Print

PrintJamie C. Smith is Investor Outreach and Corporate Governance Specialist at the EY Center for Board Matters. This post is based on an EY memorandum by Ms. Smith and Stephen W. Klemash.

As we mark a decade of engaging with investors with this year’s proxy season preview, much has changed in the investor landscape, particularly over the past year of the pandemic. Investors want boards to help companies adapt their strategies for a future in which prioritizing stakeholders and considering environmental and social impacts will be critical to building resilience and creating long‑term value.

Investors view workforce diversity as a key component in driving innovation and performance. This is of particular importance in a dynamic environment marked by ongoing business model disruption, changing stakeholder demands and accelerating sustainability risks. These are some of the key themes of our conversations with governance specialists from more than 60 institutional investors representing over US$38 trillion in assets under management, including asset managers (62% of all participants), public funds (20%), labor funds (13%) and faith-based investors (2%), as well as investor consultants and associations (3%).

In this post we focus on:

- Factors investors cite as the top strategic drivers and threats for companies

- Top investor engagement priorities for 2021

- Six ways companies can enhance their ESG reporting

- Steps investors want boards to take to strengthen their effectiveness

Top strategic drivers and threats facing companies, according to investors

Quality and execution of multi-faceted strategy will drive success

Coming out of a year of unparalleled disruption, nearly half of investors said their portfolio companies’ quality of strategy and ability to execute will be critical to success—and even survival—over the next three to five years. Many pointed out that in the current environment the ability to formulate, fund and execute a successful strategy will require adapting to new technology, strengthening crisis response and business continuity planning and having credibility with stakeholders and an open mindset around which products to focus on and which businesses to wind down.

Many investors highlighted that stakeholder needs and the external forces impacting consumers, employees and the regulatory framework—from technology and climate risk to social justice movements—must be integral to strategy development to identify forward-looking, resilient business strategies and deliver long-term value. Almost half of investors identified the integration of material environmental, social and governance (ESG) opportunities into strategy as among the biggest drivers of strategic success. These investors believe that if companies are effectively monitoring and managing ESG factors, those efforts can uncover new strategic opportunities and business model needs, position the company to be more agile and competitive as sustainability risks and stakeholder demands continue to change, and strengthen the company’ s social license to operate.

Investors discussed diversity—both across the workforce and in the boardroom—as being central to a company’ s ability to innovate and embrace change, and 42% identified diversity as a significant driver of success. While investors largely focused on diversity’s link to performance, profitability and innovation, some also pointed out that the business case intersects with the broader social movement around racial justice. If companies are not leading on social change and responding to the national conversation on race, there is an opportunity cost: a failure to act could impact the company’ s relationships with employees, customers and other stakeholders.

