Print

PrintFrederick Alexander is Founder of The Shareholder Commons; Holly Ensign-Barstow is Director of Stakeholder Governance & Policy at B Lab. This post is based on their recent paper. Related research from the Program on Corporate Governance includes Companies Should Maximize Shareholder Welfare Not Market Value by Oliver Hart and Luigi Zingales (discussed on the Forum here); Reconciling Fiduciary Duty and Social Conscience: The Law and Economics of ESG Investing by a Trustee by Max M. Schanzenbach and Robert H. Sitkoff (discussed on the Forum here); and Exit vs. Voice by Eleonora Broccardo, Oliver Hart and Luigi Zingales (discussed on the Forum here).

Corporate social responsibility. Socially responsible investing. Environmental, social and governance (ESG) integration. Sustainable investing. These phrases refer to the need for investors to pay more attention to the environmental and social (“E/S”) impacts of the businesses in which they invest.

The growing importance of this field is evident in the creation of the International Sustainability Standards Board (the “ISSB”) to establish uniform E/S disclosure standards that companies around the world will use to report to investors. The ISSB has the critical mass of support from established market participants necessary to bring the same uniformity (and thus utility) to sustainability reporting that now exists for standard financial reporting.

This article addresses a fundamental debate over the purpose of the uniform standard and reaches the following conclusions:

Four types of impact. E/S information can travel three pathways to affect investors and a fourth to affect other stakeholders:

- E/S Information that impacts future cash flows from the company to investors and thus the value of the enterprise (“ESG integration” or just “ESG”).

- E/S information that impacts the costs that companies externalize to the economy, which affect overall securities market returns (“beta”), and thus the returns of other companies in an investor’s portfolio.

- E/S information that involves the residue of E/S impacts that do not affect investment returns, but that impact on other matters that are important to individual investors (“non-financial investor impacts”).

- E/S information that does not affect investors, but is relevant to the impact companies have on civil society and stakeholders other than investors (“stakeholder data”).

ISSB embraces a single type of data. The current plan for the ISSB expressly encompasses only data that implicate enterprise value (often called “financial materiality”), although a close read of the documentation produced to date leaves the door open for an expansion to information pertinent to beta information as well. The ISSB documentation expressly rejects “double materiality,” the standard European regulators embrace, which couples financial materiality with information designed to inform other stakeholder data. The ISSB documentation does not address—or even acknowledge—the possibility of providing beta or non-financial investor information. The failure to even address beta-oriented disclosure is surprising because there is a growing emphasis on the need for diversified investors to monitor and steward the beta impact of portfolio company activity.

Expanding the ISSB definition of materiality to include beta information would not significantly expand the reporting burden. Adding beta information to the ISSB reporting standard would not significantly enlarge the reporting requirement because any company conduct that threatens or benefits beta is likely to create corresponding regulatory and reputational risks and benefits to enterprise value, so that most beta information should be deemed material even under a putative ESG standard. Such a standard, rising above a single focus on financial materiality but rooted in investor return, would not rise to the level of double materiality, and might best be described as “sesquimateriality.”

Excluding beta information from the reporting standard does not reflect evolving recognition of the importance of beta. The ISSB drafters should recognize the risk that excluding beta could, at the margins, lead to the omission of decision-critical information for investors concerned with company impact on social and environmental systems that support other portfolio companies. The increasing recognition of the importance of beta to investors could make a beta-free ISSB standard obsolete from the start. Steering clear of this risk is likely to require, at most, minor adjustments in methodology; moreover, the initial ISSB documentation, while ambiguous, does not preclude such considerations.

Finally, from a rhetorical perspective, it is important that the final documentation of the ISSB standards acknowledge that investors have significant interests in beta impacts. The law governing investment fiduciaries is evolving to make it clear that their fiduciary obligations permit—or even require—beta management. This is a critically important public policy development, not simply because it will improve investment returns, but because it will lead to better social and environmental outcomes on the ground, as many of the most serious threats to beta are also the most serious threats to people and the planet on which we live. At a time when regulation alone seems increasingly inadequate to the task of addressing threats to the environment and our social fabric, an apparent retreat from a constructive market reform in a document as influential as the ISSB standards would be a serious setback.

A. Untangling the Threads: A Very Brief Discussion of Social and Environmental Investing Concerns

Before discussing the ISSB and the desirability of a sesquimateriality standard, we review several elements of E/S investing.

