Print

PrintGranville J. Martin is General Counsel at the Society for Corporate Governance, and Maia Gez and Dov Gottlieb are partners at White & Case LLP. This post is based on a memorandum by White & Case and The Society for Corporate Governance by Mr. Martin, Ms. Gez, Mr. Gottlieb, Danielle Herrick, Colin Diamond, and Era Anagnosti. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance by Lucian A. Bebchuk and Roberto Tallarita (discussed on the Forum here); For Whom Corporate Leaders Bargain by Lucian A. Bebchuk, Kobi Kastiel, and Roberto Tallarita (discussed on the Forum here); Socially Responsible Firms by Alan Ferrell, Hao Liang, and Luc Renneboog (discussed on the Forum here); Restoration: The Role Stakeholder Governance Must Play in Recreating a Fair and Sustainable American Economy—A Reply to Professor Rock by Leo E. Strine, Jr. (discussed on the Forum here).

In light of the continued focus on improving sustainability reporting, White & Case conducted its second annual survey and in-depth review of ESG website disclosures of 80 small- and mid-cap US public reporting companies:

- Overall, more than half of the surveyed companies (approximately 51 percent, or 41 out of 80 companies) provided some form of voluntary sustainability disclosure on their websites. This represents a 16 percent increase from 2019, in which 35 percent of small- and mid-cap companies surveyed had website sustainability

- Of the 41 companies that provided ESG website disclosure in 2020, at least 13 (or 32 percent) did not engage in any ESG website disclosure in 2019, suggesting a quickening trend of voluntary ESG website

- Website sustainability disclosures ranged in length from a paragraph to multiple website pages or a stand-alone sustainability report.

Key trends and takeaways from our survey, which are set forth below, explain important factors driving the pace of sustainability disclosure journeys for US public companies, as described in the following sections of this post:

- Industry Trends

- Market Cap Trends

- Disclosure Trends: Length of Time Since IPO

- Use of Reporting Standards

- Inclusion of Disclaimer Language

- Sustainability Topics Discussed

- Considerations and Key Takeaways

Sustainability Disclosure by Industry and Market Cap

Industry Trends

In our survey, we reviewed the website sustainability disclosures of companies in the following five industries: energy, life sciences, retail, services and technology. The number of companies with sustainability disclosures in each industry group are shown in the chart above. Key trends are discussed below.

Retail and Energy Companies Lead the Way

Of the five industries represented in our survey, companies surveyed in the retail and energy sectors were most likely to provide some form of website sustainability reporting:

Energy

- Overall, the energy companies surveyed had the most robust website sustainability disclosures, reporting on the greatest number of topics at the greatest length.

- Twelve of the 13 energy companies surveyed included website sustainability disclosures. The surveyed energy companies were in the oil and gas, natural gas, renewables/clean energy and service provider categories.

- Disclosures by energy companies tended to focus on environmental issues, including climate change, use of renewables and greenhouse gas emission targets and metrics, with all 12 of the surveyed energy companies with sustainability disclosures including environmental disclosure.

- All 12 of the surveyed energy companies with website sustainability disclosures also included disclosure of human capital management matters, including ten that included health and safety Ten of the companies also included community impact/corporate social responsibility disclosures. See the “Sustainability Topics Discussed” section below for more information on topics covered.

Retail

- All six of the retail companies surveyed included website sustainability disclosure.

- Disclosure by retail companies tended to focus on environmental sustainability, employee engagement, human rights and supply chain management.

Mixed Levels of Sustainability Disclosure in Other Industries

Website sustainability disclosures were less common in other industries, with life sciences companies having the fewest disclosures:

- Seventeen percent of the life sciences companies surveyed (four out of 23) included some form of website sustainability disclosure. These disclosures focused mainly on environmental sustainability, community impact and philanthropy, and human capital management issues such as diversity and inclusions.

- Forty-six percent of the technology companies surveyed (13 out of 28) provided some form of website sustainability disclosure. Twelve of these companies included human capital management disclosures covering issues such as diversity and inclusion and employee engagement, and 10 included environmental disclosures such as emissions reduction and energy efficiency strategies.

- Fifty-six percent of the services companies surveyed (five out of nine) provided some form of website sustainability disclosure. These disclosures focused mainly on diversity and inclusion, employee training and engagement, and community impact.

