Print

PrintLavender Yang is a PhD candidate in Accounting, Nicholas Z. Muller is the Lester and Judith Lave Professor of Economics, Engineering, and Public Policy, and Pierre Jinghong Liang is Professor of Accounting, all at Carnegie Mellon University Tepper School of Business. This post is based on their recent paper. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance (discussed on the Forum here) and Will Corporations Deliver Value to All Stakeholders?, both by Lucian A. Bebchuk and Roberto Tallarita; For Whom Corporate Leaders Bargain by Lucian A. Bebchuk, Kobi Kastiel, and Roberto Tallarita (discussed on the Forum here); and Restoration: The Role Stakeholder Governance Must Play in Recreating a Fair and Sustainable American Economy—A Reply to Professor Rock by Leo E. Strine, Jr. (discussed on the Forum here).

As economist John Kenneth Galbraith remarked in a 1994 interview, knowing someone is watching can make a difference in the behavior of the watched. It is not surprising, then, that societies seek to use monitoring and disclosure as tools to encourage desirable business practices, especially in the area of social responsibility such as businesses’ environmental impacts. Large-scale, mandatory Corporate Social Responsibility (CSR) reporting has been gaining momentum in recent policy debates. Back in 2020, a Commissioner of the Securities and Exchange Commission (SEC) argued for a move toward standardized Environmental, Social, and Governance (ESG) disclosures. As discussed in this forum, the Biden administration issued an executive order in January 2021 arguing for climate change-related disclosure in all economic sectors of the United States economy.

In a recent paper, we offer causal evidence regarding the impact of mandatory CSR-relevant disclosure on firms’ emission behavior. Specifically, we investigate whether a nation-wide mandatory reporting and disclosure requirement, the Greenhouse Gas Reporting Program (GHGRP), for plant level carbon dioxide (CO2) emissions, a principal greenhouse gas (GHG), affects subsequent emissions. To answer this research question, we exploit differential disclosure requirements under the GHGRP. This regulation requires all facilities in the U.S. that emit more than 25,000 tons of CO2 per year to report their CO2 emissions to EPA who, in turn, release the data to the public in a comprehensive and accessible manner under GHGRP. Our research design exploits a unique data opportunity. For the U.S. utility sector, both pre- and post-GHGRP emissions data are available for all power plants (including those emitting less than the 25,000 ton threshold). This context facilitates the use of quasi-experimental econometric designs to assess the causal effect of the GHGRP disclosure on firm behavior. Our specifications determine whether plants whose CO2 emission reports are required to be publicly disclosed through the GHGRP behave differently than those not subjected to the program. We hypothesize a reduction in the emission rates for plants covered by the GHGRP relative to those not covered.

We construct a sample of U.S. power plants that spans the years 2004 to 2018. The GHGRP was enacted in 2010, with the first reported data becoming available in 2011. The Emissions and Generation Integrated Database (eGRID) provides annual emissions of CO2 as well as generation of electricity for all power plants. The U.S. Plant ownership information is provided by the U.S. Department of Energy’s (DOE) Energy Information Administration (EIA). Our primary outcome variable of interest is the plant level emission rate, defined as CO2 (tons)/MWH.

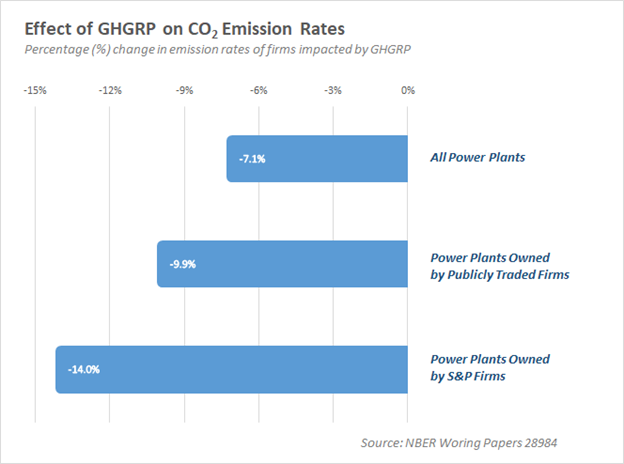

Our central empirical results are summarized as follows.

- First, we detect a significant reduction in CO2 emission rates for plants that are subject to the mandated disclosure requirements under the GHGRP. In our main specification, plants whose emission reports are disclosed through the GHGRP reduced their CO2 emission rates by 7%. The model controls for unobserved factors that may influence emission behavior. This result is robust to a number of different specifications.

- Second, the reduction in emission rates is 10%, a larger magnitude, for plants owned by publicly traded firms. Further, membership in the Standard and Poor’s (S&P) 500 suggests an even larger effect of 14%. These results are consistent with public or shareholder pressure to reduce emission intensities working through capital market channels.

- Finally, we find evidence of strategic behavior in firms that own multiple plants: companies that own facilities which are covered by the GHGRP, as well as facilities below the reporting threshold, reduce emission rates at plants covered by the GHGRP while increasing the CO2 discharge rates at plants below the reporting threshold. This effect is large: emission rates increase at non-disclosure plants by between 25% and 56%. This form of emission leakage provides direct evidence that firms find GHGRP disclosure costly.

Within the utility sector, our study focuses on the impact of a specific role of mandated environmental-related disclosure: raising the profile of emission information to the public. For the utility sector, emissions data prior to the GHGRP were collected and reported to the U.S. DOE, including those plants below the eventual GHGRP reporting threshold. These data were indeed available to the public but in a less accessible manner than under the GHGRP. Finding, cleaning, and analyzing these data prior to the establishment of GHGRP would have been considerably more costly than afterwards. The GHGRP provides more accessibility, standardization, comparability, higher frequency reporting, and overall a higher national prominence of the emissions data reported by the treated plants. Thus, to the extent our econometric results demonstrate causal evidence, the effect is caused by the raised profile of the emission information, not necessarily the creation of altogether new information.

This paper highlights the importance of how information disclosure occurs. First, we demonstrate that a nationwide disclosure program affects firm behavior. Second, the paper shows that reporting thresholds present the opportunity for leakage which attenuates net emission reductions. Third, the behavioral changes observed herein firmly support the notion that companies expect relevant stakeholders to respond to new information in ways that the firms would like to avoid. As such, our paper makes the case that standardized, mandatory CSR reporting (without thresholds) has the potential to induce large-scale changes in firm behavior that may have appreciable social benefits.

In short, in our context, one may refine Professor Galbraith’s observation by adding that it makes a real difference when power plants know someone is watching and that what is seen is easily and widely accessible for all who seek it.

The complete paper is available for download here.