Print

PrintJess Gaspar is Director of Research for Multi-Asset Solutions and Sara Rosner is the Director of Environmental Research and Engagement on the Responsible Investment team at AllianceBernstein. This post is based on their AllianceBernstein memorandum. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance by Lucian A. Bebchuk and Roberto Tallarita (discussed on the Forum here); Companies Should Maximize Shareholder Welfare Not Market Value by Oliver Hart and Luigi Zingales (discussed on the Forum here); and Reconciling Fiduciary Duty and Social Conscience: The Law and Economics of ESG Investing by a Trustee by Max M. Schanzenbach and Robert H. Sitkoff (discussed on the Forum here).

The Starting Point: Setting ESG Tone from the Top

It’s not uncommon for stakeholders in large organizations to have different views on the meaning of ESG and the importance of its pillars in defining organizational success. That’s understandable, and in fact, diverse perspectives can be a source of strength when making investment decisions.

Ultimately, though, leaders must reach consensus on tangible ESG objectives and expectations. This process requires answering weighty questions: How material a driver will ESG be to our investment success? How heavily should we weight ESG and financial considerations in our asset allocation? Are all ESG pillars equally important, or will our emphasis on individual pillars differ?

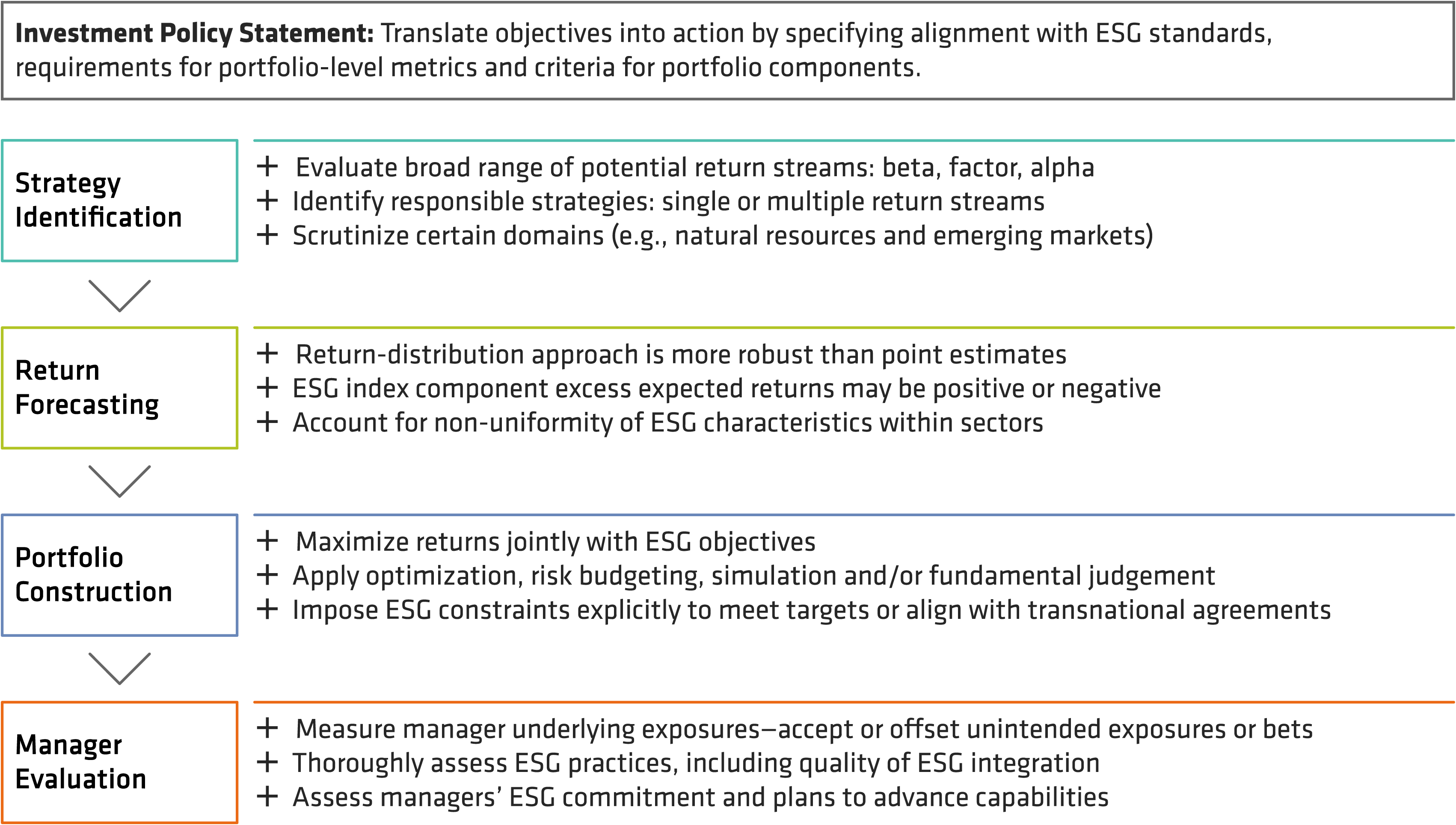

The Investment Policy Statement: Codifying ESG Guidance

A concrete investment policy can translate the answers to those questions into specific portfolio-level ESG objectives and actionable guidance for asset allocation. The investment policy statement (IPS) is the touchstone in communicating this input to shape the allocation blueprint, typically transmitted through three conduits:

- Alignment with ESG standards: A mandate to adhere to regional or global ESG standards by a specific date can help align a portfolio’s investment process with organizational ESG objectives. Relevant standards might be the Paris Agreement to limit global warming well below 2C, reaching net-zero CO2 emissions by 2050 or perhaps the European Union Sustainable Finance Disclosure Regulation (EUSFDR) Articles 8 or 9. Organizations may need to tailor standards that are too narrow (such as the Paris Agreement) or not specific enough (EUSFDR).

- Requirements on portfolio metrics: The IPS might enforce minimums or maximums on portfolio ESG characteristics based on third-party metrics such as carbon intensity or ESG scores—absolute or relative to a benchmark—in order to steer capital toward ESG-friendly strategies. This effort might result in a barbell, with low-ESG issuers on one end and high-ESG issuers on the other. A broad high-yield bond allocation, for example, would likely skew more energy-intensive, with a generally lower ESG score that might need to be countered elsewhere in the allocation or refined through guidelines.

