launch of its own SPAC, Starboard Value Acquisition Corp.

This blending of investment strategies has not been limited to activists and private equity funds; we have also observed other historically non-activist investors adopting more activist-like strategies, including active managers, shareholder proposal proponents and even institutional investors. Most notably on the active management front, last year, Neuberger Berman launched a proxy contest against software company Verint Systems, seeking to replace three directors over concerns about the company’s capital allocation strategy and governance practices. Further, in June of this year, Trillium Asset Management, a frequent proponent of ESP-focused shareholder proposals, issued a press release criticizing business process service provider Conduent’s management team and urging the company to separate its three businesses. Trillium’s M&A thesis stands in stark contrast to its historic strategies and is more in line with what would be expected from an activist hedge fund. Lastly, on the institutional investor side, in May, Vanguard issued its first-ever company-specific report, offering analysis on its decision to vote against a Boeing director and in support of a shareholder proposal at the company. A Vanguard spokesperson later stated that its future reports will not always be company-specific.

These recent entries into activist-like strategies suggest that companies would be wise to stay up-to-date on all their significant shareholders, regardless of investment strategy. As for the activists, their recent forays into private equity-like and SPAC strategies are in many ways a natural progression. As issuers increasingly address their vulnerabilities proactively, there are fewer ill-prepared companies to target. This leaves activists, who have accumulated significant amounts of capital, in need of alternate methods for putting their capital to work. It is no surprise then that investors who are already focused on identifying companies’ weaknesses and finding ways to capitalize on them would take to private equity models. One way for an activist to implement changes and potentially unlock value in a company is to buy it outright.

C. Integrating ESP and Activism

ESP themes have increasingly come to the forefront of shareholder discourse over the past several years, moving from discrete proposals by a small number of “socially conscious” organizations into corporate disclosures, legislation and regulations. Recently, the largest institutional investors and a number of business leaders reaffirmed this trend with statements that they will be intensely focused on issuers’ “purpose,” how corporations treat all their stakeholders (in addition to shareholders) and similar concepts. ESP themes have remained prevalent this year in the context of the pandemic, economic recession and racial justice initiatives, as well as climate change.

Given the growth of the largest index funds over the past few years, winning the support of these funds is crucial in almost every activism situation. Accordingly, many anticipated that activists would begin to reference ESP themes in order to attract support from institutions like BlackRock, Vanguard and State Street. This year, we began to see this become an observable trend. For example, during Third Point’s campaign at insurer Prudential, Dan Loeb noted that splitting the company into two businesses would, among other things, reduce the company’s carbon footprint. We also observed examples of this trend playing out as activists criticized issuers’ responses to the pandemic. For example, Standard General criticized broadcast and media company Tegna’s employee furloughs in a proxy contest fight letter, stating that the furloughs would “cause lasting damage to Tegna’s reputation, community standing and, importantly, its employees.”

Despite these recent examples, it remains to be seen whether activist references to ESP topics will become a primary campaign objective rather than a marketing tool. Notably, Jeff Ubben of ValueAct, who has been at the forefront of the activist-ESP movement, announced in June he was leaving the activist hedge fund that he founded in order to launch a new fund, Inclusive Capital Partners. Inclusive Capital Partners will continue to run the ESP-focused ValueAct Spring Fund that Ubben launched in 2018 while still at ValueAct. Ubben’s departure demonstrates the tension between standard activist objectives and ESP themes—Ubben told the Financial Times as much, stating that he does not think these two strategies “peacefully coexist.”

D. Multiple Campaigns at the Same Company

When an issuer brings an activist onboard through a settlement, it may view itself as less susceptible to other activism campaigns. However, we have recently seen a number of situations in which an issuer who had previously added an activist designee to its board was targeted by a different activist. One example of this phenomenon was Starboard’s recent campaign at software company Commvault. In 2018, Elliott announced a roughly 10% stake in Commvault and criticized the company’s management team. One month later, Commvault agreed to appoint two new directors identified by Elliott to its board and form operations and CEO search committees. This year, in March, Starboard disclosed a roughly 9% stake in Commvault and later nominated six directors to the Commvault board. The company ultimately agreed to add three directors to its board in a settlement with Starboard. Notably, both of Elliott’s designees remained on Commvault’s board when Starboard initiated its approach, although Elliott had reportedly already exited its position. Overseas, Toshiba prevailed in a proxy contest launched by two activists just one year after the company settled with King Street Capital Management.

It is also not uncommon to see the same activists return to a company, either following a defeat in a prior campaign or following a settlement once the underlying standstill restrictions expire. For example, in April, Ancora reached a settlement with J. Alexander’s one year after making an unsolicited bid for the restaurant chain. Other notable examples include Starboard’s campaign at eBay for four new directors one year after the e-commerce company conceded two board seats to Starboard and Elliott in a settlement and Hestia Capital and Permit Enterprise’s proxy contest for two board seats at GameStop in June, one year after adding a director to the video game retailer’s board through a settlement.

These campaigns underscore the importance for issuers of continuing to engage with shareholders and monitor stock positions even after an activist designee joins their boards. Just because one activist is under the tent does not preclude another activist from taking issue with the company’s management team or business strategy. Further, once an activist is brought onboard through a settlement, it may still not be satisfied with its level of influence on the company’s strategy and agitate for more board seats or other changes once the standstill restrictions in the underlying settlement agreement expire.

