Print

PrintJoshua Lichtenstein and Michael Littenberg are Partners, and Reagan Haas is an Associate at Ropes & Gray LLP. This post is based on a Ropes & Gray memorandum by Mr. Lichtenstein, Mr. Littenberg, Ms. Haas, and Jonathan Reinstein.

Introduction

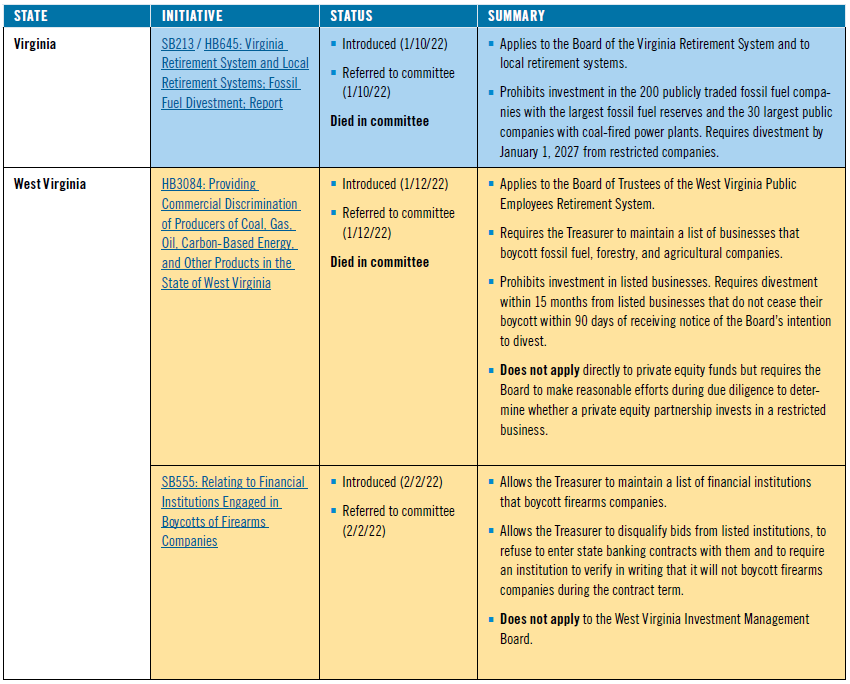

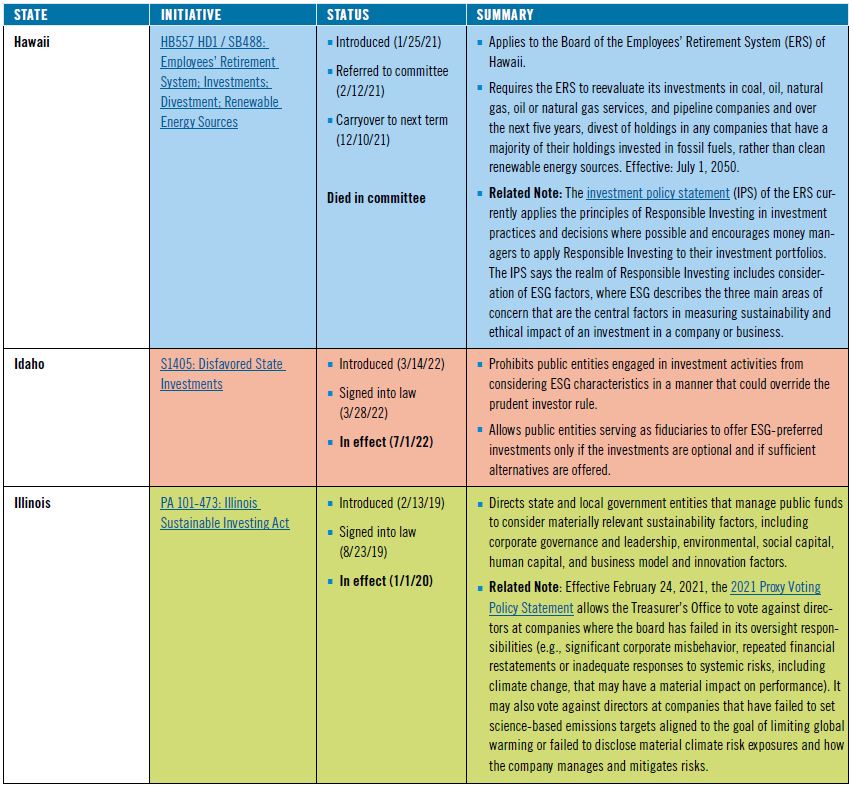

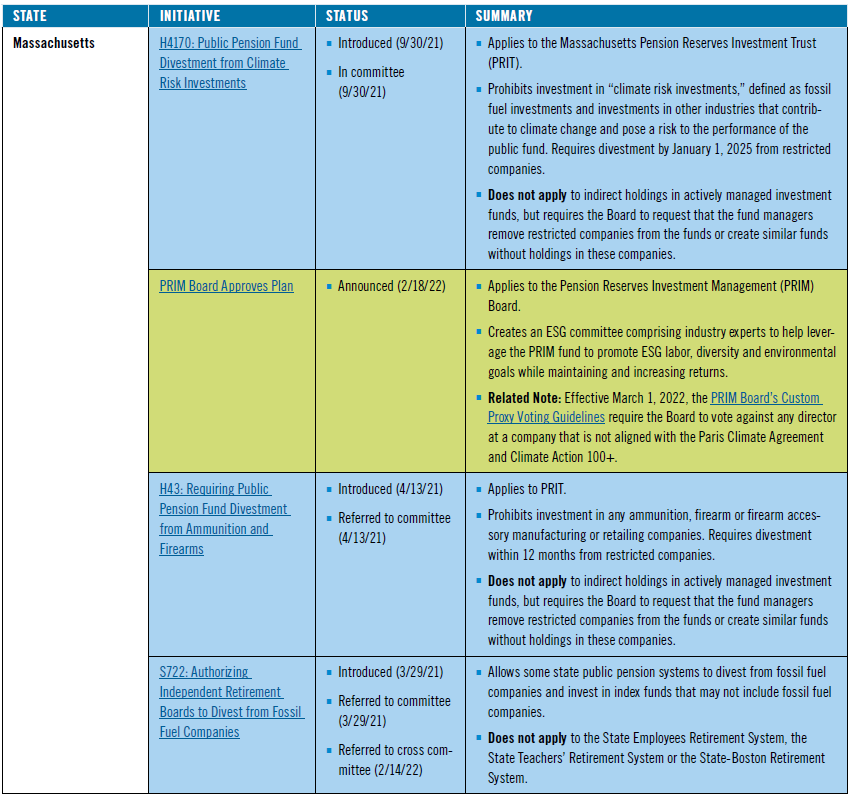

The growing divide in the ESG regulatory landscape between states became clear with the passage of legislation in Maine and Texas in 2021, which adopted contradictory ESG policies for state pension fund investments. Maine enacted legislation prohibiting investment by the Maine Public Employees Retirement System in the 200 largest publicly traded fossil fuel companies, as determined by the carbon in their reserves. Additionally, the law requires the retirement sys- tem to divest from these restricted companies by January 1, 2026. Similar legislation has been proposed in California, Hawaii, Massachusetts and New Jersey, among others, in recent months.

