Print

PrintOren Lida is a Research Director at Glass, Lewis & Co. This post is based on his Glass Lewis memorandum.

In the United States and around much of the globe, the 2023 proxy season looks set to take place in the first protracted bear market for more than a decade. That will have an impact on how shareholders vote, and on the types of proposals they are voting on. As public companies, investors and other stakeholders bear down for the annual flood of annual meetings, an old compensation technique may be taken out the drawer and dusted off by boards: option repricing.

What is Repricing?

Repricing boils down to revising the exercise price of outstanding options awards to a lower (and thus more attainable) level. Its close cousin, the option exchange, replaces outstanding stock options with new stock options with lower exercise prices than those of the stock options they replaced. Both serve the same objective, and for the purpose of this analysis, we refer to both courses of action under the general category of “repricing.”

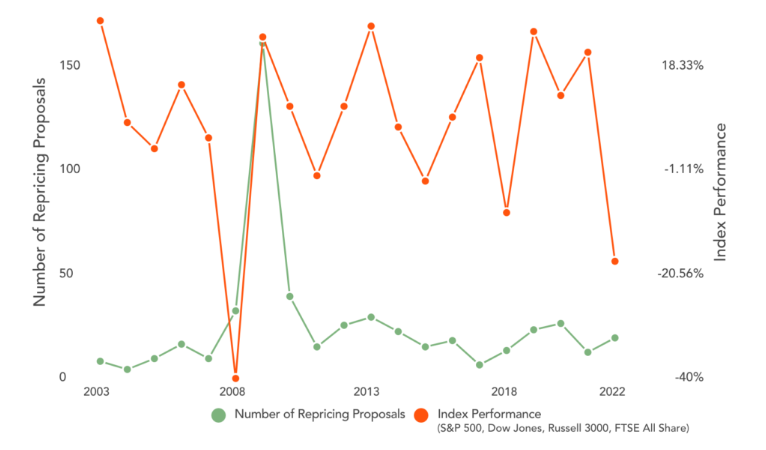

Whether a company feels compelled to re-price depends a lot on the timing of its equity granting cycle. As such, it doesn’t take a protracted global financial crisis to prompt a repricing proposal. Any volatility (see COVID-19, war in Ukraine, inflation and monetary policy or simply poor performance leading to stock price decline) may push a board to act in the name of retention. But if history is a guide, a market-wide downturn certainly helps. The last time companies faced sustained macro headwinds, during the global financial crisis, the number of repricing proposals surged as companies found their option-based incentive programs “out of the money”.

Another thing to keep in mind: repricing is generally a North American phenomenon. The overwhelming majority of the small number of repricing proposals we observed in 2022 were in the United States and Canada. Moreover, some U.S. boards can approve a repricing of options without shareholder approval, provided the equity compensation plan governing the awards to be repriced permits it.

Why Do Companies Reprice Options?

Some would argue that for a company facing a macro downturn, repricing represents the “least bad” option for keeping employees incentivized, particularly when it is conducted on a net neutral, fair value basis. When retention is crucial, a misalignment of employee and shareholder experience may be less of a concern than watching talent cross the street to take new sign-on awards from a competitor. As smaller companies are behind the bulk of repricing action, this may be a story of David versus Goliath in the highly competitive market for talent.

But the optics of bailing out well-paid executives obviously aren’t great – particularly when the economy is down, shareholders out of pocket and employees laid off – so public companies need to be thoughtful about how they are going to do this, if at all.

What it May Mean for Proxy Season 2023

The spring of 2022 already saw the start of a decline from the market’s 2021 peaks, due to a convergence of macroeconomic shocks and rising inflation and interest rates. However, last year’s shareholder voting results (and voting agenda) were on a lag — due to the retrospective nature of typical “say-on-pay” votes, in most cases shareholders were expressing an opinion on pay for surging 2021 performance.

In 2023, investors will generally be looking back on the first protracted downturn in a decade. In some cases, repricing may be one of the factors they will need to consider – whether voting directly on a repricing proposal, or in considering say on pay votes (or even the re-election of specific directors) where boards with the requisite authority unilaterally repriced or exchanged options in 2022.