Print

PrintRobert J. Jackson, Jr. is the Pierrepont Family Professor of Law, Co-Director of the Institute for Corporate Governance and Finance at NYU School of Law, and a former Commissioner at the U.S. Securities and Exchange Commission; Daniel Taylor is Associate Professor of Accounting at the Wharton School of the University of Pennsylvania; and Bradford Lynch is a PhD student at The Wharton School of the University of Pennsylvania. This post is based on their recent paper.

Related research from the Program on Corporate Governance includes Insider Trading Via the Corporation by Jesse Fried (discussed on the Forum here); and China and the Rise of Law-Proof Insiders by Jesse M. Fried and Ehud Kamar (discussed on the Forum here).

1. Introduction

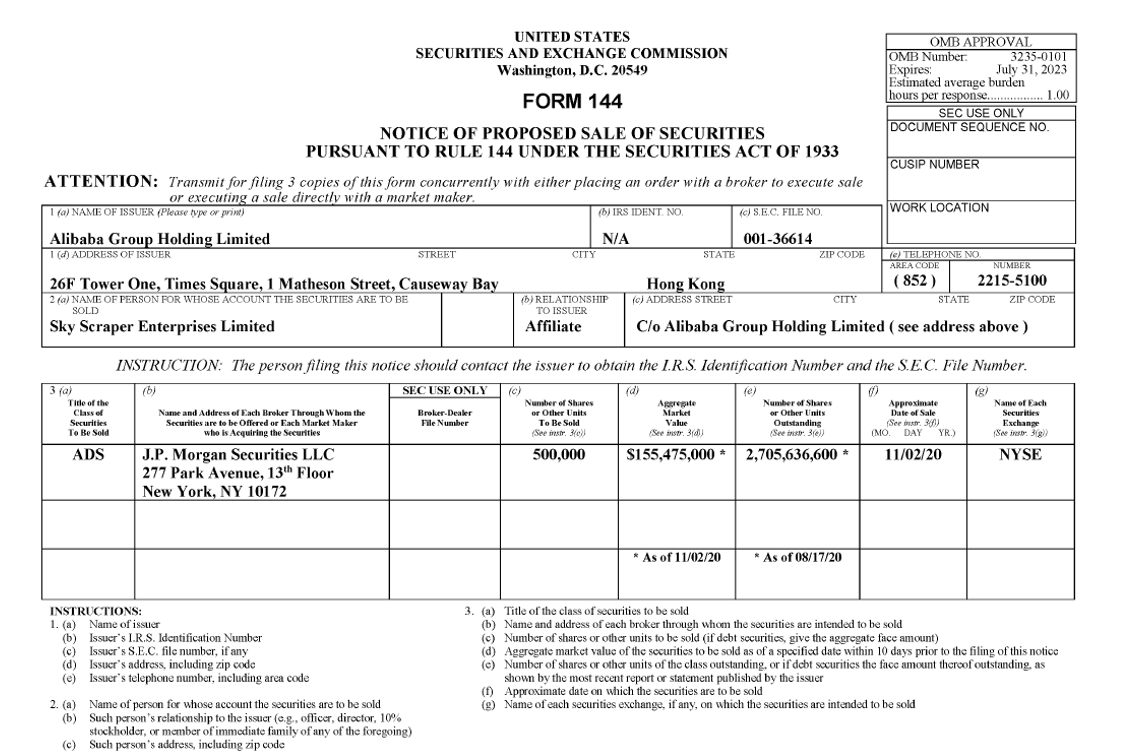

In October 2020, Ant Group, an affiliate of the Nasdaq-listed Chinese firm Alibaba, was preparing for its initial public offering (IPO). But on October 24, Alibaba CEO Jack Ma publicly criticized Chinese regulators and Communist Party officials (Zhai et al., 2020). Chinese leaders responded forcefully, and on November 3 the Ant IPO was suddenly suspended, leading Alibaba shares to fall more than 8% (Yang & Ng, 2020). Unbeknownst to most investors, however, the day before that announcement Skyscraper Limited, an entity controlled by Alibaba insiders, sold more than $150 million in Alibaba shares, avoiding millions in losses (McMorrow et al., 2021). Disclosure of that transaction was provided not in the widely-watched form that U.S. insiders must provide (Jackson, 2012) but rather on a little-known paper filing stored in file cabinets in the SEC’s reference room known as Form 144 (see e.g., Figure 1).

Figure 1. Form 144 Paper Filing by Foreign Insiders.

Below is an image of a paper filing on Form 144 associated with the sale by Sky Scraper Enterprises of over $155 million worth of shares in Alibaba, a foreign firm with American Depository Shares traded on Nasdaq. There is no corresponding Form 4. The day after this filing, shares of Alibaba fell more than 8%.

Insider trading has long been a focus of lawmakers and researchers alike. More recently, foreign firms listed on U.S. exchanges have become the subject of academic scrutiny (Fried & Kamar, 2022) and regulatory attention. But unlike their American counterparts, insiders at foreign-domiciled but U.S.-listed firms are free to trade in their firm’s stock without publicly disclosing their trades on easily-accessible electronic forms. Instead, foreign insiders’ transactions are disclosed on paper filings with the SEC, often long after the trades occur. Thus, their trading has largely eluded academic, public, and regulatory scrutiny.