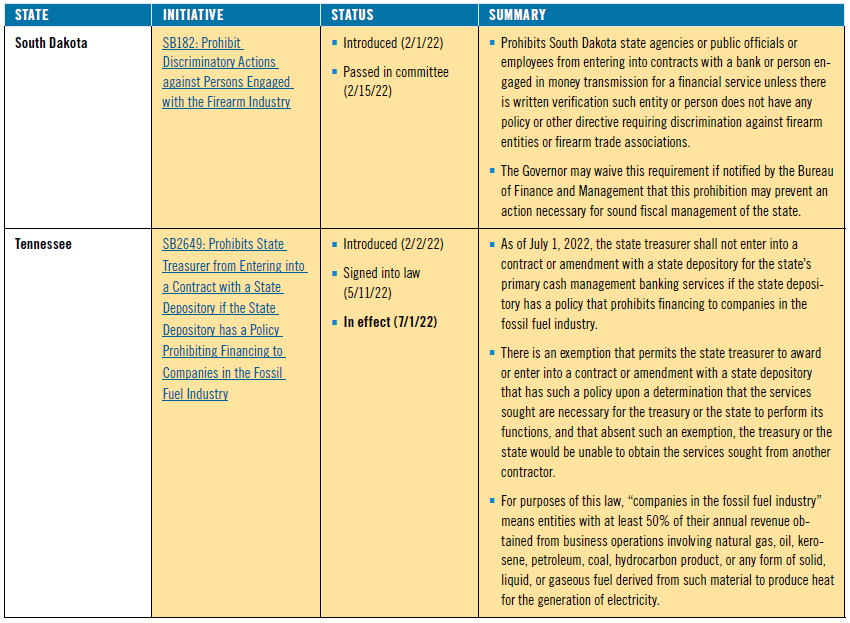

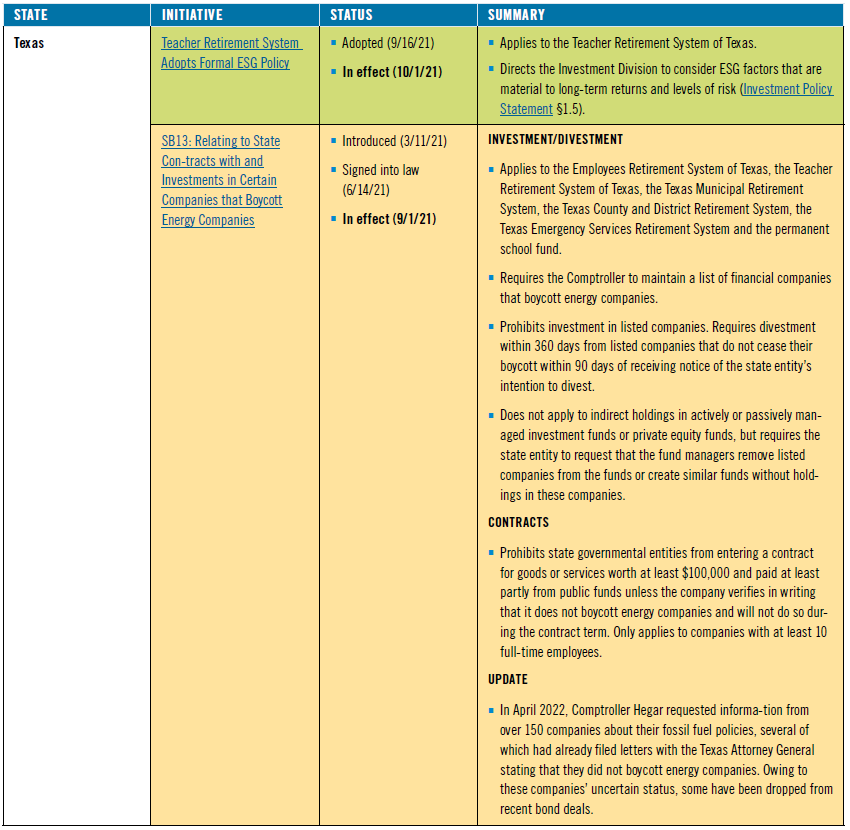

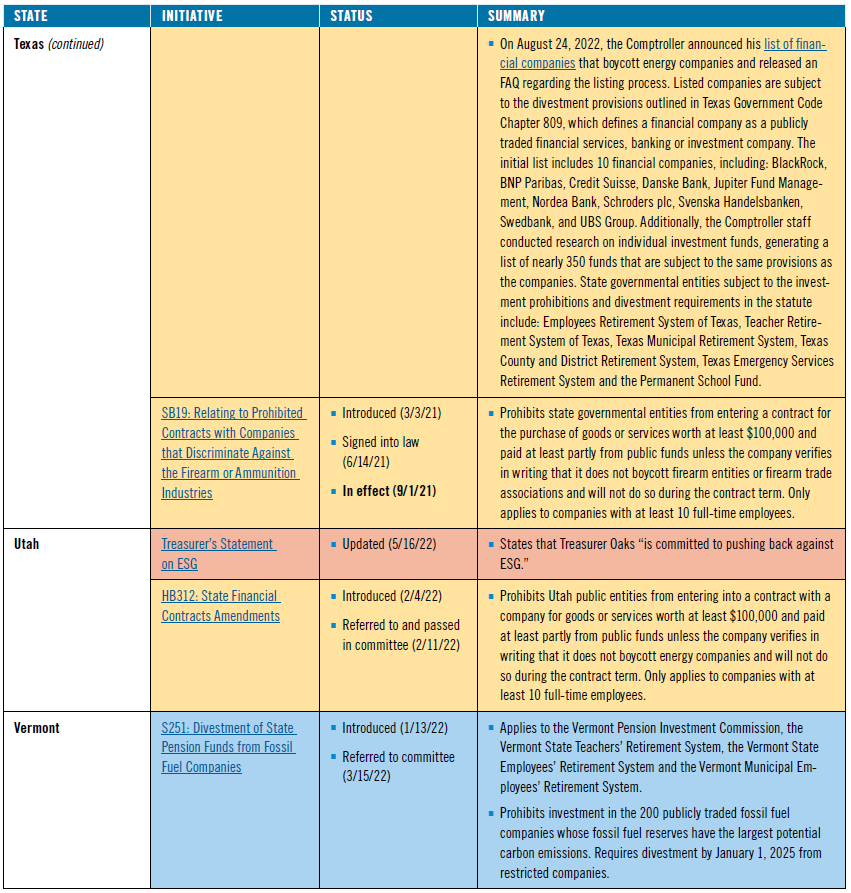

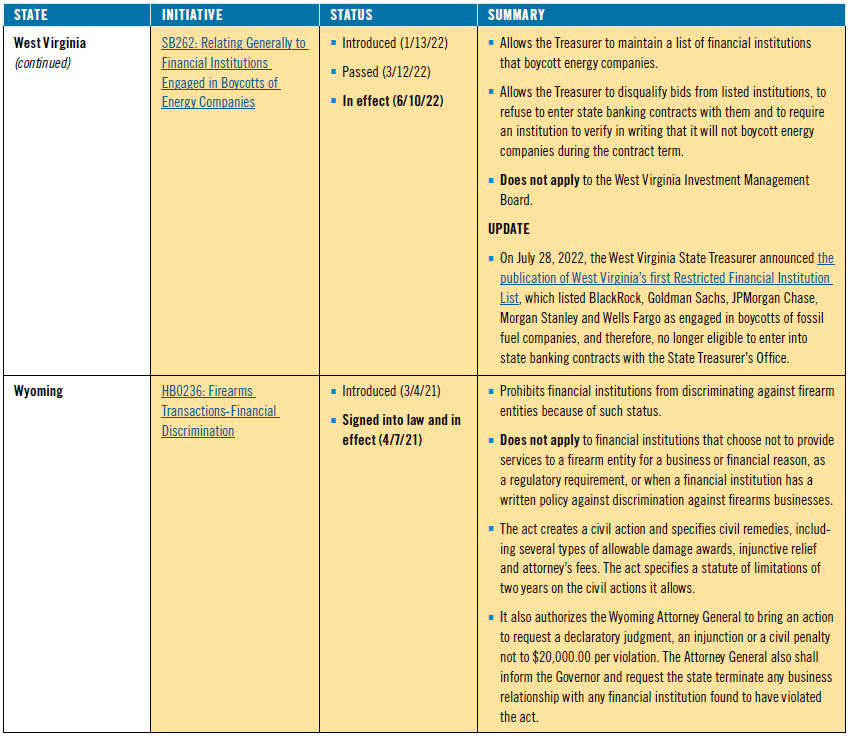

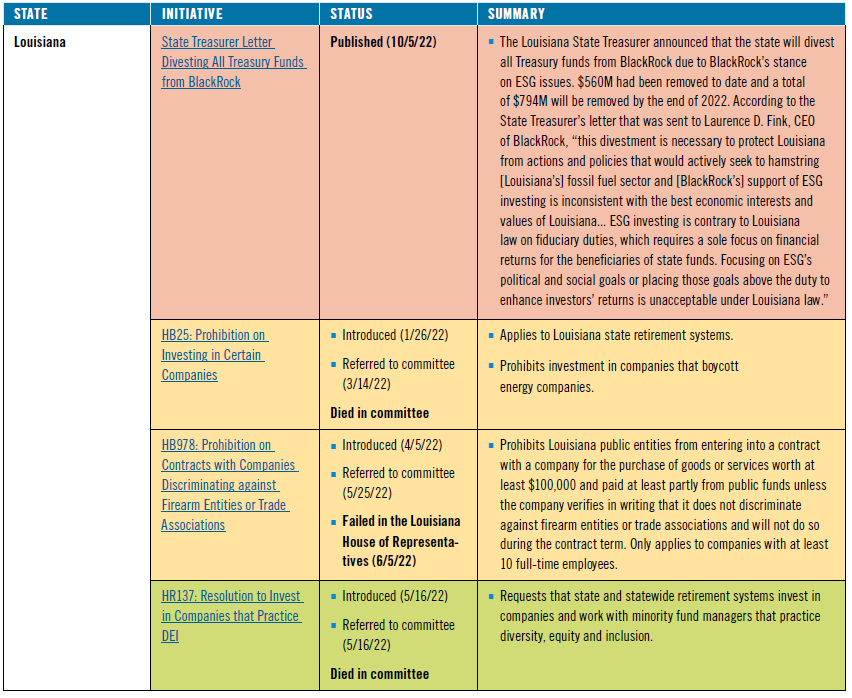

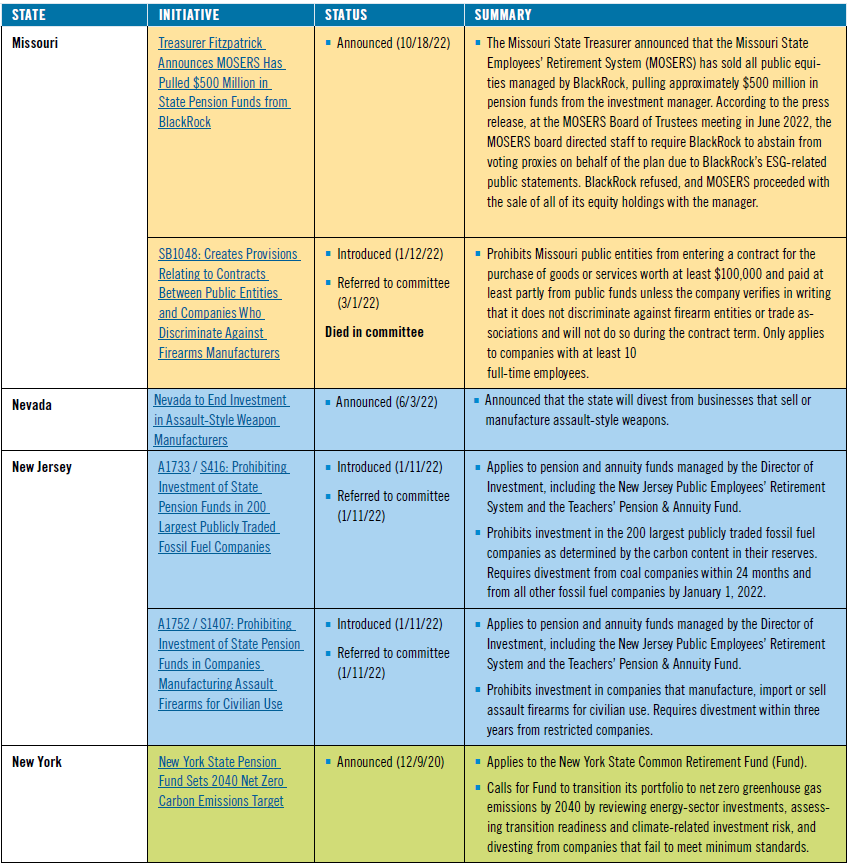

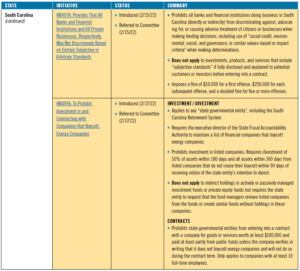

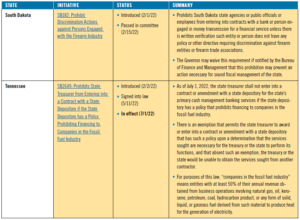

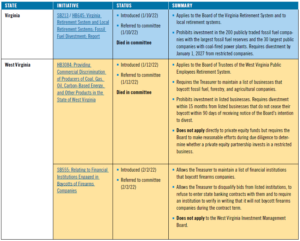

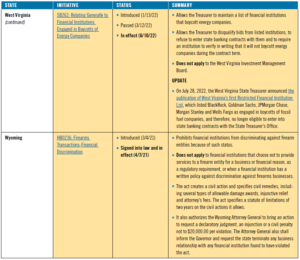

Conversely, the approach Texas took last year (which several other states have considered since) is to prohibit the state from entering into banking and financial contracts with financial companies that boycott firearms or energy companies. Several months ago, state officials in Texas began warning financial institutions that their boycotting activities endanger these companies’ ability to do business with the state, which ultimately culminated in the publication of a list of companies considered to be boycotters. Some government entities have started preemptively excluding targeted financial institutions from bond deals to avoid having to switch underwriters once the states finalize their list of restricted institutions. The state treasurers of Louisiana, Missouri and South Carolina each recently announced certain divestitures based on the ESG views of a manager.

