Print

PrintJustin Beck is a consultant and Felipe Rubio is an associate at Semler Brossy Consulting Group LLC. This post is based on a Semler Brossy memorandum by Mr. Beck, Mr. Rubio, Blair Jones, and Greg Arnold. Related research from the Program on Corporate Governance includes Paying for Long-Term Performance by Lucian Bebchuk and Jesse Fried (discussed on the Forum here).

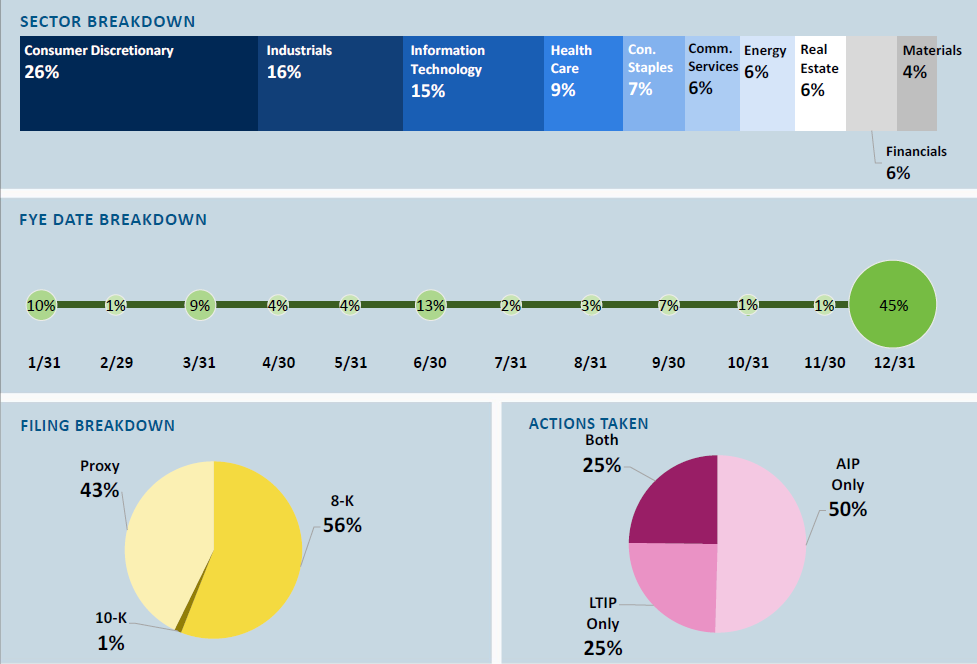

Sample Overview

N = 234 Russell 3000 Companies

Observations

- From March 1st to December 18th, 234 Russell 3000 companies announced structural changes to their inflight and/ or go-forward incentive plans:

- In-flight changes cover any structural changes to an ongoing plan, and go-forward changes cover any forward-looking structural changes to a recently started or upcoming plan

- All but four of the 234 companies explicitly disclosed that such changes were in response to economic distress caused by Covid-19

- Consumer Discretionary (26%), Industrials (16%), and Information Technology (15%) companies make up slightly more than half the sample; Consumer Discretionary and Industrials representation in the sample is higher than the broader Russell 3000 index

- Half of the sample announced changes to the annual incentive plan only, 25% announced changes to the long-term incentive plan only, and 25% announced changes to both plans

- 43% of companies in the sample previously announced temporary reductions to executive base salaries as an immediate response to Covid-19

- An additional 48 Russell 3000 companies disclosed only payout suspension, adjustments, or deferrals for a recently completed plan; these companies are excluded from the analysis of structural changes

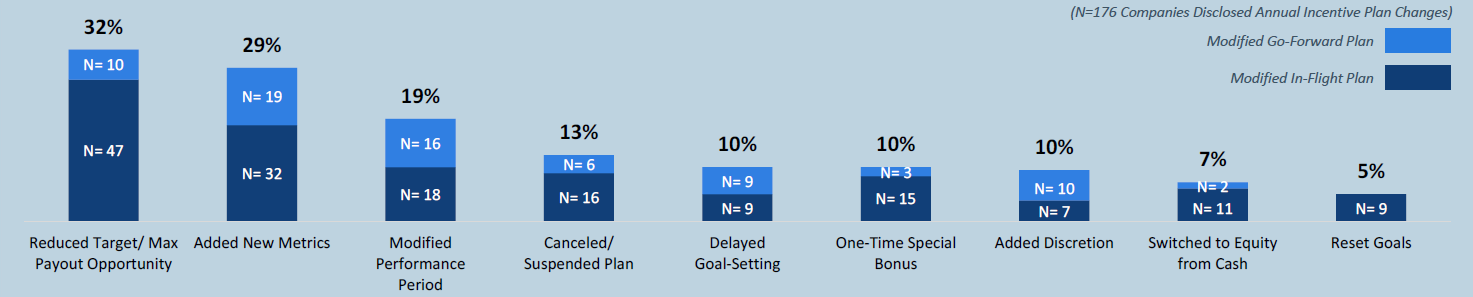

Annual Incentive Plan Changes

Covers In-Flight And Go-Forward Plans

Observations

(N=176; N=119 companies disclosed in-flight changes only, N=51 disclosed go-forward changes only, N=6 disclosed both)

