Print

PrintJune Hu is an associate, and Melissa Sawyer and Marc Treviño are partners at Sullivan & Cromwell LLP. This post is based on a Sullivan & Cromwell memorandum by Ms. Hu, Ms. Sawyer, Mr. Treviño, H. Rodgin Cohen, and Elizabeth Lombard.

Introduction

In the tenth edition of our annual proxy season review memo, we summarize significant developments relating to the 2022 U.S. annual meeting proxy season. This year, our review comprises two parts: Rule 14a-8 shareholder proposals and compensation-related matters. This is Part 1, and we expect to issue Part 2 over the next weeks. We will also host our annual webinar in September to discuss 2022 proxy season developments.

The Rule 14a-8 shareholder proposals we discuss are those submitted to and/or voted on at annual meetings of the U.S. members of the S&P Composite 1500, which covers approximately 90% of U.S. market capitalization, at meetings held on or before June 30, 2022. We estimate that around 90% of U.S. public companies held their 2022 annual meetings by that date.

The data on submitted, withdrawn and voted-on shareholder proposals derives, in part, from ISS’s voting analytics with respect to 797 known shareholder proposals submitted this year to U.S. members of the S&P Composite 1500. We have supplemented the ISS data with information published by proponents on their websites and other independent research. The number of proposals submitted includes proposals that were not included in a company’s proxy statement as a result of the SEC no-action process or withdrawn after being included in a company’s proxy statement (usually following engagement with the company). The data on submitted proposals understates the number of proposals actually submitted, as it generally does not include proposals that were submitted and then withdrawn unless either the proponent or the company voluntarily reported the proposal to ISS or on its website.

For a discussion of U.S. proxy contests and other shareholder activist campaigns, see our publication, dated December 20, 2021, entitled “Review and Analysis of 2021 U.S. Shareholder Activism and Activist Settlement Agreements.”

Part 1. Rule 14a-8 Shareholder Proposals

A. Overview of Shareholder Proposals

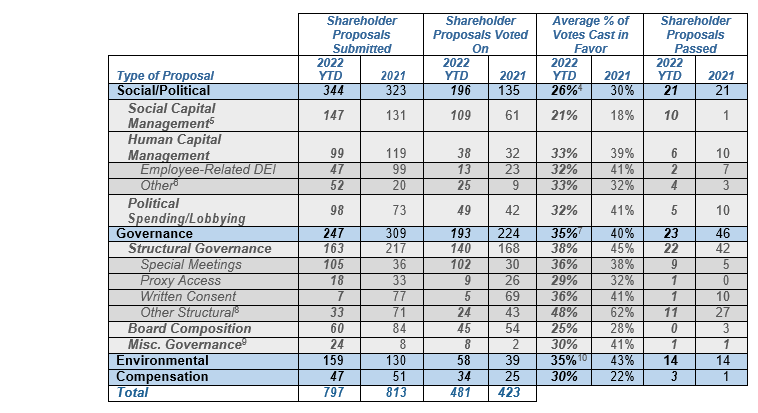

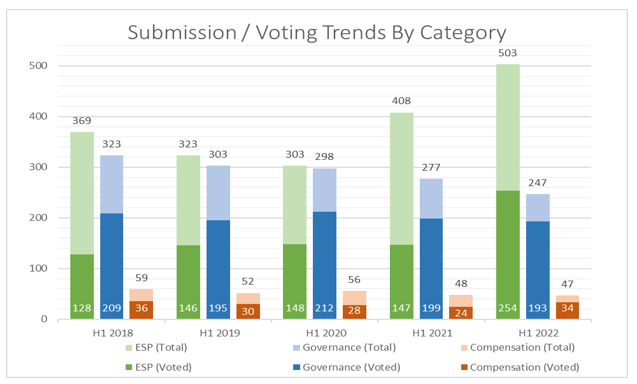

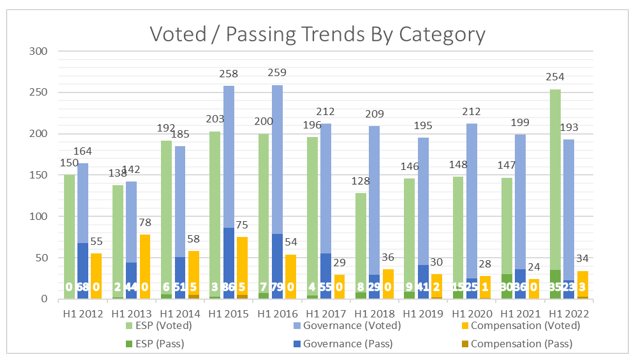

In the ten years we have been publishing our annual proxy season review, there has been a generally upward trend in the number of Rule 14a-8 proposals S&P Composite 1500 companies face each proxy season, a trend which has intensified in recent years. Following a record-breaking number of proposals in 2021, there were 797 submissions in H1 2022, compared to 733 in H1 2021 (and roughly 550 in H1 2012). There has been a shift, however, in the focus of shareholder proposals from governance topics to environmental and social/political topics (“ESP”). S&P Composite 1500 companies are now receiving far more ESP proposals (503 submitted in H1 2022 compared to 220 in H1 2012 and 408 in H1 2021), while the number of governance submissions in H1 2022 remained similar to H1 2012 (and declined from 2021). As a result, proposals on ESP now represent a much larger portion of total submissions, surging to 63% of submissions after reaching a majority of submitted proposals for the first time in the 2021 proxy season, driven by a 38% year-over-year (H1 2021 vs. H1 2022) increase in environmental proposals.