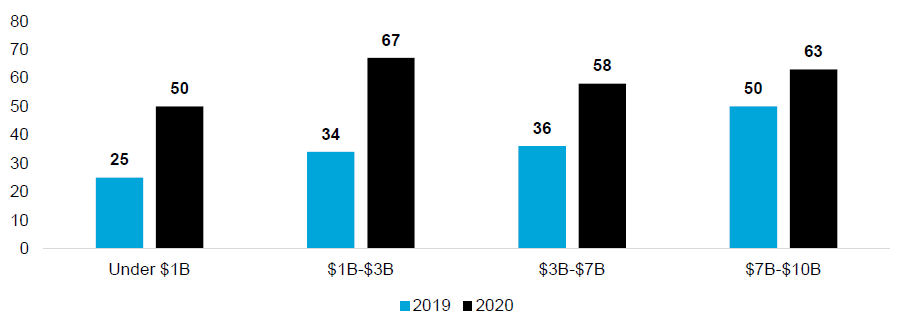

Market Cap Trends

In our survey, we categorized companies into four groups by market capitalization (“market cap”): under $1 billion; $1 billion to $3 billion; $3 billion to $7 billion; and $7 billion to $10+ billion. The number of companies with sustainability disclosures in each market cap group is shown in the chart above. Key trends are discussed below.

- Website sustainability disclosure by companies with a market cap under $1 billion jumped from 25 percent (four out of 16 companies) to 50 percent (nine out of 18 companies), the largest increase observed in our survey. While higher market cap companies are more likely to report on sustainability, the gap has narrowed considerably from the disclosure levels seen in 2019. This increase indicates that smaller companies are increasingly focused on sustainability, or at least are increasingly likely to provide public disclosures on these topics.

- Approximately 35 percent of the surveyed companies (seven out of 20 companies) with a market cap from $1 billion to $3 billion provided website sustainability disclosures, compared to 34 percent (12 out of 35 companies) in 2019.

- Approximately 58 percent of the companies surveyed (15 out of 26 companies) with a market cap from $3 billion to $7 billion provided sustainability disclosures, compared to 36 percent (eight out of 22 companies) in 2019.

- Approximately 63 percent of the companies surveyed (ten out of 16 companies) with a market cap from $7 billion to $10+ billion provided website sustainability disclosures. This is an increase from 2019, where 50 percent of the companies surveyed (five out of ten companies) in this market cap range provided sustainability disclosures.

Percentage of Companies Providing Sustainability Disclosure, by Market Cap 2019 vs. 2020

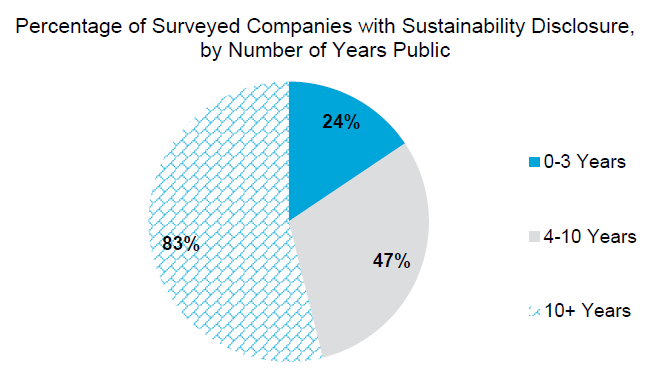

Disclosure Trends for Public Company Maturity: Length of Time Since IPO

The surveyed companies that have been public for a longer period were more likely to have website sustainability disclosures, with newly public companies being unlikely to have any sustainability disclosures.

- Eighty-three percent of the companies surveyed that had been public for more than ten years (19 out of 23) provided website sustainability disclosures.

- Forty-seven percent of the companies surveyed that had been public between four and ten years (17 out of 36) provided website sustainability disclosures.

- Twenty-four percent of the companies surveyed that had been public between zero and three years (five out of 21) provided website sustainability disclosures.

Percentage of Surveyed Companies with Sustainability Disclosure, by Number of Years Public

Use of Reporting Standards

Twenty-two percent of the surveyed companies with website sustainability disclosures (nine out of 41) disclosed the reporting standards with which they aligned their reporting. While the majority of these nine companies did not follow any one set of standards completely, they noted that they aimed to follow a certain set of standards or were guided by several different sets of standards in completing their report.

- Companies in the energy industry were by far the most likely to disclose the reporting standards they followed (eight energy companies and one technology company provided this information).

- The most commonly noted reporting framework was the Global Reporting Initiative (“GRI”) standards5 (six companies); the Sustainability Accounting Standards Board (“SASB”) standards6 and the Task Force on Climate-related Financial Disclosures (“TCFD”) recommendations7 (three companies mentioned each of these frameworks) were tied for second.