1. Social Investing Matures and Confronts Fiduciary Duties

There have long been investors who shunned “sin” stocks—alcohol, tobacco, and gambling companies, for example. This reflected moral concern with profiting from suffering, rather than the use of investment to address a social issue. But as capital markets matured, investors began to contemplate a more active role, and after a divestment campaign helped end South African apartheid, the idea that investors could change bad corporate behavior, rather than simply avoiding it, developed a broader following. This idea extended beyond security selection and included influencing corporate behavior by voting shares and engaging with management.

But while an individual investor is free to satisfy ethical goals without regard to financial consequences, many investors, such as retirement and mutual funds, have fiduciary obligations to prioritize the interests of their beneficiaries. Their primary obligation is to protect the financial interests of their beneficiaries and clients by protecting and growing their investment portfolios. These institutions cannot simply subordinate financial returns to concern for workers’ lives or the environment. Ironically, as E/S investing became popular, more capital moved into these constrained fiduciary institutions.

2. ESG Aligns Social Concerns and Fiduciary Responsibility in Some, but not All, Circumstances

The gap between fiduciary and ethical obligations can be reduced in part if companies are able to implement responsible E/S practices that drive greater enterprise value. To the extent such overlap exists, an investor can harmonize the desire for positive social and environmental impact and the desire (or obligation) to optimize financial returns. For example, an investor might conclude that a company can avoid reputational, regulatory, and supply chain risks by adopting better labor and energy practices. In such cases, E/S impact and financial return are “integrated,” as are disclosures with respect to each.

Importantly, however, to the extent that E/S impact and enterprise value at a company are not correlated—i.e., to the extent that value and values do not align—investors and companies will have to choose between optimizing enterprise value and optimizing E/S impact, or make some compromise between the two.

3. Stakeholder Capitalism: The Unlikely Claim that E/S Impact and Financial Return Are Fully Aligned at All Companies at All Times

Of course, there would be no need to decide between prioritizing E/S impact or financial return if business decisions that optimize one always optimized the other. As unlikely as this proposition seems, the Business Roundtable, an organization composed of most major U.S. corporations’ CEOs, promotes this idea under the moniker “stakeholder capitalism,” and claims that if a company treats all its stakeholders well (which can be another way of saying it optimizes its E/S impact), it will also maximize its return to its shareholders over the long term: “While we acknowledge that different stakeholders may have competing interests in the short term, it is important to recognize that the interests of all stakeholders are inseparable in the long term.” Business Roundtable, Redefined Purpose of a Corporation: Welcoming the Debate (August 2019).

