Print

PrintMatteo Tonello is managing director of ESG at The Conference Board, Inc. This post is based on a The Conference Board/ESGAUGE memorandum, in collaboration with Russell Reynolds Associates and The Rutgers Center for Corporate Law and Governance, by Mr. Tonello, Paul Washington, and Merel Spierings.

Introduction

The 2021 proxy season was unprecedented, with record support for shareholder proposals on environmental and social (E&S) issues, growing opposition to director elections, and significant support for governance proposals, especially at midsized and smaller companies. [1]

The season was unpredictable as well. Not only did institutional investors move faster than ever before to implement their views through their voting—thereby often getting ahead of proxy advisory firms and leaving companies with little time to adjust their practices—at times they surprised boards and management teams by voting against the company’s position after what seemed to be positive discussions.

This shift in voting practices is expected to continue into 2022 and should be considered in the context of the related underlying shifts currently underway in corporate America: changes in both “what” companies are supposed to address (that is, the ever-growing array of environmental, social & governance (ESG) issues) and “who” (that is, the shift toward multistakeholder capitalism in which companies are placing a higher priority on serving the long-term welfare of constituents, such as employees, beyond their shareholders). [2] Major institutional investors, especially those with large passive index funds, have embraced these shifts toward a focus on ESG and a multistakeholder model, and that is coming through in their support for E&S shareholder proposals. [3]

But institutional investors are not the only driving force here: the ongoing COVID-19 pandemic and the current US administration’s agenda have accelerated the focus on E&S issues. And in many ways, investors are responding to mounting pressures from their own upstream clients. This means the proxy season has become an arena where the broader evolution of the role of the corporation in society is playing out. In that broader context, there is no single correct answer for what companies should do. But this post and its six supplemental briefs highlight what to expect in the coming proxy season and—perhaps more importantly—suggest steps boards and CEOs can take to prepare.

Insights for What’s Ahead

Environmental & social proposals in general

Companies should brace for a challenging E&S shareholder proposal season in 2022. Expect more E&S proposals across all industries—driven by the success of such proposals last year—and for more E&S proposals to come to a vote as emboldened proponents see less incentive to negotiate a withdrawal of their proposals. And anticipate more support for proposals that do go to a vote, due not only to the growth in ESG funds, but also the increased incentive and willingness of major institutional investors—pressured by their own clients to make strides on ESG and evaluated on how they vote—to support such proposals.

But CEOs and their management teams can take several steps to prepare their boards:

- Start planning now to involve directors proactively in engagement with shareholders and on an ongoing basis—not only in response to a crisis. Also be sure directors can demonstrate fluency in ESG issues. Investors increasingly expect board members to be able to talk about E&S as well as G subjects.

- Ensure directors are well versed not only in the firm’s main ESG risks and opportunities, but also how the company compares to peers.

- Inform directors on the ESG issues their key investors care about most—and prepare them for the different expectations investors may have on some of these issues.

- Conduct mock meetings to prepare directors for in-depth engagement meetings with investors—and be sure they are prepared for tough questions.

- Analyze institutional investors’ proxy voting guidelines and policies now to ensure proxy statement disclosures (and other communications) address the issues their key investors care about.

- Ask institutional investors about their views on your firm and their evolving thinking about E&S issues in general during the “off season.” If you wait until their voting guidelines are issued, it may be too late for the board to take action that can be reflected in the proxy statement.

- Ramp up ongoing engagement efforts with institutional investors, despite the challenges the COVID-19 pandemic presents in building and maintaining relationships. While both companies and investors are hard pressed for time, there are still opportunities for constructive dialogue. Companies should be mindful that more investors 1) are becoming interested in ESG, 2) are expanding their stewardship teams, 3) have significant turnover, and/or 4) include portfolio managers in engagements, so companies will want to educate these “new faces” on their approach to ESG.

- Engage your major investors—old and new—not just during the regular “proxy season” but also during “off season” engagement calls to let them know what ESG issues you’re focusing on, why you’re focusing on those issues, and what your plans are.

- Expand engagement strategies to reach audiences beyond their major institutional investors. Investors’ upstream clients are increasingly interested in ESG—and are making their voices heard. [4] And retail investors, who are becoming more influential but don’t always have the same focus as their institutional counterparts, need to be educated as well. It is therefore vital that these stakeholder groups be brought along on the company’s ESG journey.

