Print

PrintDarragh Byrne, Marc Petitier, and Guy Potel are partners at White & Case LLP. This post is based on their White & Case memorandum. Related research from the Program on Corporate Governance includes Are M&A Contract Clauses Value Relevant to Target and Bidder Shareholders? by John C. Coates, Darius Palia, and Ge Wu (discussed on the Forum here); and The New Look of Deal Protection by Fernan Restrepo and Guhan Subramanian (discussed on the Forum here).

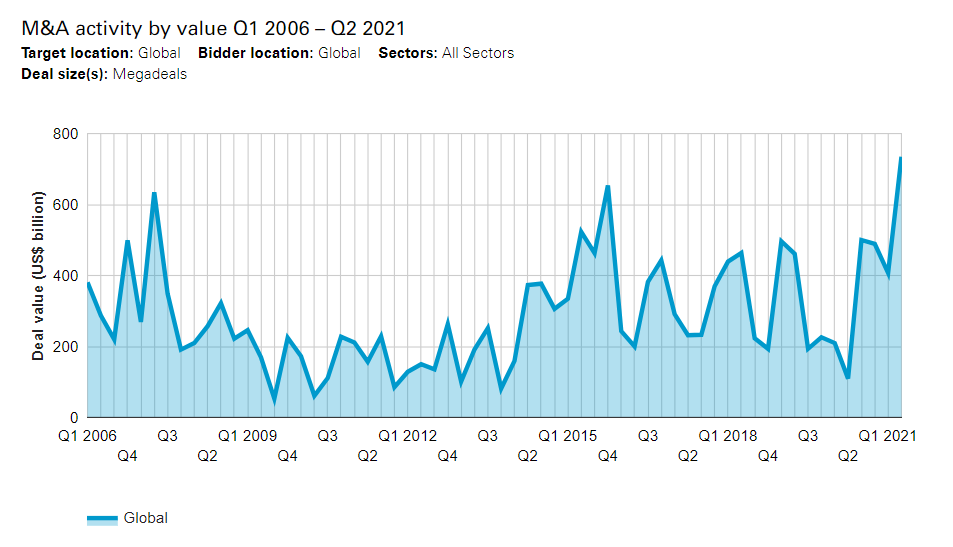

The second quarter of 2021 saw the announcement of megadeals (deals worth US$5 billion or more) totaling US$734.4 billion in value—more than in any other quarter on Mergermarket record (since 2006). Megadeal volume hit 45, the third-highest number in any quarter on record.

Activity at the top end was dominated by the US, with 25 megadeal transactions worth US$358.6 billion in Q2 targeting US-based companies. The largest of these was Discovery Inc.’s acquisition of Warner Media for US$96.2 billion, a ride on the bandwagon where traditional media players like Discovery and Warner seek to build scale—and a robust back catalog—to take on streaming mainstays like Netflix and Amazon Prime.

Although there were only 3 megadeal transactions in China in Q1, they totaled US$125.5 billion in aggregate—the highest total value for megadeal activity in China on Mergermarket record. Much of this activity was thanks to a single deal—the largest overall of the quarter—the US$111.5 billion merger between two Chinese infrastructure companies, Sichuan Railway Investment Group and Sichuan Transportation Investment Group.

Europe heats up

Although less active than the US or China, Western Europe as a region recorded US$91.3 billion in total megadeal value in the second quarter, for a near tripling of the total value in the same quarter in 2020. Volume nearly doubled, from 4 deals to 7.

The largest deal in Western Europe in H1 2021 was a US$35.3 billion proposed merger between Vonovia and Deutsche Wohnen. The transaction would see Germany’s two largest publicly listed property companies combine, and is among the largest-ever Germany deals on Mergermarket record.

The second-largest Europe transaction in H1 saw a consortium of investors led by Cassa depositi e Prestiti, an Italian state-backed investors’ consortium, grab an 88% stake in road operator Autostrade per l’Italia for US$21.8 billion. Such infrastructure deals have surged around the world as governments seek to jumpstart the economy following the pandemic.

The third top deal also involved a state-backed investment group: Suez, a French utility group, agreed to sell its domestic recycling and water utility businesses to a group of investors led by French state-backed group Caisse des Dépôts et Consignations for US$12.7 billion. The transaction cleared the path for Suez’s US$26.2 billion sale to Veolia, a France-based waste management services provider, while avoiding antitrust concerns in its domestic market.

Both the Suez and Autostrade per l’Italia deals also involved private money alongside state-backed investment. In the Autostrade deal, Cassa depositi e Prestiti partnered with Blackstone, KKR, Macquarie and F2i, while Caisse des Dépôts worked with Global Infrastructure Partners and Meridiam.

The number of deals exceeding the US$1 billion mark in H1 is also dramatically outpacing H1 2020 in a number of key European jurisdictions such as France (volume doubled from 5 to 10 deals), with the acquisition of Aviva France by Aéma Group and the proposed merger between M6 and TF1.

PE firms collaborate for bigger deals

Interest rates sit at historic lows, while private equity firms have record levels of dry powder, prompting PE and infrastructure investment groups to increase their appetites—and work together to buy out mega-targets.

In addition to the Autostrade and Suez transactions—the second- and third-largest buyout deals of Q2, respectively—the quarter also saw the largest PE buyout since 2007, the US$34 billion acquisition of medical supply manufacturer Medline by a consortium comprising Carlyle, Hellman & Friedman, Blackstone Group and Singaporean sovereign wealth fund GIC.

Healthy fundamentals drive megadeal surge

The buoyant activity at the top end of M&A is a sign of the high levels of liquidity and strong stock market performances as the world transitions out of the most acute period of dislocation caused by the COVID-19 pandemic. Very recently, concerns over a variant-driven pandemic relapse have taken some steam out of the markets, but it’s too soon to know whether the dip represents a blip or a trend.

In addition to piles of dry powder in the hands of private equity groups, corporations have been active in M&A, emboldened by both record-low interest rates and the strength of their stock. But since the strong M&A activity in H2 2020 and the first part of this year was fueled in part by pent-up demand as dealmakers came back to the table with transactions that had been paused last spring, this activity will likely taper off.

Instead, transactions will be fueled by looking to the future. The COVID-19 pandemic has accelerated many trends, among them digitalization and decarbonization, and has also prompted businesses to thoroughly examine their assets and determine where their core competencies lie and where to find growth.

All of these factors will continue to fuel megadeals in H2. Despite worries about rising inflation and emerging strains of coronavirus, dealmakers have proven their resilience and will not allow opportunities to make big investments and big changes pass them by.