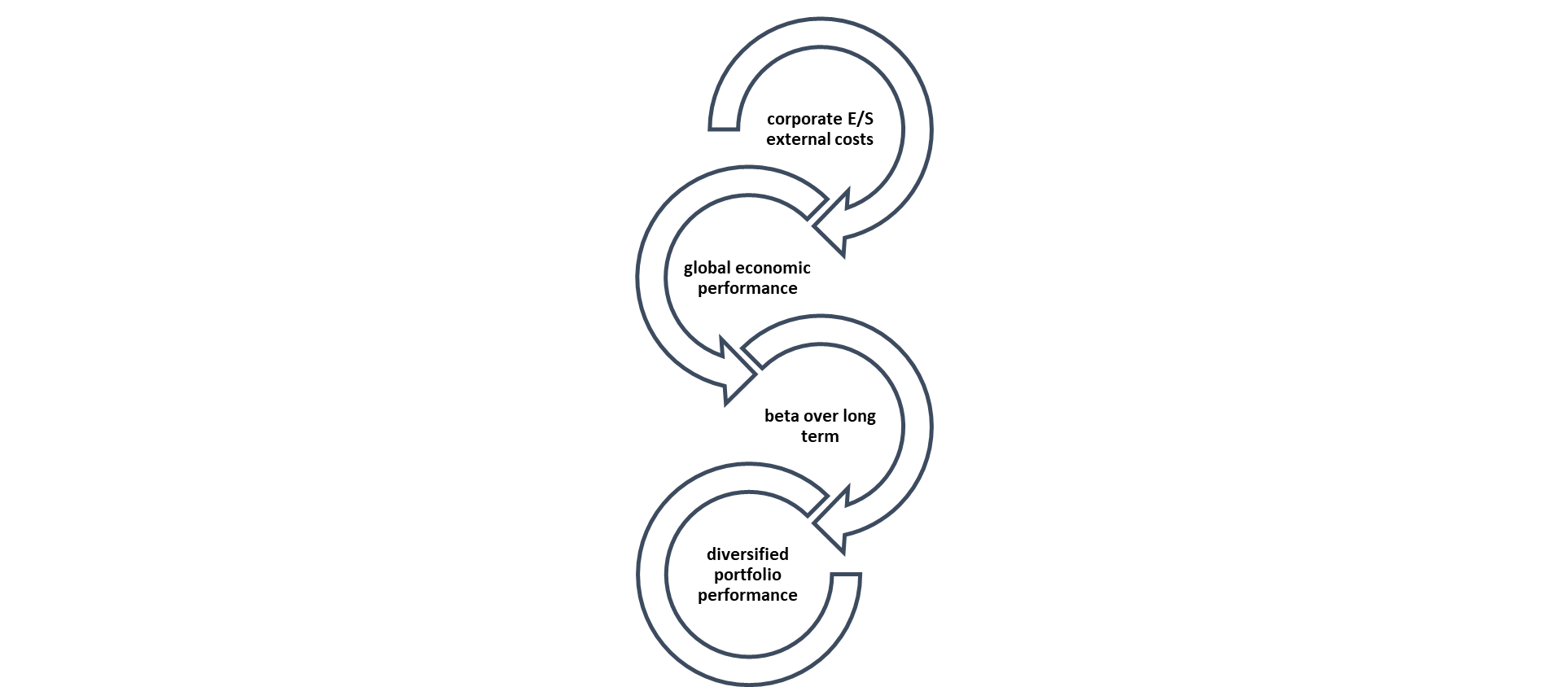

But interests do not magically align. Economists have long recognized that profit-seeking firms in free-market economies will not account for negative externalities, and there are many profitable strategies that harm stakeholders, society, and the environment. A recent study determined that in 2018, publicly listed companies around the world imposed net social and environmental costs on the economy with a value of $2.2 trillion annually—more than 2.5 percent of global GDP. See Andrew Howard, SustainEx: Examining the Social Value of Corporate Activities (Schroders 2019). This cost was more than 50 percent of the profits those companies reported.

This divergence of interests arises in many cases from the unpriced availability of finite common resources, such as the earth’s carbon sink or the capacity of society to absorb growing inequality. Companies that prioritize their financial return to shareholders face a prisoner’s dilemma with respect to such resources, and unchecked market competition will inevitably lead to their depletion. That is why we attempt to regulate companies: the choices that are best from an individual company financial perspective are not always best for society and the environment. See Thomas C. Schelling, On the Ecology of Micromotives, 25 Pub. Interest 61 (1971). The dream of stakeholder capitalism cannot align individual company financial interests with the interests of society. Hard choices must be made.

4. Beta Stewardship: Distinguishing the Financial Interests of Shareholders from Individual Company Enterprise Value

Up until this point, we have discussed financial success in terms of single companies, but the returns of the institutional investors mentioned above depend much more on beta than on alpha. Modern investing principles obligate those institutions to diversify their investments, because diversification allows them to earn the higher financial returns that come from bearing risk while diversifying some of that risk away. In many cases, the laws that govern fiduciaries, including ERISA and the Uniform Prudent Investor Act, are explicit that such diversification is required.

The return to such diversified investors chiefly depends upon beta, not the performance of individual companies. As one work describes this, “[a]ccording to widely accepted research, alpha [over- or under-performance of individual securities] is about one-tenth as important as beta [and] drives some 91 percent of the average portfolio’s return.” Stephen Davis, Jon Lukomnik, and David Pitt-Watson, What They Do with Your Money (2016). A large percentage of securities markets beneficiaries are diversified, and the relative importance of beta compared to alpha should affect these investors’ calculus when considering the impact of a portfolio company’s social and environmental externalities.