- The most common structural annual incentive plan change has been to reduce the target and/ or max payout opportunity (32%, n= 57) this change has commonly been applied in concert with changes to re calibrate the annual incentive plan with revised performance projections and operational priorities (e.g. add new metrics and reset goals)

- The second most common change has been to add new metrics (29%, n= 51) commonly added metrics are focused on operating income, liquidity, or strategic measures in the context of the pandemic and several companies disclosed that such changes may be temporary as they will re evaluate the metrics for the following fiscal year at a later time

- 34 companies modified the annual incentive plan performance period, typically to measure partial year performance or separate the year into halves

- 22 companies canceled or suspended the annual incentive plan entirely, and 13 companies switched to paying the annual incentive plan in equity instead of cash

- 18 companies delayed goal setting to later in the fiscal year although we recognize this practice may be more prevalent among companies that have not disclosed such actions

- 17 companies proactively added Committee discretion to determine payouts (although, this approach may be more prevalent in practice given the qualitative measurement of certain additional metrics) 67 companies have already disclosed the application of Committee discretion to adjust, suspend, or defer the payout for the recently completed annual incentive plan of those of 67 companies, 54 only disclosed the payout modification, and the other 13 companies also disclosed additional structural AIP changes

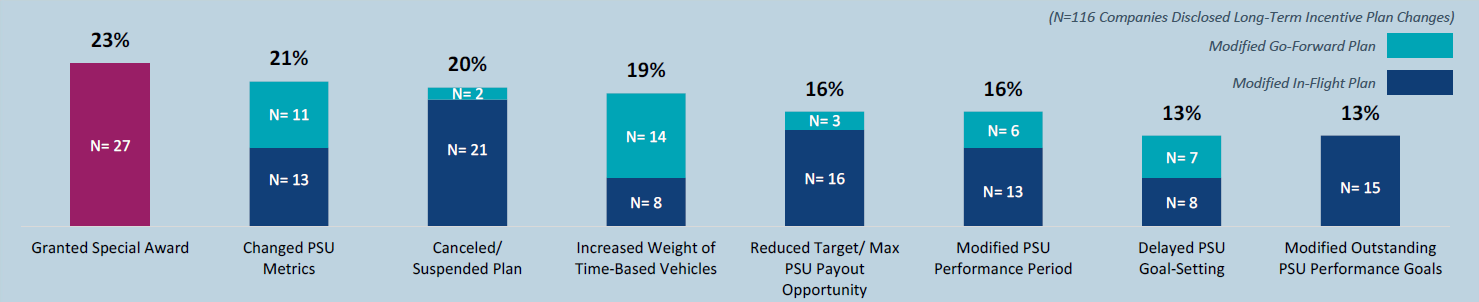

Long Term Incentive Plan Changes

Covers In-Flight And Go-Forward Plans

Observations

(N=116; N=79 companies disclosed in-flight changes only; N=32 disclosed go-forward changes only, N=5 disclosed both)

- 27 companies granted special awards to one or more NEOs (awards have typically been equivalent to less than one year annual grant value and were granted with varying rationale), and 23 companies elected to cancel outstanding LTI grants and/or suspend granting new awards five companies from these groups applied both actions together

- 24 companies switched PSU metrics, typically to metrics that are (i) more focused on operational health (e.g. cost reduction); (ii) more easily forecasted and/or (iii) relative metrics

- 22 companies adjusted the long term incentive vehicle mix to a higher weighting of time based vehicles (i.e. RSUs or stock options) half of these companies switched to 100 time vesting RSU and/or stock option awards

- 19 companies reduced the PSU target and/or max payout opportunity, and 19 companies modified the PSU performance period four companies from these groups applied both actions together

- 15 companies delayed goal setting for PSUs and 15 companies disclosed modifications to in-flight PSU awards’ performance goals

- Additionally, seven companies applied discretion to adjust the PSU/Cash LTIP payout for the performance period that just ended (not shown or included in this sample)

The complete publication is available here.