Print

PrintSubodh Mishra is Global Head of Communications and Georgina Marshall is Global Head of Research at Institutional Shareholder Services, Inc. This post is based on an ISS publication by Kathy Belyeu, Michael Ellis, Hailey Knowles, and Renata Schmitt Silva.

Overview of Process and Response

This document summarizes the findings of the ISS 2022 Global Benchmark Policy Survey, which opened on August 3 and closed on Aug. 31,2022.

The survey is a part of ISS’ annual global policy development process, and was, as is the case every year, open to all interested parties to solicit broad feedback on areas of potential ISS policy change for 2023 and beyond.

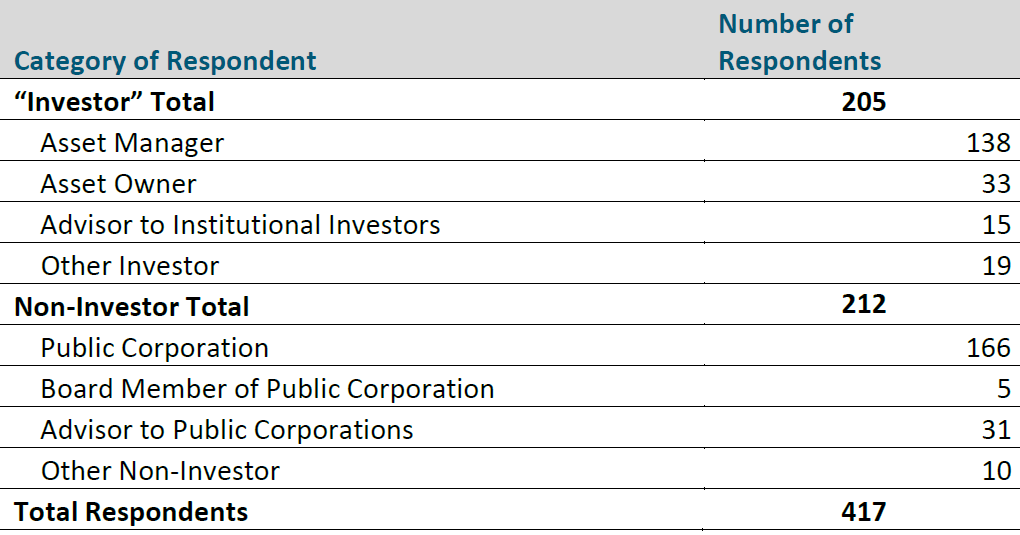

We received 417 responses to the survey: 205 responses from investors and investor-affiliated organizations, 212 from non-investor respondents. Responses that lacked an email address were not accepted. Multiple responses from the same person were also not accepted; only the response submitted last was counted.

Number and category of respondents to online benchmark policy survey

Of the 205 institutional investor respondents, 67 percent represented asset managers and 16 percent represented asset owners.

Of the 212 non-investor responses, responses from representatives of public corporations were by far the most prevalent, representing 78 percent, or 81 percent if including the board members of public corporations who responded under that separate category. Responses from non-profit organizations were deemed to be “investor” responses in cases where the organization is considered to be representing investor interests or views and “non-investor” responses in cases where the organization is considered to be representing company interests or views. Responses from academics are reported here with other non-investor responses.

Several institutional investors provided feedback to ISS through avenues other than the online survey. These responses were not aggregated in the survey results but will be considered qualitatively during the policy development process.

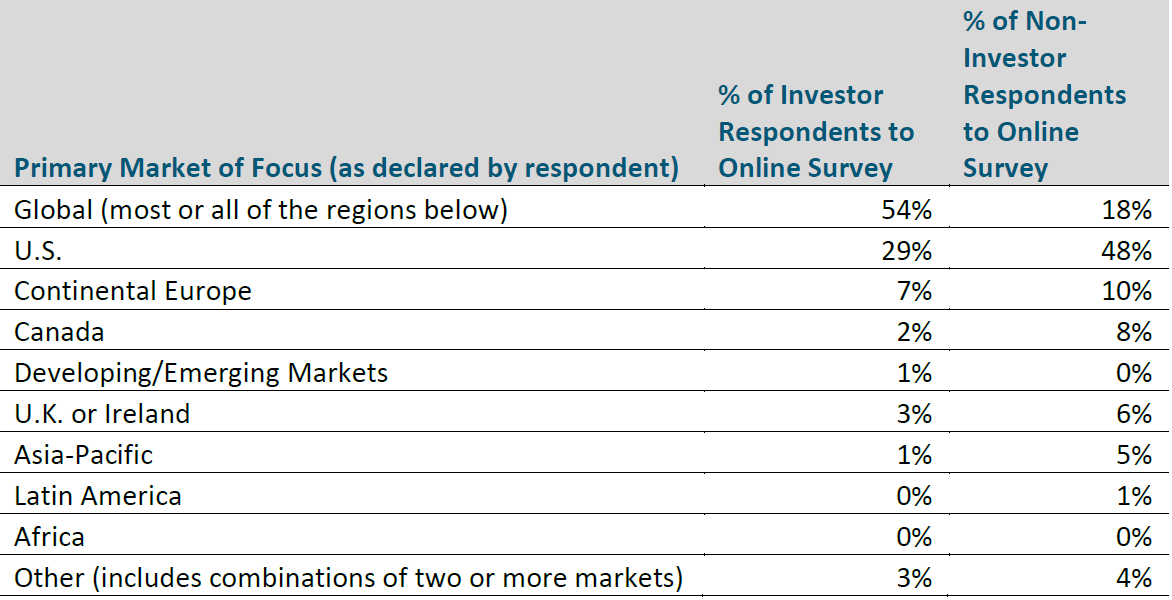

Over half of the investor respondents to the online survey represented organizations that covered most or all global markets. The largest group of non-investor respondents had the U.S. as their primary market of focus.

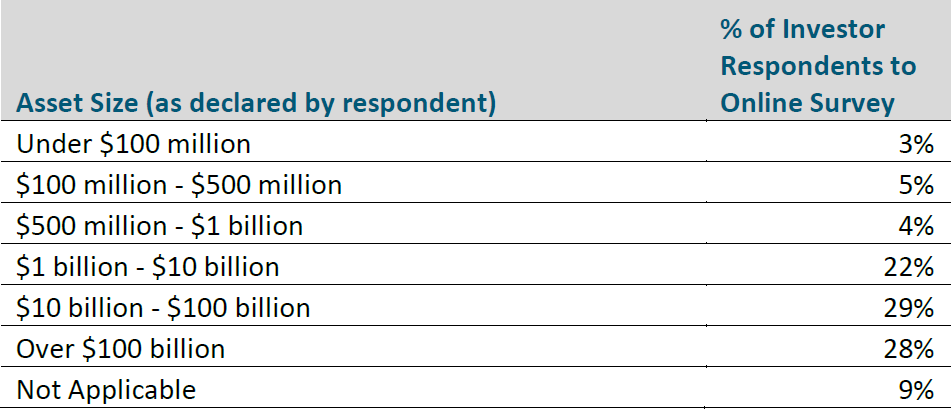

The breakdown of investors by the size of assets owned or assets under management is as follows:

Some respondents answered every survey question; others skipped one or more questions. Throughout this report, response rates are calculated as a percentage of the valid responses received on each question from respondents by category, excluding blank responses. Survey participants who filled out the “Respondent Information” but did not answer any of the policy questions or who did not provide identifying information have been excluded from the analysis and are not part of the count or the summaries above.

For questions that allowed multiple answers, rankings are based on the percentage of responses for each answer choice (percentages indicate what percentage of that category of respondent selected that answer – they will not total 100 percent). Percentages for other questions may not equal 100 percent due to rounding.

Key findings

Climate-Related Board Accountability:

A significant majority of both investor and non-investor categories of respondents expressed that they would consider there to be a material governance failure if a company that is considered to be a significant contributor to climate change is not providing adequate disclosure with regards to climate-related oversight, strategy, risks and targets according to a framework such the one developed by the Task Force on Climate- related Financial Disclosures (TCFD). Investor respondents generally agreed that the boards of companies that are large greenhouse gas (GHG) emitters are failing if they do not take steps to address emissions, but support for different actions that could be taken to address emissions varied. Besides a company failing to provide adequate disclosure according to a recognized framework, the three most common choices by investor respondents as demonstrating failures were targets-related, and were (i) a company not setting realistic medium-term targets (through 2035) for Scope 1 & 2 only (50% of investors), (ii) not declaring a net-zero by 2050 ambition (47% of investors), and (iii) not setting realistic medium-term targets (through 2035) for Scope 1, 2 & 3 if Scope 3 is relevant (45% of investors). A strong majority of investor respondents (69 percent) chose at least one of those “targets” responses, which was also the case for 43 percent of the non-investor respondents.

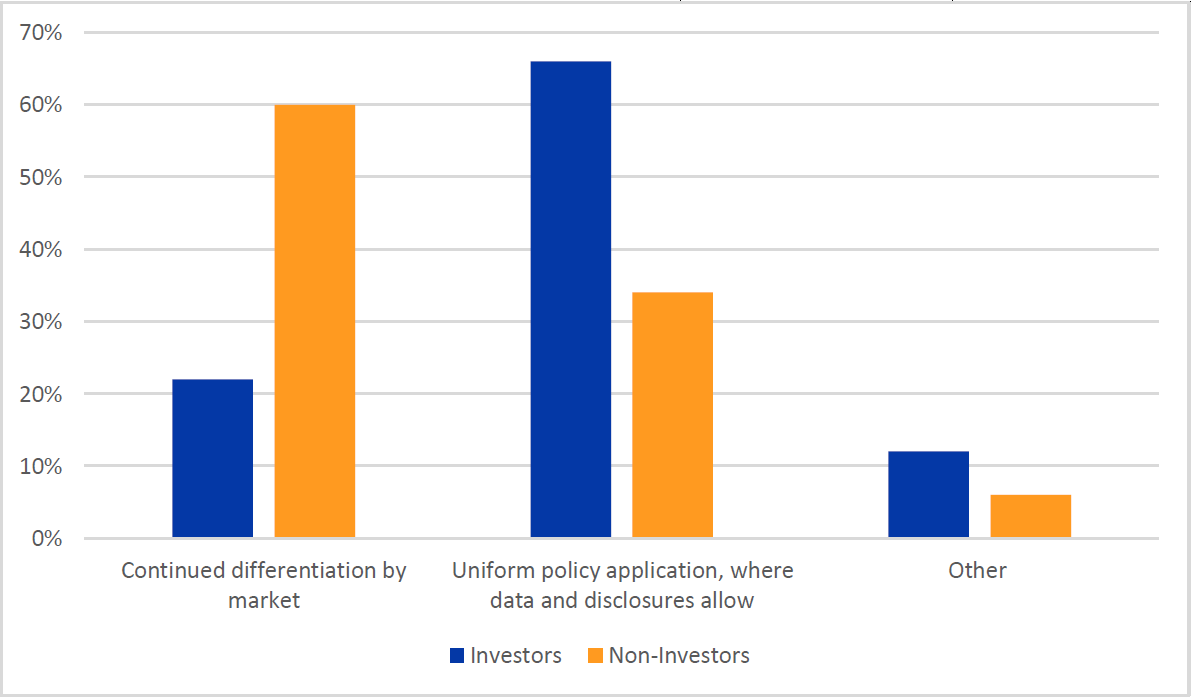

For 2022, the ISS Climate Board Accountability policy was only applied to certain markets (U.S., U.K. & Ireland, Continental Europe, and Russia). The majority of investor respondents (66 percent) voiced support for applying this policy across all markets. , Non-investor respondents tended to favor continued differentiation by market (60 percent). Several respondents submitted comments generally supportive of applying the policy across all markets, while cautioning that there may be a need for continued differentiation between developed and emerging markets.

Management Say-on-Climate Proposals:

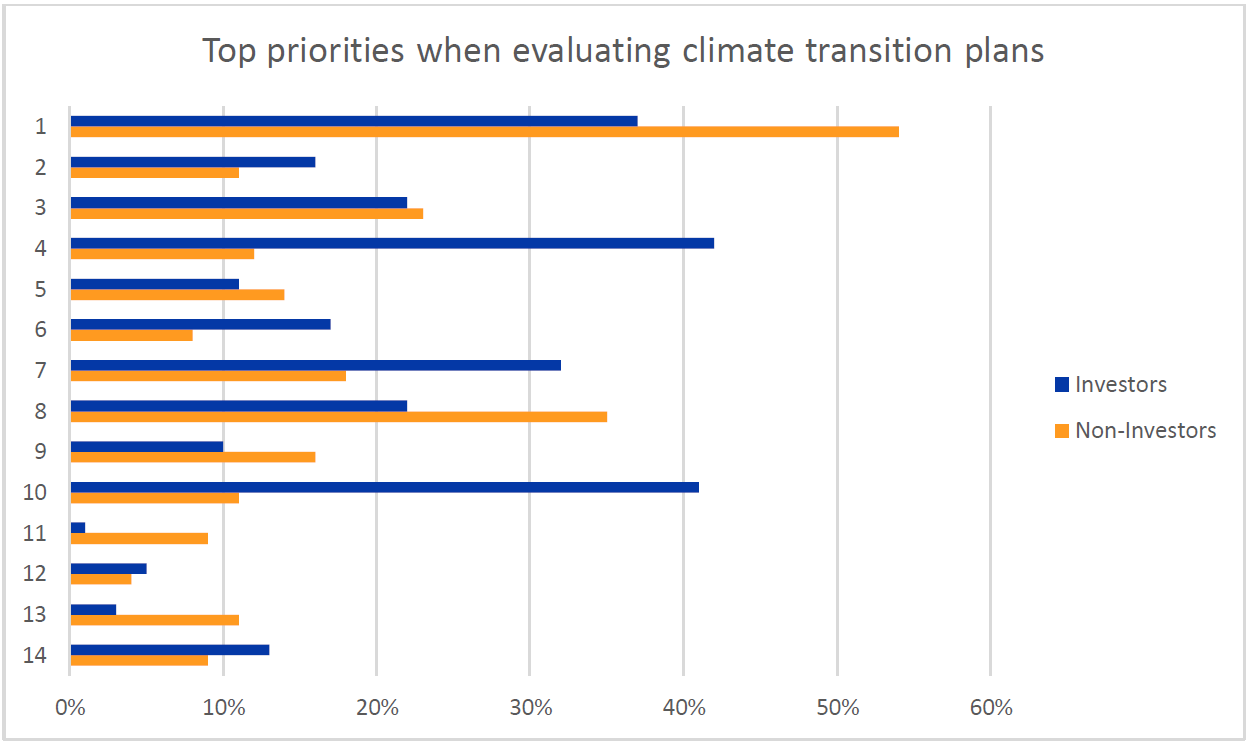

When asked “What do you consider to be the top three priorities when determining if a company’s transition plan is adequate?”, the most popular responses among investor respondents were (i) whether the company has set adequately comprehensive and realistic medium-term targets for reducing operational and supply chain emissions (Scopes 1, 2 & 3) to net zero by 2050 (42 percent), (ii) whether the company’s short- and medium-term capital expenditures align with long-term company strategy and the company has disclosed the technical and financial assumptions underpinning its strategic plans (41 percent), (iii) and the extent to which the company’s climate-related disclosures are in line with TCFD recommendations and meet other market standards (38 percent). The appropriateness of submitting management say-on-climate plans for shareholder approval was questioned by some investor respondents who believe these proposals improperly shift the responsibility for a company’s climate transition plan away from the board and management toward its shareholders.

The most popular choices among non-investor respondents for assessing management say-on-climate proposals were whether the company’s disclosures are in line with TCFD recommendations and other market standards (54 percent), and whether the company discloses a commitment to report on the implementation of its plan in subsequent years (35 percent). The third most popular choice selected by non-investors was whether the company has comprehensive and realistic medium-term targets for reducing operational emissions (Scopes 1 & 2) to net zero by 2050 (23 percent).