In this paper, we provide the first systematic study of foreign insiders’ trading activity. We document opportunistic stock sales by foreign-firm insiders and show that these sales allow these insiders to avoid losses to a far greater degree than American insiders. Using a digitized dataset of more than 147,000 paper filings over five years, we document foreign-firm insider sales of over $77 billion per year.

We show that foreign-firm insiders’ sales are highly opportunistic when compared to their counterparts at U.S. companies. In fact, consistent with prior literature (e.g., Jagolinzer, Larcker & Taylor, 2011), we show that officers and directors at U.S. companies generally do not precede stock-price declines. In contrast, foreign-firm insiders often sell prior to significant declines in stock prices, whether measured over the subsequent three, six, or twelve months. On average, foreign-firm insiders sell prior to a 5% stock-price decline in the twelve months following their sales.

We also document significant heterogeneity in foreign-firm insider selling depending on the firm’s country of domicile. Specifically, we find that opportunistic trading and loss avoidance is concentrated in firms based in China, Russia, the Cayman Islands, India, and the Netherlands. In particular, median twelve-month returns following insider sales at U.S.-listed firms based in China are -23% and in Russia are -21%. In total, insiders at U.S.-listed Chinese companies avoided more than $10 billion in losses over the five-year period we examine.

In light of recent work showing that foreign firms and their senior executives are domiciled in non-extradition countries and thus likely beyond the reach of American corporate and securities law (Fried & Kamar, 2022), we argue that excluding foreign-firm insiders’ trading from the Form 4 disclosure requirements applied to American insiders is unwarranted. There is extensive evidence that investors incorporate important information from Form 4 disclosures (Veenman, 2012). We argue that all companies listed on U.S. exchanges should be subject to the same disclosure rules concerning the trading of corporate insiders. In addition, our findings provide support for the SEC’s proposal to mandate that Form 144 be filed electronically to give investors and researchers alike easier access to information about insiders’ trades (SEC, 2020).

2. Background

Under Section 16(a) of the Securities Exchange Act of 1934, officers and directors of U.S. public companies are required to publicly disclose certain transactions in their company’s stock. Specifically, upon becoming a “reporting person,” American insiders are required to file an initial report with the SEC detailing their ownership of the company’s stock. Thereafter, insiders are required to report changes in their ownership—for example, through open-market purchases or sales of the company’s stock—to the SEC and the public on what is known as Form 4. When it was first adopted, Section 16 required monthly reporting within 10 days of the close of each calendar month, and Form 4 was principally filed on paper with the SEC (SEC, 2002).

But in 2002 Congress passed the Sarbanes-Oxley Act, significantly tightening Section 16’s disclosure requirements. After the Act’s passage, the SEC implemented new rules requiring insiders at U.S. companies to report trades within two business days (SEC, 2002). SEC rules also required that Form 4, which provides extensive information on each insider transaction, be filed electronically (SEC, 2002). Empirical evidence suggests that these disclosures help investors incorporate information about the value implications of insider transactions (Veenman, 2012).

Neither Congress nor the SEC, however, addressed the fact that the SEC has exempted foreign private issuers with securities traded on U.S. exchanges from Section 16 (SEC, 2002). Thus, insider transactions in foreign firms with securities traded on American exchanges are not reportable under Section 16 (SEC, 2013). Recent research has noted that foreign insiders in some countries, particularly China, are “law-proof”: “the law cannot prevent or deter them from expropriating substantial value from U.S. investors.” (Fried & Kamar, 2022). Like ours, that research notes that insiders at foreign firms are “exempt from the requirement to disclose their securities trades” under Section 16 (Fried & Kamar, 2022).

But some insider sales are subject to disclosure under other securities-law requirements. For example, when an affiliate of an issuer seeks to resell restricted securities during any three-month period in a transaction that exceeds 5,000 shares or has an aggregate sales price of more than $50,000, notice of that resale must be provided to the SEC on Form 144 (SEC, 2020). While foreign-firm insiders are not required to file Form 4, they are still required to file Form 144 for certain sales of their company’s stock. Thus, Form 144 provides a rare window into foreign insiders’ trading activity. Unlike Form 4, however, Form 144 is not required to be filed either speedily or electronically. In total, the SEC received more than 700,000 Form 144s on paper from 2002 to 2020 (Larcker, Lynch & Taylor, 2021). During the 2019 calendar year alone, the SEC received over 31,000 Form 144 filings, and over 99% of these were filed on paper and mailed to the SEC (SEC, 2020).

Paper filings of Form 144 are retained in the SEC’s public Reference Room for 90 days (SEC, 2020). Figure 2 provides a photograph of researchers in the SEC’s Reference Room going through Form 144s filed on paper. These paper filings have sufficiently valuable information that, prior to the COVID-19 pandemic, a commercial vendor called The Washington Service would send a daily courier to the Reference Room to scan and digitize paper Form 144s filed each day (Larcker, Lynch & Taylor, 2021). We use this database in our analysis below.

Figure 2. Accessing Form 144.

The photograph below shows researchers in the SEC Reference Room copying and digitizing paper-filed Form 144s evidencing insider transactions in U.S.-listed firms.

3. Data

Our sample includes data on all sales of restricted securities between January 2016 and July 2021 disclosed on Form 144. For each Form 144, we match the security being traded to price data from the Center for Research on Stock Prices (CRSP), focusing only on securities that trade on the principal U.S. exchanges, and use Capital IQ to identify the country in which the issuer company is domiciled.

