Print

PrintJohn Ellerman and Don Kokoskie are Partners and Ira T. Kay is Managing Partner and Founder at Pay Governance LLC. This post is based on their Pay Governance memorandum.

Introduction

Pay Governance LLC provides counsel and advice to the Board of Directors’ Compensation Committees of more than 400 prominent publicly-traded companies. We frequently are requested to attend meetings of the Compensation Committee to provide our insights and advice regarding trends and developments as well as to render technical advice and services in executive compensation. Our ongoing client work and internal research as well as the Compensation Committee meetings we have attended during the 2022 proxy season give us a comprehensive view of the prevailing issues for Compensation Committees and how these issues are shaping the design and implementation of viable and effective compensation strategies.

The 2022 proxy season has occurred during a period of economic uncertainty for many companies. Companies are struggling with a declining stock market, supply chain shortages, high interest rates, inflation, and energy uncertainty. These economic factors have been coupled with an unprecedented regulatory push from the Securities and Exchange Commission (SEC). Additionally, institutional investors and proxy advisory firms have become more demanding in their relationships with and requirements of U.S. companies, including the proper role of other stakeholder objectives vis-vis those of investors. All these factors have influenced the issues around executive pay discussed by Compensation Committees.

The purpose of this discussion paper is to summarize the most prominent issues being discussed in the Committee meetings. Most of these issues have emerged as definitive trends in executive compensation, and we expect many of them will carry over into 2023 and the years beyond.

Summary of Important Issues

The following summary lists the most prominent matters being discussed by Compensation Committees:

1. SEC Regulatory Activity – On June 22, 2022, the SEC released its Spring Unified Agenda of Regulatory and Deregulatory Actions, which listed its short- and long-term regulatory actions. The remaining Dodd-Frank rules for executive compensation (i.e., clawback) are slated to be finalized this October in time for the 2023 proxy season. The table below summarizes important SEC proposed rules moved to the final rule stage and the planned action date.

| Proposed Rule | Final Action Date | SEC Objective |

| Pay Versus Performance | Finalized on 8/25/22 | To require issuers to disclose information that shows the relationship between executive compensation actually paid and the financial performance of the issuer |

| (Clawback) Listing Standards for Recovery of Erroneously Awarded Compensation | October 2022* | To prohibit the listing of securities of issuers that have not developed and implemented a policy providing for disclosure of the issuer’s policy on incentive-based compensation and mandating the clawback of such compensation in certain circumstances |

| Climate Change Disclosure | October 2022* | To enhance registrant disclosures regarding issuers’ climate-related risks and opportunities |

| Proxy Voting Advice | October 2022* | To remove conditions to the availability of certain exemptions from the information and filing requirements of the Federal proxy rules for proxy voting advice businesses |

| Share Repurchase Disclosure Modernization | October 2022* | To require an issuer to provide more timely disclosure on new Form SR regarding purchases of its equity securities for each day that it, or an affiliated purchaser, makes a share repurchase |

| Cybersecurity Risk Governance | April 2023 | To enhance and standardize disclosures regarding cybersecurity risk management, strategy, governance, and cybersecurity incident reporting by public companies |

| Modernization of Beneficial Ownership Reporting | April 2023 | To modernize the beneficial ownership reporting obligations and to accelerate the filing deadlines for initial and amended beneficial ownership reports filed |

| Rule 10b5-1 and Insider Trading | April 2023 | To add new conditions to the availability of an affirmative defense under an Exchange Act rule that are designed to address concerns about abuse of the rule to opportunistically trade securities on the basis of material nonpublic information in ways that harm investors and undermine the integrity of the securities markets |

* Final rules have not been published as of the date of this paper

The most extensive, detailed, and impactful new regulatory requirement from the SEC is the Pay Versus Performance (PVP) disclosure rules. On August 25, 2022, the SEC adopted final rules implementing the PVP disclosure requirement under the Dodd-Frank Act. The new rules are effective with fiscal year disclosures ending on or after December 16, 2022. Therefore, those public companies with calendar-year

fiscal years will be required to adopt and conform to the new disclosure rules in next year’s proxy season. The SEC’s intention is to provide more information to shareholders and other interested parties, on pay for performance alignment, the underlying objective of every effective executive pay program. While the policies are indeed well-intended, the actual mechanics of the regulation may fall short of that goal. For each of the fiscal years required to be disclosed, the Named Executive Officer (NEO) compensation metric, Compensation Actually Paid (CAP), captures the impact of performance, especially absolute stock price change, on the potential economic value of all outstanding unvested (or newly-vested) stock held by the executives, which typically includes all or portions of three to four years of awards (assuming equity awards vest over three or four years).