- Criteria for portfolio components: The IPS can stipulate acceptable characteristics for portfolio components—including securities, issuers and investment strategies. Limits on security ratings, issuers’ economic activities or strategy objectives might even help address an ESG barbell condition in the portfolio. For example, ESG restrictions on issuers might exclude heavier carbon emitters from a high-yield bond allocation.

Of course, an IPS can use all three conduits in developing a robust framework that features top-down alignment, benchmarked portfolio standards and individual security criteria. When an IPS includes specific expectations for measuring, monitoring and managing portfolios toward these objectives, it can bring an asset allocation fully in sync with high-level ESG goals.

Strategic Asset Allocation: The ESG Focal Point

Both strategic and tactical asset allocation ultimately matter in portfolio construction and management—but in our view, strategic allocation should be the focal point for ESG. Tactical decisions on building blocks such as European, US or Japanese equities will likely be only marginally influenced by highly persistent ESG scores.

Of course, it makes sense to avoid major geopolitical and other risks tactically, but climate change, social equality and better governance are long-term propositions that require a strategic approach. This makes strategic asset allocation the focal point in translating long-term IPS guidance on ESG into multi-year asset allocations, in a process (Display) that can be segmented into four steps: identifying strategies, forecasting returns, constructing portfolios and evaluating managers.

Step One: Identifying Relevant Investment Strategies

The range of potential building blocks for multi-asset investors is incredibly broad, including betas such as equity, duration and real estate as well as factors such as value, growth and carry. Alpha exposures including security selection and market timing round out the set.

Responsible investment strategies can include any single return stream or combination of return streams. An active, low-carbon equity strategy, for instance, might include equity beta, quality and low-volatility factors, and idiosyncratic alpha from concentrated security selection.

When identifying investment strategies, some domains and strategies warrant greater ESG scrutiny. For natural resources and emerging markets (EM), ESG opportunities and risks are more dispersed. A natural resources issuer might be involved with a traditional heavy carbon –emitting source or a disruptive renewable source (perhaps even within the same firm!). In EM, generally weaker governance leads to more diverse ESG profiles (Display).