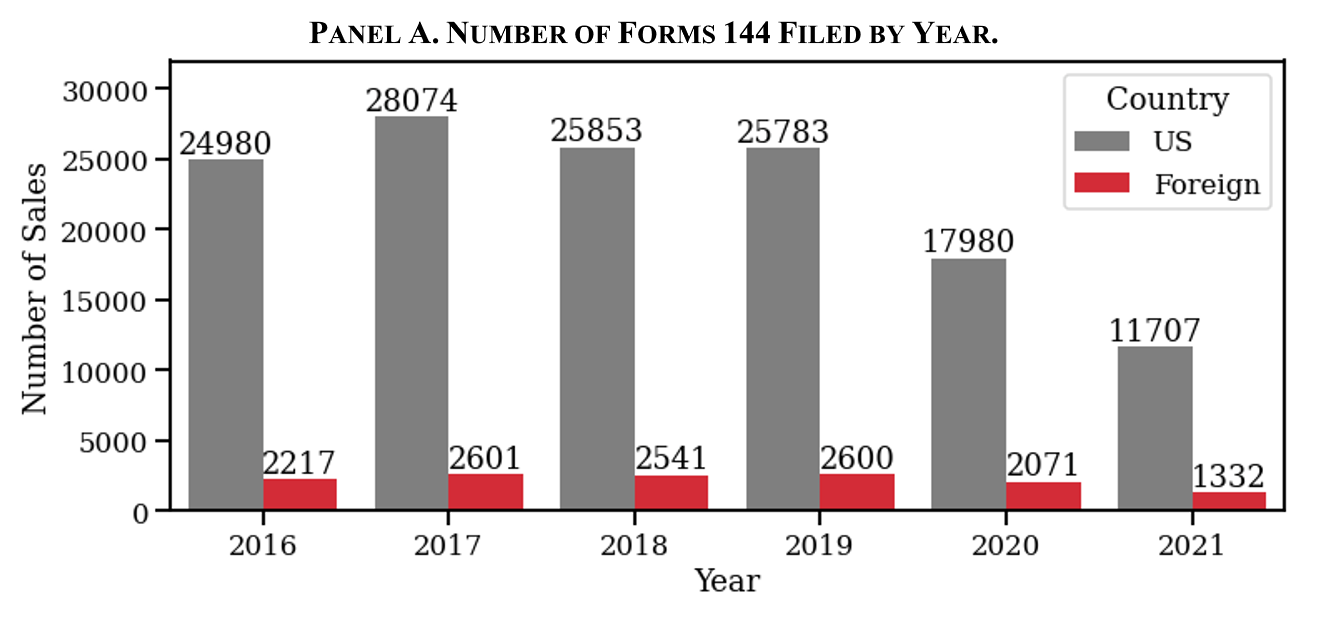

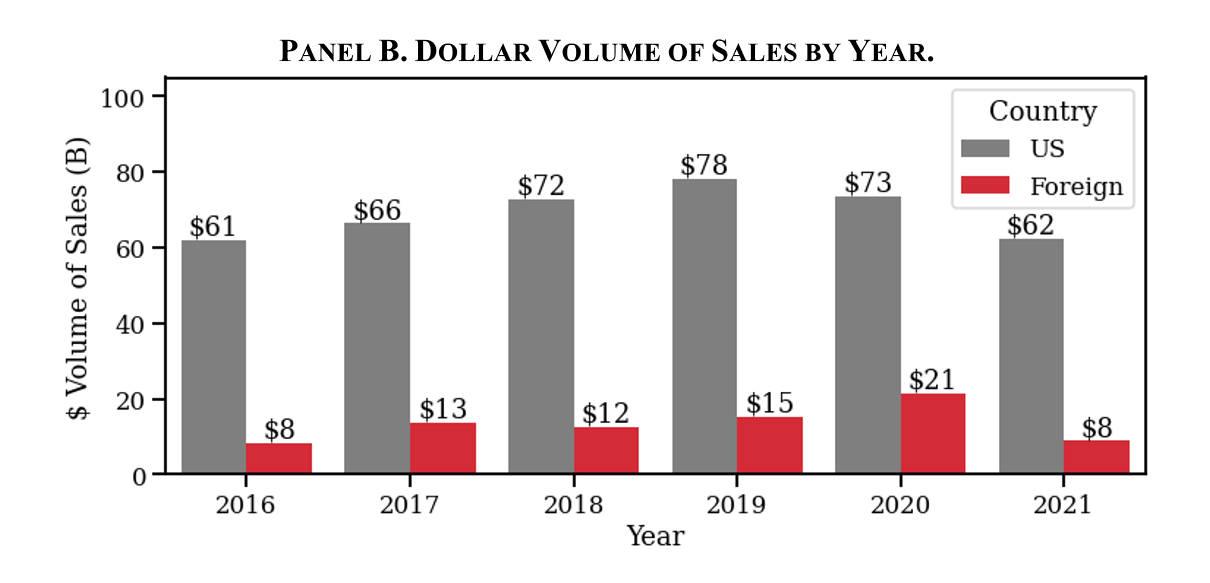

In total, we have data on 147,739 Forms 144 covering trading activity by 37,514 insiders at 4,193 unique U.S.-listed companies. Our data cover stock sales of more than $495 billion during our five-year sample period. Panel A of Figure 3 shows that, each year, over 20,000 sales are reported on Form 144. The number of documented sales declines in 2020 and 2021 due to researchers’ limited access to the SEC’s Reference Room during the COVID-19 pandemic. Nevertheless, Panel B of Figure 3 shows that Form 144s cover substantial amounts of stock sales. In total, U.S. (foreign-firm) insiders report sales of $415 ($80) billion during our sample period.

