Print

PrintErin Dwyer is Deputy Director of the Office of External Affairs at the Public Company Accounting Oversight Board. This post is based on a publication authored by PCAOB Staff.

Overview

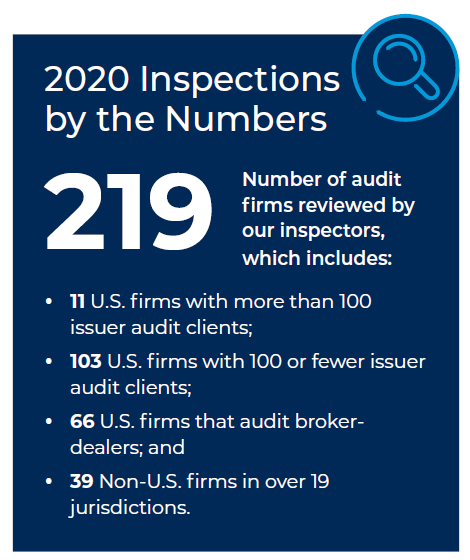

The Public Company Accounting Oversight Board (PCAOB) views engaged and informed audit committees as effective force multipliers in promoting audit quality and believes that the PCAOB and audit committees jointly benefit from our ongoing dialogue. Continuing with the expanded engagement we launched in 2019, we again reached out to the audit committee chairs of most of the U.S. public companies whose audits we inspected during 2020 and offered them the opportunity to speak with our inspection teams. In total, we spoke to nearly 300 audit committee chairs. In addition to the effects of the COVID-19 pandemic on the audit, we discussed three core topics during our conversations:

- The auditor and communications with the audit committee;

- New auditing and accounting standards; and

- Emerging technologies.

This post summarizes the feedback we received in each topic area. Please note that the PCAOB does not necessarily endorse what we heard from audit committee chairs. Rather, we present this summary in an effort to provide greater transparency into these important conversations.

COVID-19

An overarching theme of our calls in 2020 was how the COVID-19 pandemic created unprecedented challenges for auditors, audit committees, and public companies. We previously reported on that topic in Conversations with Audit Committee Chairs: COVID-19 and the Audit.

We also published two other documents—COVID-19: Reminders for Audits Nearing Completion and Staff Observations and Reminders during the COVID-19 Pandemic—that include reminders about certain auditor responsibilities, notwithstanding the challenges that may exist related to COVID-19.

The Auditor and Communications with the Audit Committee

We asked audit committee chairs a number of questions related to their audit firm and ongoing communications between the audit committee and their auditors.

Communications

Audit committee chairs frequently cited communications with their auditors—both verbal and written—as extremely important to audit quality and their overall relationship with their auditors. Most audit committee chairs commended their auditors’ communications, commonly sharing that they were thorough, timely, and at the right level of detail and frequency. Several also highlighted their appreciation for dashboards provided by their auditors that highlighted real-time data on audit progress and other topics.

Auditor Strengths and Areas for Improvement

Audit committee chairs noted that their auditors performed well in areas such as assigning resources with expertise on complex accounting issues, consulting their national offices as appropriate, offering practical approaches to problem-solving (as opposed to being highly theoretical), and providing continuity on audit teams.

Innovation and partner rotation were areas where some audit committee chairs praised their auditors, but others flagged them as areas needing improvement. Other potential areas of improvement that were identified included:

- Managing global audit operations;

- Helping more junior audit team members learn the company’s business;

- Independence communications;

- Guidance around auditing of certain controls for third-party vendors;

- “Over-auditing” and/or “overdocumentation;” and

- Increased visibility into and discussion around fee changes.

New Format for PCAOB Inspection Reports

In 2020, we began issuing inspection reports in a redesigned format, the first substantial change to the inspection report in more than 15 years. We streamlined the content to enhance readability and used charts and graphs to make the information more digestible and accessible. To enhance transparency, we also included information not previously communicated in inspection reports.

The response from audit committee chairs to the new format has been overwhelmingly positive, with many noting that the reports are more concise, better organized, easier to read, and generally more useful. We encourage audit committee members to read our Guide to Reading the PCAOB’s New Inspection Report and to share your feedback.

Reviewing Inspection Reports with Auditors

We asked audit committee chairs if they reviewed PCAOB inspection reports with their auditors. While there were varying degrees and types of reviews, audit committee chairs who did review the reports and had conversations with their auditors about them generally found the exercise to be useful. Audit committee chairs continued to cite the lag between when inspections occur and when inspection reports

are issued as an area of concern. Reducing that lag remains an important strategic priority for the PCAOB.

Awareness of Auditors’ Initiatives to Prevent Audit Deficiencies

We sought to gauge the understanding of audit committee chairs about the activities or initiatives that they observed audit firms undertaking to prevent audit deficiencies, which is a significant area of strategic focus for the PCAOB. Their responses to our questions largely centered on:

- Audit firms’ use of emerging technologies;

- Audit firms’ emphasis on tone at the top;

- The role of robust training as a guard against deficiencies; and

- The importance of auditors staying focused on implementation of new accounting and auditing standards.

Assessing Auditor Performance

Finally, we inquired about audit committees’ assessments of their auditors. Many audit committee chairs noted that they routinely assess the performance of their auditors, often with an emphasis on the lead engagement partner and the engagement team’s communications and timeliness. While some committees do it on an annual basis or in conjunction with the decision to include the ratification of the auditors in the annual proxy, many shared that they are conducting such assessments more regularly—either quarterly or in real time should the need for feedback arise.