- Implement processes for identifying emerging trends with different stakeholder groups and adopt engagement strategies for each group. While some stakeholders might prefer formal communication, others might prefer to engage through public channels.

- Adopt a retail-facing strategy to help promote retail investors’ participation in the proxy voting process. Companies may want to gain access to retail investor data to better understand who their retail investors are, what their sentiment and voting behavior is on key issues, and where and how they can best engage and educate them on ESG issues (e.g., on social media or digital trading platforms, online finance communities, or through retail investor events).

- Ensure the board knows that a new (and potentially more intense) wave of E&S proposals is coming—and with it a greater chance of negative votes from traditionally supportive investors—and understands which proposals are likely to gain majority support unless the board commits to fulfilling them to the letter. This can help prevent the board from being surprised or blindsided.

- Make the board understand that a successful proxy season is no longer about minimizing the number of proposals that go to a vote. Instead, a successful proxy season is measured by the more qualitative judgment of whether the firm has maintained a constructive ongoing dialogue with the firm’s major investors, which is more important than any vote on a precatory shareholder proposal.

See Brief 1: Environmental & Social Proposals in General for more shareholder voting trends and insights.

Human capital management proposals

The sustained focus on racial, gender, economic, and health equality and fairness means companies should expect a continued push by shareholders on human capital management (HCM) topics, with a strong focus on diversity and increased attention to disclosure. Many investors will continue to advocate for more HCM disclosure through engagement and shareholder proposals, especially since any new SEC rules on HCM and board diversity disclosure will take effect after the 2022 proxy season. EEO-1 data disclosure, workplace diversity, and employee arbitration will continue to be major topics of discussion. Additionally, anticipate a greater push on board diversity that will increasingly spill over into director elections, as proxy advisors and investors continue to make their voting guidelines relating to issues such as board diversity more stringent.

To address these issues and to reduce the likelihood of HCM shareholder proposals succeeding, CEOs and boards can take several steps:

- Develop and adopt a board-approved HCM strategy that is integrally tied to the business strategy and sets forth a plan for taking the company from the workforce it currently has to the one it will need in the coming years.

- This involves identifying the key areas where the company’s workforce drives business success, evaluating the firm’s current capabilities in those key areas, assessing the broader trends and competitive environment for talent, setting clear goals, and choosing metrics to report progress.

- Clarify and codify the board’s role with respect to HCM—and ensure it demonstrates its own commitment in this area, particularly through long-term director succession planning that prioritizes board diversity and provides enough lead time to identify, recruit, and onboard directors with the appropriate diversity of thought, experience, and background. [5]

- Boards have multiple levers with respect to HCM, including the selection, promotion, and compensation of management; approval of workforce policies; review of key disclosures; and general oversight and advisory powers. It is pivotal that these levers be deployed in a concerted manner.

- Ensure governance guidelines, as well as committee charters and policies, reflect the ways directors engage in HCM. Often, governance documents don’t keep pace with the good practices companies already have in place.

- Accelerate the diversification of the board 1) through the director search process (e.g., by adopting the “Every Other One” strategy that sets a target of recruiting women for one of every two board seat openings, as well as by defining search criteria based not on job title but on a set of skills and experiences) and 2) by adopting or more strictly adhering to policies that foster board refreshment (e.g., reducing overboarding, lowering average tenure of directors, not making exceptions to a mandatory retirement policy). [6]

- To meet investors’ increasing demands on board diversity, boards should aim for gender parity and substantial minority representation on their boards.

- Consistently communicate the company’s HCM story—beyond diversity—through various channels (10-K, proxy, ESG or stand-alone HCM reports, and website) and via shareholder engagement.

See Brief 2: Human Capital Management Proposals for more shareholder voting trends and insights.

Environmental proposals

With climate change front and center on the SEC’s and investors’ agenda—and proponents encouraged by the success of climate-related proposals last year—companies across all industries should anticipate a sustained push on climate issues as well as on broader environmental topics. Shareholder activism on environmental issues is expected to continue beyond shareholder proposals, especially after the successful proxy fight against ExxonMobil, in which Engine No.1—a small hedge fund—won three director seats at the energy giant with the goal of, among other things, implementing more forceful decarbonization strategies. Other tactics, such as vote-no campaigns against directors, are also likely to increase. In fact, proxy advisors and investors are updating their proxy voting guidelines and adopting policies to hold directors accountable for what they perceive to be ineffective oversight of ESG issues, especially as it pertains to climate change.