Unfortunately, this method is not comparable to the Summary Compensation Table (SCT) value that is placed next to the CAP amount for that year as it only contains the grant date value of only the most recent year’s grant. Thus, the CAP metric limits insights into how company and executive performance on stock grants yielded potentially realizable pay outcomes. Further, the table presenting the CAP and SCT values mandates two performance metrics: GAAP net income, which is rarely used as an incentive metric, plus a cumulative stock price index — starting from $100 ¾ which is calculated the same as the index disclosed in the annual report. This type of index is also rarely used by companies to evaluate their performance. Further, this indexed value will eventually reset annually based upon a new $100 starting point for each year while the CAP value for that year is frozen. These various incompatibilities will make a robust and accurate assessment of pay for performance alignment difficult. To be effective and accurate, this will likely require extensive additional analysis and narrative disclosure describing this alignment. This runs counter to many outside attorneys who are suggesting companies take a minimalist approach and refer the proxy-readers to the CD&A.

The new PVP disclosure requirements require management and the Compensation Committee to:

- Prepare a new PVP table that includes the company’s SCT total pay for the CEO and average SCT of the remaining proxy Named Executive Officers (NEOs), the Compensation Actually Paid (CAP) amount for the CEO and the average CAP for the other NEOs, cumulative total shareholder return (“TSR”) for the company and the company’s selected peer group, and the inclusion of a Company-Selected Metrics (CSM);

- Include a narrative explanation of the relationship between the reported CAP for the CEO and average of the other NEO and GAAP net income, company TSR, and the CSM, as well as an explanation of how the company’s TSR tracks with the peer group’s TSR. As discussed, there are several major challenges to the effectiveness of this new approach;

- Prepare a tabular list of the three to seven most important performance measures used by the company to determine the current year’s CAP amount and from that list determine which measures was the most important determining the current year’s CAP amount, and to include that measure as the “Company-Selected Metric (CSM) in the PVP table; and

- Evaluate whether to include supplemental measures of performance and other explanatory material such as charts and graphs to aide in explaining the relationships of CAP and performance and company TSR and peer TSR.

The SEC initially proposed companies develop Clawback Policies in July 2015 with the release of initial proposed rules governing such policies. In June 2022, the SEC reopened the comment period for 30 days for the proposed clawback rules. Most companies have voluntarily implemented clawback policies. However,

the SEC is still debating if an accounting restatement due to material noncompliance should be interpreted to trigger the clawback rules if the restatement is a “little r” restatement in addition to the required “Big R” restatement.

Another matter of interest to the SEC is Share Purchase Disclosure. The SEC has proposed amendments to the current rules on corporate share repurchase disclosures, which would require companies to disclose share repurchases more frequently in a new Form SR and to provide additional details for repurchases and repurchase plans in period reports such as the 10-K.

The SEC is also actively studying the rules around 10b5-1 Stock Trading Plans and would significantly increase the requirements a trading plan would need to meet to be allowed as an affirmative defense against claims of insider trading. Executives and companies may find these provisions overly restrictive, which may diminish their use.

Another active area of interest of the SEC is proposed rule amendments requiring companies to include certain climate-related information in registration statements and periodic reports, which could influence if or how companies include such results in their incentive plans, especially if the disclosure of climate targets triggers the need to have such measures assured by a 3rd party, as proposed under the rules.

2. Alignment of ESG and Incentives – The pandemic along with economic challenges and pressures from various stakeholders have accelerated the pace at which companies have adopted environmental, social, and governance (ESG) metrics in their incentive plans. Large companies (S&P 500) have adopted ESG metrics at a higher rate (83%) than smaller companies (Russell 3000, 28%). The energy and utility sectors have demonstrated the greatest usage as they historically have implemented safety, environmental and customer satisfaction measures into incentives. The vast majority of companies (88%) in the S&P 500 include ESG metrics in the annual incentive plan whereas only 12% of such companies include ESG metrics in the long-term incentive plan. To date, most ESG metrics have been qualitative of their application in incentive compensation plan designs. However, we are finding institutional shareholders and other stakeholders are pressing companies to move their metric applications from a qualitative to a quantitative approach going forward. We expect to see the trend of quantitative ESG metrics to continue for the next several years as companies become more comfortable with ESG measurement and have better data with which to benchmark their ESG goals, although this might present some unintended legal risks.

3. Legislative Activity – In August 2022, Congress adopted the Inflation Reduction Act of 2022. Included in the legislation is a key provision to levy a one percent (1%) excise tax on company share repurchases. The Biden administration has also introduced in its 2023 budget proposal a provision prohibiting executives from selling shares for three years after a company share repurchase. If this provision is retained in the final budget, we anticipate companies may replace share repurchases with special dividends.