Why? Because negative externalities burden the economy and beta. For example, if climate change stays on the current trajectory, rather than aligning with the Paris Accords, GDP could be 10 percent less in 2050. Swiss Re Institute, The Economics of Climate Change: No Action Not an Option (April 2021). More immediately, the difference between an efficient response to COVID-19 and an inefficient one could create a $9 trillion swing in GDP. Ruchir Agarwal and Gita Gopinath, A Proposal to End the COVID-19 Pandemic, IMF Staff Discussion Note (May 2021). Contributions to inequality also reduce GDP over time. Dana Peterson and Catherine Mann, Closing the Racial Inequality Gaps: The Economic Cost of Black Inequality in the U.S. (2020). If companies increase their own bottom line by emitting extra carbon, by refusing to share technology that will slow the pandemic, or by contributing to inequality, the financial benefits earned for their individual companies may be dwarfed by comparison to the costs the economy bears.

When the economy suffers, so do diversified shareholders. Over long time periods, beta is influenced chiefly by the performance of the economy itself, because the value of the investable universe is equal to the percentage of the productive economy that the companies in the market represent. Principles for Responsible Investment & UNEP Finance Initiative, Universal Ownership: Why Environmental Externalities Matter to Institutional Investors, Appendix IV. Thus, diversified shareholders internalize E/S costs that individual companies can profitably externalize:

This is a trade. When a company saves costs with cheaper, carbon-intense energy, it trades away climate mitigation (which supports the intrinsic value of the economy) in exchange for more internal profit. While this trade might financially benefit a shareholder with shares only in that company, it harms a diversified shareholder by threatening beta.

Not all investors are diversified, so if a company protects beta by accepting reduced enterprise value, it may be favoring diversified investors at the expense of concentrated investors. But the trade is inevitable—the only question is which type of investor it will favor. Because the ISSB is a standard for disclosure, and not for action, it can be neutral on which side to take and simply provide beta-relevant information, in order to inform investors of the trades being made. Nevertheless, portfolio theory’s prescription of diversification certainly suggests that widely held entities should give strong consideration to diversified investors’ interests.

5. Beyond Beta Stewardship: Non-Financial Investor Information and Stakeholder Information

In addition to interests in alpha and beta, shareholders may be otherwise affected by the E/S impact of companies in which they invest. For workers who are beneficiaries of many retirement plans, employment may be the most important financial asset. Such investors might prefer that companies in their portfolios make less money, i.e., that beta be reduced, if it were to lead to better employment opportunities. Similarly, they might be willing to sacrifice portfolio return if it meant a healthier environment in which to enjoy their retirement, or if doing so would relieve others’ suffering.

The last category of information is that which is relevant to stakeholders other than shareholders. This would be information of interest to NGOs, governments, and citizens who wanted to understand companies’ impact on the world.

As important as these two categories of impact may be, they are likely to be more heterogeneous than shareholder interests in beta, making them less likely to be good candidates for standardized disclosure. (Of course, much data relevant to investors for beta purposes would overlap with these two categories, so that an expansion to beta-relevant information would add that value as well.)

B. E/S Disclosure for Diversified Shareholders: The Case for Sesquimateriality in the ISSB

For all the reasons discussed in Section A.4, diversified investors have a financial need to know whether portfolio companies are externalizing social and environmental costs. Diversified investors internalize the collective costs of such externalities (more than $2 trillion in 2018 according to the Schroders report cited above) because they degrade the systems upon which economic growth and corporate financial returns depend.

PRI, an investor initiative whose members have $121 trillion in assets under management, recognizes this need. It recently issued a report (the “PRI Report”) that described a variety of corporate practices that can boost individual company returns while threatening the economy and diversified investor returns:

A company strengthening its position by externalising costs onto others. The net result for the [diversified] investor can be negative when the costs across the rest of the portfolio (or market/economy) outweigh the gains to the company;

A company or sector securing regulation that favours its interests over others. This can impair broader economic returns when such regulation hinders the development of other, more economic companies or sectors…

Thus, while individual companies can profitably externalize costs, a diversified investor will pay these costs through lowered return on their diversified portfolios.

Because investors vote on directors and other matters, they have the power and responsibility to steward companies away from such practices. The PRI Report described the investor action necessary to manage social and environmental systems:

Systemic issues require a deliberate focus on and prioritisation of outcomes at the economy or society-wide scale. This means stewardship that is less focused on the risks and returns of individual holdings, and more on addressing systemic or ‘beta’ issues such as climate change and corruption. It means prioritising the long-term, absolute returns for universal owners, including real-term financial and welfare outcomes for beneficiaries more broadly.