E. The Changing Face of Activism

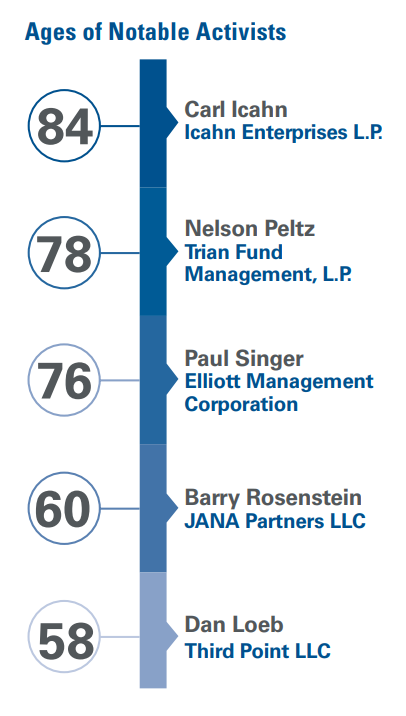

Jeff Ubben’s departure from ValueAct, the fund he founded, received substantial attention this year in part because of how much stability there has been at the top activist hedge funds over the past decades. However, there may be more turnover in the not-so-distant future. A number of other prominent activists are aging towards retirement, which would result in new faces at the forefront of U.S. activism. For example, there has been speculation for years regarding who will succeed Carl Icahn, who turned 84 years old in February, and when he will retire. In October, Carl Icahn announced that his son, Brett Icahn, is rejoining his fund and that Brett is Carl’s likely eventual replacement as chairman and chief executive. Other prominent activists are likely considering, or will be considering, similar questions—Trian’s Nelson Peltz is 78 years old and Elliott’s Paul Singer is 76 years old.

Succession is important in any industry, but especially so for activist hedge funds, where dynamic leaders have leveraged their long-standing reputations to obtain results and play a key role in drawing attention to campaigns, persuading key stakeholders and raising capital for their funds. Succession may not always be consistent with succession planning. For example, in 2019, Dan Loeb appointed Munib Islam as Co-Chief Investment Officer, leading to speculation that Islam would lead the fund upon Loeb’s retirement. In May 2020, Loeb announced that he was taking back the reins as sole-CIO and that Islam would leave the fund. Third Point, like many other funds, lost money in the first quarter of the year (prior to Islam’s exit); Loeb told investors in a letter that the fund was not adequately prepared for the pandemic. It will be interesting to see whether the largest activist funds are able to have continued success following the retirements of their founders, especially considering that a number of known protégés have left the flagship funds that trained them over the years in order to found their own funds.

F. “Short” Strategies

Recently, we have observed an increase in investors deploying short selling investment strategies targeted at individual issuers. Although we have not historically considered these strategies to be activism per se and have therefore not always included short sale activists in our data, we think these strategies are worth highlighting this year given their increased prevalence.

Hindenburg Research’s campaign at Nikola is an illustrative, high-profile example of how short selling activists operate. On September 10, Hindenburg issued a report detailing alleged fraud by Nikola surrounding its battery technology, stating that it had “never seen this level of deception at a public company, especially of this size.” The report details allegations that Nikola’s founder had exaggerated the capabilities of its Nikola One hydrogen fuel cell electric semi-truck and that the company posted staged videos on its YouTube channel in order to overstate the capabilities of its vehicles. In the two days following the release of the report, Nikola’s stock fell 11% and 14.5%, respectively. The company responded with a statement that the allegations were “false and misleading” and “designed to manipulate the market”; and Nikola subsequently announced it had hired a law firm to explore legal action against Hindenburg and that it planned to bring the matter before the SEC. The SEC responded by initiating an investigation into Nikola, rather than the short seller. Several days later, Nikola’s founder, Trevor Milton, resigned as the company’s executive chairman amid fallout from the fraud allegations and investigation. Nikola’s stock price had fallen dramatically since Hindenburg’s report, with daily trading volumes as high as 135 million shares.

Hindenburg’s report was likely produced at a relatively low cost compared to the costs associated with a traditional activism campaign, and Hindenburg was not required to make any disclosures regarding the size or nature of its short position. The activist could have closed its short positions after the initial market reaction following its reports without waiting around to see if Nikola’s stock price falls to the near zero value Hindenburg claims it is worth.

Campaigns like Hindenburg’s Nikola campaign are becoming increasingly common, with other notable targets including environmental services company GFL Environmental, COVID-19 vaccine developer Inovio and fintech company Ideanomics; although, these campaigns are not without risk. There is no guarantee how the market will react to the short seller’s report, even if it is accurate, and short positions can be incredibly costly to maintain—take, for example, the recent collapse of German fintech company Wirecard. This year, accounting fraud was uncovered at Wirecard when the company disclosed that more than $2 billion of cash was “missing.” Short sellers reportedly made paper profits of $2.6 billion off of the corresponding plunge in Wirecard’s stock price; however, short sellers had been circling Wirecard for years prior to the announcement, claiming (accurately) that the company was engaging in accounting fraud. According to reports, a number of hedge funds suffered huge losses by maintaining short positions in Wirecard before the accounting fraud was uncovered, including Blue Ridge Capital, which began shorting Wirecard in the mid-2000s and ultimately closed its position in 2017.

The complete publication, including footnotes, is available here.