Print

PrintShaun Bisman is a Partner and Jared Sorhaindo is an Associate at Compensation Advisory Partners. This post is based on their CAP memorandum. Related research from the Program on Corporate Governance includes The Perils and Questionable Promise of ESG-Based Compensation (discussed on the Forum here) by Lucian A. Bebchuk and Roberto Tallarita.

ISS recently published 2023 policy changes, which will go into effect for annual meetings held on or after February 1, 2023. This article discusses the changes and policy clarifications made to ISS’ compensation and Environmental, Social and Governance (ESG) voting policies.

Executive Compensation-Related Updates

Problematic Pay Practices

ISS has explicitly indicated that severance received by an executive when the termination is not clearly disclosed as involuntary will be considered a problematic pay practice, which may result in an adverse vote recommendation. ISS has also clarified that the types of pay practices that may result in an adverse vote recommendation are not limited to the examples provided in the policy document. The full list of problematic pay practices can be found here.

As noted by ISS, this is not a policy application change, but rather codifies ISS’ current approach to evaluating severance payments received by an executive when the termination is not clearly disclosed as involuntary.

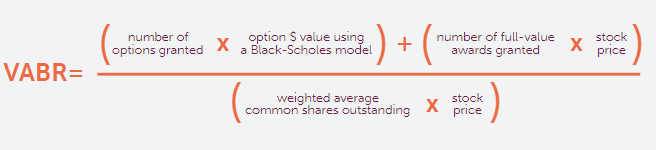

Value-Adjusted Burn Rate

ISS announced in its update last year that it would change its burn rate calculation effective as of February 1, 2023. The burn rate will be referred to as the “Value-Adjusted Burn Rate” (VABR) and will be calculated as follows:

The one-year transition period to the new VABR methodology has passed.

ESG-Related Updates

ESG Metrics in Compensation-Related Proposals

The ISS policy on ESG compensation-related proposals is to generally recommend voting against shareholder proposals seeking to set absolute levels on compensation or otherwise dictate the amount or form of compensation (such as types of compensation elements or metrics) to be used in incentive pay programs. The updated policy considers that the company’s board or compensation committee is generally in the best position to determine the performance metrics, whether they are financial or ESG specific, while affirming that improved disclosure about the committee’s rationale and considerations of pay metrics (including those for ESG topics) may benefit shareholders.

Board Gender Diversity

As announced in 2021, ISS will recommend a vote against or withhold from the chair of the nominating committee in instances where there are no women on the board for companies in the Russell 3000 or S&P 1500 indices. An exception is made when there was a woman at the preceding annual meeting and the board has made a firm commitment to return to a gender-diverse status within a year. New for 2023, a one-year grace period will be applied at companies where there are no women on the board but there is at least one director who is disclosed as identifying as non-binary. This same policy will apply to all companies, not just in the aforementioned indices, beginning February 1, 2023. The policy will also expand to all Foreign Private Issuers beginning in 2023.

Shareholder Proposals on Racial Equity and/or Civil Rights Audits

ISS slightly modified the factors it will consider when evaluating shareholder-proposed resolutions on racial equity and/or civil rights audits. In addition to the factors listed last year, ISS states that it will consider whether the company adequately discloses its workforce diversity and inclusion metrics and goals. ISS removed language that it would consider whether the company’s actions were aligned with market norms on civil rights and racial/ethnic diversity, stating that “it has not in practice been an analysis driver for this type of proposal.”

Climate Accountability

If a company considered to be a significant greenhouse gas (GHG) emitter (which ISS defines as in the Climate Action 100+ Focus Group) does not adequately disclose climate risk disclosure information and does not have either medium-term GHG emission reduction targets or Net Zero-by-2050 GHG reduction targets for at least Scope 1 and Scope 2 emissions, ISS will generally recommend a vote against or withhold from the chair of the responsible committee. This is the first time ISS has defined specifically what it considers to be “appropriate GHG emissions reductions targets.” ISS has indicated that emissions targets should cover 95% of a company’s Scope 1 & 2 emissions.

This article highlights changes to ISS’ policies and is not intended to be exhaustive. For information related to ISS voting policies, please visit ISS Proxy Voting Guidelines Updates for 2023.

As noted by ISS, there will be additional updates to the proxy voting guidelines for 2023 published in late 2022 / early 2023. Upcoming key dates include:

- Early-Mid December: Publication of all updated ISS benchmark policies (proxy voting guidelines) for 2023.

- By end of January 2023: Publication of updated Frequently Asked Questions (FAQ) documents.