To avoid the risk of shareholder activism with a big “A”—that is, efforts aimed at altering the company’s strategy or its board—CEOs and boards may want to consider:

- Providing more detailed—and where possible forward-looking and quantitative—disclosure of the company’s governance, strategy, and risk mitigation efforts regarding environmental issues, including a capital expenditure program in line with its greenhouse gas (GHG) emissions reduction commitments.

- Consider disclosing in accordance with the Sustainability Accounting Standards Board (SASB) and Task Force on Climate-Related Financial Disclosures (TCFD), as these are among the frameworks that are primarily geared toward and therefore generally favored by investors.

- Assessing how their supply chain can affect, or be affected by, biodiversity loss and deforestation, as well as assessing their exposure to water-use risks.

- Understand that the financial cost of inaction can significantly outweigh the cost of mitigation. [7]

- Demonstrating responsiveness to investors’ concerns by enhancing climate-related performance and disclosures even when not yet in line with peers or with Paris Agreement emissions reduction targets, strengthened at the UN Climate Change Conference of the Parties (COP26) in Glasgow in late 2021. [8]

- Through shareholder engagement and company disclosures, boards can convey they are taking investors’ concerns seriously and state the company’s plans (not just goals) to reduce Scope 2 and 3 emissions—even if they are not there yet.

See Brief 3: Environmental Proposals for more shareholder voting trends and insights.

Corporate political activity proposals

Corporate political activity was under intense scrutiny in 2021—and it will continue to be in 2022. The immediate and unprecedented success of the new proposal on climate-related lobbying—which asks companies to explain how their lobbying efforts align with the Paris Agreement—emphasizes that companies need to strengthen their climate-related disclosures and match their climate-related statements and commitments with consistent action on the policy front. At the same time, proposals on political contributions are evolving—from seeking disclosure on companies’ campaign financing policies and practices to asking firms how their political expenditures align with their stated corporate values. Moreover, proposals on traditional lobbying—typically asking for disclosure on companies’ lobbying policies and practices—will remain an area of tension between shareholders and companies, especially those whose lobbying efforts contrast with their positions on broader E&S issues.

To address these issues and prepare for shareholder proposals on political contributions, traditional lobbying, and climate-related lobbying, CEOs and boards can take concrete steps, including:

- Increasing board oversight—not only of their corporate contributions but also of their lobbying and other political activities. The board’s role might include approving broad principles and processes for corporate political activity.

- Some companies may choose policy over politics and decide to limit, or avoid engaging in, political contributions altogether given today’s intense political polarization and ever-greater scrutiny of corporate political activities.

- Ramping up educational and engagement efforts with key audiences—and expanding disclosure to investors and other stakeholders regarding their firm’s types of political activity and the policies and controls in place.

- Focus on employees—they were a significant driver in making corporate political activity challenging in 2021—and investors.

- Clarify the role of political action committees (PACs). The press, employees, and others conflate corporate giving and PAC giving, even though corporate-sponsored PACs are funded by voluntary contributions from employees, not by corporate funds.

- Clarify the process for deciding whether and how to communicate PAC decisions, including changing contribution criteria—and be mindful that the legal, communications, and government relations functions may have conflicting views on publicizing PAC decisions.

- Aligning political contributions and lobbying with corporate values and vetting all political activity to ensure their public policy positions are aligned with their broader corporate citizenship positions.

- Keep it simple: the more complex the corporate political activity, the more difficult it may be to manage reputational risk.

- Rigorously vet third-party organizations to which the company donates money, including the governance process in place to control their activities, and ask for reports on how they are using company funds.

- Consider involving the corporate citizenship function in reviewing political activity.

- Adopt (or have your PAC adopt) a policy for political contributions that incorporates the company’s and employees’ values as part of the framework for managing political activities.

See Brief 4: Corporate Political Activity Proposals for more shareholder voting trends and insights.