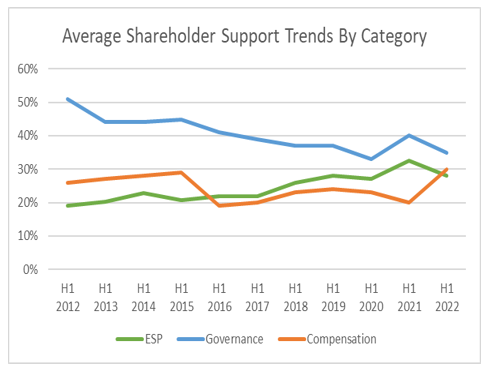

It is clear that the growing environmental, social and governance emphasis of proponents and other shareholders has altered proxy season engagement between shareholders and their investors over the course of the last decade. This year the SEC also had a significant impact on submission and voting trends. Notably companies had a significantly lower likelihood of obtaining no-action relief on ESP proposals following the SEC’s release of Staff Legal Bulletin No. 14L (“SLB No. 14L”, further discussed in Section H). For the first time, we observed that a majority of ESP submissions reached a vote. With institutional investors expressing concern over the increasingly prescriptive ESP proposals that went to a vote this year, support on ESP proposals decreased after steadily rising throughout the last decade, reaching the lowest average percentage of votes cast since 2018 (dropping to 28% in H1 2022 after increasing from 18% in H1 2012 to a record high of 32% in H1 2021). We expect the SEC’s extensive rulemaking on environmental, social and governance issues, as well as the efforts of other federal and state regulators and lawmakers on these topics, to have an even greater impact on submission, voting and engagement trends in future proxy seasons, as further discussed below.

The following table summarizes the Rule 14a-8 shareholder proposals submitted in full-year 2021 and 2022 year-to-date, the number voted on and the rate at which they passed:

The following charts illustrate trends in submitted, voted and passing Rule 14a-8 shareholder proposals since we began tracking the relevant data, as well as changes in shareholder support:

On July 13, 2022, the SEC proposed amendments to Rules 14a-8(i)(10), (i)(11) and (i)(12) (“Rule 14a-8 Proposed Amendments”) that would significantly narrow the standards for exclusion of proposals on grounds of substantial implementation, duplication and resubmission exclusions. If adopted as proposed, the Rule 14a-8 Proposed Amendments would not only result in a further increase in voted proposals but also is likely to mean that companies will face a larger number of submissions, more granular proposals, multiple proposals on the same topics at each meeting and similar proposals year after year.

B. Who Makes Shareholder Proposals

A small group of prolific proponents continued to drive submissions to U.S. S&P Composite 1500 companies. Once again, the top 10 proponents accounted for over 60% of proposals submitted.

The following table summarizes the submissions from the top shareholder proponents in 2022:

- Individuals. During the 2022 proxy season, the most prolific proponents were the same individual investors that have been active for a number of years—John Chevedden, Kenneth Steiner, James McRitchie, and Myra Young. Collectively, these four proponents, individually and as co-filers with other organizations and individuals, submitted 253 proposals, or 32% of all submissions this year. This group has traditionally focused on governance proposals. Although around 75% of their submissions in 2022 were governance-related, around 15% of proposals from this group were social proposals, as was the case in 2021, and these proponents submitted for the first time a meaningful number of proposals on compensation (focusing on CEO pay-ratio) issues.

- Social Investment Entities. Social investors, including asset management or advisory institutions with a mandate to make “socially responsible” investments or advance social causes, continued to be the main proponents of ESP proposals, submitting 221 ESP proposals, or 44% of all ESP-related proposals. As You Sow and Green Century Capital Management were the most prolific environmental proponents in 2022 and submitted 45% of all environmental proposals. Although the entities that have submitted high numbers of social proposals in recent years (e.g., Trillium Asset Management and Arjuna Capital) remained active in engaging with companies on social topics, their Rule 14a-8 proposals represented a smaller portion of our data this year than As You Sow and Green Century, perhaps because Trillium and Arjuna withdrew more often and before their submissions were included in proxy materials or reported to ISS.