A new report from the law firm Freshfields Bruckhaus Deringer (the “Freshfields Report”) explains how externalized costs affect investment trustees’ fiduciary duties:

System-wide risks are the sort of risks that cannot be mitigated simply by diversifying the investments in a portfolio. They threaten the functioning of the economic, financial and wider systems on which investment performance relies. If risks of this sort materialised, they would therefore damage the performance of a portfolio as a whole and all portfolios exposed to those systems.

The Freshfields Report goes on to suggest that alpha-oriented strategies (e.g., ESG integration) are of limited value to diversified shareholders, and that beta focus is the best way for investors to improve performance:

The more diversified a portfolio, the less logical it may be to engage in stewardship to secure enterprise specific value protection or enhancement. Diversification is specifically intended to minimise idiosyncratic impacts on portfolio performance…

Yet diversified portfolios remain exposed to nondiversifiable risks, for example where declining environmental or social sustainability undermines the performance of whole markets or sectors… Indeed, for investors who are likely to hold diversified portfolios in the long-term, the question is particularly pressing since these are likely to be the main ways in which they may be able to make a difference.

For similar reasons, Professor John Coffee predicted in a recent article that beta would surpass ESG integration as a motive for investor activism:

This latter form of activism [beta focused] is less interested in whether the target firm’s stock price rises (or falls) than in whether the activist investor’s engagement with the target causes the total value of this investor’s portfolio to rise (which means that the gains to the other stocks in the portfolio exceed any loss to the target stock). This recognition that change at one firm can affect the value of other firms in the portfolio implies a new goal for activism: namely, to engineer a net gain for the portfolio, possibly by reducing “negative externalities” that one firm is imposing on other firms in the investor’s portfolio.

The message is clear: to optimize returns, investors must exercise their governance rights and other prerogatives to protect themselves and their beneficiaries from individual companies that threaten beta. As we discuss in the next section, this will require beta-oriented disclosure.

C. Materiality under the ISSB Standards

The following chart sums up the four possible uses of data for which the ISSB might be optimized:

| Investor-Related Focus | Investor-Return Orientation | Do Data Address Financial Benefits to Investors? | Are Interests Appropriately Homogeneous for Standardized Disclosure? | Would Disclosure Map Onto Fiduciary Obligations? | |

|---|---|---|---|---|---|

| ESG Integration Data | Enterprise value of individual companies |

Alpha-oriented | Yes | Yes | Yes |

| Beta Data | Value of diversified portfolio |

Beta-oriented | Yes | Yes | Yes, as per Freshfields Report |

| Non-Financial Investor Data | Heterogeneous impacts such as employment prospects, quality of life, ethical concerns |

Not oriented to shareholder returns |

In some situations, but outside of portfolio effects |

No | Not under current law |

| Stakeholder-Based Data | None | Not oriented to shareholder returns |

Only indirectly | No | No |

1. The Artificial Choice between Financial Materiality and Double Materiality

As investors have become more cognizant of the importance of corporate impact on society and the environment, disclosure standards proliferated, making it difficult to compare the impact of companies that report on different standards. The ISSB is the product of agreement among a critical mass of relevant industry participants to develop a uniform standard for disclosure of social and environmental impact.

One of the first parameters to be established must be the purpose of disclosure. The Technical Readiness Working Group (the “TRWG”) recently released a set of recommendations for general requirements for the ISSB standards (the “General Requirements”) that addressed this question by defining what would be “material” for the standards overall.

The General Requirements propose two possibilities, which correspond to what disclosure specialists call “financial materiality” and “double materiality.” The first is disclosure designed for ESG integration. This means disclosing information related to a company’s social or environmental impact that is likely to affect its enterprise value. Financial materiality is in line with current U.S. disclosure rules.

In the alternative double-materiality rubric, financial materiality is referred to as “outside-in” information, because it addresses how social and environmental matters affect the company. But double materiality adds “inside-out” information, namely, information relevant to the company’s impacts on society and the environment. Importantly, the inside-out concept as discussed in the General Requirements is not designed to address beta; instead, it is focused on how the E/S performance of a company affects society overall. The Statement of Intent to Work Together Towards Comprehensive Corporate Reporting co-authored by five important standard setting organizations, was a 2020 document that was an important step towards the ISSB process; it describes inside-out information as being targeted at:

various users with various objectives who want to understand the enterprise’s positive and negative contributions to sustainable development [in contrast to enterprise value information targeted] [s]pecifically to the sub-set of those users whose primary objective is to improve economic decisions.