Climate Risk as Critical Audit Matter

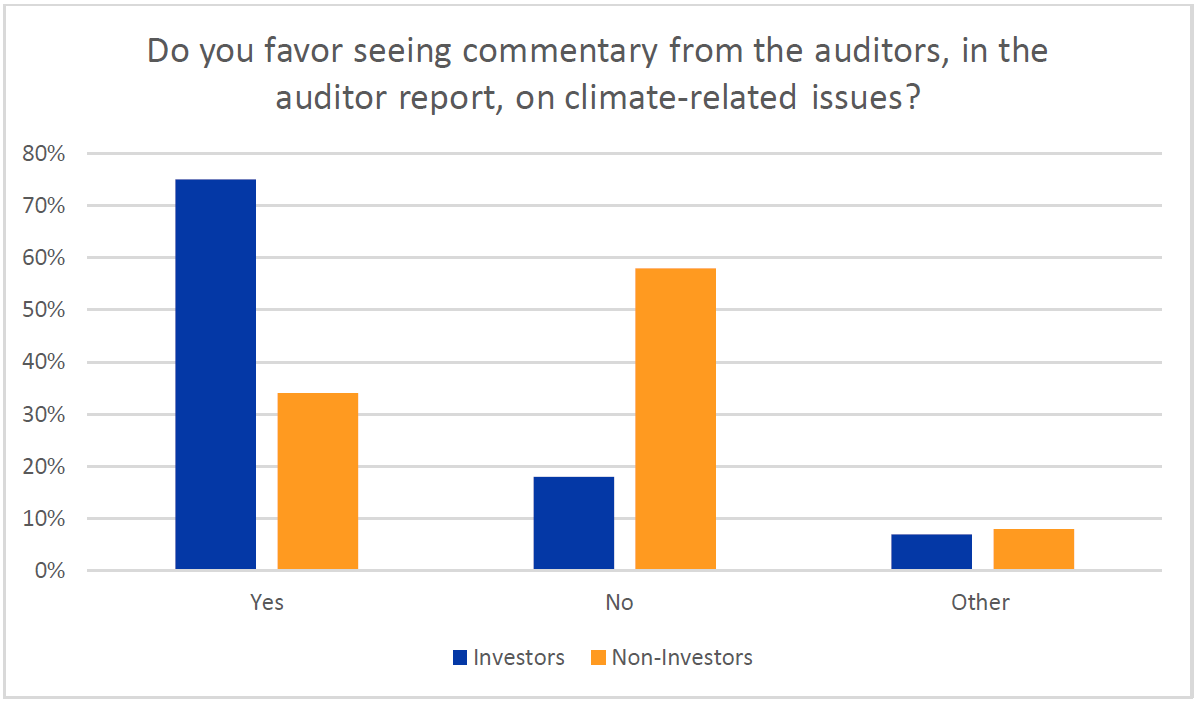

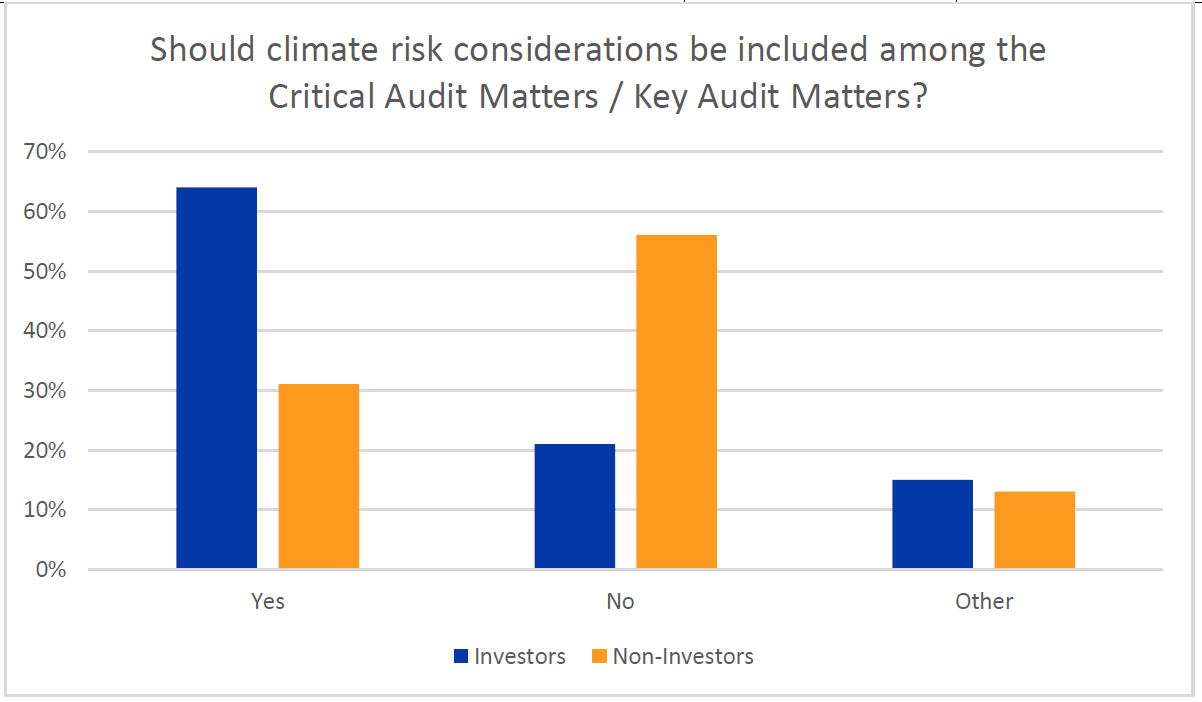

A substantial majority of investor respondents (75 percent) favored seeing commentary by auditors in the audit report on climate-related risks for significant emitters. A smaller majority (64 percent) of investor respondents supported climate-related risks being included by auditors in Critical Audit Matters / Key Audit Matters (CAMs). A majority of investor respondents (52 percent) would favor supporting a related shareholder proposal on this issue. Voting against the re-election of audit committee members and voting against the re- appointment of auditors got somewhat lower support (42 percent and 35 percent respectively). In comments, several respondents – including both those who favored and opposed the inclusion of climate risks – raised the question of whether auditors currently have the expertise to accurately gauge these risks. Others wrote that this issue is currently not a market norm but may develop quickly due to regulatory requirements that are being finalized in the U.S. and EU and as the International Sustainability Standards Board (ISSB) develops its sustainability standards. Non-investor respondents tended to not support seeing auditors comment on climate-related risk.

Financed Emissions

During the 2022 proxy season, a number of shareholder proposals were filed that asked companies to restrict their financing or underwriting for new oil and gas development in line with the assumptions in the International Energy Administration’s Net Zero 2050 Scenario, which prompted us to ask a question about expectations on climate-related disclosure and performance of financial institutions. Around half of investor respondents said that in 2023 large companies in the banking and insurance sectors should fully disclose their financed emissions (54 percent), have clear long-term and intermediary financed emissions reduction targets for high emitting sectors (51 percent), have a net-zero by 2050 ambition including financed portfolio emissions (49 percent), or should publicly commit to disclose financed emissions at some point in the future by joining a collaborative group such as the Partnership for Carbon Accounting Financials (PCAF) and/or the Glasgow Financial Alliance for Net Zero (GFANZ) (45 percent). Around 30 percent of investor respondents voiced support for these companies committing to cease financing for new fossil fuel projects. The most popular response among non-investors was that companies in the banking and insurance sectors should not be expected to comply with shareholder requests on financed emissions (40 percent). Non-investor respondents also expressed lower support than investors for companies in these sectors declaring targets to reduce financed emissions.

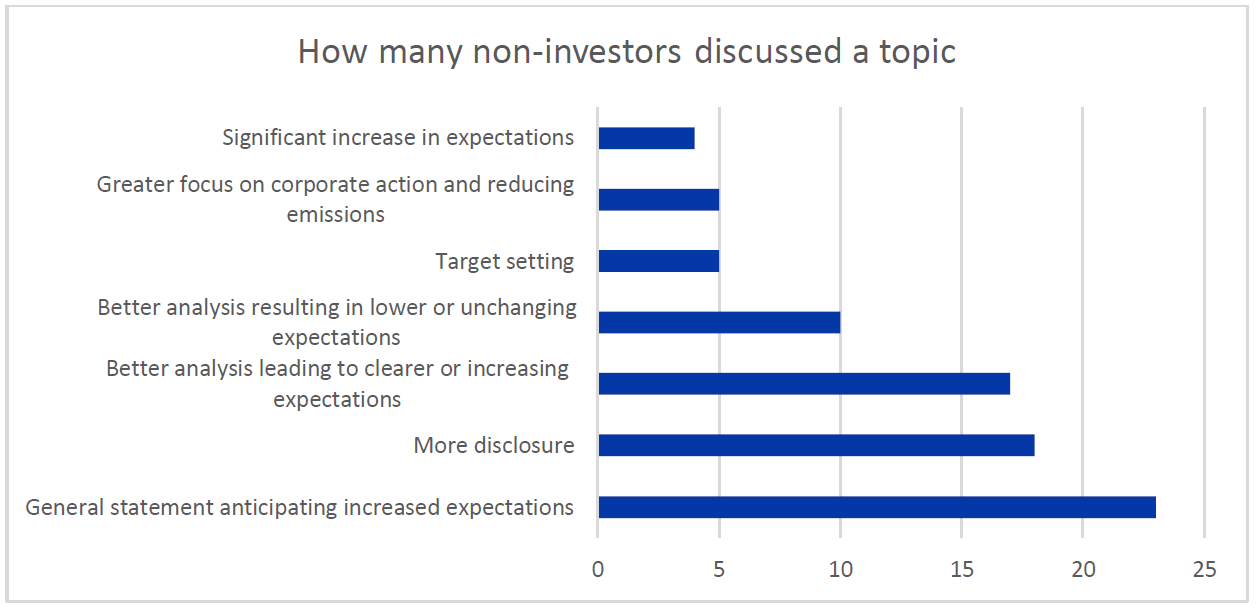

Climate Expectations

Most respondents, both investors and non-investors, expect investors’ minimum expectations on thresholds for climate-related disclosure and performance to increase over time. Comments about what these expectations looked like varied, but the four common buckets among investor respondents were:

- Heightened focus on whether companies’ targets are aligned with net-zero, and these targets being verified by organizations such as the Science Based Targets initiative (SBTi).

- Disclosure of more climate-related information driven by regulatory changes and industry practices and more effective utilization of climate-related disclosure to allow for greater comparability between companies and to incorporate more specific information, such as industry-specific considerations. Others expressed that their expectations about best practices will not change, but rather disclosures that are considered to be optional or nice-to-have now will become expectations in the future.

- Greater disclosure of Scope 3 emissions and this information being more integrated into investors’ strategies.

- More interest in companies investing in low-carbon products and a shift toward expecting corporate climate strategies that result in reductions in greenhouse gas emissions.

Multi-class Structures and Problematic Provisions – U.S.

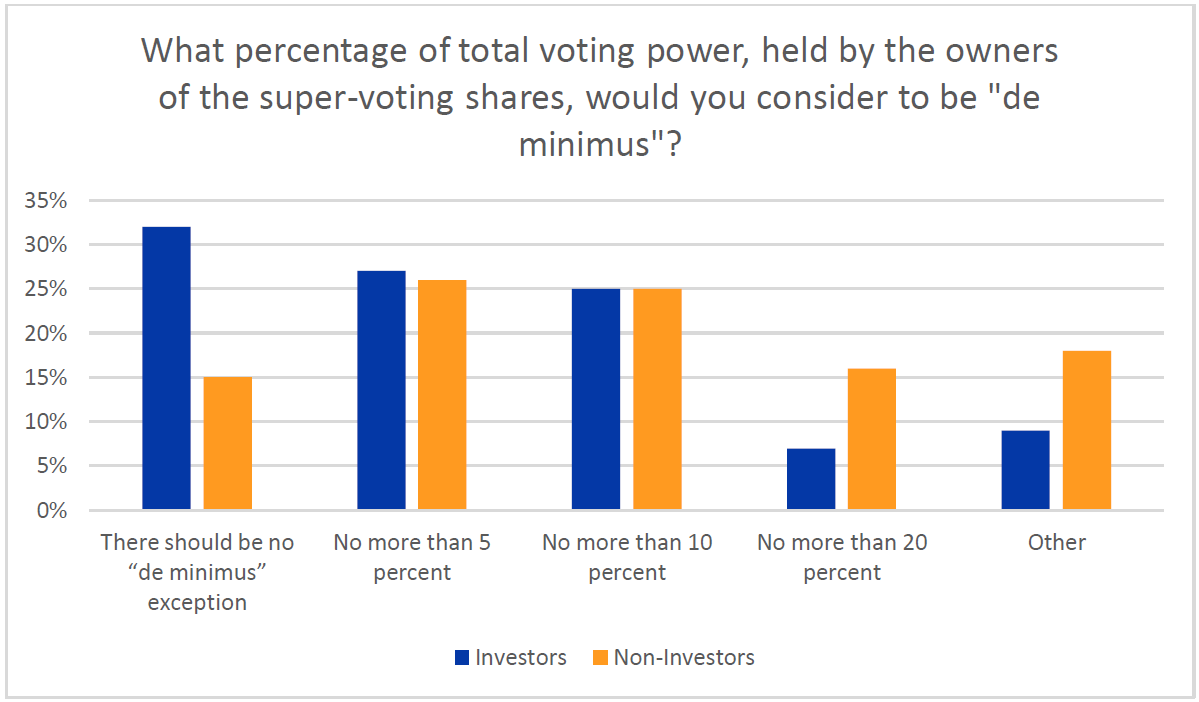

Already announced in 2021, effective as of Feb. 1, 2023, ISS plans to start recommending votes against certain directors at U.S. companies that maintain a multi-class capital structure with unequal voting rights, including companies that were previously exempted from adverse vote recommendations. In 2022, we said that we planned to apply exceptions in cases where the capital structure is not deemed to meaningfully disenfranchise public shareholders. When asked what the appropriate threshold for exemption should be, a strong majority of investor respondents agreed that there should be an exception. They were split on exactly what that threshold should be, but “no more than five percent” was the most popular threshold chosen by investor and non-investor respondents. Almost a third of investors responded that there should be no exemptions.

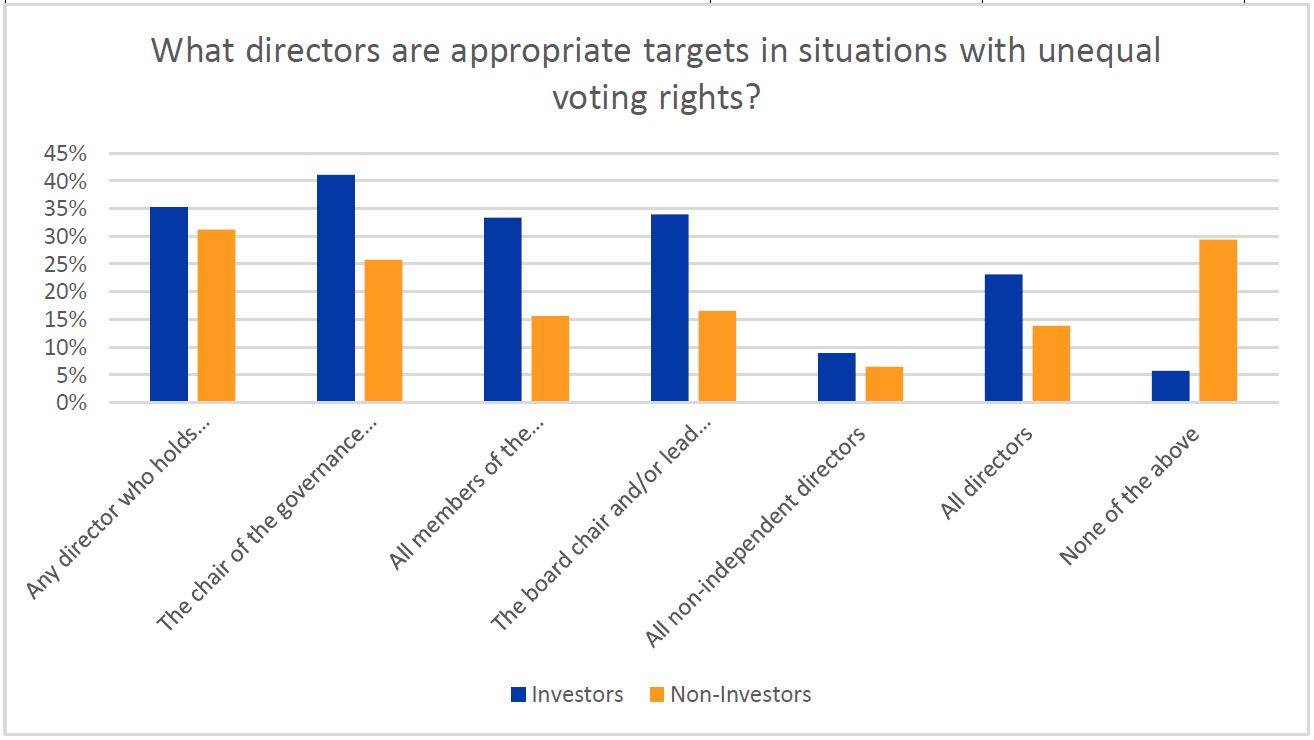

When asked what the appropriate target for an adverse vote recommendation, respondents favored any director who holds super-majority shares and the chair of the governance committee. Twenty-nine percent of non-investor respondents stated that there should not be votes against directors in this situation.