- Some of the surveyed energy companies also used industry-specific guidelines, such as the International Petroleum Industry Environmental Conservation Association’s (“IPIECA”) Oil and Gas Industry Guidance on Voluntary Sustainability Reporting and the American Gas Association’s voluntary sustainability metrics.

Institutional investors have been influential in the push towards the use of specific reporting frameworks. In January 2020, Larry Fink, the CEO of BlackRock, asked BlackRock portfolio companies to: (1) publish disclosures in line with industry-specific SASB standards by year-end; and (2) disclose climate-related risks in line with the TCFD’s recommendations, including a plan for operating under a scenario where the Paris Agreement’s goal of limiting global warming to less than two degrees is fully implemented. In 2021, BlackRock reinforced its support of the SASB and TCFD reporting frameworks and further asked companies to disclose a plan for how their business model will be compatible with a net zero economy – that is, one where global warming is limited to well below 2ºC, consistent with a global aspiration of net zero greenhouse gas emissions by 2050 – including how this plan is incorporated into the company’s long-term strategy and reviewed by its board of directors.

Below are examples of disclosure from the surveyed companies on the standards that guided their reporting:

Disclosure based on a variety of standards: “These additional sustainability disclosures provided in this report take into consideration various third-party ESG reporting standards and ratings, including [SASB], [IPIECA] and [GRI]. Further, our climate change strategy section aligns with the [TCFD].” [Energy company]

Disclosure based on industry standards: “The assessment followed a process as recommended by the Oil and Gas Industry Guidance on Voluntary Sustainability Reporting, published jointly by [IPIECA], the American Petroleum Institute (API) and the International Association of Oil & Gas Producers (IOGP). …. [Energy Company] also evaluated common reporting frameworks, including those of IPIECA and Global Reporting Initiative (GRI).”

Inclusion of Disclaimer Language

As more companies publish website sustainability disclosures, they are also beginning to include disclaimers on their websites and in their sustainability reports. Seven of the 41 companies surveyed that had website sustainability disclosures included disclaimer language. These disclaimers were generally similar to forward-looking statement language used in SEC filings, and many specifically referenced the risk factors in their SEC filings or directed readers to review them.

The inclusion of disclaimer language is appropriate in light of the potential liability associated with such disclosures, including under the anti-fraud provision of the U.S. federal securities laws (Section 10(b) of the Securities Exchange Act of 1934, as amended, and Rule 10b-5 promulgated thereunder), which apply to all public disclosures, regardless of whether or not they are contained in an SEC-filed document.

In order for a forward-looking statement legend to be effective, it is important to carefully tailor it to the information disclosed in the sustainability disclosures. This includes taking the following steps:

- Companies should carefully tailor the disclaimer language to specifically identify the forward-looking statements in the report. For example, one company in our survey stated: “All statements other than statements of historical facts, including information about sustainability goals and targets and planned social, safety and environmental policies, programs and initiatives, are forward-looking statements.”

- Companies should carefully tailor the disclaimer language to identify the specific factors that may cause actual results to differ materially from those in the forward looking statements disclosed in the website sustainability disclosure.

Moreover, the legend should make clear that any forward-looking statements are made as of the date of the report and that the company undertakes no obligation to update such statements.

Companies should ensure they do not label an ESG issue “material” if it is not included in the company’s SEC filings. Moreover, companies may wish to avoid use of the terms “material” or “materiality” in their website disclosures altogether; to the extent a company’s website sustainability disclosures use the term “material”, a separate legend should be provided that clarifies how the report is using this term. See our Considerations and Key Takeaways below for more information.

Sustainability Topics Discussed

The 41 companies with website sustainability disclosures frequently focused their disclosures on the following topics: human capital management (including diversity and inclusion, employee engagement and employee health and safety); environmental impact and risk management (including waste reduction); community impact; and ethical business practices, as more fully described below. In addition, disclosures regarding current social and economic issues were prevalent for companies both with and without website sustainability disclosures.

Human Capital Management

Human capital management (“HCM”) disclosures were the most commonly included type of website sustainability disclosure, with all but one of the 41 surveyed companies with website sustainability disclosure reporting on HCM in some form. This is a change from 2019, in which environmental disclosure was the most common type of website sustainability disclosure and reflects the increased focus from investors and the SEC on this issue.