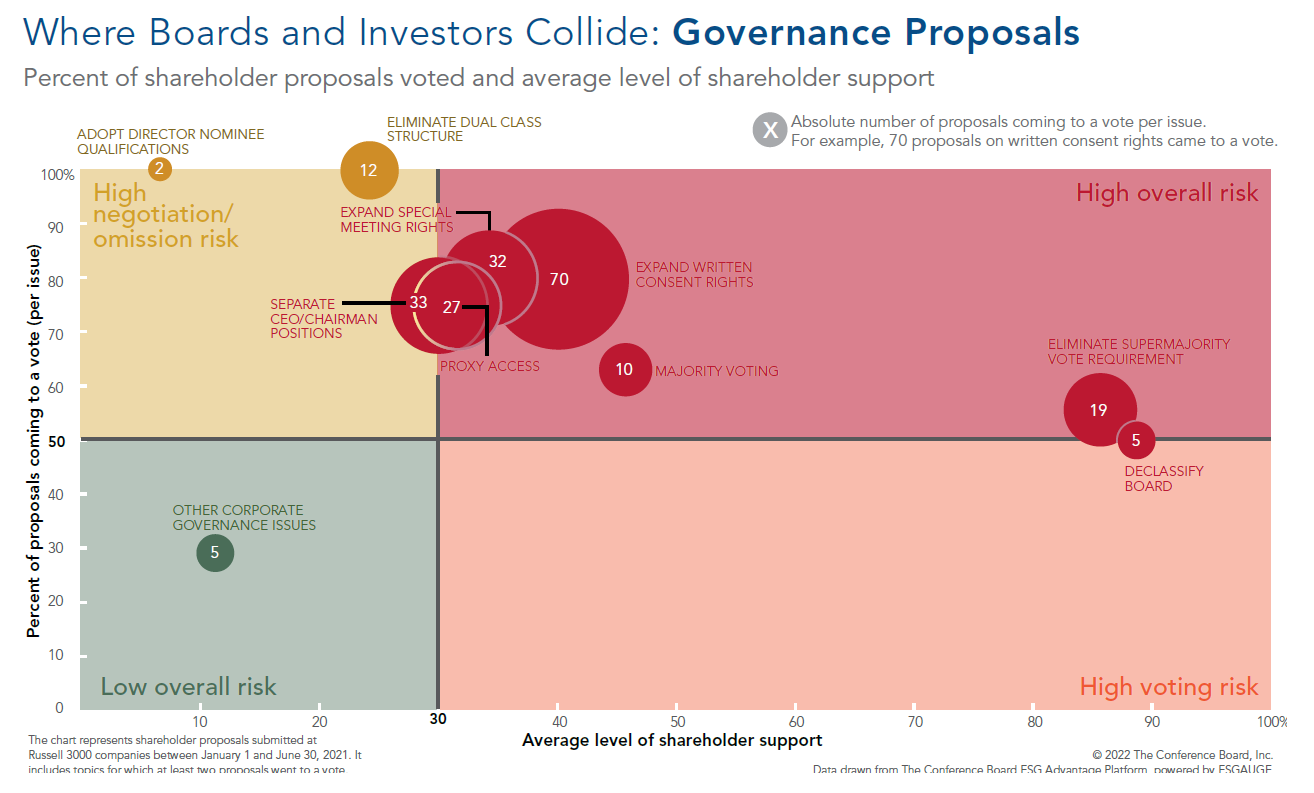

Corporate governance proposals

Corporate governance continues to be a hot topic for shareholders, as demonstrated by the success of governance-related proposals in the 2021 proxy season. CEOs and boards, especially at midsized and smaller companies, should consider revising their governance practices to align with common practices among companies with larger market capitalization, such as expanding special meeting rights and written consent rights, declassifying the board, or eliminating the supermajority voting requirement.

Companies that are out of alignment with long-standing investor expectations in these areas should be prepared to have such proposals pass—or come close to passing. By removing wedge issues, companies are less likely to be exposed not only to shareholder proposals but also to big “A” activism aimed at altering the company’s strategy or its board.

See Brief 5: Corporate Governance Proposals for more shareholder voting trends and insights.

Company-sponsored proposals

Shareholders continue to scrutinize the largest companies for their executive compensation practices, and they are increasingly holding smaller companies to account for their governance practices. Expect negative say-on-pay votes, especially at the largest companies that don’t provide sufficient context and detail on executive compensation decisions. When it comes to governance practices—including board composition and oversight of ESG issues—shareholders perceive smaller companies to be lagging their bigger counterparts, as evidenced by significant opposition to director elections at those companies. This trend is expected to continue in 2022, as proxy advisors and investors have updated their proxy voting guidelines and policies for 2022 to hold directors accountable for what they see as lack of board diversity and effective ESG oversight.