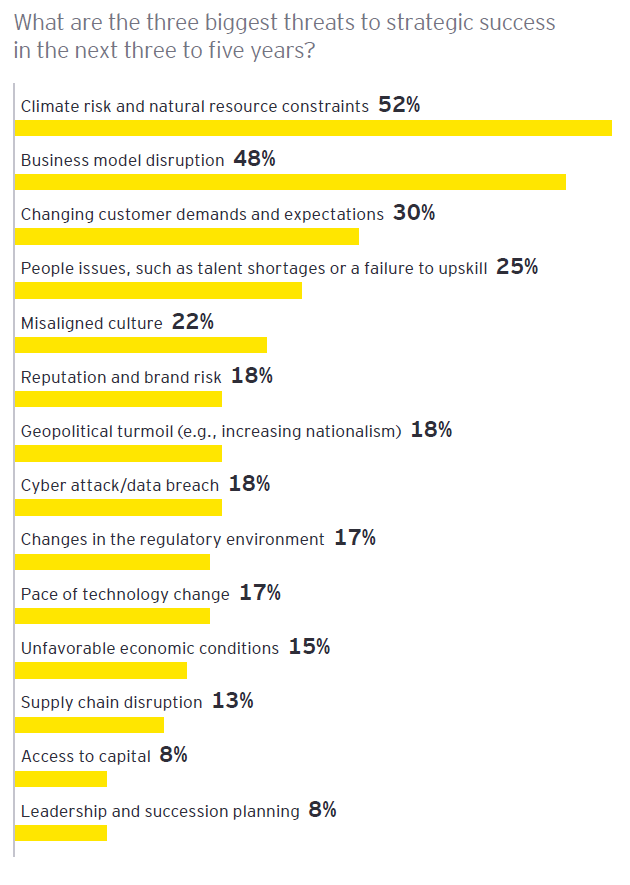

Climate risk, business model disruption and changing customer demands viewed as biggest threats

More than half of investors said climate risk and natural resource constraints are among the biggest threats facing companies over the next three to five years, with most of those investors specifically focused on climate risk. The physical risks of climate change are front and center for many who noted that severe climate‑related events are happening faster, more often and more severely than expected, and will broadly impact sectors and markets in different ways across the globe.

Further, investors noted a heightened attention during COVID‑19 to severe, systemic risks related to exogenous events, and pointed to climate change as the next such challenge on the horizon. Some investors stressed that climate change will further accelerate other systemic risks (e.g., biodiversity loss, economic inequality) and suggested that it has the power to disrupt traditional notions of corporate preparedness. In other words, investors are looking beyond the basics of climate risk in the supply chain. To be successful going forward, these investors said companies will need to be more future‑oriented. They will need to integrate climate and other sustainability risks into the business strategy, and to focus on having the culture, values and people in place to continually look forward and build resilience.

Business model disruption more broadly was the second‑most‑ cited key threat, chosen by nearly half of investors. Most of these investors highlighted the need for companies to innovate and disrupt in order to adapt to the rapidly shifting business context and meet changing stakeholder needs. Investors pointed to extensive sources of disruption and pressure on business models, including accelerating technology change, the transition to a low‑carbon economy, regulatory changes, new entrants and the broad impacts of the pandemic on work, travel and consumption. It’ s not surprising that close on the heels of business model disruption, 30% of investors identified changing customer demands and expectations as a top threat. Many of them highlighted that this goes beyond changing customer demands to the changing demands of stakeholders more broadly. And those demands span numerous dimensions, from expectations around how technology can enable new ways of working and consuming to how businesses impact the environment, communities, privacy, politics and culture.

Shifts in the investor landscape over our decade of investor dialogue

The investor landscape has undergone major changes in recent years, spurred by crises as well as opportunities. Some of the most dramatic shifts we have observed in 10 years of ongoing conversations with investors include the rise in company‑shareholder engagement, which was emerging in response to mandatory say‑on‑pay proposals as we began our investor outreach in 2011 and has since become a defining governance trend of the past decade.

ETF and index fund managers who used to be labeled “passive” have become much more vocal, becoming active stewardship leaders and driving engagement campaigns that help define the board agenda. Along with these developments, investors have been steadily increasing transparency around their stewardship priorities and proxy voting, which is expanding opportunities for companies to educate themselves on individual investors’ perspectives.

And most recently, ESG has gone mainstream. While a decade ago investors raising environmental and social topics with us were predominantly socially responsible investors (SRIs), ESG is now fundamentally reshaping investment and stewardship, dominating our conversations across all investor types and revealing SRIs as harbingers of current investment trends.

Heading into 2021 and beyond we are attuned to new shifts underway that could continue to alter the investor landscape, including how stakeholder capitalism is implemented and governed, potential growth in investors using proxy votes to communicate their views and drive change, and the potential impacts of consolidation in the asset management industry on investor stewardship and ESG trends.

Key board takeaways

- Assess how the strategy is delivering long-term value for the multiple stakeholders on which the company depends and strengthening its social license to operate.

