Print

PrintSander de Boer is Senior Manager at KPMG in the Netherlands, and Julie Santoro is Partner at KPMG in the U.S. This post is based on a KPMG by Mr. de Boer, Ms. Santoro, Wim Bartels, Matthew Chapman, Maura Hodge, and Mark Vaessen. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance by Lucian A. Bebchuk and Roberto Tallarita (discussed on the Forum here); For Whom Corporate Leaders Bargain by Lucian A. Bebchuk, Kobi Kastiel, and Roberto Tallarita (discussed on the Forum here); Socially Responsible Firms by Alan Ferrell, Hao Liang, and Luc Renneboog (discussed on the Forum here); and Restoration: The Role Stakeholder Governance Must Play in Recreating a Fair and Sustainable American Economy—A Reply to Professor Rock by Leo E. Strine, Jr. (discussed on the Forum here).

A new EU proposal would significantly expand the scope of ESG reporting by companies operating in Europe.

Applicability

Proposal for a Corporate Sustainability Reporting Directive (CSRD)

EU-listed companies, and other companies operating in the EU that are ‘large’ (see definition below).

Fast facts, impacts, actions

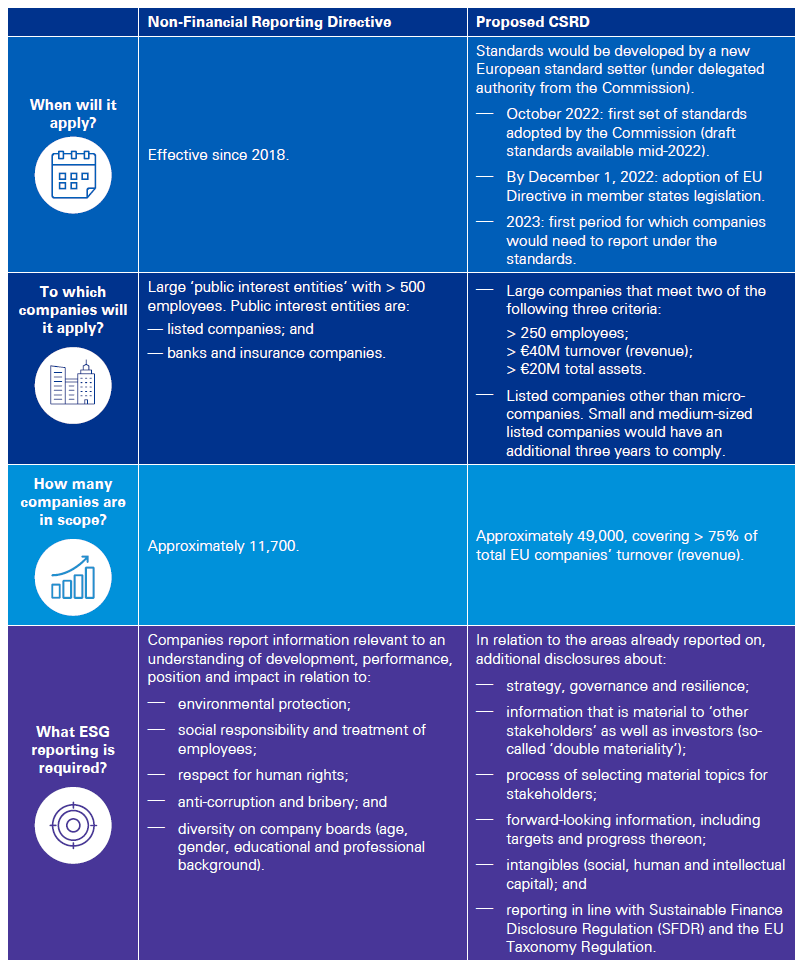

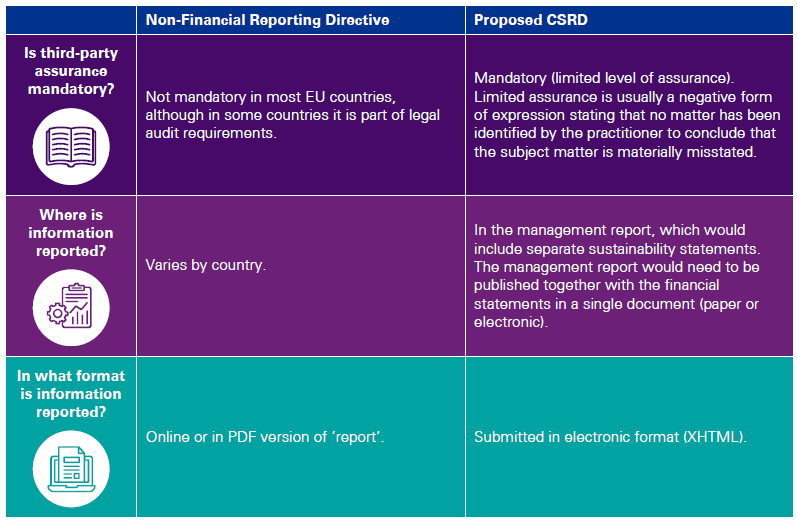

The following are key points about the proposed CSRD, which would amend an existing EU Directive and take effect in 2023. US companies with operations in the EU should take care to understand the effect of the proposed disclosures and related assurance requirements.

- Extended coverage. The current rules scope in ‘large’ public interest entities. The amendments would extend coverage to all ‘large’ (see new definition below) companies and all companies (other than micro-companies) with securities listed on EU-regulated markets; a three-year deferral would apply to small and medium-sized listed companies. These changes would extend the scope from under 12,000 to nearly 50,000 companies.

- Extended ESG reporting For companies reporting on ESG matters for the first time, the disclosures would be extensive, covering the environmental, social and governance categories of ESG. For companies already in the scope of the current rules (Non-Financial Reporting Directive), new disclosures would include information that is material for stakeholders other than investors, as well as disclosures about social, human and intellectual capital.

- New assurance The CSRD would introduce mandatory limited assurance over the ESG reporting (including the processes followed in preparing it). The scope may be extended to full assurance after three years.

Summary of requirements

The following table summarizes key differences between the existing EU Directive (2014/95/EU) and the proposed CSRD. The next step is for the European Commission to engage in discussions with the European Parliament and Council.

Alignment with global developments

Taken at face value, the proposed CSRD may appear to signal that the European Commission does not support the International Financial Reporting Standards Foundation’s initiative to create a new global Sustainability Standards Board that would set baseline ESG reporting requirements. However, the proposal requires the Commission to take account of other standards and frameworks for sustainability reporting in adopting standards, while also considering additional Europe-specific needs and public policy objectives.