Figure 3. Form 144 Filings Over Time.

Panel A shows the number of unique Form 144s in our five-year sample period, categorized by whether the U.S.-listed company is domiciled in the United States or overseas. Approximately 83% of the sample documented below was filed on paper, by mail, with the SEC. Panel B documents the dollar volume of sales by insiders reported on Form 144. The Washington Service provided all data described below from a digitized database on information from filed Forms 144.

Panel A. Number of Forms 144 Filed by Year.

Panel B. Dollar Volume of Sales by Year.

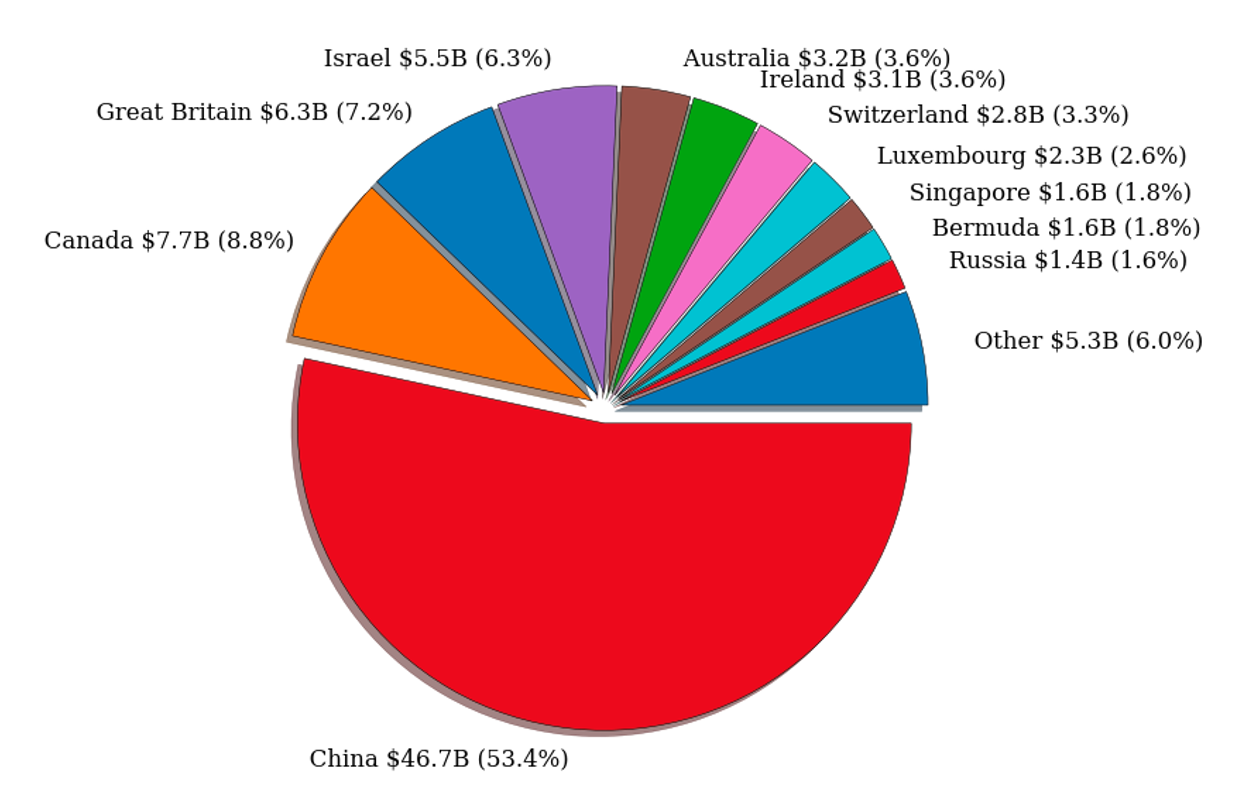

Figure 4 shows that the majority of sales by insiders at foreign companies listed in the U.S. originate in China. Specifically, sales by insiders at Chinese firms listed in the U.S. account for 53% of all foreign insider sales by volume. There are two reasons for this. First, China has more U.S.-listed companies than any other non-U.S. jurisdiction.

Figure 4. Total Dollar Volume Sold by Country.

This figure documents the distribution of sales by insiders reported on Form 144 based on the country where the U.S.-listed firm is domiciled; for example, Alibaba is listed on the New York Stock Exchange but is domiciled in China. The Washington Service provided all data described below from a digitized database on information from filed Forms 144.