- Consider the role of purpose in the company’s strategy and decision-making, and how the company can strengthen its business resilience and growth opportunities by becoming part of the solution for global challenges.

- Confirm that the company has the right leadership team and board, culture and values to innovate and lead.

- Challenge how the company is being resilient in all aspects of strategy, risk management and

capital allocation.

Top investor engagement priorities for 2021

In 2021 investors continue to engage their portfolio companies on how they are responding to the pandemic, particularly what steps they are taking to build resilience and strengthen business continuity while supporting employee engagement, health and well-being. When we asked investors what engagement topics they will prioritize this year, the following themes were cited most often.

Workforce and board diversity

Around two-thirds of investors told us they will press for robust diversity disclosures inclusive of the workforce and boards. Regarding the workforce, most want disclosure of diversity data aligned to the disclosure framework of the U.S. Equal Employment Opportunity Commission’ s EEO-1 Survey (EEO-1 data) at minimum to enable assessment of diversity across the employee base and talent pipeline and, over time, progress related to diversity initiatives and commitments. Some encourage companies to supplement EEO-1 data as needed with data that better reflects how the company is run but emphasize the need for EEO-1 data as a baseline to ensure comparability. A few investors seek promotion, retention and recruitment data for protected classes of employees to directly illustrate the upward mobility of diverse talent.

Investors pointed out that to be meaningful, workforce diversity data must be supported by a narrative about the company’ s human capital strategy and goals. While many said they’ll be looking closely at racial diversity, some added that they’ re interested in diversity across many dimensions, including age demographics, noting interest in understanding how companies are managing a workforce that extends from millennials through retiring baby boomers.

At the board level, investors want disclosure of the board’ s diversity across gender, race and ethnicity, and to see more diverse directors brought into the boardroom and policies that encourage diverse director recruitment (e.g., adoption of the Rooney Rule, which commits boards to including women and minority candidates in director nominee search pools). Investors may vote against certain directors at companies not disclosing this information or making related progress. Having already established voting guidelines around minimum gender diversity standards, some are now incorporating broader diversity thresholds into their proxy voting policies and others indicated they may do so in the future.

Climate risk/environmental issues

Around two-thirds of investors said they will prioritize climate risk, and many of those are working with Climate Action 100+, an initiative of over 500 investors pressing for corporate action on climate change. Investors cited the acceleration of physical climate risks and the urgency to fundamentally reorganize the economy over the next decade to avoid the most catastrophic outcomes. While the nature of climate-related engagements can be sector- and company-specific, a consistent thread is investors seeking company disclosures aligned to the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD), which include disclosures related to the governance, strategy, risk management approach and metrics and targets used relative to climate-related risks and opportunities. Additional comments we heard include requesting companies to commit to net-zero greenhouse gas (GHG) emissions by 2050, adopt science-based GHG reduction targets aligned to the goal of the Paris Agreement, conduct climate-related scenario analysis and adopt renewable energy targets.

Many investors seek more specificity around companies’ decarbonization strategies for reaching aggressive, longer-term emissions reduction targets. They want to understand how businesses are transitioning in the short and mid-term and to hold companies accountable on the pace and trajectory of that delivery. To that end, some investors said they will look to capital expenditures as a key indicator of how a company is positioning itself for the future and whether its climate ambitions are credible. Many are also focused on how physical climate risks are assessed and managed across the value chain, and how corporate political and lobbying expenditures align to stated climate commitments.

Investors are also making their own climate-related commitments, including through the United Nations-convened Net-Zero Asset Owner Alliance and the Net Zero Asset Managers Initiative, both of which support aligning investments with the goal of net-zero emissions by 2050. As investors act on these commitments, the pressure on companies to accelerate their transition to a low-carbon future will grow.

Executive compensation

Just under a third of investors said they will prioritiz e executive pay in their 2021 engagements. Most are focused on pay decisions related to the impacts of COVID-19 and are evaluating those decisions through the lens of stakeholder alignment, particularly how executive pay aligns with decisions related to the broader workforce (e.g., pay cuts, furloughs and layoffs)—and their expectations are more pronounced for companies that have received government subsidies.