Step Two: Forecasting Expected Return Drivers

Once a portfolio team has identified appropriate return streams, it can isolate and forecast the drivers of expected returns, risks and correlations. In our view, employing a return-distribution approach makes the process more robust than point-return estimates.

Bear in mind that expected returns for ESG index components don’t have to be positive. If ESG hasn’t yet been fully priced into markets, and if flows continue to support a strategy, expected alpha could be positive. In contrast, an organization may wish to promote socially positive activities in segments where markets have already priced out alpha, so the risk/return trade-off from higher portfolio concentration in those segments could be negative.

Return forecasts must account for a lack of uniformity in ESG characteristics within sectors. Natural resources, for example, include both backward-looking fossil fuel strategies and forward-looking renewable strategies. Backward-looking strategies will likely rate lower on ESG but offer alpha potential from issuers who improve their ESG practices. They’re also more likely to have a value tilt, while forward-looking issuers tend to be more growth oriented.

Step Three: Constructing an ESG-Aligned Portfolio

Using inputs from the previous steps, portfolio construction seeks to design a portfolio that maximizes expected returns subject to stated objectives and constraints, including ESG guidance. The engine for portfolio construction varies: mean-variance optimization, risk budgeting, simulation and fundamental judgment are among the choices.

ESG can be incorporated at this step as an explicit objective—perhaps maximizing a portfolio’s score or minimizing carbon emissions—alongside maximizing risk-adjusted returns. ESG-related constraints can also be plugged in to guide the outcome. For example, minimum ESG scores might be specified for the overall portfolio, asset classes or even individual strategies.

Allocation ranges can be specified for ESG-integrated strategies, levels of ESG scores or carbon emissions. In each case, specific objectives or constraints can be configured to align a portfolio with transnational arrangements, such as the EUSFDR Article 9 or the Paris Agreement.

Step Four: Evaluating Underlying Investment Managers

Once the portfolio blueprint is finalized with generic investment strategies, the portfolio team begins selecting the specific investment managers best equipped to deliver what’s needed from each building block. Individual managers’ risk/return exposures must be assessed individually versus their benchmarks and collectively to form a coherent portfolio.

For instance, an allocation might call for a low-carbon indexed strategy—fillable by a passive exchange-traded fund or active manager. Underlying risk exposures (such as value or growth) may differ from the index. Security-selection alpha might also be embedded, from high-conviction fundamental or systematic quantitative managers. Multi-asset portfolio teams must measure exposures, accepting or offsetting unintended ones with a complementary manager or overlay.

To ensure alignment with the IPS, portfolio teams must thoroughly vet managers’ ESG practices. If the IPS formally outlines manager expectations, it can serve as the ultimate basis for monitoring and measuring ESG results. Common metrics used include proprietary or third-party ESG scores, quantity and quality of issuer engagements, and expected improvement in ESG scores of managers’ holdings.

In terms of ESG-integration quality, the depth of integration an organization expects or accepts from managers is an important bar. Passive strategies may be cost efficient but also rudimentary in ESG integration. Active quantitative strategies can offer solutions for a wide range of ESG objectives and constraints. Fundamental managers frequently bolster engagement efforts as a way to drive better alpha and ESG outcomes.

Finally, investors should look at not only where managers are today but where they’re headed, because responsible investing continues to evolve rapidly. Climate change–scenario analysis, for instance, is rapidly becoming a priority, and we think this capability should be squarely in managers’ sights, despite the resources required and the still-developing nature of the technology and tools.

The Big Picture: Alignment Matters

For multi-asset investors, achieving targeted portfolio outcomes requires strong planning and effective implementation. These processes may be well understood for traditional risk and return considerations but may be less ingrained for the ESG dimension of asset allocation.

It’s not a simple task to secure end-to-end organizational ESG alignment, especially given the multitude of approaches, but the complexity of the task is exactly what makes alignment so valuable: upstream clarity limits downstream confusion. Even the best intentions can fall short without clear expectations and tangible metrics.

With a clear mandate and comprehensive approach, strategic asset allocation can improve the odds of achieving organizational ESG objectives. In our view, an organization’s IPS is the best place to hardcode ESG expectations.