Print

PrintMaria Castañón Moats is Leader, Paul DeNicola is Principal, and Colin Wittmer is Deals Leader at PricewaterhouseCoopers LLP. This post is based on their PwC memorandum.

Introduction

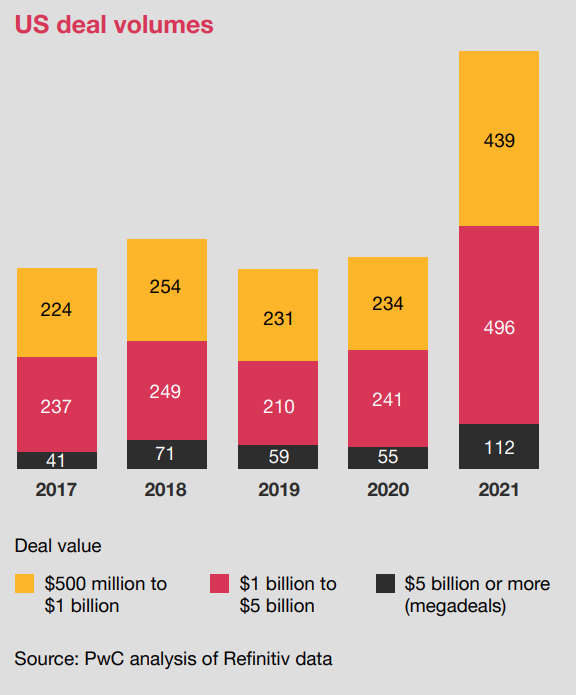

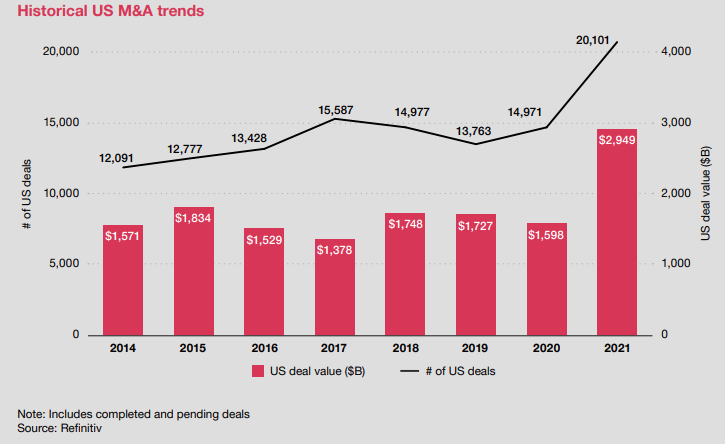

The deal volume in 2021 reached levels not seen in recent years, a trend that continued into the first part of 2022. But since then, the markets have shifted.

With rising inflation rates, geopolitical uncertainty, continued supply chain interruptions, and a lingering pandemic, deal volume began to slow significantly as 2022 progressed.

A period of economic contraction will certainly influence transactions. This flows through inflationary, and borrowing rate pressure, real wage challenges, consumer spending variability, and other factors. The markets in 2022 still have an abundance of capital for both corporate and private equity (PE) to fund deals. As market volatility stifles IPO activity, alternative sources of capital (including from PE) become more appealing.

Some of the same forces creating market uncertainty also are driving dealmaking imperatives. Whether a company needs to transform its capabilities, supply chains, or go-to-market approach, the market is impatient and one of the fastest ways to accelerate transformation is through M&A.

Navigating this rapidly-evolving market presents a challenge for any business leader. But in any environment, a well-tailored deals strategy will open opportunities. And the current environment still poses a fiercely competitive deals marketplace as companies look to unlock value in new ways.