Many said they will scrutinize adjustments to performance goals and payout opportunities, option repricings and equity grants made at the bottom of the market. Additionally, some investors are engaging companies on tying ESG goals to executive pay, including considering whether current incentives exacerbate ESG-related risks.

Strategic workforce issues beyond diversity

A quarter of investors are prioritizing human capital management engagement more broadly. They are focused on the health and safety of the workforce as the pandemic continues, as well as on how companies are thinking about human capital strategy in a post-pandemic future. Investors want to understand how companies are taking what they’ve learned about their workforce through the pandemic and translating that into opportunity, including how they’ re investing in job retraining and workforce adaptation as the nature of work and ways of working continue to transform. Some investors want to see boards assign the compensation committee, or another board-level committee, responsibility for overseeing workforce matters, and want to understand board members’ line of sight into the employee experience (e.g., are they having regular discussions with the Chief Human Resources Officer and unstructured interactions with employees). Additional discussion themes include continuing concerns from some investors around the impact of automation on jobs and the economy, and the impact of independent contractor models on workforce management, the long-term prosperity of workers and the economy.

Emerging areas of focus

A handful of topics stood out this year as gaining traction among a broader group of investors. These include biodiversity loss and protecting the ecosystems upon which business and society depend, the refection of climate risk in financial statements, how companies are operationalizing their stakeholder commitments, and understanding and valuing the environmental and social impacts of a company’ s products and operations. Investors interested in these topics have in the past been leading indicators of where investor sentiment will go.

Key board takeaways

- Understand the evolving disclosure expectations, engagement priorities and proxy voting guidelines of key investors.

- Across key focus areas such as workforce and board diversity and climate change, consider whether company communications make clear what the related strategy is, how progress is incentivized and measured and how oversight is executed at the board and committee level.

- Approach engagement as an opportunity to gain external insights to further develop the company’s strategy and disclosures.

- Recognize that some investors have indicated an increased willingness to vote against directors, and in favor of shareholder proposals, as ways to communicate their views and drive change.

Six ways companies can enhance their ESG reporting

When it comes to assessing a company’s ESG practices and performance, investors said that company disclosures—along with direct engagement conversations and the investors’ own subject-matter expertise and research—are their most valuable resources. Most investors told us they use third-party ESG ratings (if at all) as initial, scalable screening tools or guideposts that may give them an indication of where to focus deeper research and analysis.

Investors are working to improve the ESG data set on which they rely by asking companies to enhance their ESG reporting. When we asked investors what key enhancements they want companies to make, most of their answers aligned to one or more of the following six tips.

1. Focus on what is material and the connection to strategy

Investors want reporting to focus on the ESG topics that intersect most directly with the business and tie directly to strategy. Some investors noted that it is particularly valuable when company reporting discusses the results of a formal materiality assessment, providing deeper context around how the company defined priorities. While investors generally said that financial value should define ESG topics of focus, some urged companies to also consider areas that may be material to stakeholders from an impact perspective and pointed to values-aligned investing and consumer behavior as growth areas.

2. Align disclosures to external frameworks

Investors want companies to align their disclosures to an external framework, and many encouraged companies to provide a report card or appendix map to make that alignment explicit. Nearly all cited the Sustainability Accounting Standards Board (SASB) as a decision-useful framework. Investors seek a baseline level of standardized data to support relevance, objectivity and comparability.

Which human capital disclosures do investors want most?

We asked investors which workforce disclosure topics would be of greatest value to them as they assess human capital management, and as new human capital disclosure requirements take effect. By far, workforce diversity across gender, race and ethnicity was the top choice, with 85% of investors saying they want increased disclosure in this area. This finding aligns with diversity being a top investor engagement priority and an area many investors view as a top strategic value driver.