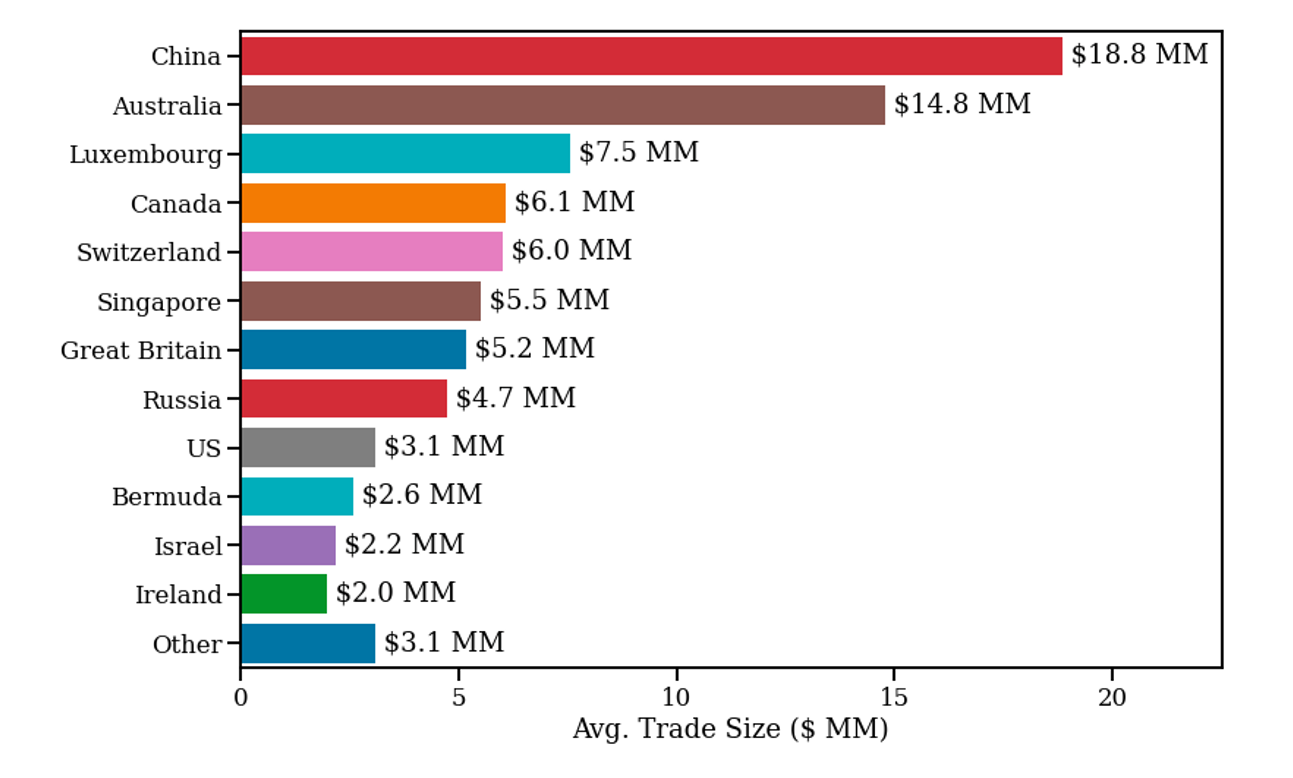

Second, Chinese insiders trade much more aggressively than their American counterparts. Figure 5 shows the average trade size for all corporate insiders in our sample. While the average sale by insiders at American companies is just over $3 million, the average sale by insiders at U.S.-listed, Chinese-domiciled firms is six times larger, at over $18 million.

Figure 5. Size of Average Stock Sale.

This figure documents the size of the average sale by insiders reported on Form 144 based on the country where the U.S.-listed firm is domiciled. The Washington Service provided all data described below from a digitized database on information from filed Forms 144.

4. Results

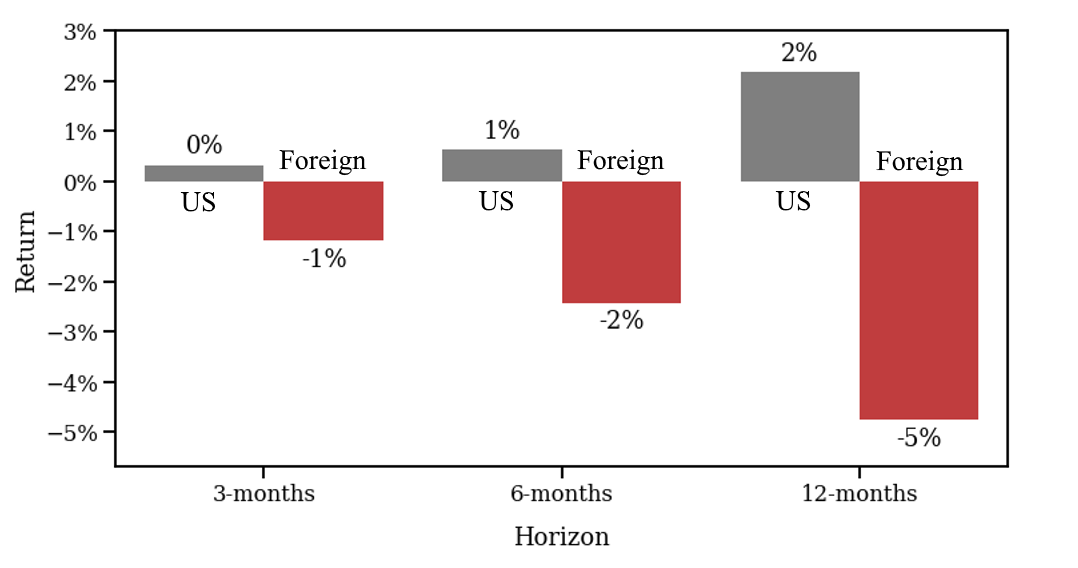

We document significant loss avoidance by corporate insiders at foreign firms listed in the United States. Figure 6 shows average market-adjusted stock returns over the three-month, six-month, and 12-month period after the stock sale separately for both American and foreign-firm insiders. Negative returns after a sale imply that the insider avoided losses. For example, a -5% market-adjusted return after an insider sale indicates the insider avoided a 5% loss on her company’s shares by selling when she did.

Figure 6. Market-Adjusted Returns After Form 144 Sales.