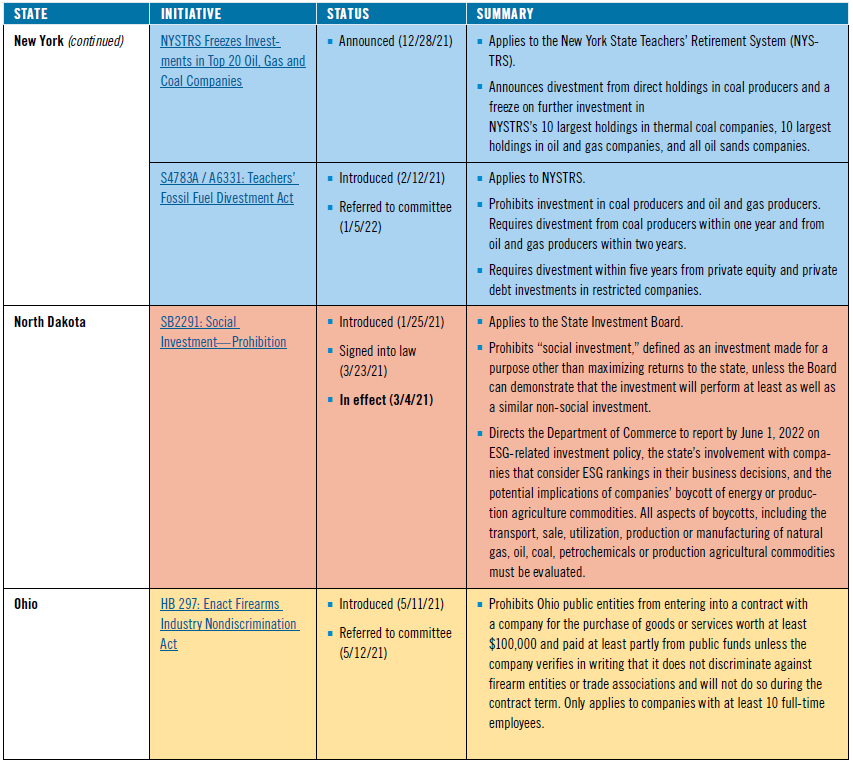

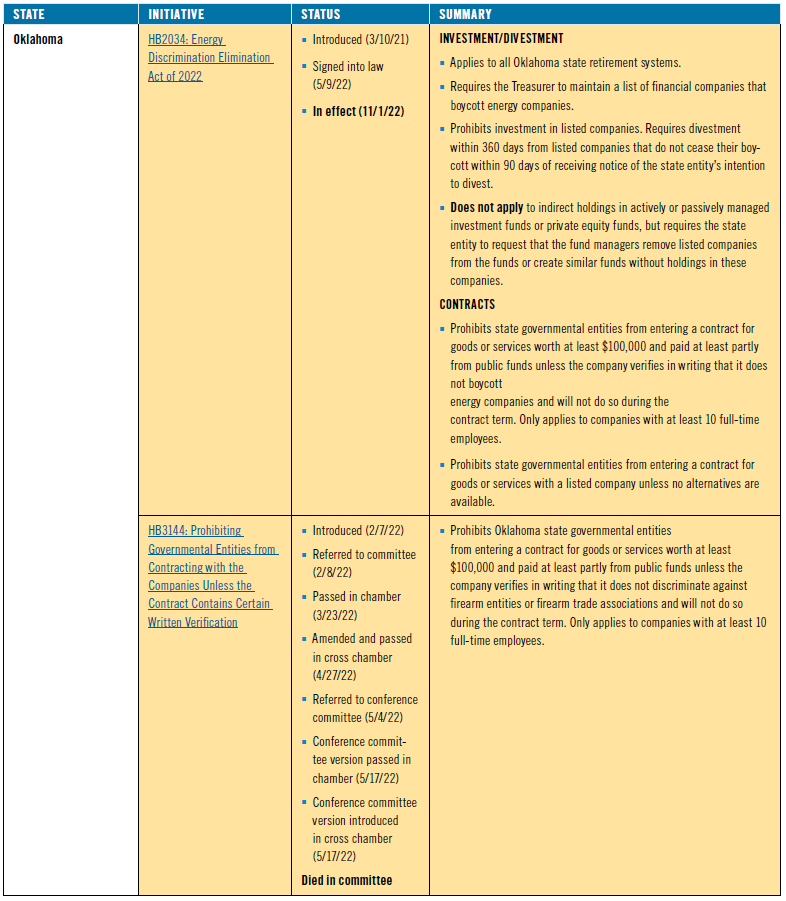

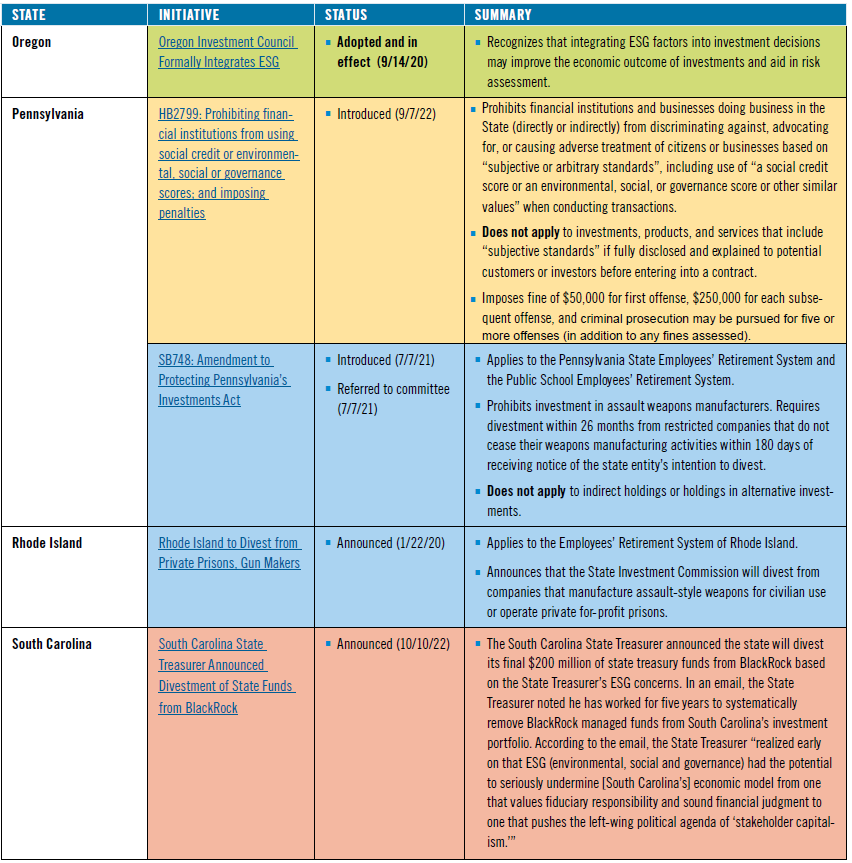

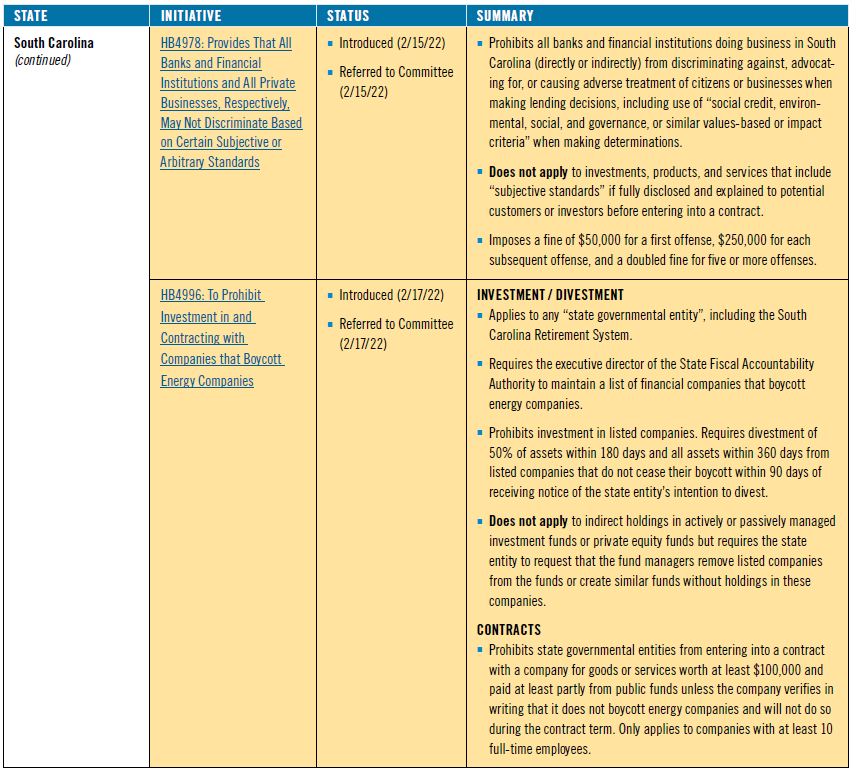

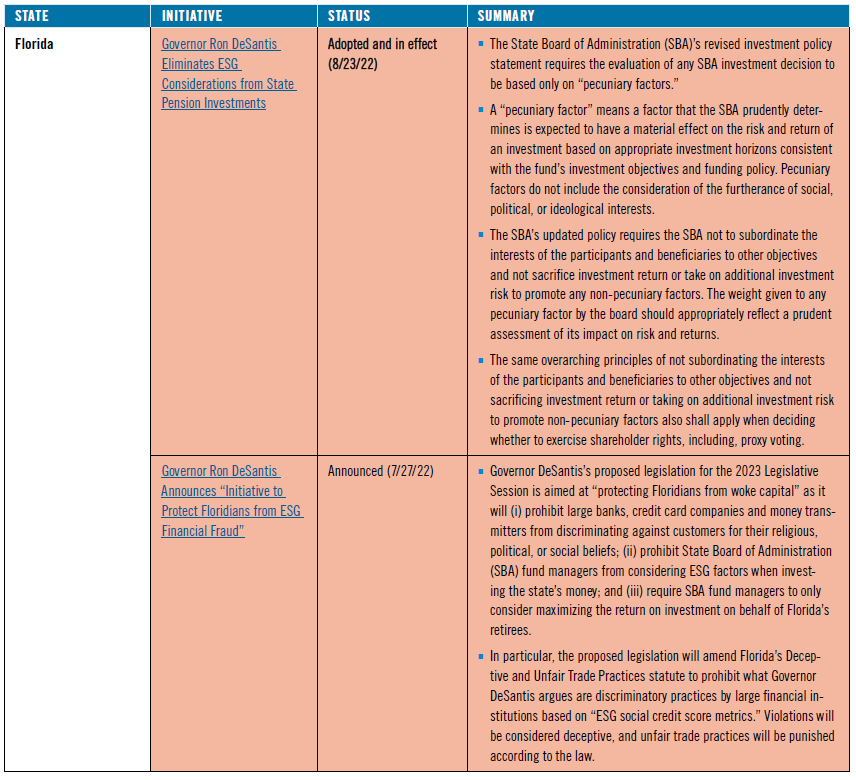

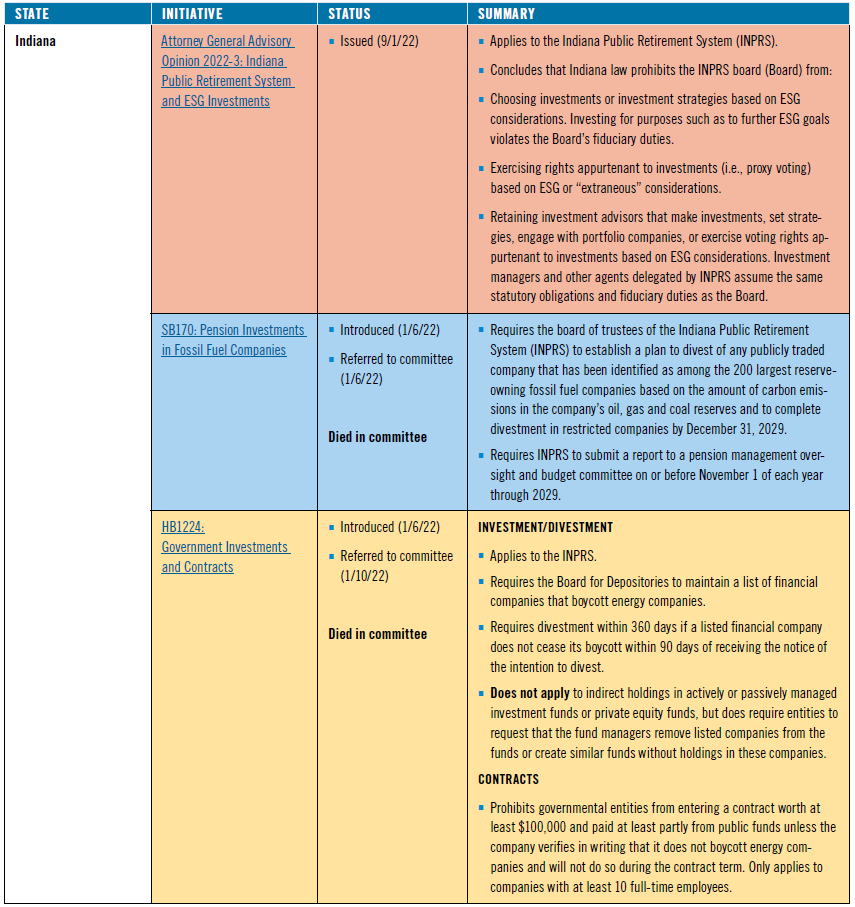

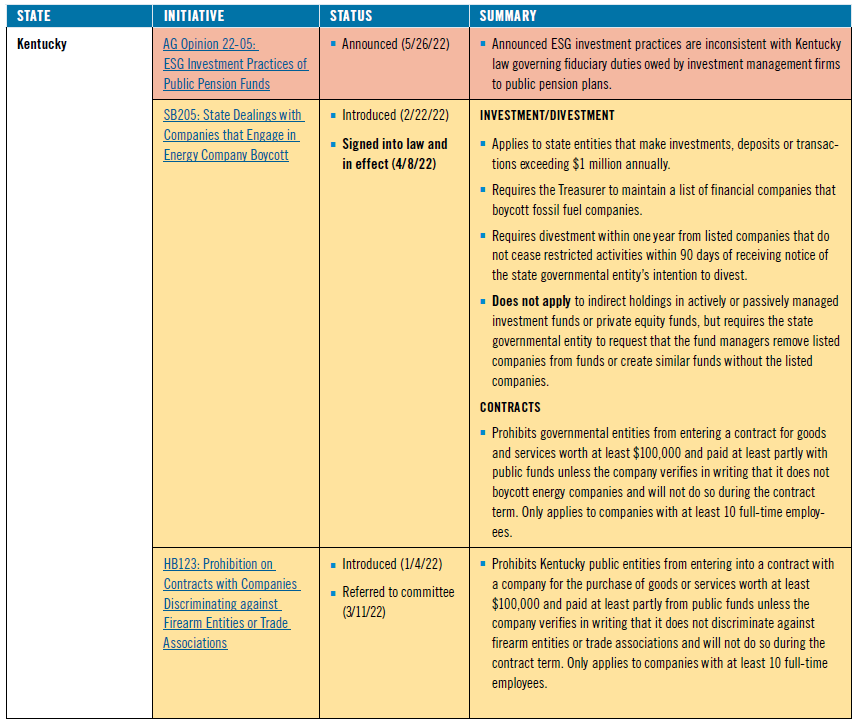

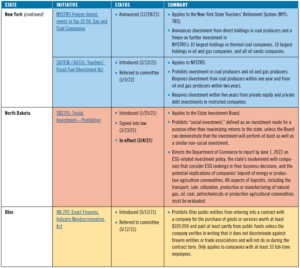

This divide has deepened as more than a dozen states introduced new initiatives over the last year seeking to either divest state pension funds from gun and