For example, 2021 is the first year where human capital resource disclosure is required by the SEC, to the extent material, in annual reports on Form 10-K. On the investor front, BlackRock has asked companies in 2021 to provide disclosures that “fully reflect [a company’s] long-term plans to improve diversity, equity, and inclusion, as appropriate by region.” In addition, following a push by NYC Comptroller Scott Stringer, 40 S&P 100 companies have disclosed or have committed to disclose their EEO-1 data, which will result in the majority of S&P 100 companies providing such data.

Human capital management disclosures included information on diversity and inclusion (including 16 companies that provided at least some statistics on the gender and/or ethnic diversity of their workforce), minority-focused affinity groups, training and benefits, overall employee wellness and employee engagement.

Below are sample human capital management disclosures on websites from the surveyed companies:

Diversity and Inclusion (qualitative): “At [Energy Company], we aspire to attract a diverse group of employees and create an inclusive work culture where differences are valued. We want our employees to feel supported and encouraged to collaborate, learn and grow because we recognize [that] the unique perspectives and thoughts that all people bring to our environment stimulates innovation and generates out-of-the-box solutions that benefit our employee[s], clients, and industry.”

Diversity (quantitative): “30% of employees on [Energy Company’s] U.S. payroll self-identified as a member of an ethnic minority group in 2019, up from about 25% in 2015.”

Training: “At [Services Company] and across our brands we are committed to advancing our employees’ and consultants’ careers, through training and development that support both personal and professional growth…[W]e provide continued education, customized training programs and professional development…Our clients benefit from having a well-trained workforce, while our professionals gain enhanced skills and confidence.”

Health and Wellness: [Technology Company] “The health and wellness of our employees are paramount. We also strive to foster healthy lifestyles, promote work-life balance, and provide wellness support by: [i]ntegrating wellness spaces into all new office designs…[o]ffering flexible work hours and locations for exempt employees; [and] enhancing family leave benefits…”

Employee Engagement: [Energy Company] “We are a people driven company and as a result our employees are our greatest asset. We are committed to engaging our employees on our progress and core values that define us as a company. We believe that the more our people feel engaged and aligned to our business and goals, the more likely they are to invest and contribute to our success. We would not be the company we are today without our talented network of employees[;] it is critical that we demonstrate to them the importance of their contributions and value.”

Health and Safety

Health and safety disclosures were a prominent HCM disclosure topic, with 51 percent of the surveyed companies with sustainability disclosure (21 out of 41) including health and safety disclosures. These disclosures included information on workplace injury prevention, emergency preparedness, and safety trainings. Sample disclosures include:

Reducing Safety Incidents: “[Energy Company] operates in a culture committed to safety excellence. By fostering a zero-incident mindset, we believe that workplace incidents and injuries are preventable. The safety of our employees, contractors, customers, visitors, and communities is a core value. Working safely and looking out for the safety of others is an expectation and a basic responsibility of all employees and contractors at all times and at all locations.”

Employee Safety: “[Energy Company] designs, builds and operates our technologies with safety as a top priority. We have received multiple industry awards for technologies that reduce risks to personnel through automation, elimination of manual handling, and remote operation that keeps people out of the red zone.”

Environmental Disclosure

Environmental topics comprised the second most commonly included category of sustainability disclosure. Eighty-five percent of the surveyed companies with website sustainability disclosures (35 out of 41) included some information on their environmental practices or goals. Disclosures often focused on emissions reductions, renewable energy use, sustainable sourcing/operating, climate change and environmental impact.

Below are sample environmental disclosures from the surveyed companies:

Climate Change/Environmental Impact:

- “[Energy Company] has a strong commitment to managing our environmental performance. Our Environmental, Social and Governance (ESG) Steering Committee sets strategy and monitors environmental performance and issues, including climate-change related issues, to address stakeholder concerns….[Our] strategy [is] to continuously improve our environmental performance and to protect [our] social license to operate. [Our] environmental professionals work hand-in-hand with our business units to ensure our operations are environmentally sound and to comply with all laws, regulations and company policies.”

- [Energy Company] “We are committed to reducing fuel consumption and emissions at the wellsite through innovation, technology, and investment. Our core value of Innovate shows we are committed to a culture that works continuously to implement new, or improved, technologies and processes which can increase our sustainability and reduce our environmental impact.

- [Technology Company] “Our management approach emphasizes reducing consumption as well as using resources more sustainably through technology solutions. We’re focusing on reducing our energy usage, greenhouse gas (GHG) emissions, waste to landfill, and water usage. To ensure that we are advancing our sustainability performance, we use data management systems that allow us to accurately and efficiently collect data in key impact areas.”