Audit Committee Perspectives: What’s Working Well

- Asking the external auditors to provide constructive feedback or tangible recommendations on areas where the company’s internal audit team or financial reporting systems could improve.

- Asking the audit firm if they have training or resources for new audit committee members or a newly appointed chair.

- Regularly assessing the engagement team’s performance.

- Asking the auditors to review the PCAOB inspection report with the audit committee and to discuss any initiatives the firm has implemented to address deficiencies described in the inspection report.

- Reviewing year-over-year PCAOB inspection report trends within and between audit firms.

New Auditing and Accounting Standards

The next area of focus in our conversations was the implementation of new auditing and accounting standards. Audit committee chairs oversaw implementation of a variety of new accounting standards during the period covered by our 2020 inspections. New accounting standards for revenue recognition, lease accounting, and where applicable, preparing for implementation of current expected credit losses (CECL), stood out as particularly challenging and time consuming for many audit committee chairs.

Implementation of the critical audit matter (CAM) requirements by auditors, by contrast, was generally viewed as smooth, with audit committee chairs noting that dry runs and other early preparation with their auditors led to few surprises. These views were consistent with what we have heard elsewhere from audit committees and others, as discussed in our interim analysis report: Evidence on the Initial Impact of Critical Audit Matter Requirements. Many audit committee chairs were surprised to learn the PCAOB is studying the economic impact of the CAM requirements. To increase awareness of the role and use of economic analysis in standard setting, including how we conduct economic analysis and gather stakeholder input both before and after our standards take effect, we published a new resource, The PCAOB’s Use of Economic Analysis and Stakeholder Input in Standard Setting, providing a high-level overview of our process, as well as a “case study” on how economic analysis has informed the adoption and implementation of the CAM requirements.

Accounting Estimates and Use of Specialists

The PCAOB’s new requirements related to auditing accounting estimates, including fair value measurements, and using the work of specialists took effect for audits of fiscal years ending on or after December 15, 2020.

In our 2020 conversations with audit committee chairs, however, we learned that over three-quarters had not yet discussed the new requirements in detail with their auditors. We encourage audit committees to review our resource for them on this topic.

Audit Committee Perspectives: What’s Working Well

- When reviewing the audit plan, asking the auditors if there will be any significant changes to their audit approach for the year in light of new or revised accounting or auditing standards.

- Asking the auditors to provide the audit committee early notice and frequent updates when new standards are being implemented. Setting aside time for educational sessions or deep dives where auditors can explain and answer questions about how new audit requirements may impact the audit.

- Requesting that auditors communicate their approach to auditing the implementation of new accounting standards (that are coordinated with management’s timelines) and implementation of new auditing standards.

- Discussing with the auditors whether they assessed any possible challenges or issues associated with auditing the implementation of new accounting standards or applying new auditing standards and, if so, how the auditors plan to address them.

Emerging Technology

The final area we addressed in our conversations was emerging technologies and their use in the audit. Many audit committee chairs cited the potential benefits from the use of emerging technologies, notably to improve both the audit and overall financial reporting quality. Specifically, they shared their belief that the use of data analytics, workflow automation, cloud computing, and other tools will allow auditors to reduce manual work, obtain better evidence, and become more efficient. Other audit committee chairs noted that technology, if deployed properly, can (1) cut down on opportunities to manipulate or falsify financial information and (2) provide auditors with the ability to more easily identify anomalies.

Yet audit committee chairs also discussed numerous challenges associated with emerging technologies. For example, several audit committee chairs highlighted the gap between the technological capabilities of the company and those of the audit firm. While some audit committee chairs noted that their companies had more sophisticated technology than their auditors, others said the opposite. Either way, audit committee chairs largely agreed that companies and auditors need similar levels of technological capabilities for the benefits of using emerging technologies to be fully realized.

Audit committee chairs were also wary of the risks that come with emerging technologies. They commonly flagged cybersecurity risk as the thing that keeps them up at night, especially with the shift to remote work during the COVID-19 pandemic. Another risk cited was overreliance on technology leading to less attention to or emphasis on preparer and auditor judgment, experience, or professional skepticism.

Additionally, some audit committee chairs voiced concerns about how: (1) the issuer maintains robust controls and makes necessary adjustments, (2) the auditor evaluates and tests changes to new controls, and (3) the audit firm implements internal controls over its technology. Some believed that companies and auditors alike should think about ways to increase training and to adjust existing controls or develop new controls.

Finally, audit committee chairs expressed concerns about technology unknowns, given that many technologies have only recently been adopted or put into use. They noted that while the benefits of emerging technologies are often immediately clear, the risks involved can take longer to become apparent or to understand.

Audit Committee Perspectives: What’s Working Well

- Regularly discussing with the auditors how they and their firms are thinking through challenges, risks, and opportunities associated with use of emerging technologies.

- Asking the auditors if/how the use of technology will change the way the team’s time and/or resources will be allocated.

- As new technologies are implemented, discussing with management if/how the underlying controls will change and discussing with the auditors how they will evaluate and test any changes to the new controls.

- Holding committee or full board deep dives on specific topics related to emerging technologies, new technology tools used in the audit, and cybersecurity.

- Asking the auditor to provide best practices or benchmarks for the use of technology and/or information security within the issuer’s industry.

- Discussing whether the company uses third-party software or data processing for financial reporting processes and, if so, how risks and controls are considered and addressed.

- Asking the auditors for their views on expertise or tools related to emerging technology, data protection, or cybersecurity that may supplement management’s existing expertise or tools.