ammunition, oil and gas, and/or coal companies or, conversely, to require state pension fund divestment from companies that boycott fossil fuel companies. At least one state, Indiana, has considered measures both to divest from fossil fuel companies and to divest from fossil fuel boycotters. In August, the State Board of Administration (SBA), the governing body of the Florida Retirement System Defined Benefit Pension Plan, revised the plan’s investment policy statement to say that investment decisions must be based only on pecuniary factors, and these do not include the consideration of the furtherance of social, political, or

ideological interests. Moreover, the SBA may not sacrifice investment return or take on additional investment risk to promote any non-pecuniary factors when making investments or proxy votes.

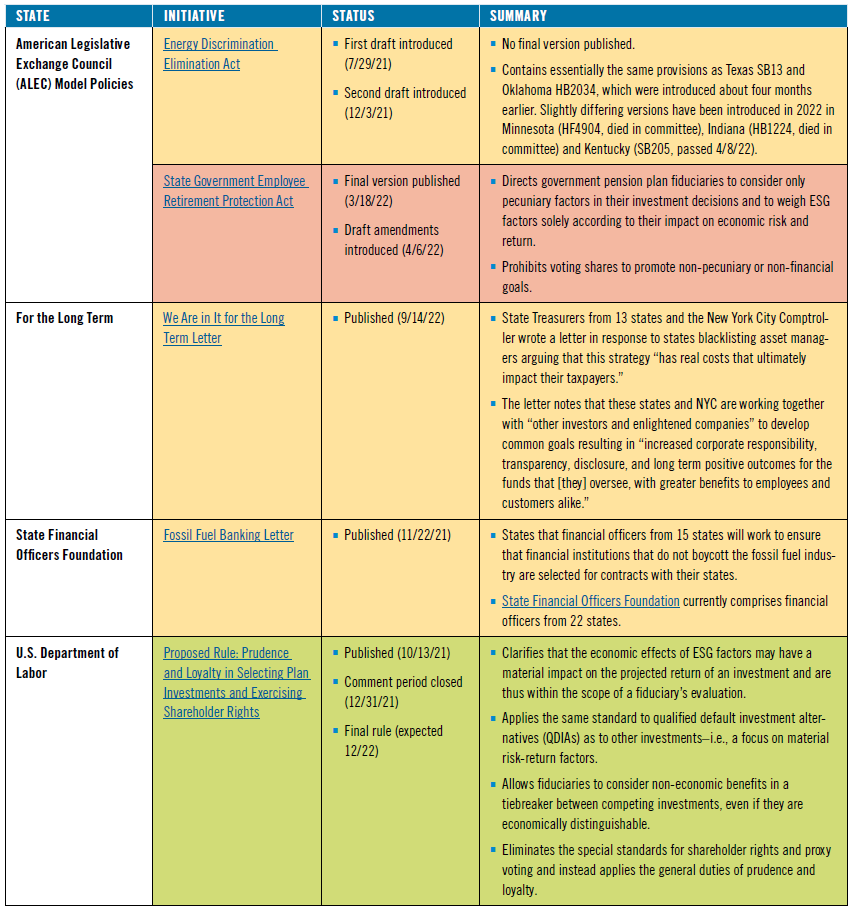

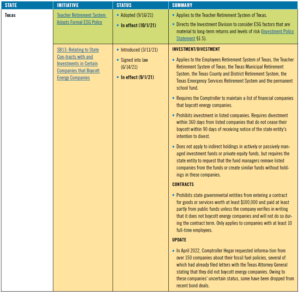

Beyond legislation on divestment and state contracts, states are deploying task forces, investigations and report committees to encourage or discourage ESG investing. Additionally, some pension funds are adopting their own ESG investment and proxy voting policies, notwithstanding what their state mandates say. For example, only two weeks after the Texas fossil fuel boycott divestment bill took effect, the Teacher Retirement System of Texas announced that it would consider material ESG factors in its investment decisions.

Other Related Initiatives

Other Related Initiatives