- “At [Life Sciences Company], we believe that the reduction of the carbon footprint of the community benefits us all. We encourage our employees to walk and bike to work, or to enjoy reduced fees if they elect to take public transportation. Additionally, our solar panels, parking decks equipped with electric car charging stations, and office furniture constructed from renewable and environmentally-friendly materials, help to make our facilities as eco-friendly as possible.”

Goals or Commitments:

- [Retail Company] “We continued to work towards our science-based targets on climate, which we first announced in 2018 and which are aligned with limiting global temperature rise to 1.5°C above pre-industrial levels. We have committed to reducing our carbon emissions by 90 percent in our owned-and-operated facilities and 40 percent across our entire global supply chain by 2025, while shifting to 100 percent renewable electricity in our owned-and-operated facilities in that same time ”

- “[Retail Company’s] commitment to the RE100 initiative has increased the amount of renewable energy we source. We began sourcing renewable energy for our offices, distribution centers and stores in Pennsylvania and Ohio at the end of 2018 and have expanded to New York and Texas in 2019. This led to a 20% increase between 2018 and 2019…We continue to look for opportunities to source renewable energy for more of our facilities and expect to see this percentage increase year over ”

- [Technology Company] “Our Environmental Goals: 100% compliance with all applicable environmental laws and directives; Increase use of renewable energy sources and energy efficient equipment; Reduce waste and increase efficiency in our operations; Reduce the volume and toxicity of hazardous substances used in our processes; Engage employees to be fully aware of environmental practices and ”

Community Impact and Philanthropy:

Sixty-eight percent of the surveyed companies with website sustainability disclosure (28 out of 41) included disclosure on community impact and corporate citizenship. Sample disclosures include:

- “The [Technology Company’s] Foundation was established in 2015…to invest in our communities and to ensure that there would be support for efforts made in projects aligned with improving the lives of those where we live and work.”

- “[Technology Company] has [an] initiative with UNICEF USA to help provide lifesaving nutrition to [Company] also helped provide education supplies via UNICEF USA’s School in a Box inspired gift program.”

- “[Services Company] has always been and will always be a community of care and commitment. Our goal is to have a positive impact on our stakeholders and the communities we serve, through meaningful engagement, contribution and volunteerism.”

Ethical Business Practices:

Sixty-three percent of the surveyed companies with website sustainability disclosures (26 out of 41) included disclosures on ethical business practices, including human rights policies and supply chain management.

Sample disclosures include:

- “We scrupulously avoid conflicts of interest and always conduct ourselves ethically when dealing with customers and business opportunities…We prize [Technology Company’s] reputation for honesty, fairness, respect, responsibility, integrity, trust, and sound business judgment and know that no illegal or unethical conduct on the part of our employees is ever in the company’s best interest.”

- “[Energy Company] partners with suppliers who can support us in our drive to deliver high quality products and services to our customers, and who share our commitment to business conduct that not only complies with all applicable laws and regulations governing their business activities, but which also conforms to high ethical standards and accountability for quality, reliability, health, safety and the environment.”

Current Social and Economic Issues in Website Disclosure: COVID-19 and Black Lives Matter

Sixty-eight percent of the companies surveyed (54 out of 80) included website disclosures on COVID-19 and/or the Black Lives Matter (“BLM”) movement in separate press releases, in corporate statements or as part of a company’s broader website sustainability disclosures. Companies across all industries surveyed provided COVID-19-related disclosures, and overall these website disclosures focused on employee health and safety and business continuity planning; however, specific disclosures varied, with companies focusing on what was most salient for their particular business.

For example, website sustainability disclosures by retail companies typically discussed the process of closing stores or changing warehouse policies to meet customer demands. By contrast, companies in the service industry explained potential impacts to customers and ways that those companies were helping both customers and the community, including resources they were providing to meet changing needs resulting from the pandemic. COVID-19 has amplified the importance of employee health and safety among investors, even for those industries for which health and safety was not historically a focus. In addition, the pandemic has led to increased focus from investors on issues of business continuity and disaster response.

Disclosures regarding the BLM movement detailed corporate support for employees of color, workplace equity, community social justice and supporting diverse businesses and institutions. The trend in this disclosure reflects, in part, a recent push by investor groups. For example, the Council of Institutional Investors published a “call to action” for companies, noting that many of its investor members have supported greater diversity and fair workplace treatment for years. Similarly, the Interfaith Center on Corporate Responsibility is developing a formal position about racial equality and Ceres has stated that it is “reviewing all policies and practices to achieve a just and sustainable future for all people.” Some investors are also paying attention to which companies follow through on their anti-racism statements. For example, As You Sow is maintaining a database of companies that have published statements on the BLM movement and racial equality and stated that it plans to use the information gathered in its database to hold companies accountable if they fail to follow through.