In cases where shareholder do not have the ability to vote against the director who holds super-majority shares, a majority of investor respondents said that shareholders should vote against whatever director was on ballot to protest against the multi-class structure.

When asked to define the most appropriate time for a sunset to begin phasing out problematic governance structures such as a classified board, a plurality of investor respondents chose “between 3 and 7 years.”

When asked whether smaller companies should be exempted from negative vote recommendations for maintaining a classified board or supermajority voting requirement, a strong majority of investor respondents said that should not. Nearly two-thirds of non-investor respondents, on the other hand, replied that smaller companies should be exempted from either one or both of those provisions.

Both investors and non-investors supported having a supermajority vote requirement of two-thirds of shares outstanding to amend governing documents.

Diversity, Equity, and Inclusion, U.S.

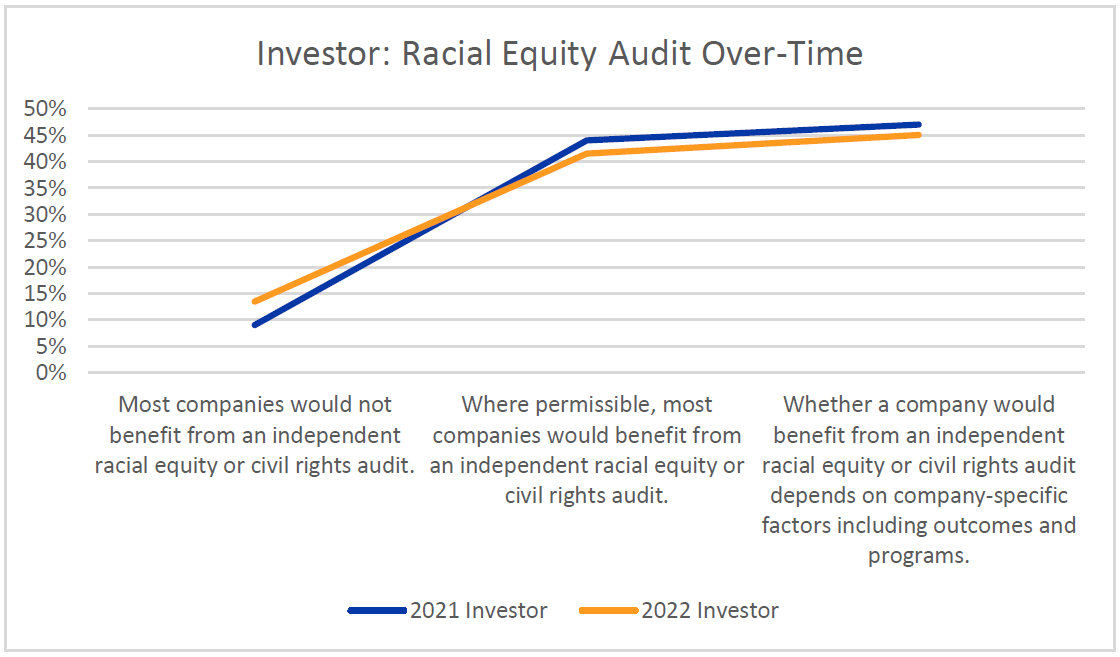

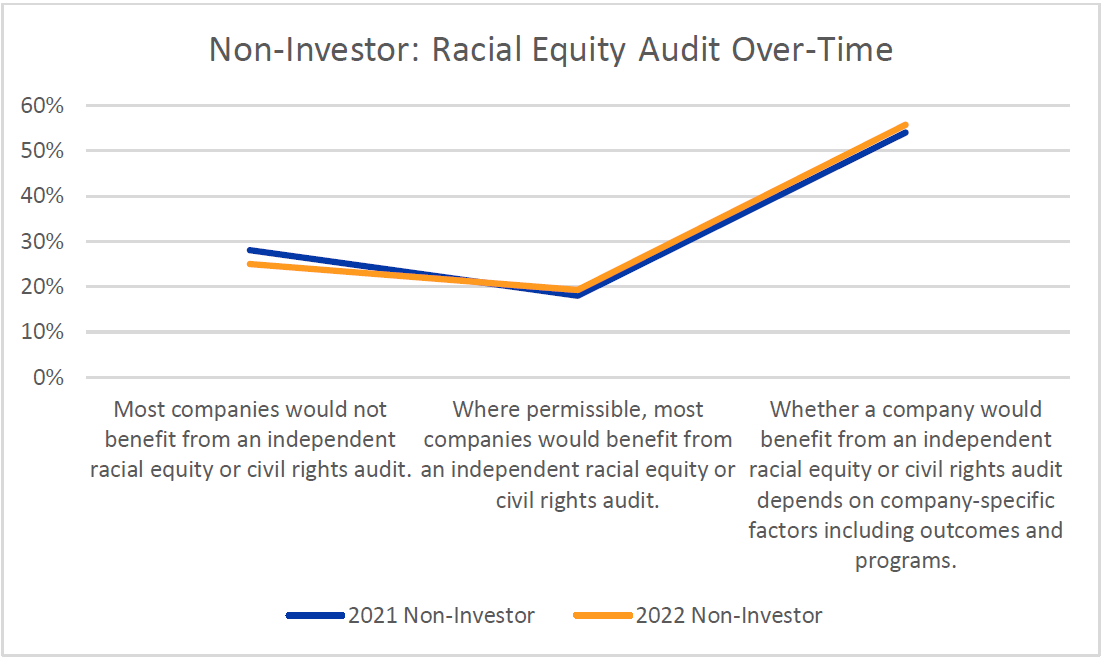

The 2021 and 2022 proxy seasons saw a new kind of shareholder proposal that asked for companies to commission an independent audit to assess potential racial bias throughout their business practices, both internal, directed at the company’s board and workforce, and external, directed at customers, communities, and other stakeholders. Discussions with clients and proponents and the survey results lead ISS to conclude that investors are roughly evenly split into two camps on this issue. Approximately 42 percent of investor respondents to the survey said most companies would benefit from an independent racial equity or civil rights audit, while a slightly larger 45 percent responded that whether a company would benefit from an independent racial equity or civil rights audit depends on company-specific factors including outcomes and programs. A majority of non-investor respondents indicated that they believe company specific criteria are the best determinations of which companies would benefit from a racial equity audit.

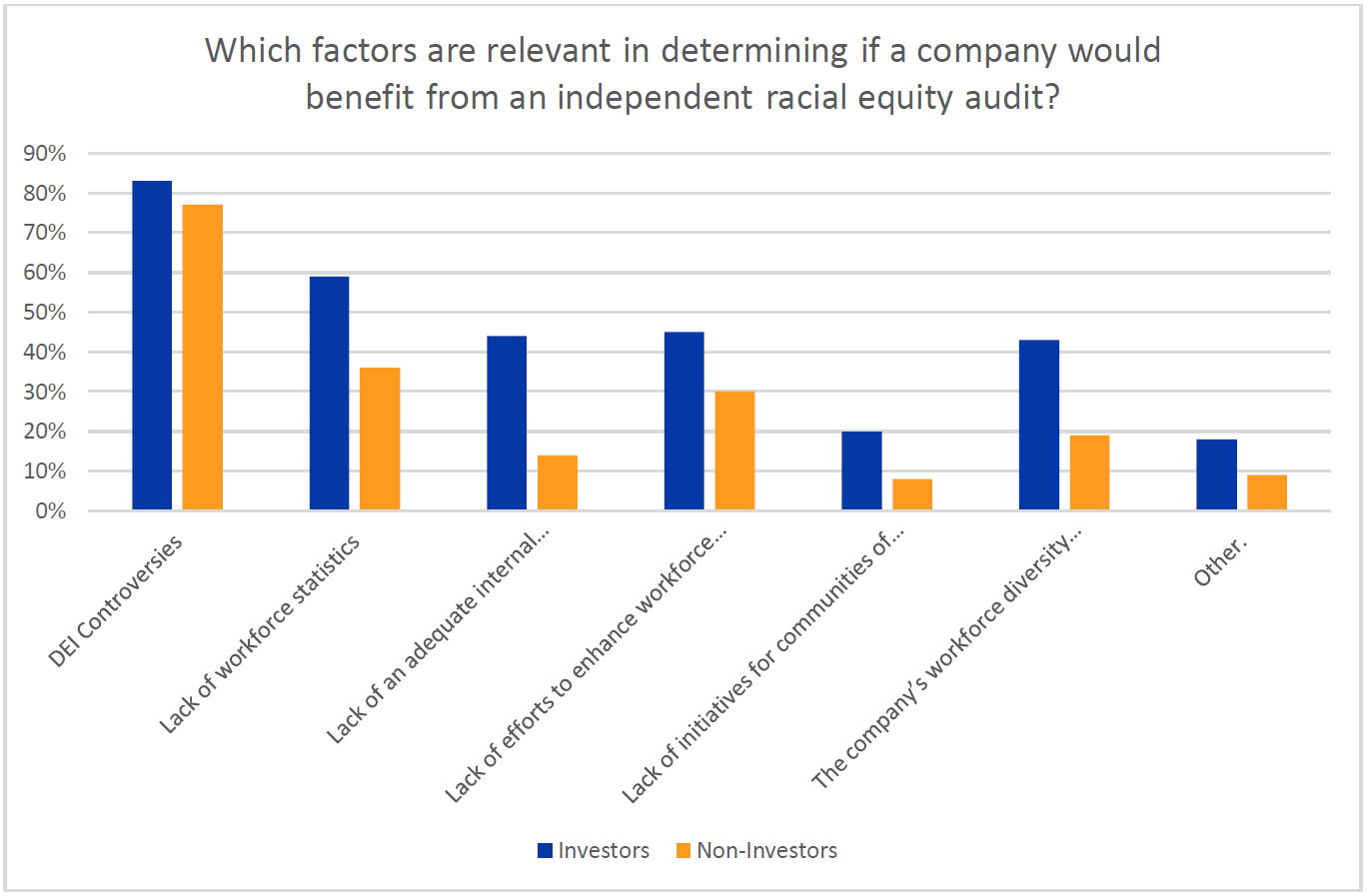

When asked what factors were relevant to determine whether a company would benefit from an independent racial equity or civil rights audit, “significant diversity-related controversies” were the most popular choice – being selected by a majority of investor and non-investor respondents. This was followed by whether the company disclosed workforce diversity representation statistics, such as EEO-1 type data, and has undertaken initiatives/efforts aimed at enhancing workforce diversity and inclusion, including training, projects, and pay disclosure. The least popular choice for investor respondents was whether the company offered products or services and/or made charitable donations with a specific focus on helping create opportunity for people and communities of color.

The question asked this year was the same as the one asked in the 2021 Benchmark Policy Survey to assess any changes in sentiment over time, especially given the strong vote support that many of these proposals received at annual meetings in 2022. The responses for investor and non-investor respondents changed only slightly from last year to this one.

Share Issuance Mandates at Cross-Market Companies Under ISS Coverage

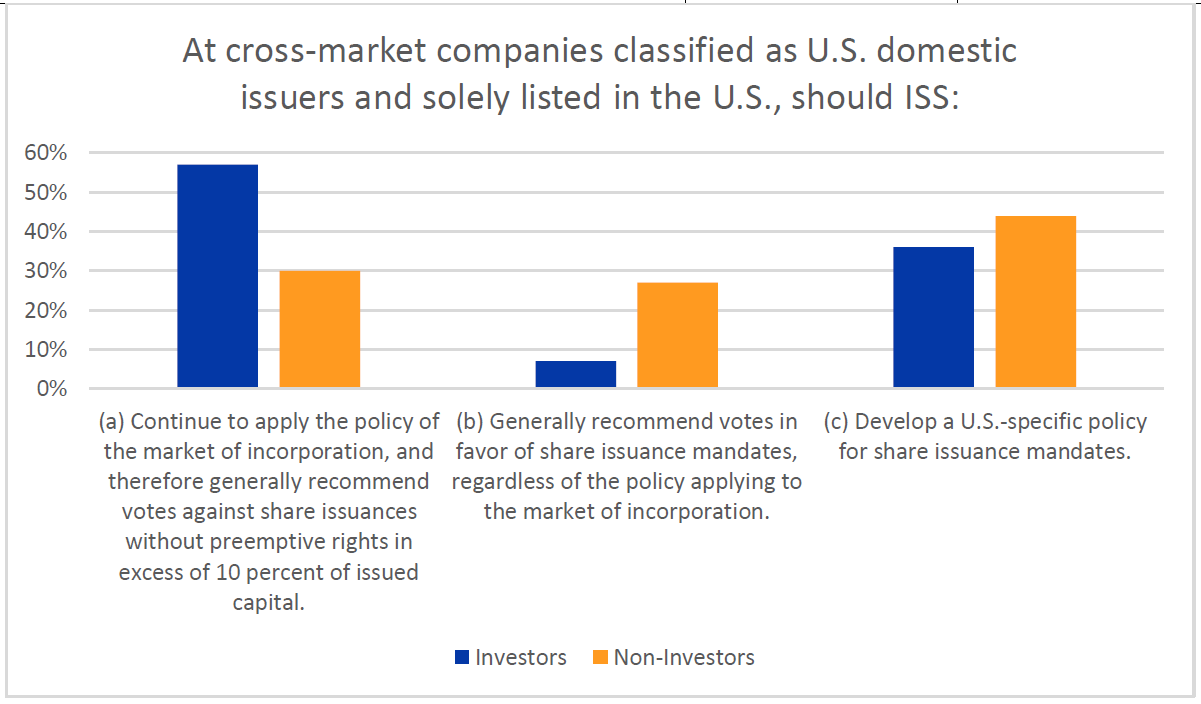

Investor respondents’ views of the preferred approach to share issuance mandates at cross-market companies listed in the U.S. varied depending on where the investors were based. Investor respondents were roughly divided between those based outside the U.S. and those based inside the U.S. While a majority of investor respondents based outside the U.S. favored continuing to apply the policy of the market of incorporation, a majority of investor respondents based in the U.S. favored either developing a U.S. policy for these proposals or simply generally voting in favor of them. Of the investors who favored the creation of a U.S. policy for these proposals, a majority favored applying a limit of 20 percent of issued share capital. However, more than a third of investor respondents said that the limit on such issuances should depend on the company’s financial condition and stage of development. A majority of investor respondents prefer to see companies seek approval for share issuance mandates on an annual basis rather than every five years as is allowed in some markets.