Overseeing deals and your company’s portfolio strategy

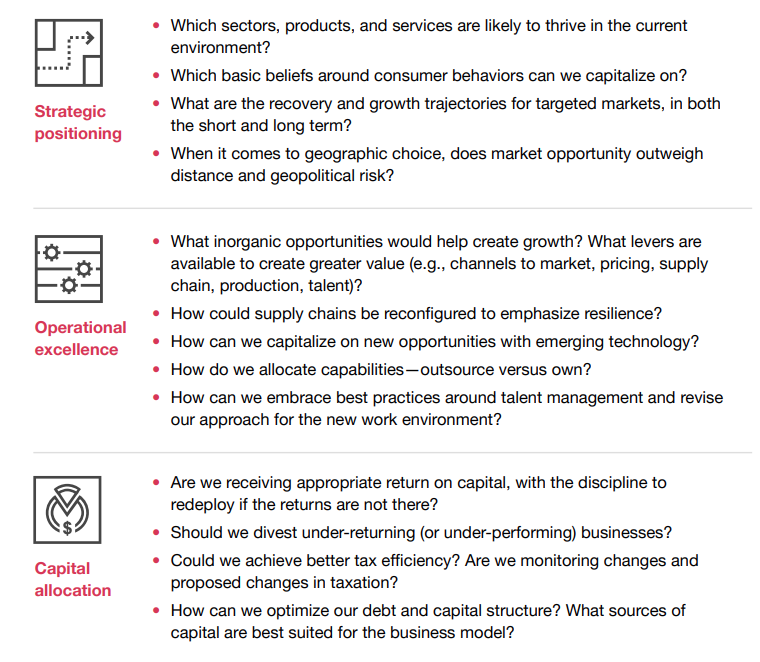

Having a focused deals strategy is critical to success. Along with organic growth through increased sales and new products and services, growth can also come through acquisitions, mergers, joint ventures, and other deals. What’s critical for the board is understanding the ins and outs of the deal, and how various transactions a company has done or wants to do are tied together in a portfolio strategy.

Drivers of a deals strategy

Understanding the current portfolio and how deals can optimize it

Back to fundamentals. Separate from and before considering individual deals or a deals strategy, board members should be fully briefed on the company’s portfolio of businesses— what the company already has. Once directors establish that initial understanding and have a clear view of the company’s components, they can better consider how deals can improve the overall mix. In this way, a deals strategy is part of the overall strategy—a means to a greater organizational goal—not a separate process for handling individual transactions.

Unlike the management team, directors generally don’t need to know all the details of each business. But boards do need to regularly review each business to understand the portfolio as a whole. This also helps them understand why they’re categorized as they are (i.e., Grow, Maintain, Fix, or Exit) and what the optimal future mix is based on the business strategy.

Many companies still do M&A reactively, evaluating deals as they come on the market and then trying to make the case for strategic fit. But increasing dialogue around inorganic growth in general will put the board in a much better position when specific deal opportunities emerge, especially if they’re a departure from the agreed-upon deals strategy.

The best-performing companies:

|

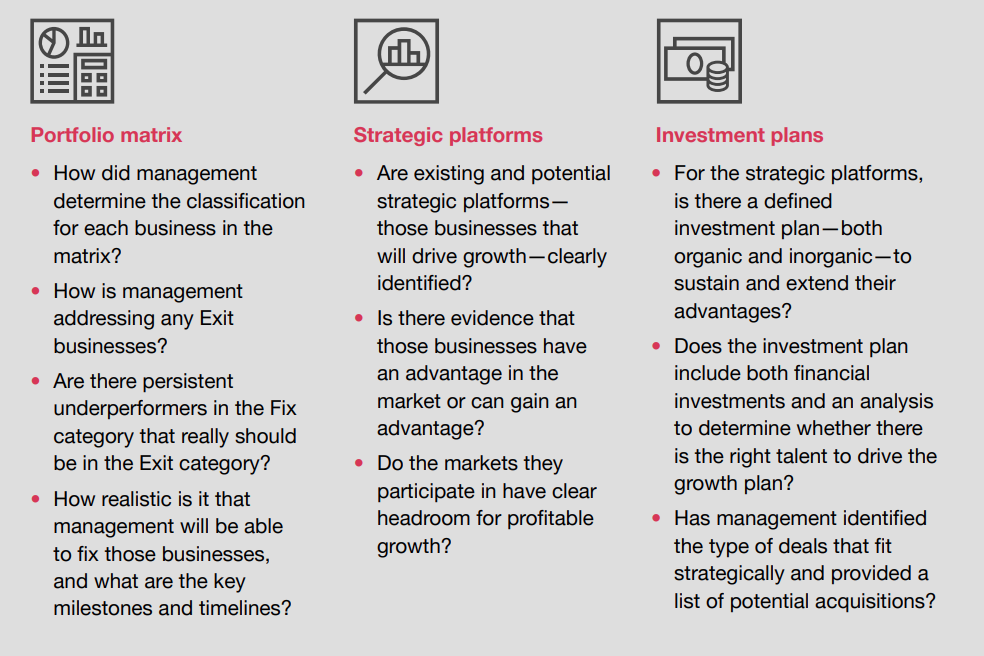

Key questions directors should ask about their company’s portfolio strategy

Board involvement in a transaction

The board’s oversight of the portfolio strategy is critical. Before the company moves on a transaction, the board should be confident that it fits the company’s strategy and that the timing is right. The board should understand what’s motivating the deal. Is it a road to a new business or market? Are shareholders pushing for a change? Are economic factors creating unique opportunities?

It’s also important to agree on the level of the board’s involvement. All deals are not equal, and they don’t need the same level of board attention. Some factors are quantitative, like relative deal size compared to the company. They can also be qualitative, such as when a deal is important to executing the company’s established strategy, or is the first step in a new strategic direction. The company’s Delegation of Authority policy can help clarify the criteria for a board’s involvement.

If a company does a lot of deals, it might work well for the board to be informed of the list of targets on a regular basis. Management can give updates at every board meeting—sharing the business plans for each, the status of due diligence, and pricing and other factors. Directors can give feedback and share any concerns and advice in real time. Then, by the time management asks for board approval, the board is well positioned to make its decision.

For companies without a track record in transactions, board involvement can be even more important. The deal may be a departure from the company’s established strategy, meant to take advantage of a unique opportunity. In that case, involving the board early (and more deeply) can help bring critical skills to the table as the deal is negotiated.

Pushing the pause buttonIn some cases, management can become overly invested in doing a deal. A transaction that made sense at first might start to become less appealing. When that happens, it’s up to the board to reset the strategy and make sure the deal should proceed. |

Seeking outside opinions

Strategic advisors can help a board properly evaluate an opportunity. They can be essential in confirming or questioning management’s risk assessment and valuations. For each transaction, directors should be aware of which outside advisors the company used to evaluate the deal. They may decide to challenge management on any advice received especially for significant transactions, or ones where the board senses “deal fever.” Or they may want to bring in another advisor for an unbiased view. Fundamentally, the board needs to be sure the deal is right for the company before approving it.

Directors should be sure to get regular updates from management. But they should also take advantage of opportunities to discuss the deal without management present. Such private sessions are especially valuable in helping the board feel comfortable pushing on any assumptions in the valuation or voicing concerns about overzealous pricing.

For a particularly significant deal that will require a substantial investment of director time, or for one that could pose independence concerns for certain directors, boards will form a special committee, sometimes with separate legal counsel or other advisors.

Keeping all audiences informed, and monitoring after the fact

Communication and transparency are vital during and after a transaction, and companies should be able to clearly articulate the argument for the deal. Companies benefit from an internal communication plan that keeps employees and vendors appropriately informed during the process. Besides limiting uncertainty, knowing the plan can boost the team’s motivation.

Management should consider all communication angles—not just financial metrics, but how the transaction might impact the company in areas such as talent development and organizational culture. Boards should get regular updates on post-transaction metrics, including performance measure, any cost synergies, and how management is addressing any culture clashes.

Externally, big transactions often generate interest in the market, and the less confusion about why a deal was done, the better. Boards will want to be sure management clearly explains to investors the rationale for a deal and how it fits into the company’s overall strategy. When Wall Street understands the message, deals are usually viewed more favorably.

Monitoring the transaction post-deal also allows boards to assess whether the deal met the objectives and understand how much value it ultimately added. Determining what made a specific deal a success can help improve the overall process, from strategy to integration. This will better arm the board and the company for future deals.