Considerations and Key Takeaways

ESG continues to be at the forefront of governance and disclosure issues facing public companies today, and the ESG ecosystem continues to expand with the proliferation of sustainability reporting standards, guidelines, frameworks and rating systems. It may be daunting to tackle sustainability reporting for the first time or to embark on a meaningful expansion of the company’s disclosures, in part due to the variety and complexity of reporting standards available. This can be particularly true for smaller companies, with fewer resources and potentially less internal expertise and/or capacity for such an endeavor.

It is important to acknowledge that sustainability reporting can be a process that evolves and expands over time, and that some disclosure is generally better than no disclosure. Even if it means starting small, developing processes and controls around sustainability information and reporting will provide the backbone for sustainability reporting going forward. Companies considering launching or enhancing their sustainability reporting should consider taking the following steps:

- Identify Your Company’s Key Risks, Opportunities and Priorities. In deciding which sustainability topics to report upon and how to report on them, companies should first identify what is most important for them. Asking and assessing what the key risks, opportunities and priorities are for your company before starting to draft sustainability disclosure is crucial to producing effective sustainability reporting that will benefit your company. Some companies may do this through a formal assessment process, sometimes with the help of an outside consultant, to hone in on the topics most pertinent to their industry, business and stakeholders. Smaller companies should consider, and discuss within their sustainability disclosures, the scope and boundaries of the disclosure they are providing, and should prioritize giving detailed information to stakeholders on the sustainability topics most important to the company.

- Focus on Your Investors. One of the main drivers behind a company’s decision to begin sustainability reporting is often a company’s investor base. Understanding your investors’ views, which ESG topics they believe to be relevant to your industry and company and how they would want that information packaged are key to a successful reporting strategy. Your company’s investor base should help guide a wide range of items, including (i) when to begin reporting, (ii) which reporting frameworks to use, and (iii) which topics to cover. Several large institutional investors have disclosed what sustainability information or frameworks they prefer. Other investors will appreciate bespoke engagement by your team on these topics.

- Assemble the Right Team. ESG reporting is a multidisciplinary effort that can involve accounting, human resources, governance, investor relations, and legal and operations functions, among others. The right individuals and departments at your company should help (i) decide what information to report, (ii) gather the information for reporting, and (iii) review and vet the information drafted for disclosure.

In addition, it is important to keep senior management and the board of directors updated and involved throughout the process, as appropriate, as their support is critical to the success of the effort. In this respect, it may be important to provide internal education to directors and senior management to ensure they understand the strategic importance of sustainability disclosure to the company, the approach the company will be taking, and that appropriate company and employee resources will be devoted to the company’s sustainability reporting endeavors. Such education might also extend to employees in order for them to better understand the importance of any additional responsibilities they may be asked to take on.

- Be Committed to the Journey. Investors understand that ESG reporting is a journey and that different companies have progressed at a difference pace. Generally, investors want to (i) understand how companies are approaching governance over these issues and (ii) see measured progress in ESG Continuity among the individuals (or disciplines) that contribute to your ESG reporting will help establish systems for maturing disclosures and managing future reporting.

- Establish Controls Over Sustainability Reporting. The ESG information that is disclosed in voluntary sustainability reports must be accurate and consistent, as the SEC may actively compare the information your company voluntarily provides with any information disclosed in SEC filings. In addition, it is important to keep in mind that the anti-fraud provisions of the U.S. federal securities laws under Section 10(b) and Rule 10b-5 apply to all public disclosure, including disclosure on a public company’s website. Accordingly, companies should take steps to ensure that they have controls in place to effectively process, summarize, assess and review the accuracy of all of their ESG disclosure. Further, such controls should ensure that a company’s disclosure matches its actions in practice, as companies may face scrutiny from both governmental agencies and investors on this front.

- Don’t Forget Your Legends. Website sustainability disclosures could lead to potential liability, and it is therefore important to have counsel review the disclosures to reduce liability risk and include a forward-looking statement legend when providing new website sustainability disclosures. Such a legend should not be boilerplate or a duplicate of the legend provided in SEC filings but should be specifically tailored to the information disclosed in the sustainability disclosures to better protect the company from potential liability.

The complete publication, including footnotes, is available here.