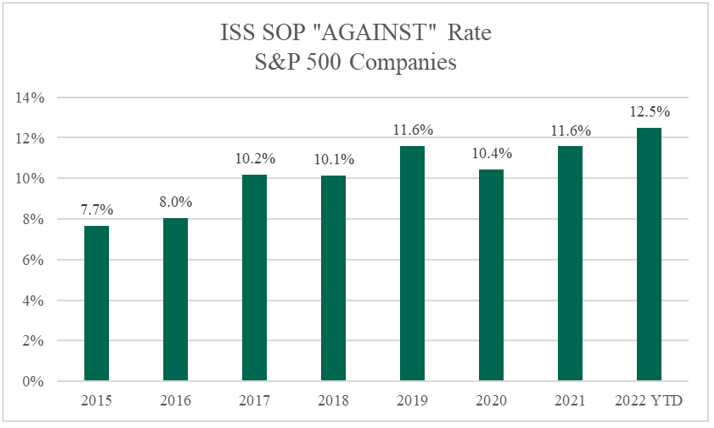

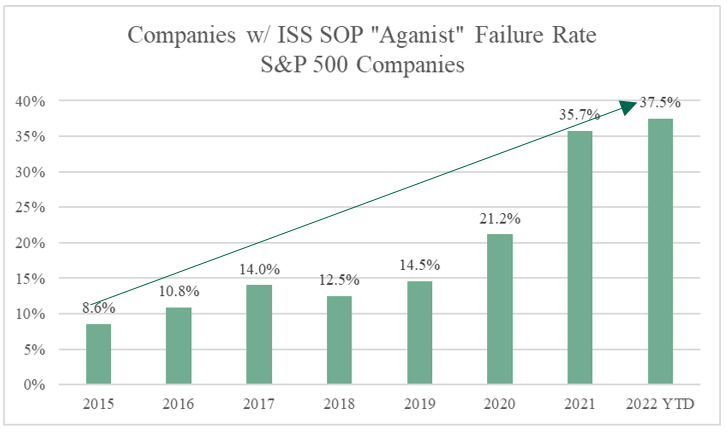

4. Say on Pay (SOP) Vote Results – As of August 31, 2022, 21 of 448 S&P 500 companies (4.7%) failed SOP during 2022, which is higher than the failure rate of 4.1% in 2021. Institutional Shareholder Services (ISS) issued against recommendations on SOP for 56 S&P 500 companies. This rate of opposition by ISS (12.5%) is the highest percentage of against recommendations it has ever delivered. Further, the average SOP support for these 56 companies was 54% (versus 92% among those with a “for” recommendation from ISS). These results suggest ISS’s SOP vote recommendations may be carrying more weight with investors.

5. Key Trends From ISS – During 2022, the average shareholder support for companies receiving an “against” vote from ISS declined to 60% whereas it had averaged 70% in years past. ISS has shown an increasing sensitivity to the magnitude of pay. The ISS model may not work for mega-cap companies since it is hard to find comparable companies of the same market cap size. Further, ISS has continued to expand its list of problematic practices — new problematic practices include:

- Incentive plans with no caps

- Incentives which appear to rely on discretion

- ESG modifiers which contribute to maximum payouts despite subpar achievement of financial goals

- Special retention awards or the majority of long-term incentives delivered in the form of time-based awards

- Plans using r-TSR and delivering target awards at median results or failing to cap payouts for negative TSR

- Consulting agreements with a former executive officer offering excessive pay (stealth way to provide termination benefits)

- Failure to adequately address shareholder concerns a year after failing SOP

One area where we have found companies addressing a particular shareholder concern is a long-term incentive plan which pays at target award levels if the company achieves a relative TSR equal to the 50th percentile or median of the peer group. Many companies are modifying their plans to include a 55th percentile relative TSR achievement for the payment of target award levels to plan participants.

Another area of note has been the valuation methodology used by ISS in valuing stock options. ISS’s stock option values are up to three times [higher?] than the accounting values reported by companies. Rather than using longer-term volatility assumptions called for under accounting rules, ISS has continued using the most recent three-year period that largely reflects major, pandemic-related market swings. Also, ISS values options using their full term (often 10 years) rather than their expected life. This ISS valuation methodology often results in companies appearing to have a far greater long-term incentive weighting on stock options than that of their median peer.

6. Shareholder Proposals – Over the past 18 months, high-profile companies have received a growing number of shareholder proposals (n=60+) focused on human resource issues. These proposals generally have called for increased disclosure — the most prevalent topics include:

- Disclosure of unadjusted median gender pay gap

- Disclosure/elimination of mandatory arbitration in cases of alleged harassment or discrimination

- Demand for racial equity/civil rights audits

- Report on diversity, equity, and inclusion

It is not surprising ISS has supported these proposals since ISS typically favors greater transparency. More importantly, three large institutional investors (BlackRock, State Street and Vanguard) have dramatically increased their support of such shareholder proposals.

Closing Remarks

Discussions within Compensation Committee meetings have been lively in recent months. As companies struggle with a difficult economy, competing stakeholders’ interests and a declining stock market, we expect the discussions in future months will be rigorous as well, and executive pay issues will continue to draw debate. We will keep you apprised of future developments in the coming months as they unfold.