Acquisitions

The right acquisition can boost a customer base, increase revenue, and even reduce costs. But making an acquisition is a huge decision for a company. Before taking the plunge the board needs to be confident it’s the right move with the right target. This applies not only to an individual deal, but also to how acquisitions fit into a company’s overall portfolio strategy.

Identifying risks

Companies have to take the bad with the good in an acquisition, and boards should push management to assess the key risks that can affect value. These include:

- Cybersecurity risks • Vulnerability to lawsuits

- Underpayment of taxes

- Underfunding certain parts of the organization or ongoing liabilities

- Environmental damage and remediation

- For cross-border deals—Foreign Corrupt Practices Act violations and other regulatory hurdles

In general, the farther the target is from the company’s current situation—geographically, operationally, or product-wise—the riskier the deal.

Looking for culture clashes

The due diligence phase is a time for directors to raise the issue of culture. Ideally, the board should confirm that management is considering how the two cultures align, and how they can be integrated. Acquisitions naturally raise concerns around loss of the target company’s identity and history. Boards should ask whether integration plans respect the legacy of both companies, and about plans to assimilate new employees into the organization following the acquisition.

In cross-border deals, cultural concerns may include managing different worldviews along with the workplace environment and practices. A change that seems minor to a US-based company could have much more significance to people working in another country.

Never a simple task, these culture evaluations have become more difficult as many companies navigate differing work-from-home and hybrid work expectations. Company culture is harder to define or assess when employees are not working on-site, and harder to influence when employees are not gathering together in a workplace. And the policies themselves have become a significant part of a company’s culture.

The integration challenge

In significant deals, the period after the acquisition closes is crucial. Failure to successfully integrate the employees, processes, systems, and culture from an acquired organization can seriously hamper realizing a deal’s benefits. It’s also essential to have a robust postdeal communications strategy that explains the advantages of the acquisition to key external audiences and updates employees across the combined enterprise about the progress of integration.

Talent is often a major concern in acquisitions. Some executives and their teams are key to the deal value. Others may not be needed beyond a transition point. Management needs to figure out who fits into which category. These can be sensitive decisions. From the company’s perspective, layoffs will impact employee morale, while failure to address redundancies can create long-term consequences.

Board changes

Major acquisitions will have effects on the board. In a merger of equals, both company boards will be significantly impacted, as they go from two boards to one. The deal negotiation will typically cover these changes. Each entity usually receives a right to a certain number of seats, and the combined board may be larger than either company’s prior board. Deciding which directors will fill those roles can be tricky. Successful boards focus on finding ways to work together, and recognize that directors may be experiencing a culture shift along with the rest of the company.

In a slightly smaller transaction, it’s common for the target to negotiate a role on the board. Target directors may fill one or two seats, depending on the size of the deal.