Responses from non-investor respondents favored the creation of a U.S. policy to cover share issuance mandates. They were roughly evenly divided regarding what level of dilution should be considered acceptable among “20 percent,” “It should depend on the company’s financial condition and stage of development,” and “other.”

Audit Related Matters – UK & Ireland

When asked whether ISS should note the frequency of audit committee meetings held each year and consider negative vote recommendations where the number of meetings appeared to be insufficient, both investor and non- investor respondents (74 percent and 61 percent, respectively) strongly supported doing that.

Executive Pay Increases – UK & Ireland

In the context of rising inflation and cost of living challenges, ISS asked whether the explanation in a company’s compensation report of regular salary increases to executives being in line with the general workforce was still considered appropriate. Although a salary increase to executives may be similar to that granted to the general workforce in percentage terms, the actual increase may be much larger, and executives usually also have greater opportunities for bonuses. Non-investor respondents strongly believed that each board should determine executive pay in the context of the company’s needs. Investor respondents were split between that answer and “executive salaries should generally be rising more slowly in percentage terms.”

Unequal Voting Rights/Multi-Class Share Structures – Continental Europe

Over 70 percent of investor respondents replied that ISS should revisit its policy toward companies with governance structures considered poor, such as unequal voting rights, and should consider issuing adverse voting recommendations where they still exist.

Virtual Meetings – Continental Europe

As virtual-only meetings become more prevalent, we asked whether respondents would consider such meetings a problematic diminution of shareholder rights. A little over a third of investor respondents said that they did consider it problematic. Still, the most popular answer was “No, as long as the company put in shareholder rights safeguards such as time limits and participation rights.” Non-Investor respondents were split between that response and “No.”

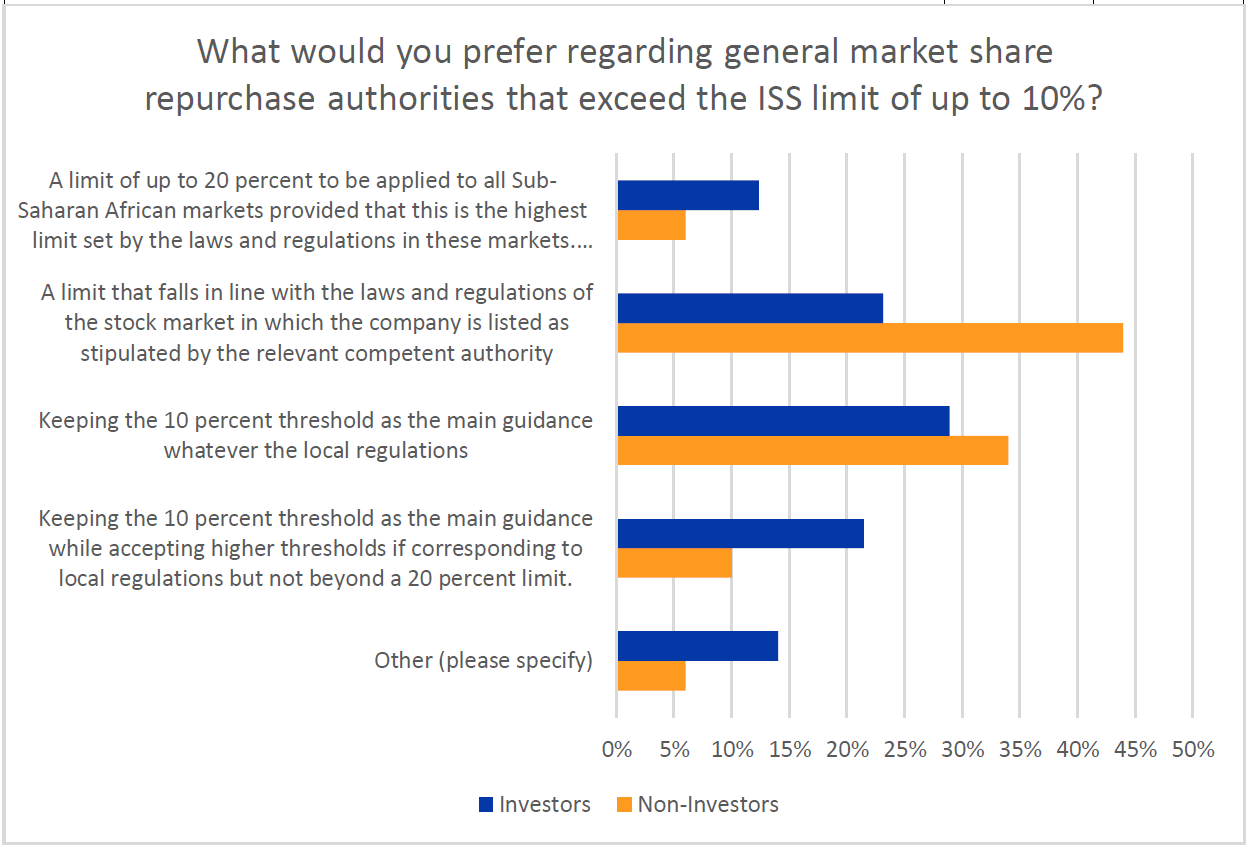

Share Repurchases – Sub-Saharan Africa

Given that sub-Saharan companies regularly seek approval on general market share repurchase authorities that exceed the ISS limit of up to 10 percent under ISS policy, we asked what market participants would favor among several options. Investor respondents, were split, but the response that garnered the most votes was “Keeping the 10 percent threshold as the main guidance whatever the local regulations.” Non-investor respondents, on the other hand, preferred “A limit that falls in line with the laws and regulations of the stock market in which the company is listed as stipulated by the relevant competent authority” most frequently.

Detailed survey questions and summary of responses

1. Climate Board Accountability

For companies considered to be significant greenhouse gas (GHG) emitters*, what actions or lack of actions may be considered to demonstrate such poor climate change risk management that rise to the level of “material governance failure,” which would call for an ISS recommendation against a director or directors?

*currently defined as those in the Climate 100+ Focus Group

**The targets do not overly rely on technologies that are not yet commercially available and are not overly reliant on offsets

| Response | Investors | Non-Investors |

| 1. Lack of climate change risk management disclosure and performance should not result in a vote against directors. | 16% | 40% |

| 2. Absence of adequate disclosure with regards to climate-related oversight, strategy, risks and targets according to a framework such as the one developed by the Task Force for Climate-related Financial Disclosure. | 79% | 57% |

| 3. Has not declared a “net-zero by 2050” ambition. | 47% | 17% |

| 4. Has not set realistic** medium-term targets (through 2035) for Scope 1 & 2 only (including direct emissions and those associated with purchased power). | 50% | 27% |

| 5. Has not set realistic** medium-term targets (through 2035) for Scope 1, 2 & 3 if Scope 3 is relevant (generally over 60% of company’s footprint) (including the scopes above and emissions associated with goods bought, sold, and financed). | 45% | 20% |

| 6. At least one “targets” answer. | 69% | 43% |

| 7. Is not showing or on track to show an absolute decline in GHG emissions for Scope 1 & 2 only (including direct emissions and those associated with purchased power). | 30% | 19% |

| 8. Is not showing or on track to show an absolute decline in GHG emissions for Scope 1, 2 & 3 if Scope 3 is relevant (generally over 60% of company’s footprint) (including the scopes above and emissions associated with goods bought, sold, and financed). | 36% | 11% |

| Total Number of Respondents | 188 | 161 |

In 2022 ISS began applying the new climate board accountability policy to the Climate 100+ focus group companies based in the U.S., Europe, UK/Ireland, and Russia. Would you support uniform application of this policy in every market or continued differentiation by market?

|

Response |

Investors |

Non-Investors |

|

| Continued differentiation by market | 22% | 60% | |

| Uniform policy application, where data and disclosures allow | 66% | 34% | |

| Other | 12% | 6% | |

| Total Number of Responses | 188 | 171 | |

2. Company Climate Transition Plans

With regards to the ISS global policy guidelines on Management Say on Climate proposals, what do you consider to be the top three priorities when determining if a company’s transition plan is adequate? (Choose up to three)

*Meaning that the targets do not rely on technologies that are not yet commercially available and are not overly reliant on offsets.

|

Response |

Investors |

Non- Investors |

| 1. The extent to which the company’s climate-related disclosures are in line with TCFD recommendations and meet other market standards. | 37% | 54% |

| 2. Whether the company has stated an ambition to be “net zero” for operational and supply chain emissions (Scope 1, 2 and 3) by 2050. | 16% | 11% |

| 3. Whether the company has comprehensive and realistic* medium-term targets for reducing operational emissions (Scopes 1 & 2) to net zero by 2050. | 22% | 23% |

| 4. Whether the company has set adequately comprehensive and realistic* medium-term targets for reducing operational and supply chain emissions (Scopes 1, 2 & 3) to net zero by 2050 for example, quantified actions accounting for reduction of at least 75 percent of its medium-term operational and supply chain GHG emissions (Scopes 1, 2, and 3 if relevant). | 42% | 12% |

| 5. Whether the company has set adequately comprehensive long-term targets for reducing operational emissions (Scopes 1 & 2) to net zero by 2050. | 11% | 14% |

| 6. Whether the company has set adequately comprehensive long-term targets for reducing operational and supply chain emissions (Scopes 1, 2 & 3) to net zero by 2050 for example, quantified actions accounting for reduction of at least 50 percent of its long-term operational and supply chain GHG emissions (Scopes 1, 2, and 3 if relevant). | 17% | 8% |

| 7. Whether the company has sought and received third-party approval that its targets are science-based, such as from the Science Based Targets initiative. | 32% | 18% |

| 8. Whether the company discloses a commitment to report on the implementation of its plan in subsequent years. | 22% | 35% |

| 9. Whether the company’s climate data and/or financial assumptions have received third-party assurance. | 10% | 16% |

| 10. Whether the company’s short- and medium-term capital expenditures align with long-term company strategy and the company has disclosed the technical and financial assumptions underpinning its strategic plans. | 41% | 11% |

| 11. Whether the company’s direct GHG emissions have increased in the past year. | 1% | 9% |

| 12. Whether the company’s direct and indirect GHG emissions have increased in the past year. | 5% | 4% |

| 13. No preferences. | 3% | 11% |

| 14. Other. | 13% | 9% |

| Total Responses | 192 | 167 |

3. Climate Risk As Critical Audit Matter

Some institutional investors have called on companies, especially high emitters, to ensure that their financial reports include material climate change risks and are prepared using assumptions consistent with the Paris Agreement on climate change. Although most global auditing standards require adequate considerations of climate risk, the “Flying Blind” report from Carbon Tracker concludes that most of the world’s largest GHG emitting companies are not meeting these standards. Do you favor seeing commentary from the auditors, in the auditor report, on climate-related issues (in the case of significant emitters)?

|

Response |

Investors |

Non-Investors |

| Yes | 75% | 34% |

| No | 18% | 58% |

| Other | 7% | 8% |

| Total Number of Responses | 192 | 172 |

In your view, should climate risk considerations be included among the Critical Audit Matters / Key Audit Matters?

|

Response |

Investors |

Non-Investors |

| Yes | 64% | 31% |

| No | 21% | 56% |

| Other | 15% | 13% |

| Total Number of Responses | 193 | 170 |

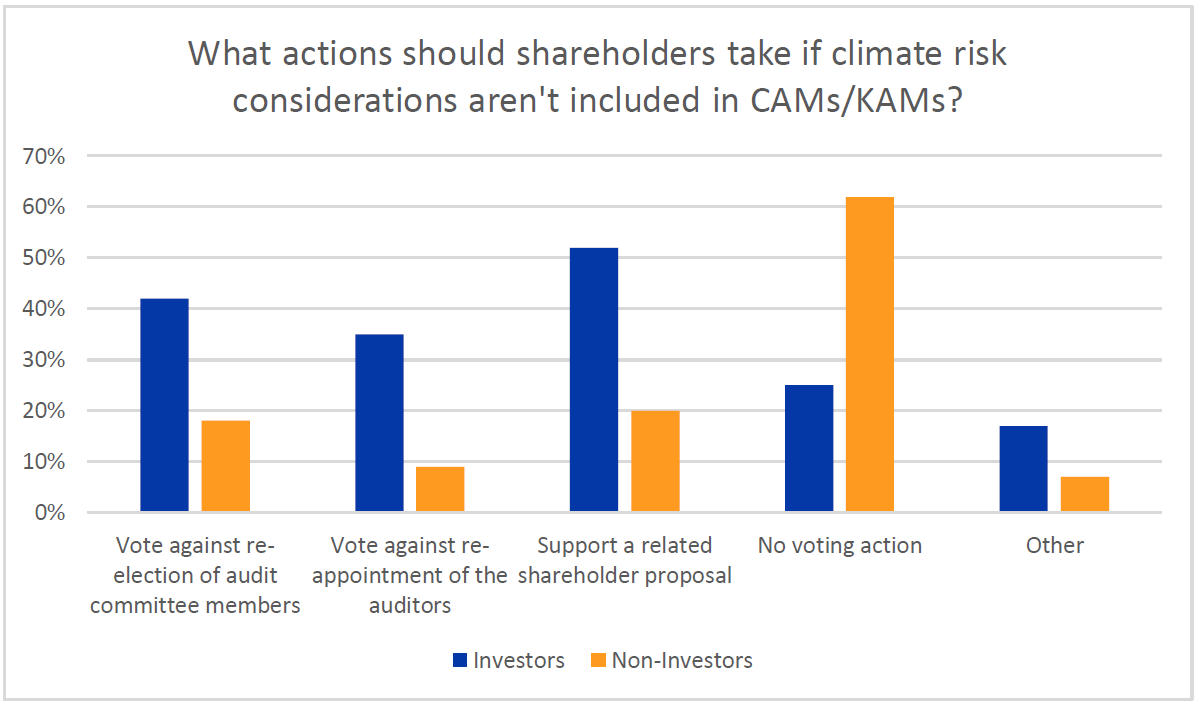

Which of the following actions would you consider appropriate for shareholders to take if climate risk considerations are not included among a company’s Critical Audit Matters/Key Audit Matters? (choose all that apply)

|

Response |

Investors |

Non-Investors |

| Vote against re-election of audit committee members | 42% | 18% |

| Vote against re-appointment of the auditors | 35% | 9% |

| Support a related shareholder proposal | 52% | 20% |

| No voting action | 25% | 62% |

| Other | 17% | 7% |

| Total Number of Responses | 193 | 168 |

4. Financed Emissions

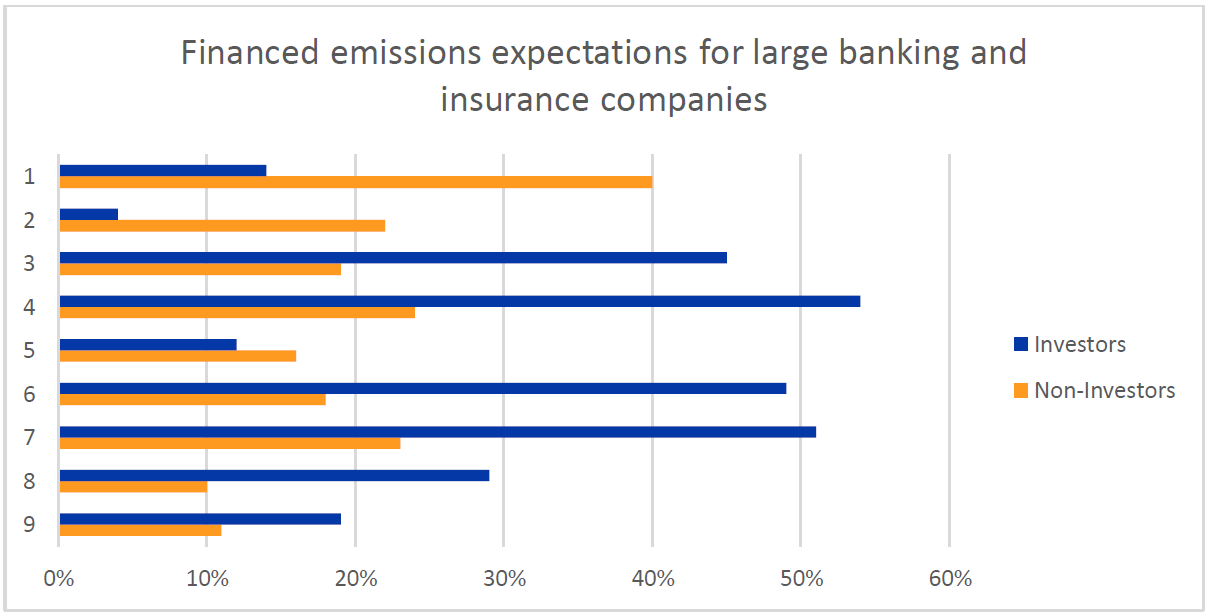

There were a number of shareholder proposals in 2022 that requested companies in the finance sector to adopt a policy to restrict their financing or underwriting for new fossil fuel projects. Thinking about 2023, what do you consider to be appropriate investor expectations for large companies in the banking and insurance sectors regarding the GHG emissions associated with their lending, investment, and underwriting portfolios (choose all that apply):