Coming in second was pay equity, which investors generally discussed as an extension of workforce diversity disclosures and a window into whether the company has structural issues around diversity, equity and inclusion (DEI) that need to be addressed. Many of these investors specified that they want companies to disclose median pay gap data, which shows how women and minorities across the organization are paid on average regardless of role. They said that this information can signal whether diverse talent is stagnating at less-senior, lower-paying roles, and some said they want to see this unadjusted pay gap for each defined level of the company’s workforce.

Discussions around workforce stability, the third-most-chosen topic, focused on how turnover data can provide insights into whether companies are building on the investments they’ re putting into onboarding and training, and whether the company is an employer of choice in its industry. Some investors said they would ideally like to see workforce stability data disaggregated by gender, race and ethnicity (to enhance their view into DEI challenges) and/or by job level (to better understand the level of turnover happening at more-senior levels). A few investors said they explore alternative data sources to get insights into turnover rates when company data is not available.

Other key themes from these discussions included investor interest in understanding the nature of a company’ s relationships to independent contractors and their role in the company’ s business model (e.g., are independent contractors being valued relative to their role in the business) and seeing how companies are developing, upskilling and rebalancing employee skill sets to adapt their workforce to changes in the company’ s strategy. Investors also highlighted that data should align to external frameworks and be put into the context of the company’ s strategy, expectations and goals.

3. Disclose metrics, performance and goals

Investors also focused on the need for more quantitative data. They want disclosure of the metrics management is providing to the board to measure progress and year-over-year performance against ESG goals. Investors said that without the data, they cannot assess the company’ s progress on ESG initiatives and may not have the context needed to understand certain goals (i.e., baseline data is necessary for understanding what a percentage increase or decrease goal means). Some investors noted that they increasingly see forward-looking climate goals and want to see the same for workforce and human rights topics.

4. Consider integrating material ESG disclosures alongside traditional financial metrics

While some investors made clear that they don’t have a strong view on where the disclosures are made, some believe that integrating material ESG disclosures into regulatory filings, particularly the 10-K, is the ideal approach and best reflects how ESG is aligned to the core business model and integrated into the business. These investors acknowledged that ESG reporting is a journey and view the integration of sustainability factors into financial reporting as the ultimate endgame.

5. Enhance data credibility through assurance

Some investors said that attestation would help validate sustainability reports and generally characterized assured ESG data as the gold standard for demonstrating high-quality information.

6. Make sure company disclosures are picked up by third-party data aggregators

Some large asset managers rely on third-party data providers to aggregate and structure company disclosures in a way that is more scalable and efficient to their processes, allowing raw ESG data across thousands of companies to be uploaded into their internal platforms for assessment. While investors generally acknowledged limitations of third-party data (e.g., gaps, data quality issues) they stressed their need to have data at scale. To make these processes successful, investors encouraged companies to take a more proactive role in confirming that their data is being picked up correctly by leading third-party providers.

Key board takeaways

- Challenge whether the company’ s ESG disclosures communicate how the company is competitively differentiating itself to create value over the long-term. Consider whether the company is providing the comparable ESG data investors seek and confirm that those disclosures are being picked up by leading third-party data and ratings providers.

- Consider whether obtaining external assurance and integrating material ESG metrics into regulatory filings could strengthen the company’ s positioning.

- Given that social topics came to the fore in 2020, ask management about opportunities to enhance disclosures on social topics such as diversity and equity in the workplace, other strategic workforce issues and human rights.

Steps investors want boards to take to strengthen their effectiveness

We asked investors what steps they want boards to take to strengthen their effectiveness, particularly in the current environment. Most of their suggestions align to the following steps.