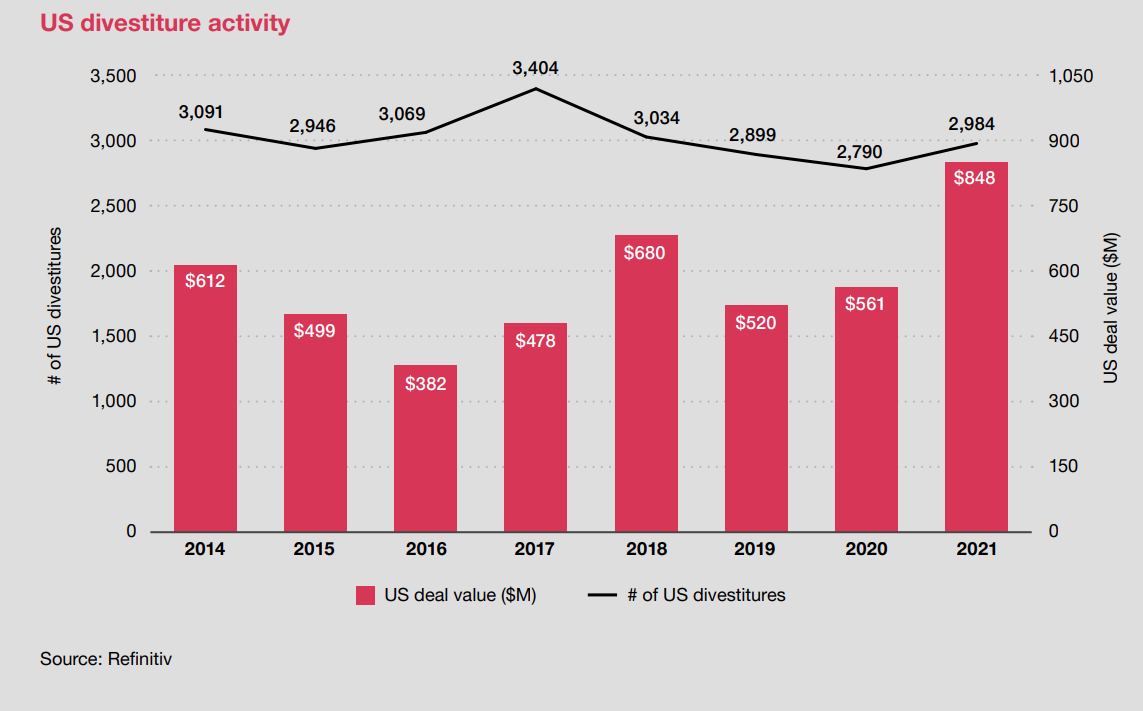

Divestitures

Divestitures can be challenging. A company must identify the business units to be separated, decide on the type of separation, and either develop a standalone operating model and cost structure for that business or prepare it for sale. While these steps may seem straightforward, a divestiture ultimately is a surgical procedure, with a degree of complexity that demands careful planning and caution.