|

Response |

Investors |

Non-Investors |

| 1. Such companies should not be expected to comply with shareholder requests regarding financed emissions. | 14% | 40% |

| 2. Disclosure – such companies should only be expected to disclose their direct emissions (Scope 1 & 2), not their financed emissions (Scope 3, Category 15). | 4% | 22% |

| 3. Disclosure – such companies should publicly commit to disclose financed emissions at some point in the future by joining a collaborative group such as the Partnership for Carbon Accounting Financials (PCAF) and/or the Glasgow Financial Alliance for Net Zero (GFANZ), although they may not yet have disclosed the data or may not have disclosed it completely. | 45% | 19% |

| 4. Disclosure – Such companies should fully disclose financed emissions. | 54% | 24% |

| 5. Targets – Such companies should only be expected to have targets to reduce emissions from their own operations. | 12% | 16% |

| 6. Targets –Such companies should have a net-zero by 2050 ambition including financed portfolio emissions. | 49% | 18% |

| 7. Targets – Such companies should have clear long- term and intermediary financed emissions reduction targets for high emitting sectors. | 51% | 23% |

| 8. Companies should commit to cease financing or underwriting new fossil fuel projects. | 29% | 10% |

| 9. Other | 19% | 11% |

| Total Number of Respondents | 190 | 159 |

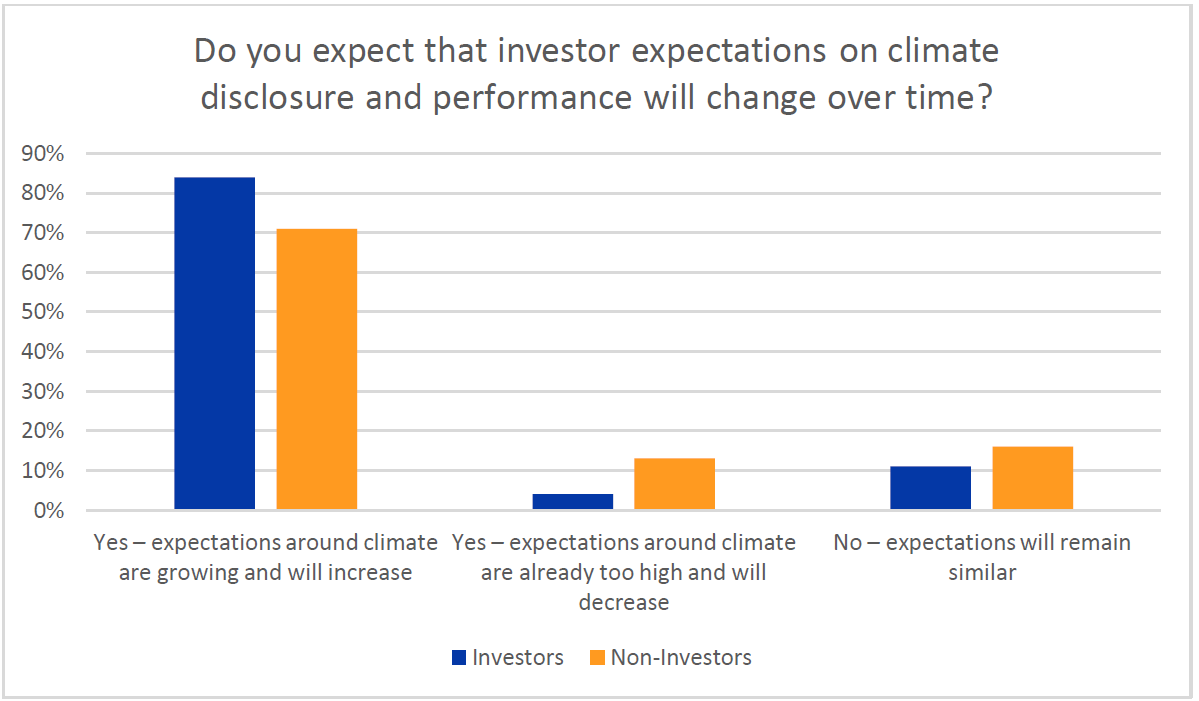

Do you expect that investors’ minimum expectations on thresholds for climate-related disclosure and performance will change over time?

|

Response |

Investors |

Non-Investors |

| Yes – expectations around climate are growing and will increase | 84% | 71% |

| Yes – expectations around climate are already too high and will decrease | 4% | 13% |

| No – expectations will remain similar | 11% | 16% |

| Total Number of Responses | 187 | 166 |

If you answered yes, and you are an investor, how do you expect your thresholds to change?

If you answered yes, and you are representing a company or other non-investor organization, how do you expect investors’ thresholds to change?

5. Potential Exceptions to Adverse Recommendations Under ISS Policy on Multi-Class Capital Structures – U.S.

Already announced in 2021, and beginning in 2023, ISS plans to start recommending votes against certain directors at U.S. companies that maintain a multi-class capital structure with unequal voting rights, including companies that were previously “grandfathered” (exempted from adverse vote recommendations) based on the date they went public. ISS plans to apply a “de minimis” exception in cases where the capital structure is not deemed to meaningfully disenfranchise public shareholders: for example, where most of the super-voting shares have already been converted into regular common shares.

What percentage of total voting power, held by the owners of the super-voting shares, would you consider to be “de minimus“?

|

Response |

Investors |

Non-Investors |

| There should be no “de minimus” exception | 32% | 15% |

| No more than 5 percent | 27% | 26% |

| No more than 10 percent | 25% | 25% |

| No more than 20 percent | 7% | 16% |

| Other | 9% | 18% |

| Total Number of Responses | 163 | 110 |

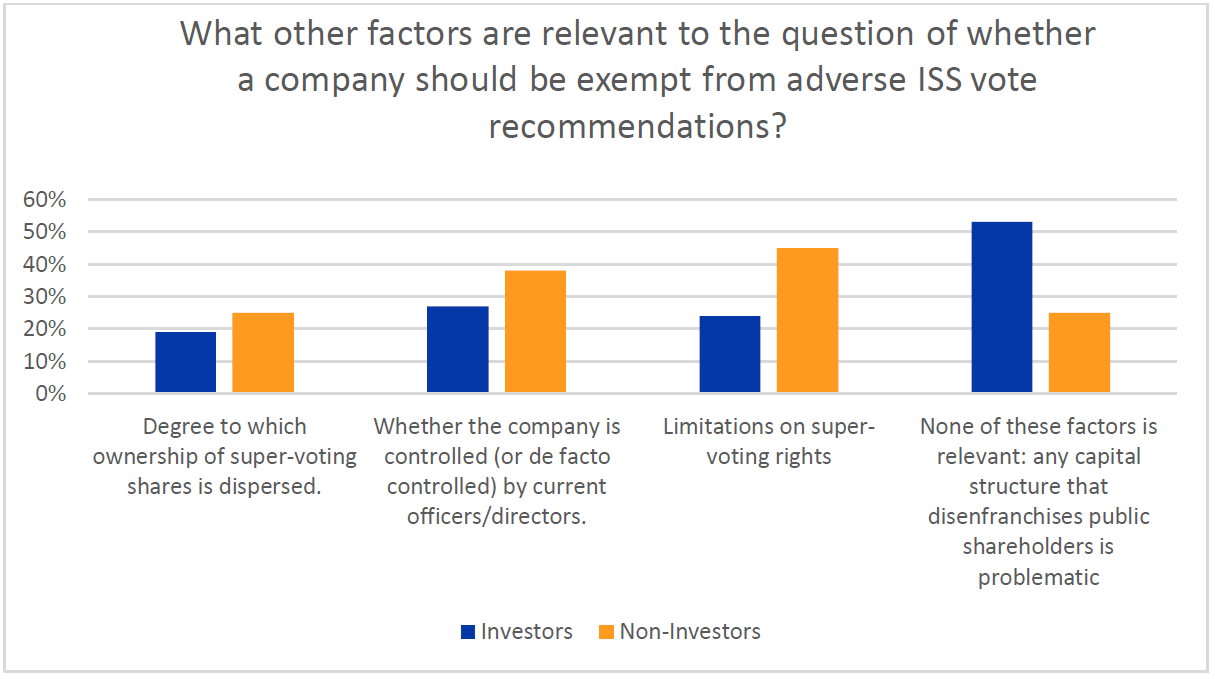

What other factors do you consider relevant to the question of whether a company should be exempt from adverse ISS vote recommendations under this policy?

|

Response |

Investors |

Non-Investors |

| Degree to which ownership of super-voting shares is dispersed. | 19% | 25% |

| Whether the company is controlled (or de facto controlled) by current officers/directors. | 27% | 38% |

| Limitations on super-voting rights (e.g., shares held by insiders have super-voting rights with respect to a merger, but not with respect to ordinary director elections, say-on-pay, etc.) | 24% | 45% |

| None of these factors is relevant: any capital structure that disenfranchises public shareholders is problematic | 53% | 25% |

| Other | 16% | 15% |

| Total Number of Responses | 161 | 106 |

Which directors do you consider appropriate targets for adverse vote recommendations due to a capital structure with unequal voting rights? (Please choose all that apply)

|

Response |

Investors |

Non-Investors |

| Any director who holds super-voting shares. | 35% | 31% |

| The chair of the governance committee. | 41% | 26% |

| All members of the governance committee. | 33% | 16% |

| The board chair and/or lead independent director. | 34% | 17% |

| All non-independent directors | 9% | 6% |

| All directors | 23% | 14% |

| None of the above | 6% | 29% |

| Total Number of Responses | 161 | 106 |

At some multi-class companies, public shareholders do not have the ability to vote on certain directors, such as the CEO, board chair, or members of the founding family. Where shareholders may only vote on a limited number of independent directors, do you consider they should vote against such directors if they wish to protest against the multi-class structure?

|

Response |

Investors |

Non-Investors |

| Yes | 57% | 46% |

| No | 21% | 42% |

| It depends | 22% | 12% |

| Total Number of Responses | 155 | 105 |

6. Problematic Governance Structures – U.S.

In 2020, ISS U.S. benchmark policy regarding newly-public companies with a problematic capital structure was codified to indicate that no sunset provision of greater than seven years from the date of the IPO would be considered reasonable. The inclusion of a reasonable sunset provision is considered a mitigating factor for ISS’ policy regarding other problematic governance structures (i.e., if a classified board structure and/or supermajority vote requirements to amend the governing documents) at newly-public companies. However, to date this policy has not defined a time period which would be considered reasonable.

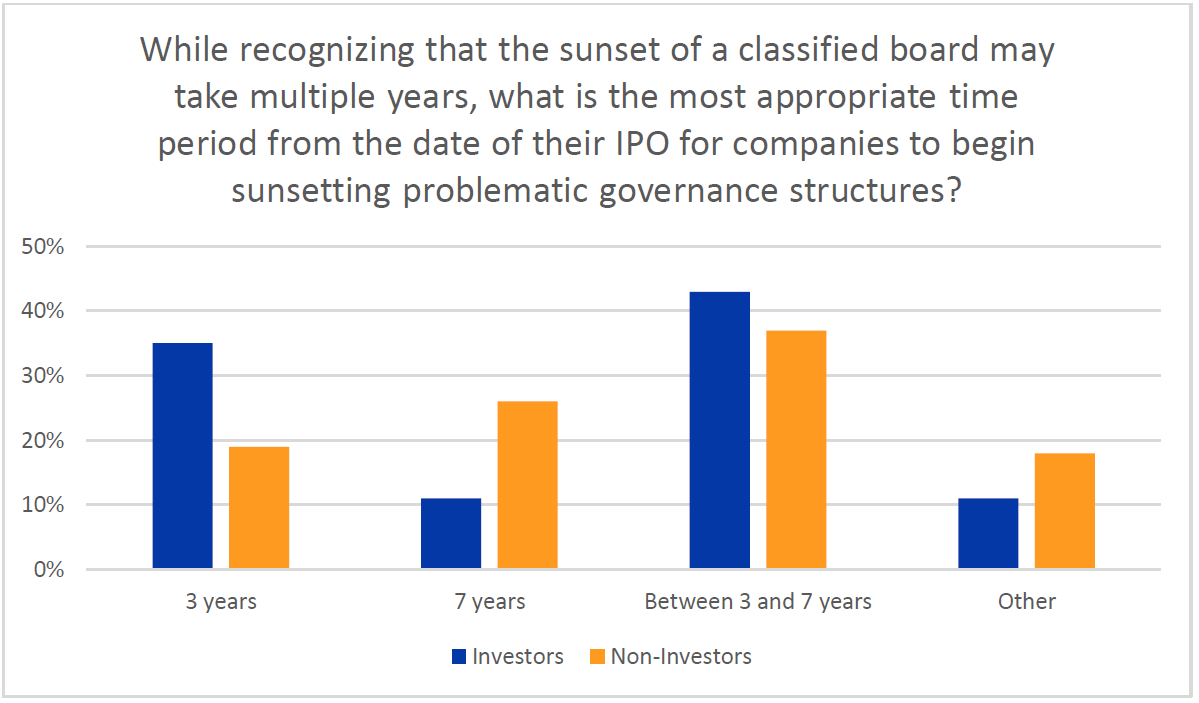

While recognizing that the sunset of a classified board may take multiple years, what is the most appropriate time period from the date of their IPO for companies to begin sunsetting problematic governance structures?

|

Response |

Investors |

Non-Investors |

| 3 years | 35% | 19% |

| 7 years | 11% | 26% |

| Between 3 and 7 years | 43% | 37% |

| Other | 11% | 18% |

| Total Number of Responses | 157 | 109 |

The results of the 2021 ISS policy survey indicated that a large majority of investor respondents were opposed to classified boards and supermajority vote requirements even at companies that have maintained these practices for many years. However, ISS recognizes that these practices may be seen by investors as more acceptable for smaller companies.

