Print

PrintSubodh Mishra is Global Head of Communications at Institutional Shareholder Services. This post is based on an ISS Corporate Solutions memorandum by Senior Editor, Paul Hodgson. Related research from the Program on Corporate Governance includes The Untenable Case for Perpetual Dual-Class Stock (discussed on the Forum here); The Perils of Small-Minority Controllers (discussed on the Forum here); and Keynote Presentation on The Lifecycle Theory of Dual-Class Structures (discussed on the Forum here) all by Lucian Bebchuk and Kobi Kastiel.

KEY FINDINGS

- The proportion of companies in the Russell 3000 excluding the S&P 1500 with unequal voting rights increased significantly since 2020

- The proportion of companies in the S&P 1500 with unequal voting rights remained relatively flat from 2015 to 2022, with some variations

- None of the sunset provisions in the S&P 1500 met best corporate governance standards and only around one in 10 did so in the Russell 3000 excluding the S&P 1500

- The Russell 3000 increase in dual class shareholder structures may have been driven by new entrants to the index and SPAC transactions

- The number of companies in the whole Russell 3000 adopting sunset provisions – which terminate a dual class share structure – increased over the whole 2015-2022 period

Dual class share structures have been traditionally used to protect newly public companies from hostile takeovers or other forms of interference. Such arrangements typically gave founders disproportionate control over the company through supervoting shares that command multiple votes, as opposed to publicly held common shares, which usually have one vote per share or sometimes no voting power at all.

To look at trends in unequal voting structures, we examined two data points from ISS Corporate Solutions Data Analytics: 1) whether a company has an unequal voting rights capital structure, and 2), if they do, whether there is any sunset clause attached to it. Sunset provisions set out how, and sometimes when, dual class share structures are terminated and all shares turned into a single class.

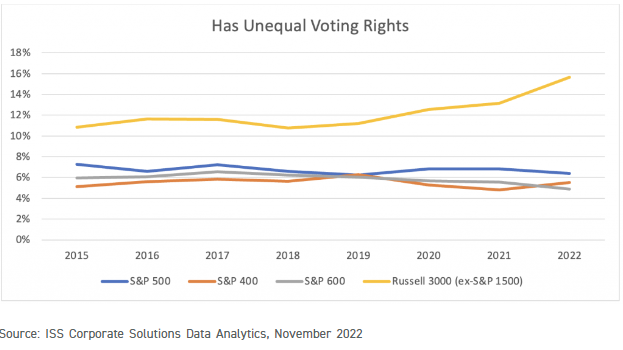

Trends in Unequal Voting Rights, 2015-2022

For large-cap companies (S&P 500), the proportion with unequal voting rights remained relatively flat at just under 7% after reaching a high of 7.3% in 2015 and a low of 6.2% in 2019, with a slight downward trend over the last two years. The pattern of unequal voting rights for mid-cap companies in the S&P 400 and small-cap companies in the S&P 600 also show a relatively flat line, though at a lower proportion than in the S&P 500. S&P 400 companies had a high of 6.6% in 2017 and a low of 4.8% in 2021, though, in contrast to the S&P 500, the proportion rose in 2022, to 5.5%. In the S&P 600, the low of 4.9% was in 2022, while the high of 6.6% was reached in 2017.

Among the smallest caps, Russell 3000 companies excluding the S&P 1500, there is a notable increase of companies with unequal voting rights, especially starting from 2020. These increases are likely driven by new entrants as an unequal voting rights capital structure is almost always adopted before a company goes public. In addition, the number of SPAC (special purpose acquisition company) transactions started to rise rapidly in 2020 and spiked in 2021, which may also have driven this increase. Between 2019 and 2022, the percentage of Russell 3000 companies excluding the S&P 1500 with unequal voting rights increased from 11.2% to 15.7%.

Percentage of Companies with Unequal Voting Rights Capital Structure

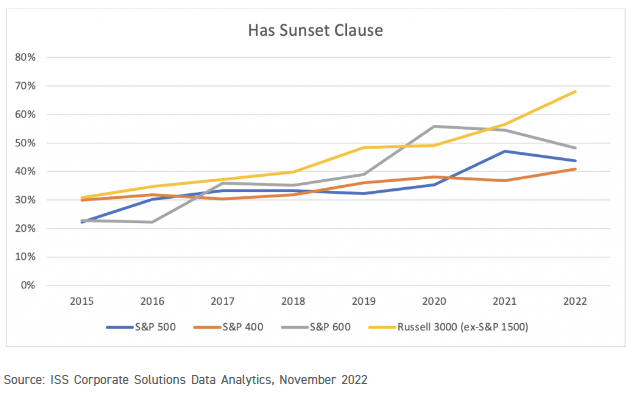

Sunset Provisions

By contrast, the proportion of companies with unequal voting rights that have adopted sunset provisions has been increasing fairly steadily since 2015. In the Russell 3000 excluding the S&P 1500, the proportion more than doubled between 2015 and 2022, from 30.9% to 68.1%. While there was a similar increase in the S&P 500 until 2021 (from 22.2% to 47.1%), it fell back in 2022. Notably, the proportion of companies with sunset provisions in the S&P 500 is much lower than in most of the rest of the Russell 3000, more than 20 percentage points lower than the smallest companies in some years.

Percentage of Companies with a Sunset Clause (as a Percentage of Companies with Unequal Voting Rights)

ISS Corporate Solutions data indicates that institutional investors may not view most of these sunset clauses to be sufficiently robust, given that the triggering event is either indeterminate or takes place more than seven years after the IPO. Indeed, none of the sunset clauses in the S&P 1500 meets this market best practice of going into effect seven years or less from IPO. Among the Russell 3000 excluding the S&P 1500, only about one in 10 sunset provisions meets this standard. Most are structured such that if the founder leaves his or her management or board position, their shares would be converted to ordinary shares. Such an occurrence, of course, has no time limit.

Dual Class Share Structure Origins

Prior to the rise of Silicon Valley tech startups, dual class structures were largely confined to media companies. Generally, these companies viewed a dual class structure as a necessity to maintain journalistic integrity. More recent dual class share companies, such as technology and social media companies, established and maintained these structures so that founders, whose visions are seen as integral to the company’s success, could maintain control.

The Institutional Investor Viewpoint

Many institutional shareholders disapprove of dual class shares, preferring one-vote one-share structures. The Council of Institutional Investors (CII), for example, opposes such structures, while recognizing the value of the protection they offer for a certain period after an IPO. As the CII says: “CII has pressed dual-class IPO companies to include reasonable time-based “sunset” provisions in their charters.” It views a sunset provision of seven or fewer years as acceptable.

The CII is also part of the Investor Coalition for Equal Votes, which was launched in June this year by the UK pension fund Railpen and U.S. pension funds the Minnesota State Board of Investment, New York City Comptroller’s Office, New York State Common Retirement Fund, Ohio Public Employees Retirement System and the Washington State Investment Board. The Coalition seeks to engage with pre-IPO firms to encourage them to adopt the kind of robust sunset provisions called for by the CII. By contrast, over the last few years, the UK, Singapore, Spain, Italy and Hong Kong have all adopted regulations that made it easier for companies to adopt a dual-class structure.