The General Requirements simply do not discuss or even acknowledge the existence of specifically beta-relevant information as pertinent to diversified investors’ economic decisions.

The General Requirements Background section described inside-out and financial materiality in the following paragraphs (a) and (b):

(a) disclosures to stakeholders about sustainability matters that have impacts on people, the environment and the economy—these disclosures normally provide the broadest range of information because they aim to meet the needs of multiple stakeholders…

(b) disclosures to investors, lenders and other creditors about sustainability matters that affect their assessment of enterprise value—these disclosures enable investors, lenders and other creditors to understand the impacts that sustainability-related risks and opportunities have on the value, timing and certainty of the entity’s future cash flows, over the short, medium and long term and therefore users’ assessment of enterprise value.

Having given itself these two choices, the TRWG chose financial materiality: “Sustainability matters that do not affect the reporting entity’s enterprise value are outside the scope of general purpose financial reporting.”

2. The Unexplained Nature of ISSB’s Failure to Consider Sesquimateriality

It is unclear why the General Requirements present double materiality and ESG as the only choices. As shown above, there is significant literature establishing that E/S disclosures that go beyond enterprise value may be of great importance to diversified investors’ economic decisions because of their financial interest in beta. The absence of any discussion of this interest seems to be an important and unexplained omission from the analysis.

Indeed, in another section of the General Requirements that discusses the materiality concept in more detail, the TRWG uses a definition that would certainly include beta information:

General purpose financial reporting includes financial statements of and sustainability-related financial information about a specific reporting entity. Sustainability-related financial information is material if omitting, misstating or obscuring that information could reasonably be expected to influence decisions that the primary users of general purpose financial reports make on the basis of those reports.

As discussed in the Freshfields Report and the PRI Report, decision-useful information extends beyond information that affects enterprise value; if a company’s E/S impact has the potential to affect beta, diversified shareholders may well act on that information by, for example, voting against directors who fail to act to mitigate negative externalities. Indeed, Institutional Shareholder Services, the world’s leading proxy adviser, recently announced it would do exactly that in its benchmark recommendation policy, treating a company’s climate damage to the economy in parallel with damage to the enterprise.

On its face, the exclusive choice of enterprise value as the measuring stick for materiality means the standards will only be useful for investors who want to use environmental and social data to determine how a particular company will perform financially, in order to decide whether to buy or sell it, or perhaps to use their shareholder rights to push the company to change its practices to improve future cash flows. In light of the diversification mandate of Modern Portfolio Theory, and the importance of beta to diversified investors, this anachronistic hyper-focus on enterprise value is troubling.

Diversified investors cannot avoid certain common risks almost all companies face. These are the risks to the social and environmental systems in which the economy is embedded. In their 2021 book, Moving beyond Modern Portfolio Theory: Investing that Matters, Jon Lukomnik and James Hawley explained that these systematic risks inevitably “swamp” any alpha strategy:

It is not that alpha does not matter to an investor (although investors only want positive alpha, which is impossible on a total market basis), but that the impact of the market return driven by systematic risk swamps virtually any possible scenario created by skillful analysis or trading or portfolio construction.

The focus of the General Requirements on ESG integration appears to reject the notion that information relevant to beta is important to shareholders. It suggests that corporate activity that threatens critical systems is not material if that activity does not threaten enterprise value at the company in question. Yet the scope of externalities is enormous. The Schroders Report calculated that one third of all listed companies around the world created net social costs that exceeded their profits. Pause on that figure: prioritization of individual company financial return leads to one third of all listed companies around the globe destroying more value for society than they create for their own shareholders. Diversified shareholders will internalize the costs of this negative-sum behavior through the economic harm the rest of their portfolios absorb.

Investors need a reporting standard that accounts for all the costs a portfolio company imposes on them, even if the company itself avoids those costs. The materiality principle chosen in the General Requirements seems to ignore the most important issue on the table without explanation.

3. Why ISSB’s Financial Materiality Is Still Close to the Mark: The Limited Distance between Financial Materiality and Sesquimateriality

Although the financial-materiality test articulated in the General Requirements seems inadequate to address the system level issues, the drafting implications may be more theoretical than practical, especially if the drafters understand the concern.

a. No Context for ESG Data

It is important to understand that ESG data are often provided without much context. See Bill Baue, Compared to What? A Three-Tiered Typology of Sustainable Development Performance Indicators (UNRISD 2019). ESG metrics will typically say something like, “companies in X industry often hire low-wage workers in countries with poor regulatory schemes; this can expose them to reputational risk and cost increases over the long term and perhaps increased regulation and enforcement” or “fuel prices are subject to rapid change and efficiency measures can limit future costs.” Accordingly, the disclosure line items will require the company to describe the programs and standards in place to assure workers are not being abused, its record in meeting such standards and relevant legal requirements, its plans to reduce fuel use, etc.