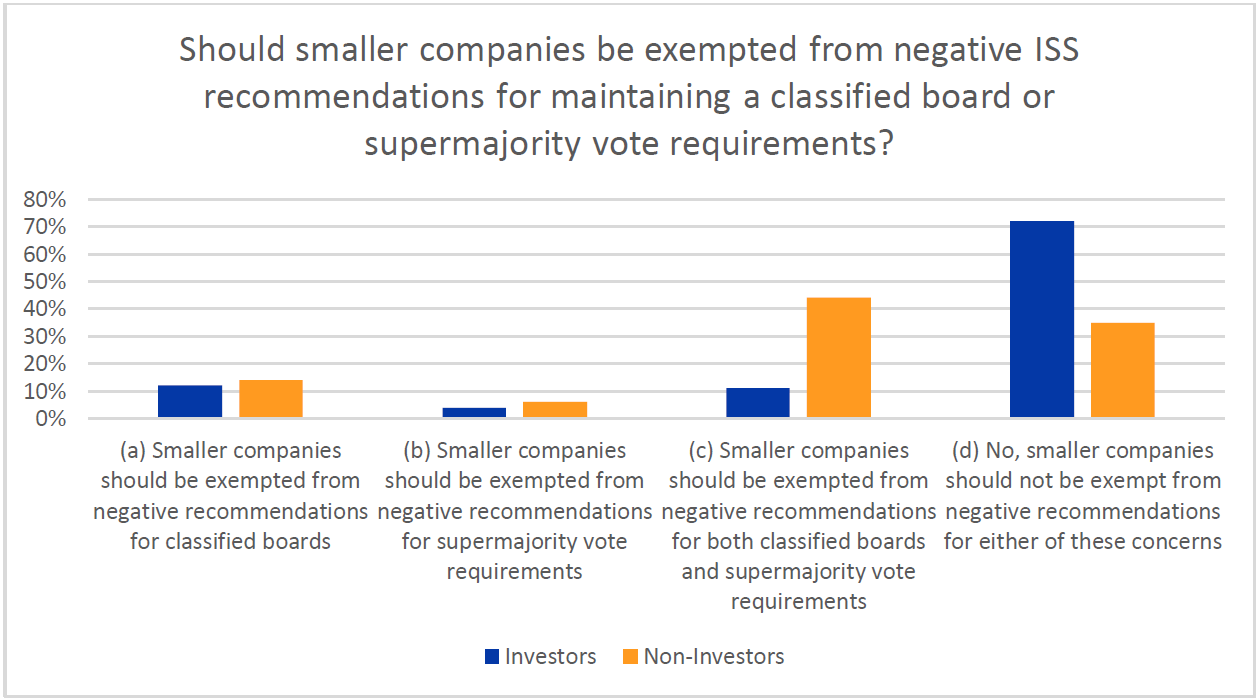

In your opinion, should smaller companies be exempted from negative ISS recommendations for maintaining a classified board or supermajority vote requirements?

|

Response |

Investors |

Non-Investors |

| (a) Smaller companies should be exempted from negative recommendations for classified boards | 12% | 14% |

| (b) Smaller companies should be exempted from negative recommendations for supermajority vote requirements | 4% | 6% |

| (c) Smaller companies should be exempted from negative recommendations for both classified boards and supermajority vote requirements | 11% | 44% |

| (d) No, smaller companies should not be exempt from negative recommendations for either of these concerns | 72% | 35% |

| Total Number of Responses | 155 | 107 |

If you answered (a), (b), or (c) to the question above, which companies would you consider to be sufficiently small to be exempt from adverse recommendations?

|

Response |

Investors |

Non-Investors |

| Companies outside the Russell 3000 | 64% | 35% |

| Companies outside the S&P 1500 | 27% | 35% |

| Companies outside the S&P 500 | 9% | 30% |

| Total Number of Responses | 45 | 66 |

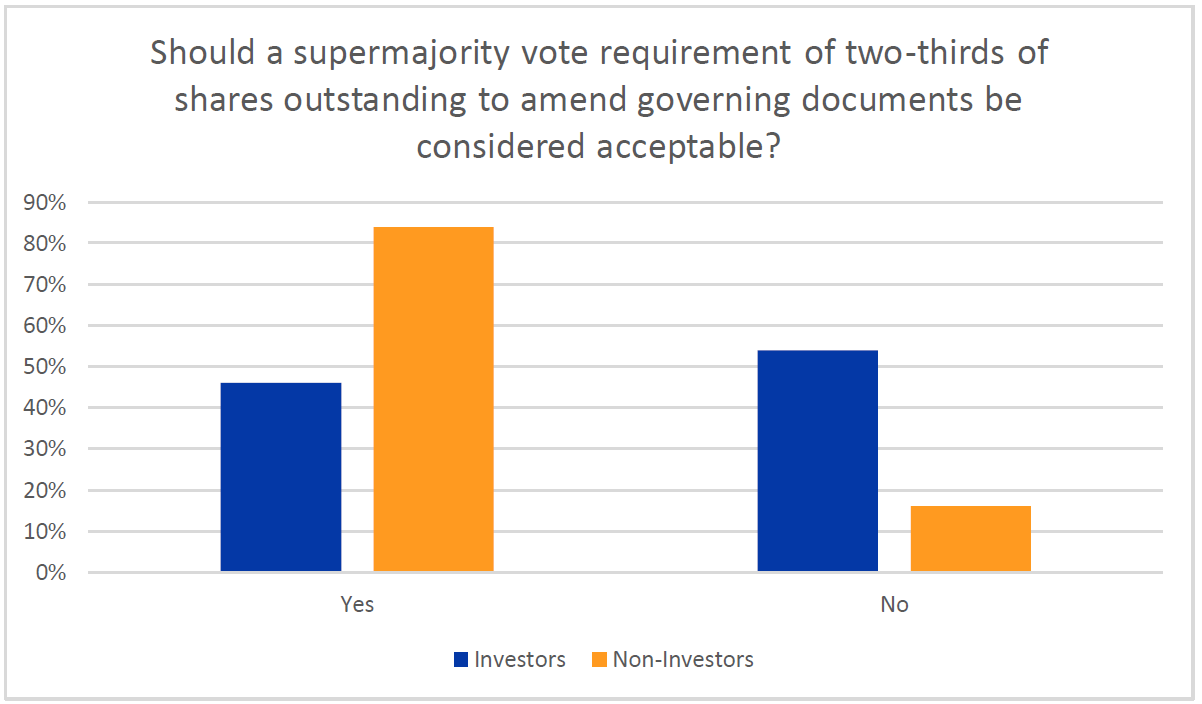

Currently, any vote requirement to amend the governing documents of greater than a majority of outstanding shares is considered a problematic governance practice. However, ISS recognizes that not all supermajority vote requirements are alike and that certain supermajority vote requirements, notably those requiring two- thirds of shares outstanding, are easier to achieve or eliminate as shareholder bases evolve than those requiring 75, 80, or 85 percent of shares outstanding.

In your opinion, should a supermajority vote requirement of two-thirds of shares outstanding to amend governing documents generally be considered acceptable?

|

Response |

Investors |

Non-Investors |

| Yes | 46% | 84% |

| No | 54% | 16% |

| Total Number of Responses | 155 | 112 |

7. Diversity, Equity & Inclusion (DEI) – U.S.

Since the racial justice protests sparked by the Black Lives Matter movement after the deaths of George Floyd and others in 2020, many shareholders have increased their engagement with companies on diversity and racial equity issues, seeking better disclosure on fair representation in the workforce and more information about corporate programs for employees of color.

In 2021, ISS undertook a careful review of its policy regarding racial equity audits and announced a new U.S. benchmark policy for 2022 on assessing proposals calling for racial equity and/or civil rights audits. The policy states that ISS will undertake a case-by-case analysis, looking at a number of relevant factors relating to the company’s disclosure and performance in the area of racial equity and/or civil rights.

In 2022, the number of and support for this type of proposal grew as compared to 2021. ISS recognizes that questions of racial and ethnic identification and diversity vary considerably globally, with different legal and cultural sensitivities. However, for companies operating in jurisdictions where racial equity or civil rights audits are permissible and may be relevant, and in cases where shareholder resolutions may be put forward to request such audits or similar information, we seek feedback on the following questions:

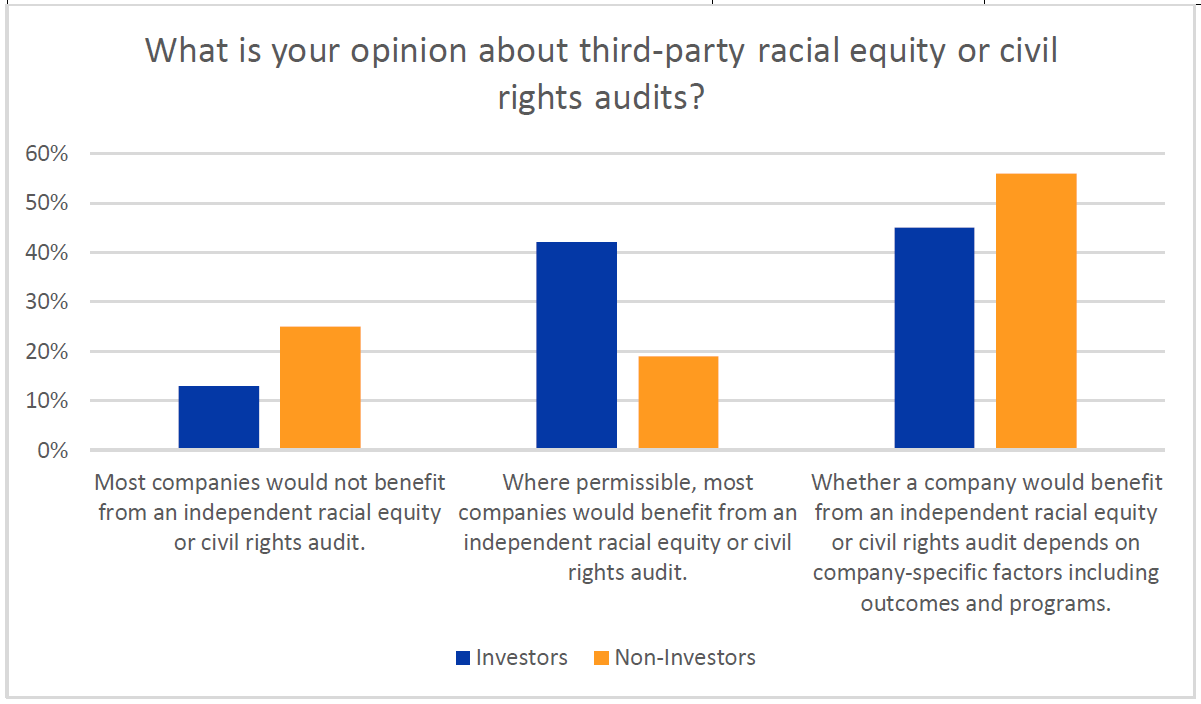

What is your opinion about third-party racial equity or civil rights audits?

|

Response |

Investors |

Non-Investors |

| Most companies would not benefit from an independent racial equity or civil rights audit. | 13% | 25% |

| Where permissible, most companies would benefit from an independent racial equity or civil rights audit. | 42% | 19% |

| Whether a company would benefit from an independent racial equity or civil rights audit depends on company-specific factors including outcomes and programs. | 45% | 56% |

| Total Number of Responses | 171 | 140 |

If you selected the second or third options above, which of the following company-specific factors do you consider relevant in indicating whether a company would benefit from an independent racial equity or civil rights audit (where permitted to do so)? (Please select all that apply)

|

Response |

Investors |

Non-Investors |

| The company is involved in significant diversity-related controversies. | 83% | 77% |

| The company does not provide detailed workforce diversity statistics, such as EEO-1 type data. | 59% | 36% |

| The company does not disclose an adequate internal framework/process for addressing implicit or systemic bias throughout the organization. | 44% | 14% |

| The company has not undertaken initiatives/efforts aimed at enhancing workforce diversity and inclusion, including training, projects, pay disclosure. | 45% | 30% |

| The company has not undertaken initiatives/efforts aimed at offering products/services and/or making charitable donations with a specific focus on helping create opportunity for people and communities of color. | 20% | 8% |

| The company’s workforce diversity statistics disclosure shows a lack of minority representation or increases in minority representation. | 43% | 19% |

| Other. | 18% | 9% |

| Total Number of Responses | 96 | 105 |

8. Share Issuance Mandates at Cross-Market Companies Under ISS Coverage

Companies domiciled in the U.S. generally do not need to seek shareholder approval for share issuances up to the level of authorized capital specified in the charter, unless required to do so by stock exchange listing rules. Both NYSE and Nasdaq require shareholder approval for issuances in excess of 20 percent of shares outstanding, but this limit applies to acquisitions and private placements and not to public offerings for cash. However, companies incorporated in certain other markets, even those considered U.S. domestic issuers by the SEC, may be required by the laws of the country of incorporation to seek approval for all share issuances. These cross-market companies typically seek approval for a mandate to cover issuances during the coming year (or a multi-year period).

There is currently no specific U.S. benchmark or Foreign Private Issuer (FPI) policy on share issuance mandates, and when they arise as a proposal to be voted on, they are covered under the policy of the market of incorporation. Those policies are generally based on local codes of best practice, which are not otherwise applicable to companies without a local stock market listing. ISS policies for markets such as the UK, Ireland and the Netherlands seek to limit dilution to existing shareholders from issuances without preemptive rights. However, preemptive rights have not been a feature of U.S. capital markets in the modern era. Cross-market companies often argue that they should not be subject to restrictions that are not applied to their U.S.- domiciled peers, when most of their shareholders are based in the U.S.; and argue specifically that having to offer pre-emptive rights, to a shareholder base unfamiliar with such rights, could delay or prevent an acquisition or financing transaction. At the same time, shareholders may reasonably expect to see safeguards against repeated dilutive share issuances.

At cross-market companies classified as U.S. domestic issuers and solely listed in the U.S., should ISS:

|

Response |

Investors |

Non-Investors |

| (a) Continue to apply the policy of the market of incorporation, and therefore generally recommend votes against share issuances without preemptive rights in excess of 10 percent of issued capital. | 57% | 30% |

| (b) Generally recommend votes in favor of share issuance mandates, regardless of the policy applying to the market of incorporation. | 7% | 27% |

| (c) Develop a U.S.-specific policy for share issuance mandates. | 36% | 44% |

| Total Number of Responses | 143 | 94 |

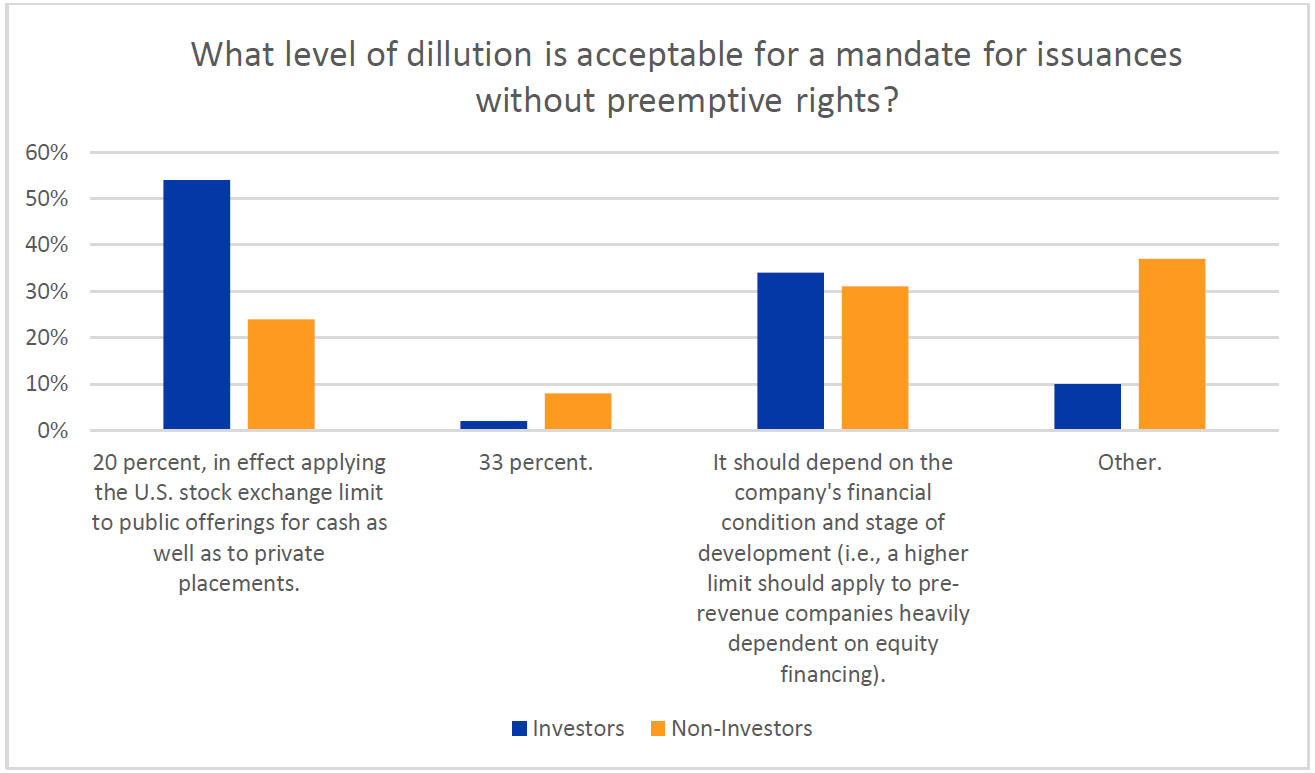

If you answered (c), what level of dilution do you consider acceptable for a mandate for issuances without preemptive rights (i.e., not tied to a specific transaction)?