This figure shows the average stock return over the indicated horizon after stock sales reported on Form 144. Negative values indicate insider loss avoidance. For example, when the average U.S. insider in our sample sells, her firm’s stock price increases by 2%, over the next 12 months so we conclude that she did not avoid losses. By contrast, when the average foreign-firm insider sells, her firm’s stock price falls by 5%, so we conclude that she avoided losses. The Washington Service provided all data described below from a digitized database on information from filed Forms 144.

First, consistent with the existing literature, Figure 6 shows that insiders at American companies do not systematically sell shares prior to stock price declines—that is, they do not generally avoid losses (Jagolinzer, Larcker & Taylor 2011; Jagolinzer, Larcker, Ormazabal & Taylor, 2021). Indeed, on average stock prices increased by 2% during the 12 months following their sales. By contrast, Figure 6 shows that foreign-firm insiders systematically sell shares prior to stock price declines: on average, stock prices decreased by more than 5% over the twelve-month period following their sales.

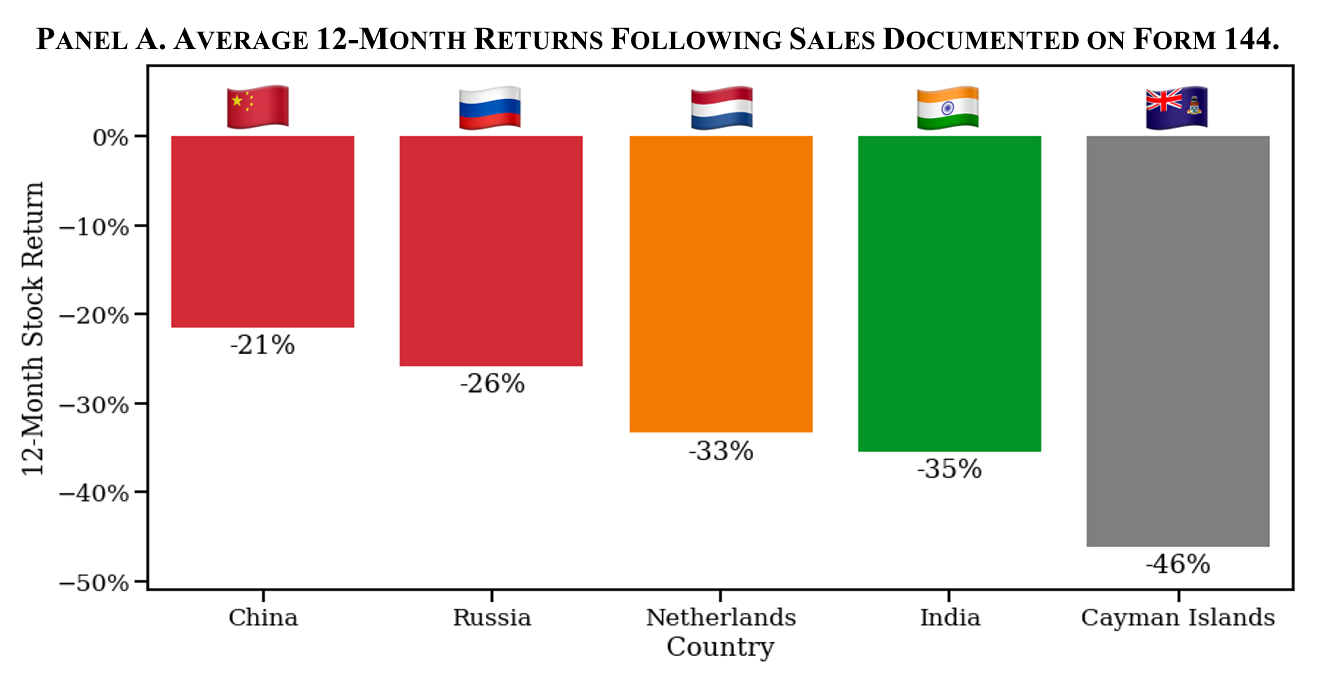

Panel A of Figure 7 presents stock returns after sales by the firm’s country of domicile. For parsimony, we present results for the five countries with firms featuring the largest negative average returns following the sale. The results in Panel A are striking. When insiders of U.S.-listed Chinese companies sell shares, stock prices of these firms on average decline by 21%; when insiders at U.S.-listed Russian firms sell, stock prices of their firms fall by 26%. Foreign-firm insiders’ ability to anticipate significant stock-price declines is unrivaled at American firms; recall by comparison that on average share prices of American firms rise after Form 144 sales.