But these standards do not provide for a grade or make a judgment as to whether the company’s treatment of workers or fuel efficiency will in fact threaten its cash flows and enterprise value: that is generally left for investors to decide. This is the same way that traditional financial disclosures work: the purely financial data securities regulators require informs investors about items such as historical earnings data, sources of liquidity, and risk factors. But it does not tell shareholders how to use this data to value securities: the user provides that context.

This does not mean that disclosure standards drafters do not themselves need to understand the context—that understanding is critical to eliciting the correct information for investors to use. For purely financial information, the standard must elicit the financial metrics and qualitative descriptions that investors use to model value. For ESG integration, the standard must call for disclosures of E/S matters that investors can use to model an enterprise’s value and future cash flows. These will include information that allows investors to draw conclusions as to whether the company’s reputation is at risk, or whether it may be subject to regulation or increased costs when regulation is adopted to address currently unmitigated social or environmental costs.

b. The overlap of decontextualized data regarding financial materiality and beta impact

By the same token, a proper sesquimateriality standard would elicit the inside-out E/S data that was likely to impact the social and environmental systems that support beta. But the context for beta-relevant data is such that an enterprise value-based E/S disclosure regime may in many cases be very close to “good enough” for beta as well. The reason is that if a company’s activities create the type of economic risk that threatens beta, it will almost surely be at risk for damaged reputation, increased regulation, and the increased costs that follow regulation. In other words, an enterprise cannot be accurately valued without information concerning the threats it poses or benefits it promises to beta.

Thus, to gather the E/S data that are material for company valuation purposes, the ISSB standard will have to include the same data that will be used to determine whether a company is externalizing costs to the detriment of people, planet, and other companies.

Of course, a company may make the judgment that it can “get away” with a certain amount of cost externalization, so that corporate managers may make business judgments that financial return can be maximized without optimizing social value. But from a disclosure perspective, investors should have the data that would allow them to understand the risk the company is taking by continuing to externalize costs.

4. Where to go from here

Given the real reputational and regulatory risk for companies that rely on externalized costs, those of us focused on beta impacts can do several things with the ISSB process.

- Encourage the ISSB drafters to move to an express sesquimateriality standard. Ensure that the drafters of the ISSB keep front of mind the fact that most of the investors for whom ISSB is being created are diversified. This means that beta information is decision-useful, and thus comes within the broad parameters established in the General Requirements. This change will not create a significant additional burden but will make the project more coherent and consistent with evolving fiduciary standards.

- Make the case, early and often, that cost externalization always creates material business risks due to concerns with future regulations, costs, reputation, and license to operate. This will narrow any gap between the raw data supplied by the ISSB standards and what a sesquimateriality standard would include (assuming the ISSB does not move off its current position).

- Continue the context-setting projects for beta-level impacts of E/S issues outside the ISSB process. These projects help investors determine a company’s “fair share” of a limited common resource or the proper social and environmental boundaries for individual companies that are necessary to preserve the systems upon which all companies rely. Once such a standard is established, failure to adhere will become a reputational and regulatory risk, so that the question of meeting that standard becomes financially material.

- Keep the distinction between ESG integration, beta management, and other sustainability purposes at the top of the discussion. Crisp thinking about the purpose of the disclosure leads to clearer understanding of the decision-critical nature of beta-relevant information.

* * * * *

The final documentation of the ISSB standards should acknowledge that most investors have significant, largely uniform interests in beta impacts. The law governing investment fiduciaries is evolving to make it clear that fiduciary obligations permit—or even require—beta management. This is a critically important public policy development, not simply because it will improve investment returns, but because it will lead to better social and environmental outcomes on the ground, as many of the most serious threats to beta are also the most serious threats to people and the planet on which we live. At a time when regulation alone seems increasingly inadequate to the task of addressing threats to the environment and our social fabric, an apparent retreat from a market-based solution in a document as influential as the ISSB standards would be a serious setback.