|

Response |

Investors |

Non-Investors |

| 20 percent, in effect applying the U.S. stock exchange limit to public offerings for cash as well as to private placements. | 54% | 24% |

| 33 percent. | 2% | 8% |

| It should depend on the company’s financial condition and stage of development (i.e., a higher limit should apply to pre-revenue companies heavily dependent on equity financing). | 34% | 31% |

| Other. | 10% | 37% |

| Total Number of Responses | 58 | 51 |

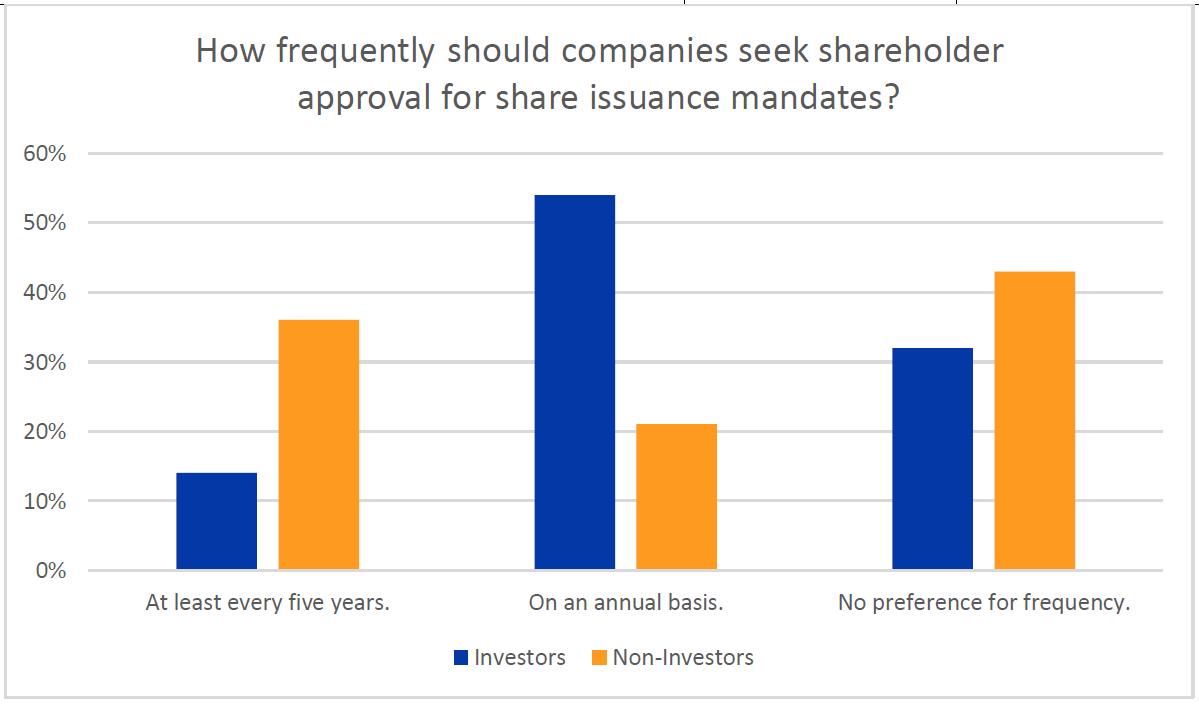

How frequently should such companies seek shareholder approval for share issuance mandates?

|

Response |

Investors |

Non-Investors |

| At least every five years. | 14% | 36% |

| On an annual basis. | 54% | 21% |

| No preference for frequency. | 32% | 43% |

| Total Number of Responses | 140 | 94 |

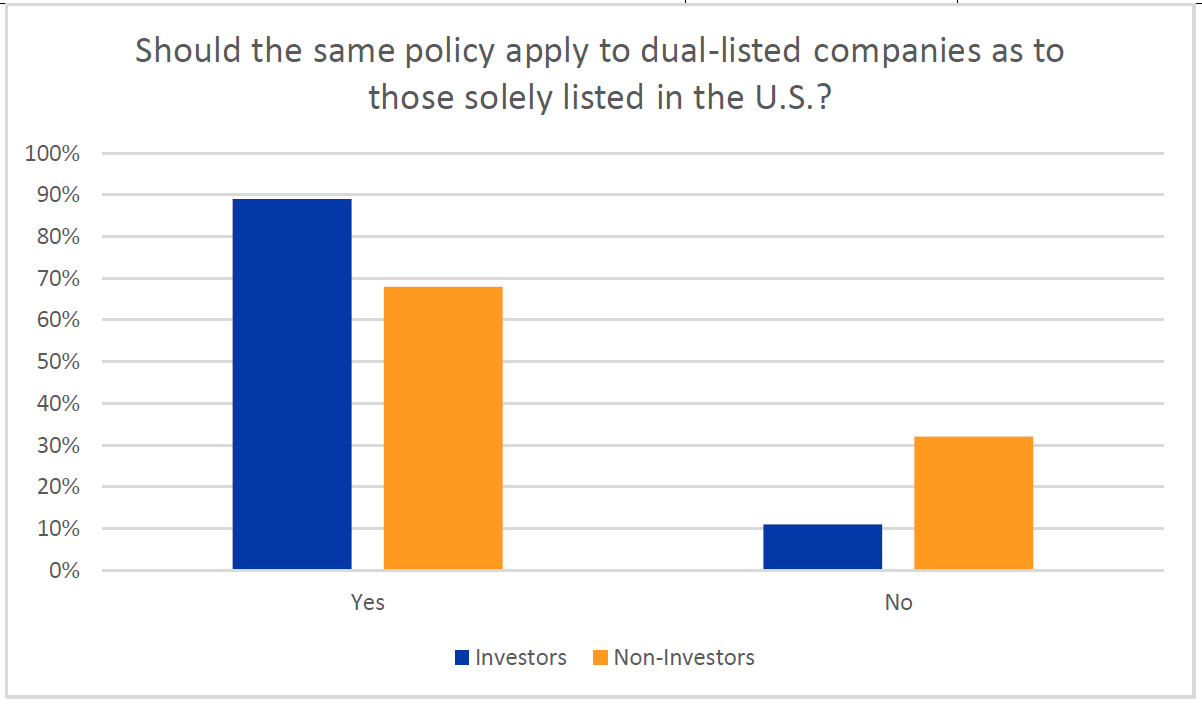

Should the same policy apply to dual-listed companies (those listed both on a U.S. exchange and an exchange in the market of incorporation) as to those solely listed in the U.S.?

|

Response |

Investors |

Non-Investors |

| Yes | 89% | 68% |

| No | 11% | 32% |

| Total Number of Responses | 142 | 92 |

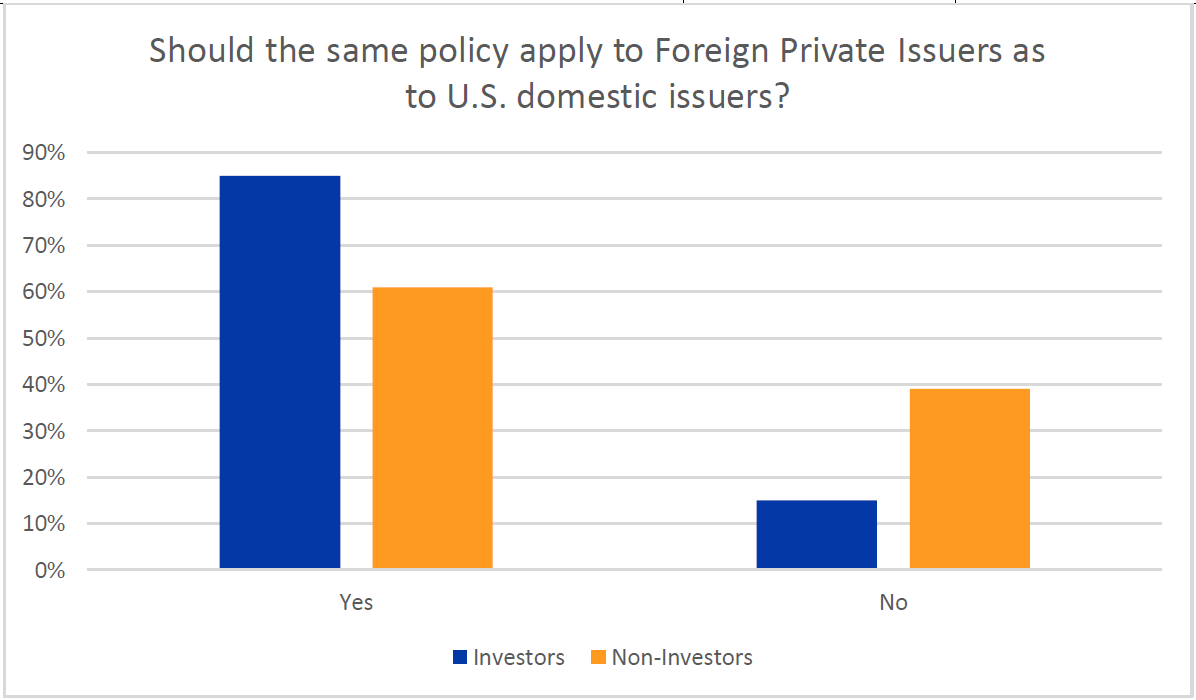

Should the same policy apply to Foreign Private Issuers as to U.S. domestic issuers?

|

Response |

Investors |

Non-Investors |

| Yes | 85% | 61% |

| No | 15% | 39% |

| Total Number of Responses | 140 | 92 |

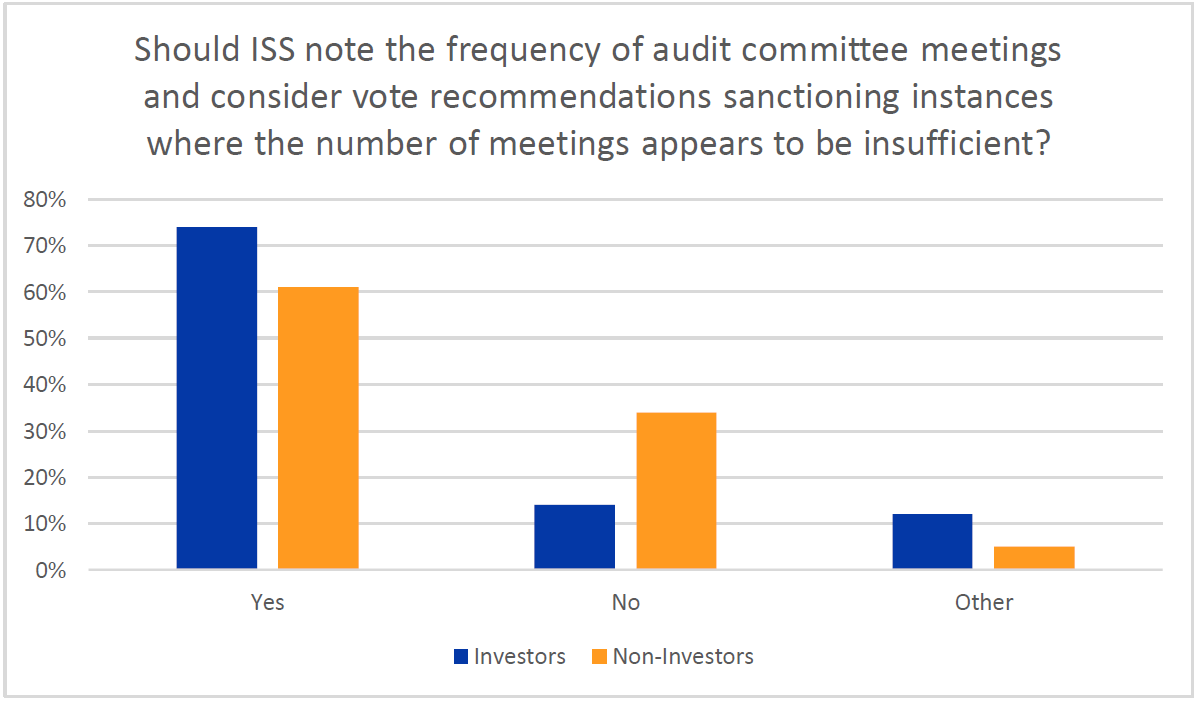

9. Audit Related Matters – UK & Ireland

Many markets typically promote a minimum number of meetings that audit committees are recommended to hold each year to ensure that the interests of shareholders are properly protected in relation to financial reporting and internal control. In the UK, the FRC’s Guidance on Audit Committees recommends that audit committees hold at least three audit committee meetings during each year but notes that “best practice requires that every board should consider in detail what audit committee arrangements are best suited for its particular circumstances” and that “audit committee arrangements need to be proportionate to the task, and will vary according to the size, complexity and risk profile of the company.” In light of a series of high-profile audit and internal control failings in companies in recent years, there are growing calls for increased scrutiny of companies’ internal controls and audit oversight.

Given the importance of the audit committee’s role, should ISS note the frequency of audit committee meetings held each year and consider vote recommendations sanctioning instances where the number of meetings appears to be insufficient?

|

Response |

Investors |

Non-Investors |

| Yes | 74% | 61% |

| No | 14% | 34% |

| Other | 12% | 5% |

| Total Number of Responses | 152 | 80 |

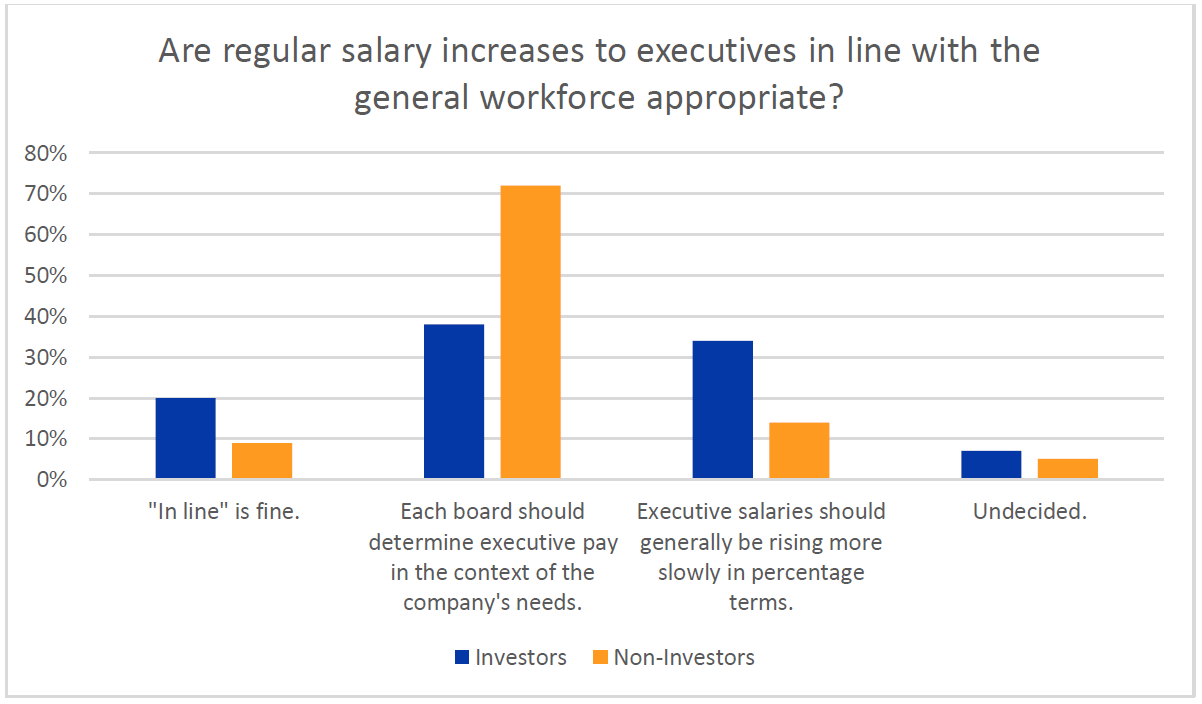

10. Executive Pay Increases – UK & Ireland

Executive pay (both practice and disclosure) is structured differently to that of a company’s average worker and typically comprises a large fixed component (salary, pension and benefits) along with a significant variable element (bonus and long-term incentives) which is normally expressed as a multiple of salary. For the average employee, the fixed element typically represents the largest single element. UK corporate governance principles expect companies to explain executive pay increases larger in percentage terms than those of the median employee. However, any salary increase made to executives – even those in line with increases awarded to the wider workforce – will likely result in a much larger increase in total pay opportunity because of the greater size of salary and because most remuneration elements for executive directors are expressed as a multiple of salary. For example, a 3 percent increase to an executive’s basic salary is likely to have a more profound impact on their total pay opportunity in monetary terms when compared to the same percentage salary increase awarded to the average worker. This will also lead to a ‘widening of the gap’ between average worker pay and total pay opportunity available to executives.