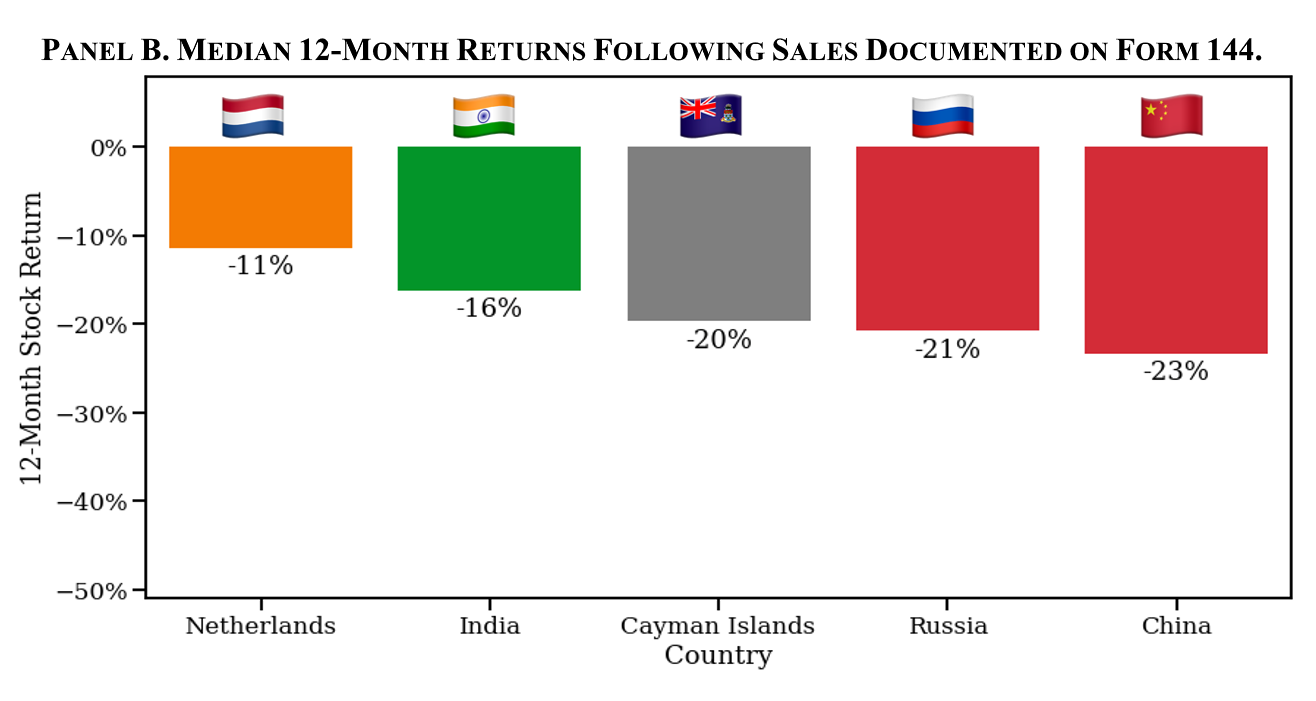

Figure 7. Market-Adjusted Stock Returns After Form 144 Sales, by Country.

Panel A shows the average 12-month return after insider sales for the five countries with the largest negative returns (i.e., loss avoidance); Panel B provides median values. For each foreign country with firms featuring U.S.-listed securities, we identify sales by insiders reported on Form 144 and calculate the market-adjusted stock return over the 12 months after the sale. Negative returns after the sale indicate that the insider avoided a loss. For example, Panel A indicates that, when an insider at a U.S.-listed Cayman company sells the U.S.-listed securities, prices decline by 46% over the next 12 months. The Washington Service provided all data described below from a digitized database on information from filed Forms 144; stock-price returns were provided by the Center for Research on Security Prices.

Panel A. Average 12-Month Returns Following Sales Documented on Form 144.

Panel B. Median 12-Month Returns Following Sales Documented on Form 144.

Given the significant negative returns after the average foreign-firm insider sale, a natural concern is whether these returns are representative or skewed by large outliers. To address this concern, Panel B shows the median 12-month return following stock sales for firms domiciled in each country. The median represents the midpoint of the distribution: 50% of the distribution is above (below) the reported return. We present the five countries with the largest negative median returns following the sale. The results are striking: half of trades by insiders at Chinese firms listed in the U.S. avoid stock-price declines of more than 23%, while half of trades by insiders at Russian firms listed in the U.S. avoid stock-price declines of 21%.