See Brief 6: Company-Sponsored Proposals for more shareholder voting trends and insights.

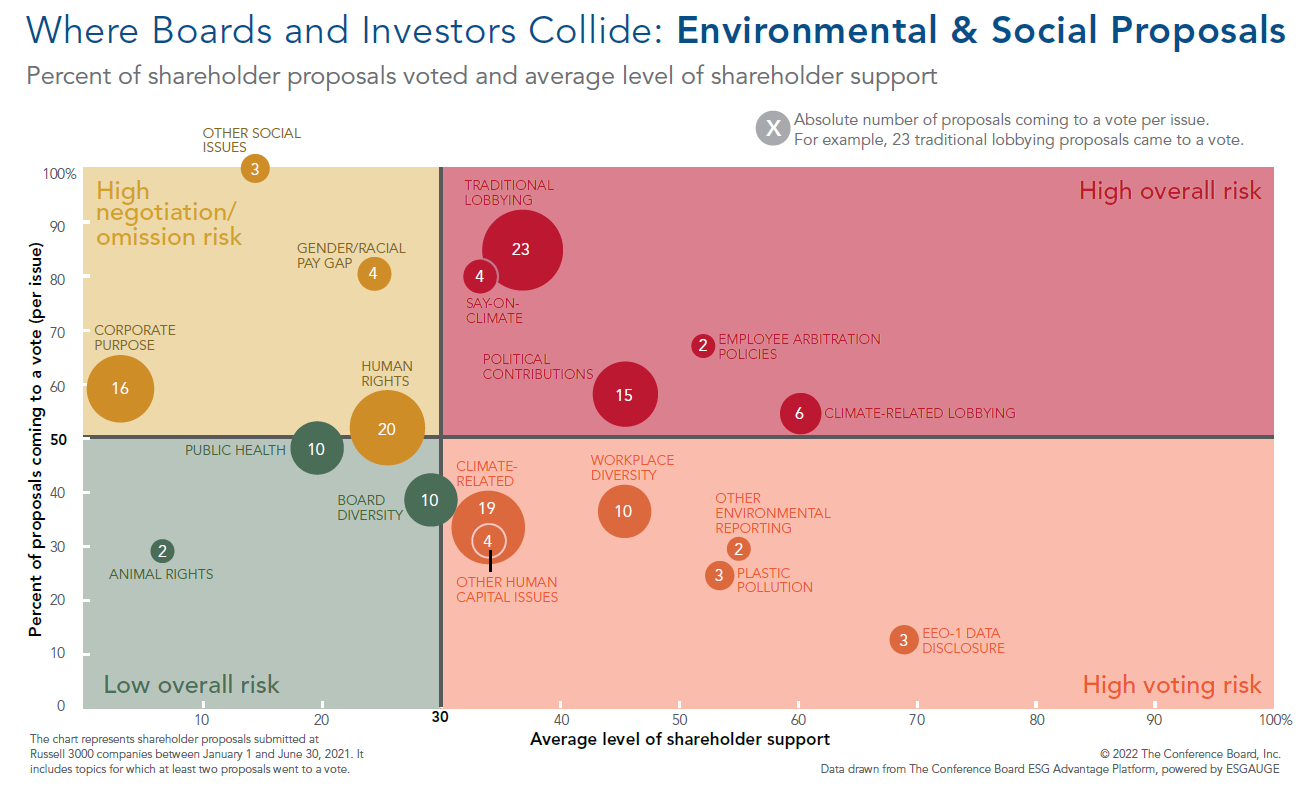

Where to Expect the Most Tension in the 2022 Proxy Season

Several factors lead to a challenging proxy season for companies:

- The number of shareholder proposals that investors submit, which is expected to increase this year;

- The number of proposals going to a vote because of the difficulty of negotiating proposal withdrawals or omitting them through the no-action letter process; [9] and

- The level of support for those proposals that come to a vote.

The following charts map the E&S shareholder proposals and the governance proposals from the 2021 proxy season against these three dimensions and indicate which topics are most and least likely to cause tension between companies and investors in the 2022 proxy season.