In the context of rising inflation and cost of living challenges, is the explanation of regular salary increases to executives being in line with the general workforce still considered appropriate or do you consider that they should generally be lower? Please select the option below that most closely reflects your view.

|

Response |

Investors |

Non-Investors |

| “In line” is fine. | 20% | 9% |

| Each board should determine executive pay in the context of the company’s needs. | 38% | 72% |

| Executive salaries should generally be rising more slowly in percentage terms. | 34% | 14% |

| Undecided. | 7% | 5% |

| Total Number of Responses | 154 | 87 |

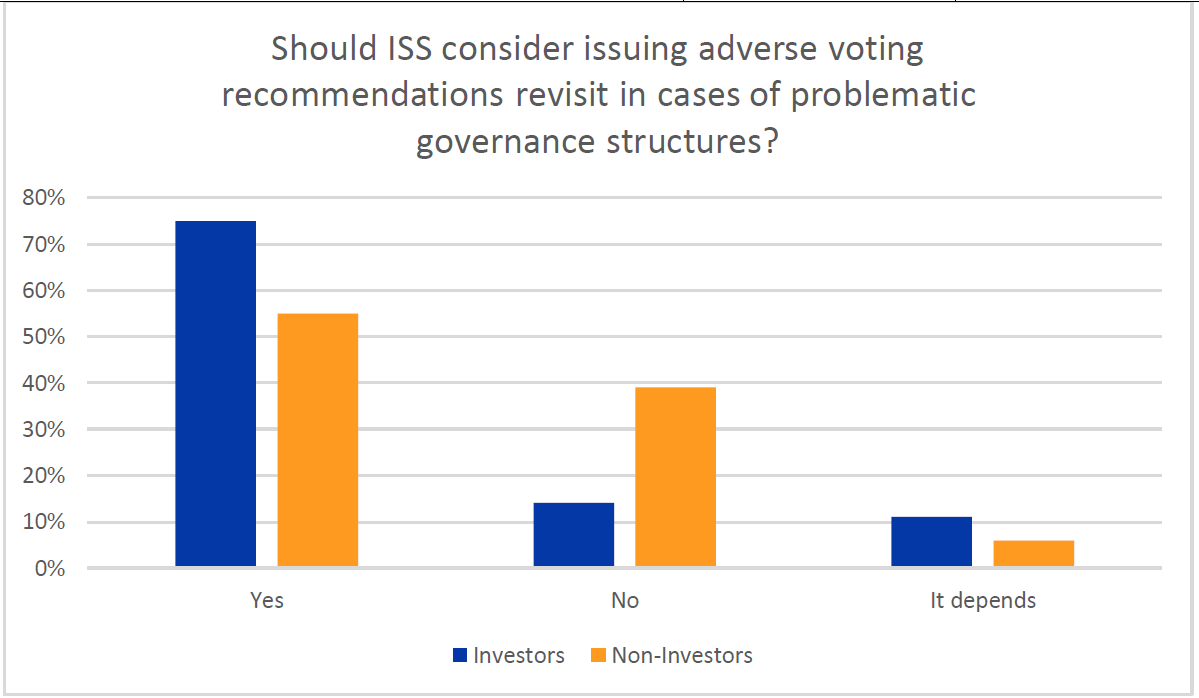

11. Unequal Voting Rights/Multi-Class Share Structures – Continental Europe

Since 2015, ISS policy for the U.S. has been to recommend votes against directors of newly-public companies that have certain poor governance provisions, such as multiple classes of stock with unequal voting rights. Starting in 2023, ISS will recommend against directors at U.S. companies with unequal voting rights, irrespective of when they first became public companies.

From the ISS Global Voting Principles, under the core tenet of Board Accountability, is the principle that “…shareholders’ voting rights should be proportional to their economic interest in the company; each share should have one vote.” This also aligns with the ICGN’s Global Governance Principles (Principle 9).

Given a number of recent developments in Europe, the question arises whether ISS should revisit its approach to board accountability in the context of unequal voting rights in Continental Europe and introduce a specific policy in this area.

We recognize that on the European continent, which consists of many different markets, many companies take different governance approaches and a variety of governance structures have historically been applied. Whether through golden share structures, multiple share classes, or the increasing numbers of “loyalty” preferential voting structures, Europe has a large variety of structures that may be considered to treat shareholders unequally. However, some of these structures have been designed with positive governance intentions and may not be universally considered to treat shareholders unequally (e.g., loyalty voting structures are in theory open to all shareholders but due to practical reservations minority shareholders rarely apply to register). In addition, there are questions of whether the board is accountable for the continued existence of such structures in all instances, for example given that holders of special share classes must often approve the abolition of an existing structure.

In your opinion, for Continental European companies with governance structures considered poor, such as having unequal voting rights, should ISS revisit these problematic provisions and consider issuing adverse voting recommendations (e.g., against discharge or reelection of directors depending on AGM agenda composition) in the future where they still exist? (i.e., at companies that still maintain these poor governance provisions and irrespective of the board being able to change the structure?)

|

Response |

Investors |

Non-Investors |

| Yes | 75% | 55% |

| No | 14% | 39% |

| It depends | 11% | 6% |

| Total Number of Responses | 150 | 69 |

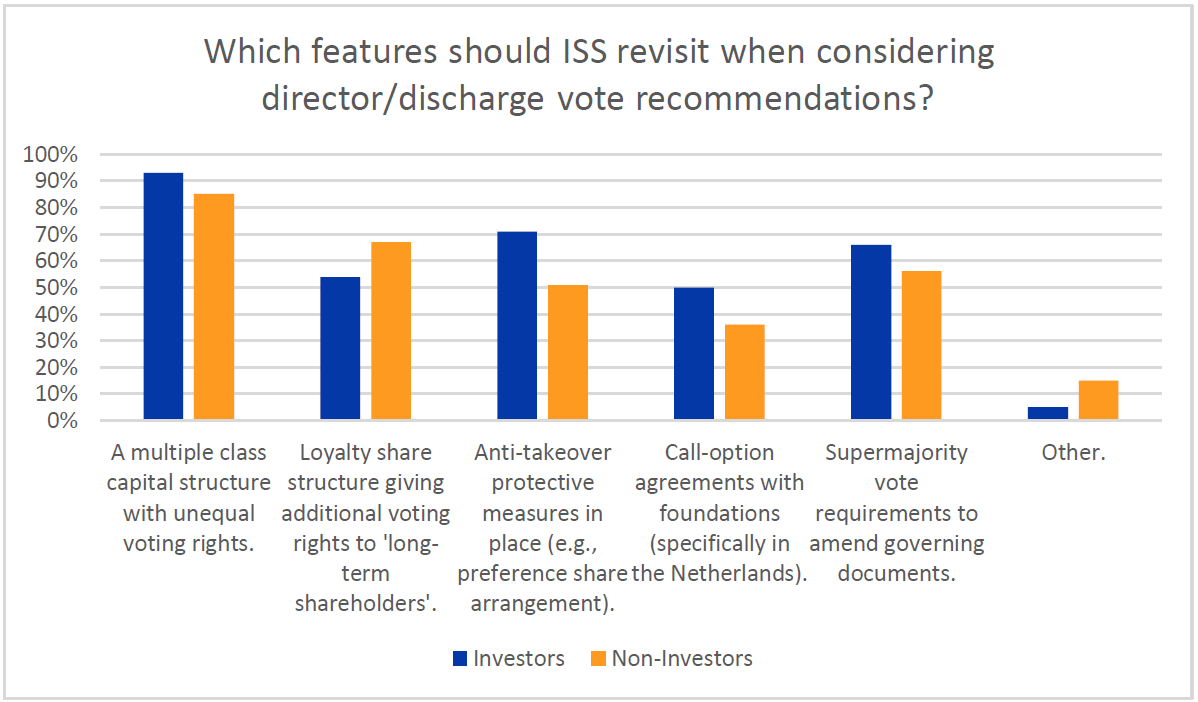

If you answered Yes above, which of the following features do you think ISS should revisit when considering director/discharge vote recommendations (check all that apply)

|

Response |

Investors |

Non-Investors |

| A multiple class capital structure with unequal voting rights. | 93% | 85% |

| Loyalty share structure giving additional voting rights to ‘long-term shareholders’. | 54% | 67% |

| Anti-takeover protective measures in place (e.g., preference share arrangement). | 71% | 51% |

| Call-option agreements with foundations (specifically in the Netherlands). | 50% | 36% |

| Supermajority vote requirements to amend governing documents. | 66% | 56% |

| Other. | 5% | 15% |

| Total Number of Responses | 122 | 39 |

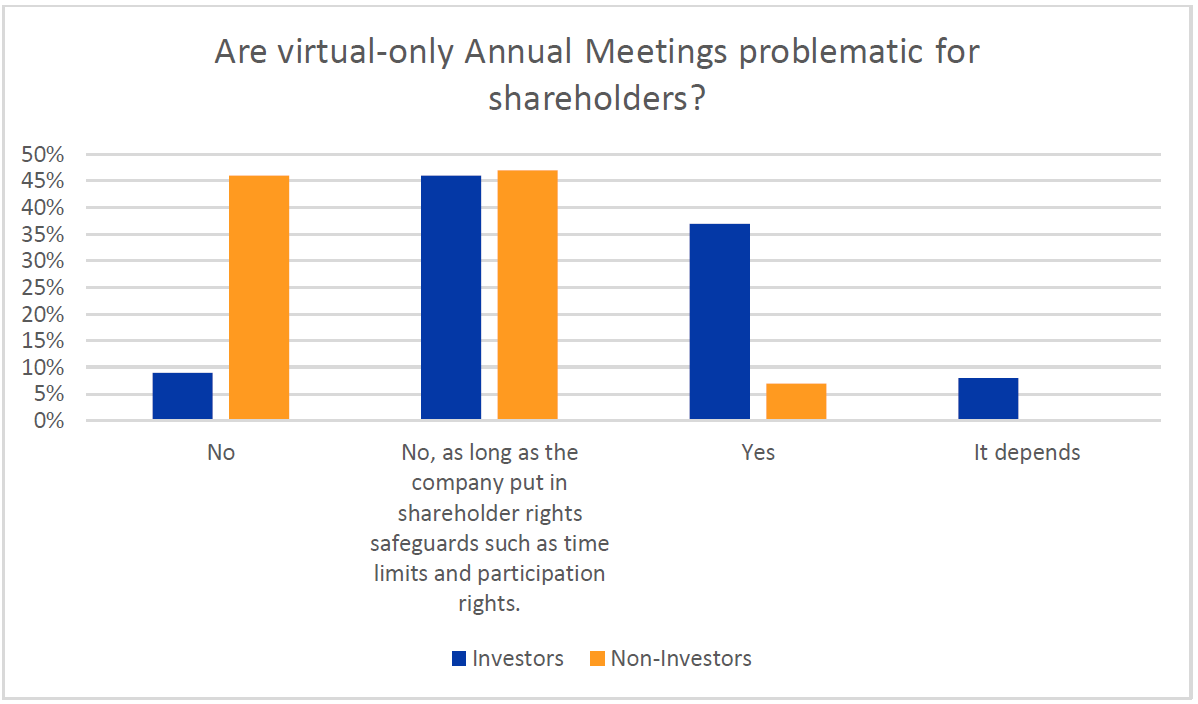

12. Virtual Meetings – Continental Europe

Various markets across Continental Europe are examining or implementing legislation that will provide for virtual-only Annual General Meetings on a permanent basis. For example, Germany has just passed a law making the option to hold virtual-only meetings a permanent one (up until now it was just an “emergency authorization” limited in time). The new law in Germany requires each company that wants to hold virtual- only meetings to amend its articles in this regard every five years, which will require shareholder approval.

Would you consider it a problematic diminution in shareholder rights for a company to hold virtual-only Annual General meetings going forward?

|

Response |

Investors |

Non-Investors |

| No | 9% | 46% |

| No, as long as the company put in shareholder rights safeguards such as time limits and participation rights. | 46% | 47% |

| Yes | 37% | 7% |

| It depends | 8% | 0% |

| Total Number of Responses | 154 | 89 |

13. Share Repurchases – Sub-Saharan Africa

In Sub-Saharan African (SSA) markets such as Botswana, Ghana, Kenya, Nigeria, Namibia and Zimbabwe, companies often submit general authorizations for market share repurchase plans for shareholders’ approval at annual general meetings. Currently, ISS Sub-Saharan African (SSA) policy guidelines support the approval of market repurchase authorities if they comply with a repurchase limit of up to 10 percent of the outstanding issued share capital, a holding limit of up to 10 percent of a company’s issued share capital in treasury and a duration of no more than five years, or a lower threshold as may be set by the applicable law, regulation, or governance code. Support is also warranted for repurchase programs in excess of the 10 percent repurchase limit on a case-by-case basis provided that on balance, the proposal is in shareholders’ interests.

However, depending on Sub-Saharan African markets’ laws and regulations, while the repurchase limit may fall in line with the current 10 percent threshold of the outstanding issued share capital as per ISS policy, it may exceed such limit, therefore being not aligned with the current ISS SSA policy guidelines.

Given that SSA companies regularly seek approval on general market share repurchase authorities that exceed the ISS limit of up to 10 percent, and in order to be in line with the respective applicable local laws and regulations as well as the South African policy guidelines, what would your organization favor among the following options?

|

Response |

Investors |

Non-Investors |

| A limit of up to 20 percent to be applied to all Sub-Saharan African markets provided that this is the highest limit set by the laws and regulations in these markets. Note that a limit of up to 20 percent would be aligned with the South African ISS policy guidelines. | 12% | 6% |

| A limit that falls in line with the laws and regulations of the stock market in which the company is listed as stipulated by the relevant competent authority. | 23% | 44% |

| Keeping the 10 percent threshold as the main guidance whatever the local regulations. | 29% | 34% |

| Keeping the 10 percent threshold as the main guidance while accepting higher thresholds if corresponding to local regulations but not beyond a 20 percent limit. | 21% | 10% |

| Other. | 14% | 6% |

| Total Number of Responses | 121 | 50 |