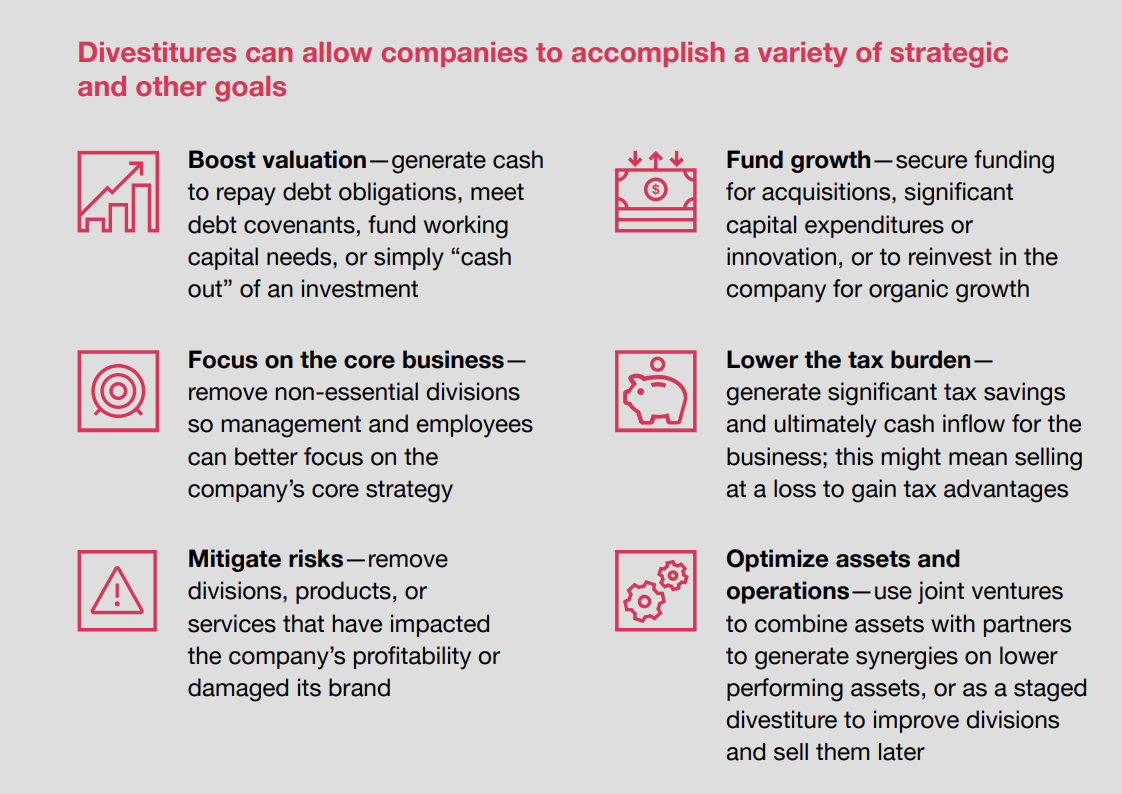

The reasons for divesting part of a company can vary. Changes in economic circumstances may have made a particular business unit unsustainable. A business unit may no longer align with the company’s current strategy. Divestitures can also present opportunity: a thriving business may have outgrown the parent company, or individual parts of an enterprise could be more valuable as separate businesses or part of another company. Or a company may divest a business so it can reinvest the proceeds in the remaining company or pursue growth opportunities, including acquisitions.

A company’s rationale for a divestiture should be strategic, clear, compelling, and one the board fully understands and endorses. One simple question directors can ask is if and how removing a business unit will allow the company to do something it can’t do today. The divestment should result in the company being in a stronger position.

Timing

If a company has decided that a divestiture is wise, a threshold question will be whether there is a market for the transaction. In some cases, the company may want to delay the transaction until the market is right.

Timing can also be an important consideration in any discussion about a potential divestiture. Different types of divestitures typically take different lengths of time to complete, with a sale typically presenting the quickest exit. If a company needs to secure capital, reduce expenses, or make some other financial or strategic move in the short term, it may be limited to contemplating a sale because other deals would take too long.

Sales raise key considerations around how to maximize value for shareholders. Management should tell directors if there’s a specific buyer in mind or if the business unit will be marketed to a wide range of possible buyers—and if the latter, how and to whom. Private equity buyers may have different requirements or conditions than corporate buyers. The board should be able to share any concerns it might have with management. This might include challenging management on whether the company is comfortable totally giving up the business in question instead of maintaining a relationship through another type of divestiture.

Carve-out IPOs, spin-offs, split-offs, and joint ventures (JVs) take longer to finalize— sometimes more than a year. As in a sale, there’s the work of separating the business unit from the parent company’s operational and financial infrastructure. But forming a new entity can also involve legal, regulatory, and other requirements, which can add weeks or months.

Company resources

The investment of time, money, and energy into a divestiture process is usually significant and can test management, especially if a company is already lean or struggling. Without adequate resources, the transaction could become a distraction that affects day-to-day operations—something the board should be aware of and discuss with management ahead of time.

Before the company embarks on a divestiture spanning several months, directors should ensure management has or will hire the right people to handle the heavy lifting. Divestitures often involve multiple workstreams spanning areas like finance, HR, IT, and others. Coordination among those teams will be critical, as is bandwidth. Many companies underestimate the time involved in separating a business unit, so the board should be confident that management has a fulsome plan to keep the remaining businesses running effectively during that time.

Talent management

Depending on the type of divestiture, handling talent can also be a challenge. In a sale, the employees and leaders in the business unit often stay in their existing roles as the business moves to new ownership. But the divesting company may want to retain certain talent, such as executives with senior leadership potential. Board members should be aware of those conversations and efforts to ensure that such pursuits don’t jeopardize the transaction.

Talent migration can be complex, particularly for employees working outside the separating business unit, such as finance or IT. While people attached to the divested business can expect to be affected, the transaction could also pull employees from these enterprise functions, and management needs to be strategic about who stays and who goes. Tackling these issues early will help prevent scrambling to fill key positions later.

A divestiture can also have an indirect impact on employees and managers who aren’t involved in the transaction. Uncertainty about the parent company’s future could cause talent to consider other opportunities. The board should confirm that management has a comprehensive communications plan for the entire deal cycle.