- Public Pension Funds. Public-sector pension funds and related entities continued to be among the most prolific proponents on social issues, focusing in particular on human capital management and social capital management issues. The New York City and State retirement funds once again submitted the largest number of proposals among public pension funds (although the total number of submissions decreased compared to prior years), focusing on racial equity audits and political contribution disclosures this year. In contrast, California public pension funds such as CalPERS and CalSTRS, which have recently played important roles in ESG-related shareholder activism and urged the SEC to expand its climate-related proposal to require even more disclosures, once again submitted only a handful of proposals, focused on climate-related issues.

- So-Called “Anti-ESG” Proponents. There was a notable increase in the number of proposals submitted by so-called “anti-ESG” entities (i.e., entities that have self-identified or been identified by the media as “anti-ESG” for expressing concerns with commonly used ESG investment criteria), as well as individuals with known affiliation to these entities. This year, 54 proposals were identifiable as being submitted by these proponents, compared to 25 in full-year 2021). The National Center for Public Policy Research, which had been focusing on ideological diversity on the board for many years, continued to be one of the most prolific “anti-ESG” proponents, focusing on workplace diversity metrics, training and policies. In addition, another politically conservative group, the National Legal and Policy Center, which in recent years has focused on investigating potential corruption by Democratic politicians and Black Lives Matter leaders, submitted a meaningful number of proposals for the first time, including proposals on ideological board diversity and use of child labor in connection with electric vehicles. In 2022, “anti-ESG” proponents focused on demanding that companies assess the costs and benefits of ESP activities (e.g., climate-related activities, civil rights and racial equity audits), and report on their lobbying payments and policies as well as charitable contributions. In response to some companies’ commitments to abortion access after the Supreme Court’s overturned Roe v. Wade, some “anti-ESG” entities have already indicated that they will submit proposals on the topic of abortion. Out of the 54 proposals identifiable as being submitted by an “anti-ESG” proponent this year, 43 went to a vote and received average shareholder support of 9%. Companies were much more successful in excluding these proposals (including on “ordinary business” grounds), receiving no-action relief in 50% of the instances where relief was requested (compared to a 37% success rate across all proposals). Companies also had a 50% success rate for excluding social/political proposals from “anti-ESG” proponents, compared to 26% across all social/political proposals considered by the SEC. In addition, as further discussed below, this year, in cases where the same company received proposals addressing the same issue (e.g., civil rights audit) from both a social investment entity and an “anti-ESG” proponent, the “anti-ESG” proponent’s proposal received significantly lower support.

- Religious Organizations. Religious organizations continued to focus on ESP issues. They submitted a total of 73 proposals this year, representing a 40% increase from the prior year. Many of the active religious organizations were affiliated with the faith-based investor coalition, the Interfaith Center on Corporate Responsibility (ICCR), and they often co-filed proposals. Among the ICCR affiliates, proposals on civil and human rights, human capital management and climate-related issues were the most commonly submitted proposals. In addition to the healthcare, financial services and technology sectors commonly targeted by ICCR affiliates in previous years, the retail and consumer goods industry also received a significant number of proposals from these organizations in 2022. Mercy Investment Services was the most prolific religious organization in terms of submission.

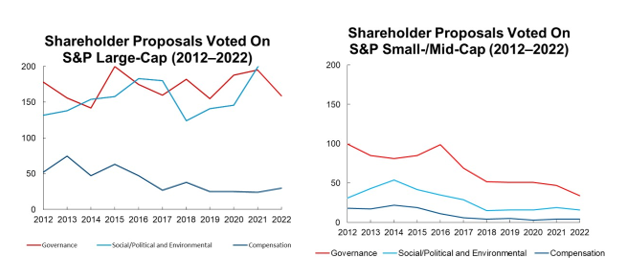

C. Targets of Shareholder Proposals

Traditionally, large-cap companies have received the vast majority of shareholder proposals. In 2022 so far, S&P 500 companies received 89% of proposals voted on, on par with 2021 (85%). The following graphs show the frequency of proposals, by category, voted on at large-cap companies compared to small- and mid-cap companies. Large-cap companies received a significantly higher number of proposals even though there are twice as many mid- and small-cap companies.

This year, retail and consumer goods companies, which represent only 7% of the S&P Composite 1500, received 18% of total submissions, outstripping all other industries. Companies in the healthcare/pharmaceutical and utilities and energy sectors, each of which also represent 7% of the S&P Composite 1500, received 15% and 14% of total submissions, respectively. Financial services companies, despite representing over 23% of the S&P Composite 1500, received 14% of total submissions. Companies in the technology and manufacturing sectors, which represent 12% and 10% of the S&P Composite 1500, respectively, each received 13% of total submissions. Proponents tended to focus on social issues in the retail/consumer goods, healthcare/pharmaceuticals and technology sectors, environmental issues in the utilities and energy sector, governance issues in the manufacturing sector and a mixture of governance and ESP issues in the financial services sector.

The complete publication, including footnotes, is available here.