For proposals on topics that fall above the Y-axis demarcation line, it was relatively difficult to negotiate a withdrawal or have it omitted. Proposals on topics that sit right of the X-axis demarcation line received high levels of shareholder support when voted on. And along the borders are the topics that could very well migrate into the red zone this upcoming proxy season.

- Upper right-hand quadrant: Shareholder Proposals in the Red Zone

- Proposals on topics that were hard to get withdrawn or omitted and that received high levels of shareholder support when going to a vote.

- These proposals will very likely continue to create the most friction between companies and proponents, so boards will want to make engagement and disclosure on these topics, especially on corporate political activity, a high priority.

- Lower right-hand quadrant: Shareholder Proposals in the Orange Zone

- Proposals for which it was somewhat easier to negotiate a withdrawal or seek their omission but still received high levels of shareholder support when going to a vote.

- These topics will likely continue to present challenges to boards, especially board diversity, workplace diversity, and climate-related issues. And these topics may move into the red zone if proponents become less willing to negotiate because of the high level of shareholder support these proposals receive.

- Upper left-hand quadrant: Shareholder Proposals in the Yellow Zone

- Proposals on topics that were difficult to negotiate away or omit from the proxy statement but that received—on average—not as much support as their counterparts in the red zone.

- Even though these proposals garner lower levels of average support, boards should be mindful that with a little boost from institutional investors, some of these proposals (e.g., on gender/racial pay gap, human rights, and dual class structure) could migrate into the red zone in the 2022 proxy season. Therefore, board attention for these topics is warranted.

- Lower left-hand quadrant: Shareholder Proposals in the Green Zone

- Proposals on topics that were rather easy to get withdrawn or omitted and received lower levels of shareholder support.

- Generally speaking, these proposals are least contentious and need less board attention. However, proposals on these topics still need to be monitored, as over time they can be modified to receive higher shareholder support and proponents can become less willing to negotiate a withdrawal.

The complete publication, including footnotes and appendix, is available here.

Endnotes

1The data and figures in this post and all six supplemental briefs represent shareholder proposals submitted at Russell 3000 companies in the first half of 2021, 2020, and 2018. About 90 percent of shareholder meetings at Russell 3000 companies take place in the first half of the year, and this cutoff point also allows easy comparisons with our prior-year shareholder voting benchmarking reports.(go back)

2Charles Mitchell et al., “Toward Stakeholder Capitalism: What the Shift Means for CEOs and the C-suite,” The Conference Board, December 2021.(go back)

3See, for example, BlackRock’s “Larry Fink’s 2022 Letter to CEOs,” State Street Global Advisors’ “CEO’s Letter on Our 2022 Proxy Voting Agenda,” and Vanguard’s “Proxy Voting Policy for U.S. Portfolio Companies.(go back)

4Noteworthy is BlackRock’s recent move, starting in 2022, to allow institutional investors in some of its index strategies in the US and UK to cast proxy votes in line with their own values and goals: “Working to Expand Proxy Voting Choice for Our Clients,” BlackRock, October 7, 2021.(go back)

5Matteo Tonello and Paul Hodgson, “Corporate Board Practices in the Russell 3000, S&P 500, and S&P MidCap 400: 2021 Edition,” The Conference Board, October 2021.(go back)

6“Board Practices: A Look Ahead,” The Conference Board ESG Watch webcast, July 13, 2020.(go back)

7Thomas Singer, “Sustainability Disclosure Practices: 2022 Edition,” The Conference Board, January 2022.(go back)

8The central goal of the COP21 Paris Agreement is to “strengthen the global response to the threat of climate change” by holding the increase in the global average temperature to well below 2°C above preindustrial levels and pursuing efforts to limit the temperature increase to 1.5°C. The COP26 Glasgow Climate Pact reaffirms this goal and its resolve to pursue efforts to limit the temperature increase to 1.5°C.(go back)

9Proponents may decide to withdraw the proposal they submitted before the proxy statement is officially filed; this usually only happens after a negotiation during which the company makes specific commitments to the proponent. Omission of a shareholder proposal, on the other hand, often happens against the proponent’s will. Rule 14a-8 of the Securities Exchange Act of 1934 permits a company to exclude a shareholder proposal from its proxy materials if the proposal fails to meet any of several specified requirements. If a company wants to omit a proposal, it submits a letter to the SEC asking for no-action relief from the staff.(go back)