Transition services agreementIn some divestitures, a transition service agreement (TSA) requires the seller of a business to provide certain services and support for a certain period after the deal closes. Divestitures can be tricky to pull off, particularly when essential services and infrastructure are shared across multiple business units. In those cases, a TSA is important to help ensure business continuity while the new company establishes its own internal capabilities or transitions to a third-party vendor. A TSA may require the seller to provide services for the business that is being divested for a period of time following the transaction. These services might include finance and accounting, human resources (HR), legal, information technology (IT), procurement, or others. The cost of a TSA can affect the overall transaction value, and should be estimated during early divestiture planning. These costs could affect negotiations between the buyer and seller, as well as the purchase price or cost of the TSA. |

Post-transaction risks

In some divestitures, accounting, legal, tax, IT, or other important services may not go with the subsidiary, leaving the parent with more employees or capacity than it needs. The parent company will have to determine how to deal with the resulting stranded costs or overhead. The board should discuss with management how those costs will be managed.

The board should also understand whether the divestiture process could make the company vulnerable to competitors. With highly visible and/or complex separations, other companies could see an opportunity to disrupt customer relationships and grab market share. Management should explain to the board how the company is prepared to handle any such attacks and how they will provide business as usual for customers.

Alliances and joint ventures

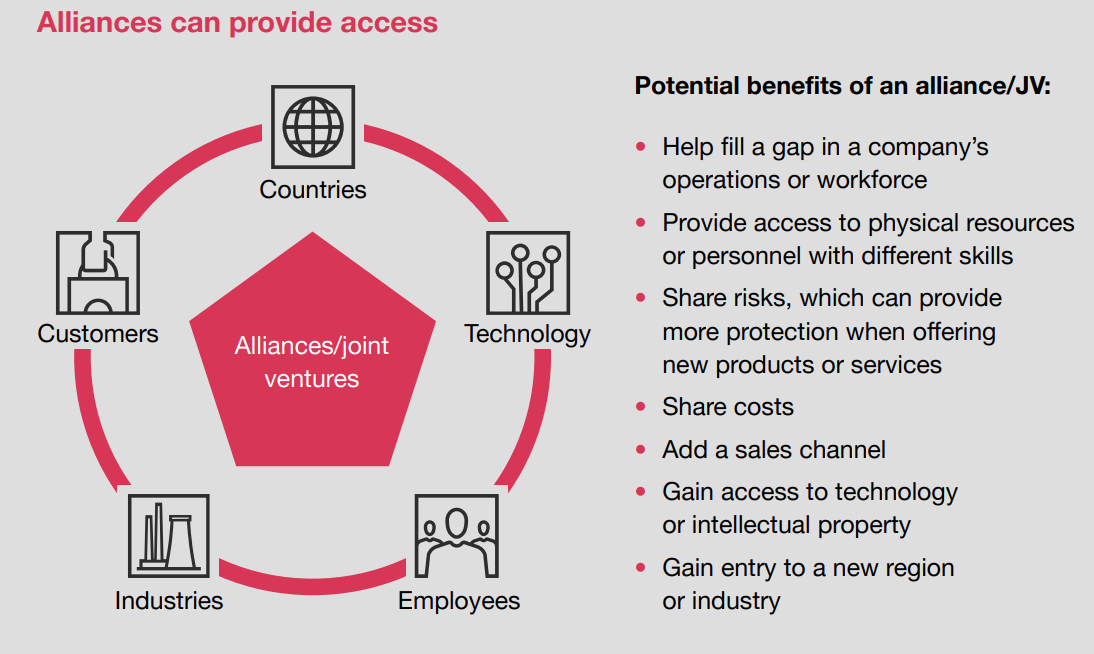

Strategic alliances and JVs hold a unique place in the deal universe. Unlike an acquisition that adds a business or a divestiture that eliminates one, an alliance or joint venture allows two or more companies to pursue a shared goal while continuing to operate the other parts of their businesses independently. When considering an alliance or JV, the board should know the broader deal landscape, including market trends and recent actions by competitors, and understand how the move fits into their broader portfolio strategy.

An alliance or JV may make sense when a company faces regulatory restrictions, is dealing with market uncertainty, or wants access to specific distribution channels or intellectual property. These types of deals allow the parties to share costs, and may provide access to technology or entry to a new region or industry. For an alliance or JV to move a company forward, the benefits should be apparent at the outset.