Focus on board refreshment aligned to strategic oversight needs

Around 40% of investors expressed a desire for boards to have stronger discipline around turnover in the boardroom to better align board expertise with strategy and meet investor expectations for board diversity. Some want boards to consider mechanisms to increase refreshment (e.g., managing to an average tenure goal, adopting a retirement age or overboarding policies). Given the accelerating pace of change, investors said that the relevance of long-tenured directors’ skills and experience is increasingly less clear, and that burden of proof is on the board to show how it approaches ongoing director education. Investors also said that a robust self-assessment process should play a key role in refreshment considerations.

Diversify

Around a third of investors focused on the opportunity for boards to enhance their effectiveness by diversifying across numerous dimensions, specifically including race, ethnicity, gender, skills and experiences. Key themes of these conversations included the need for challenging groupthink, enabling more robust discussion, setting the tone at the top for the company’ s DEI goals, and having diverse perspectives and experiences in the boardroom to stress test ideas in a crisis and more effectively oversee strategy.

Challenge how reporting from management, use of external resources and director education can be improved

One other aspect that came up more than expected was the topic of how boards are staying informed and receiving ongoing education to meet evolving oversight demands and navigate a rapidly shifting risk landscape. A point we heard consistently is the opportunity for boards to access more external expertise to help management look forward and see how external trends and stakeholder expectations are changing over time. Interestingly, we are hearing more from boards themselves on this topic as well. Some investors emphasized that they want boards to demonstrate an independent, informed view on the key issues facing the company (specifically including ESG issues like climate risk). Some investors also encouraged boards to assess the effectiveness of management reporting to the board, including the frequency of that reporting, the sources of information (e.g., is the CHRO meeting with the board regarding human capital matters), the usefulness of the data and dashboards provided in enabling strategic oversight, and the robustness of the discussions.

Key board takeaways

- Look inward and challenge whether the board has the right people, structure, processes and information to be effective as the business environment, stakeholder demands and company strategy continues to evolve.

- Ensure all directors have access to ongoing education opportunities that include external sources, particularly around emerging issues.

- Develop a structured and intentional approach to managing board turnover and refreshment.

- As company sustainability practices and impact, strategic workforce issues and stakeholder commitments come under more scrutiny, consider how the board is governing social issues and upholding its commitments to stakeholders.

Looking ahead

The past year has stress tested the social contract and expanded opportunities for companies to lead on global challenges. In response, board members will need to take on more of a leadership role in focusing their companies on long-term-value creation, and from what we’ re hearing, investors expect them to do so. Heading into proxy season 2021, investors seek to hold boards accountable for how companies are charting a course through recovery and continued disruption to long-term-value creation and acting as responsible stewards of natural and human capital. Investors are also communicating an increased willingness to vote against board members, and in favor of shareholder proposals, to express their views on environmental and social topics—and are doing so as sustainable investment trends continue to accelerate and the political context and regulatory framework around ESG continue to evolve.

Questions for the board to consider

- How is the company’ s strategy evolving to deliver value to multiple stakeholders as trends around technology and sustainability accelerate, and as attention to companies’ environmental and social impacts grow? How are related goals and performance incentivized and communicated?

- Does the company have the right leadership, culture and values—both in the C-suite and the boardroom—to help the company innovate, lead and thrive in today’ s business environment?

- How is the company using workforce data to demonstrate to the market its progress on, and integrity around, diversity commitments and goals and the company’ s investments in its people?

- Do the company’ s disclosures clearly communicate how key environmental and social topics are overseen at the board level and any actions the board is taking to deepen its expertise and inform an independent perspective on those topics?

- Does the company approach ESG as a strategic differentiator or a compliance exercise?

- Does the company’ s ESG reporting provide the comparable, high-quality ESG data investors seek? And is the company’s ESG data getting picked up by leading third-party data and ratings providers?

- Does the board have the diverse skills, expertise and perspectives it needs to guide strategy over the next five or more years? If not, what is the board doing to recruit new directors and expand its search to include more diverse nominees?

- How does the board stay informed about the views and priorities of the company’ s major investors and other key stakeholders? To what extent are board leaders involved in investor engagement?