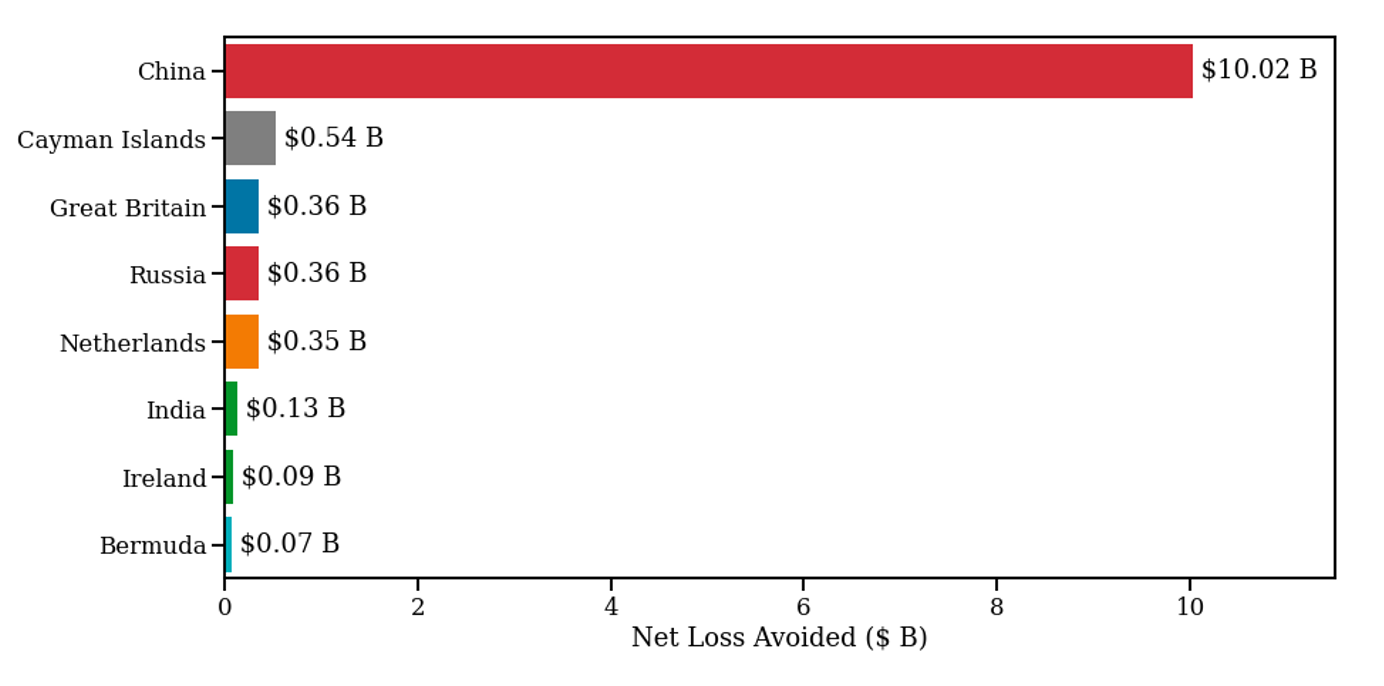

Thus far, our evidence indicates that insiders at foreign-domiciled firms listed in the U.S. sell shares prior to significant declines in the value of the company’s stock, avoiding significant losses. To get a sense of how large this loss avoidance is, we next estimate total dollar losses avoided by the firm’s country of domicile. To do so, we identify share sales by foreign-firm insiders reported on Form 144, calculate the stock’s market-adjusted return over the 12-month period following the sale, multiply by the dollar value of the sale, and sum at the country-of-domicile level. Figure 8 presents results.

Figure 8. Net Loss Avoided, by Country.

This figure presents an estimate of net loss avoidance by domicile country of the U.S.-listed firm. For each foreign country with U.S.-listed securities, we identify sale shares by foreign-firm insiders reported on Form 144, calculate the stock’s return over the 12 months following the sale, multiply by the dollar value of the sale, and sum at the firm-country-of-domicile level. This yields an estimate of the net dollar loss avoided by insider sales documented on Form 144. The Washington Service provided all data described below from a digitized database on information from filed Forms 144; stock-price returns are drawn from the Center on Research on Security Prices.

Among all of the countries in our sample, only eight featured net loss avoidance—that is, U.S.-listed firms domiciled in only eight countries have insiders who, on average, avoid losses. Yet we estimate conservatively that loss avoidance by insiders at firms domiciled in those countries exceeds $11.9 billion. Of that amount, insiders at U.S.-listed, Chinese-domiciled firms account for $10 billion in aggregate losses avoided. China represents such a large portion of avoided losses because both (1) the average insider trade at U.S.-listed Chinese-domiciled firms avoid larger losses in percentage terms, and (2) the average trade of insiders at these companies is significantly larger in size.

5. Conclusion

Important recent work suggests that insiders at foreign firms listed in the U.S. are “law-proof,” shielded from the deterrent effects ordinarily provided by American corporate and securities law. We show that they are also sunlight-proof: foreign-firm insiders are exempt from prompt disclosure of their trading, shielding them from the market scrutiny that insiders at American public companies face when trading. For example, while executives at Pfizer and Moderna faced considerable scrutiny over their stock sales at the height of the COVID-19 pandemic, their counterparts at AstraZeneca largely avoided such scrutiny. Of course, AstraZeneca, while listed in the United States, is based in the United Kingdom. Consequently, AstraZeneca’s insiders are not subject to Form 4 reporting requirements, and thus their trades largely eluded public scrutiny.

Drawing on data from the SEC’s Form 144, we show that foreign-firm insiders engage extensively in opportunistic selling. On average, insiders at Russian-domiciled firms avoid market-adjusted losses of 26% by selling; the average insider at Chinese-domiciled firms avoids losses of 21%. These well-timed trades enable foreign-firm insiders to avoid significant losses. Insiders at U.S.-listed, Chinese-domiciled firms have avoided more than $10 billion in losses.

Our evidence suggests that policymakers should revisit the SEC’s decades-old decision to exempt U.S.-listed, foreign-domiciled firms from insider-trading disclosure. When the SEC adopted that position, American insiders were not yet subject to the more strict disclosure requirements imposed by the Sarbanes-Oxley Act, so the comparative advantage given to foreign insiders was not as large as documented here. Moreover, far fewer foreign firms were then listed on U.S. exchanges—particularly firms domiciled in non-extradition countries. In light of more recent conditions, the SEC’s decision to exempt foreign firms from insider-trading disclosure is less tenable. Indeed, in September 2021, the SEC’s Investor Advisory Committee recommended that the SEC require foreign-firm insiders to disclose their trades on Form 4 (SEC, 2021).

We do not contend that transparency of this kind would address all of the concerns raised by exposing American investors to law-proof insiders at foreign-domiciled firms. We do think, however, that allowing market forces to meaningfully discipline insider-trading activity at foreign firms—just as they do for insiders at American public companies—would be beneficial. For markets to play that role, however, regulators must provide meaningful transparency into the insider trading activity of insiders at foreign firms that list in the United States. Accordingly, we urge lawmakers to promptly revisit foreign firms’ exemption from American law requiring prompt disclosure of insider trading.

The complete paper is available for download here.