Goals and governance

By identifying and pursuing common goals, partners can jointly develop a compelling business case for the alliance or JV. Partners should agree on how performance toward those goals will be measured and monitored, and establish interim goals along the way. It’s essential to be clear on the strategic, operational, organizational, and financial metrics, how frequently they’ll be tracked and reported, and how adjustments will be made. Monitoring should begin on day one, with the agreed upon metrics closely tracked and shared as scheduled with the appropriate people.

Companies planning an alliance or JV also need to establish clear, appropriate governance for the entity up front. Boards may express particular interest in the selection of the JV leadership— not only its board, but also the CEO and key management appointments. In some cases, it may make sense for a director from each partner company to sit on the board of the JV.

Appropriate communication and consultation throughout the process will improve the odds of success. While the partners in an alliance or JV still control their own operations, sharing resources and risks requires a lot of information-sharing and trust. Sometimes an alliance or JV can be more complex and require more collaboration and upfront planning than an acquisition.

| Pre-approving an operating budget for the first year can help smooth the start of an alliance or JV. |

People and culture

Determining which employees—existing and/or new—will support the alliance or JV is vital for a successful launch. The partnership team must be capable and enthusiastic about the new opportunity, and the board should ensure that management has approved appropriate incentives to secure the right people—from inside and outside the company. Not having a clear organizational design can hinder the management of the alliance.

Management decisions in this area can involve sensitive negotiations and reveal potentially divergent cultures of the partner companies—an important consideration, especially if there are cross-border issues. The board should encourage a culture assessment to understand how each partner works. This awareness can help in building a common culture for the alliance or JV and embedding it into the partnership’s communications and engagement strategies, governance, individual performance, assessment, and reward philosophies.

Board changes

If a new company is created through a JV, it will need its own board of directors. The parent companies’ boards and management should collaborate on a recommendation for that new board, including its structure and how much the new entity’s governance policies should align with those of each of the parent companies. Depending on the focus of the new entity, it could make sense for some of the parent companies’ directors to join the new entity’s board.

Risks

Identifying potential significant risks in a new alliance or JV is an important part of planning. It starts with the partner. Unlike in the acquisition context, indemnification or segregation of risks may not be possible given the continuing involvement with the partner. So the board should be informed about the process for vetting potential partners, including possible red flags. Due diligence covering commercial, financial, tax, operations, legal, and insurance, as well as environmental and information technology should be comprehensive enough to uncover potential concerns. The board will also want to be sensitive to the potential for market cannibalism—that a partnership intended to grow business for all partners instead benefits only one at the expense of another.

The board should ask management and the deal team how all key risks associated with a particular partner have been considered and mitigated to reduce their potential impact on the company. Directors also should be clear on how disputes between partners will be resolved and confident that the resolution process doesn’t pose legal or other risks to the company.

After the alliance or JV launches, the board will want to monitor for early warning signs. Beyond poor financial performance, these can include a disconnected culture, flawed business strategy, lack of execution on commitments by another partner company, or disputes within the alliance or JV.

Exit

Since it’s often easier to form a partnership than to unwind it, it’s a good practice to anticipate the end even before you begin. Sometimes the parties will agree on an end date at the outset. If reporting shows it is accomplishing its objectives and the partner companies are satisfied with its performance, then the partnership likely will continue to that date. The boards of the partner companies would receive updates on the exit timeline and allocation of assets and resources, as well as any financial reporting issues and legal and tax implications. There also could be an opportunity to amend and extend the partnership.

But if poor performance, financial issues, or changing regulatory conditions alter plans, the boards of both entities need to have a frank discussion with management about options. Changing the alliance or JV may be possible; alternatives range from a simple change in contract—mitigating the damage to one or more partners—to a merger or acquisition.

If modifying the structure or deal isn’t an option, then the board may need to consider unwinding the alliance or JV through an early exit. Penalties outlined in the original agreement need to be considered, as do the prospects of legal action that could have a financial and reputational impact. Then there’s the impact on the company’s strategy, especially if the alliance or JV was heralded as a strategic fit.