Print

PrintEdna Twumwaa Frimpong is the Head of International Research at Diligent Institute. This post is based on her Diligent memorandum. Related research from the Program on Corporate Governance includes The Myth of the Shareholder Franchise (discussed on the Forum here) by Lucian A. Bebchuk; and Universal Proxies (discussed on the Forum here) by Scott Hirst.

“Proxy advisors Glass Lewis and ISS appear to be taking opposing sides when it comes to issuing recommendations on directors.”

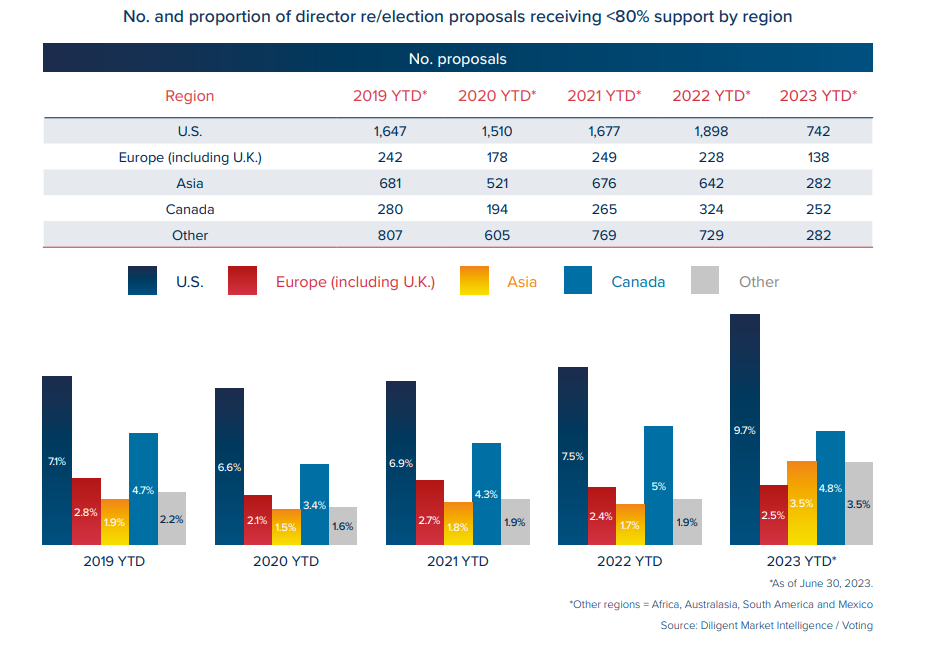

Proxy season offers shareholders essential vision into how companies are reacting to various risks and opportunities, which often results in issuers being confronted with tough questions from key stakeholders, an issue that has likely become more common, given the current unstable business environment. The first half of 2023 demonstrated that a growing portion of investors are opposing directors on a global scale, and there are a variety of reasons why this is the case.

According to Diligent Market Intelligence (DMI) data, there is a growing level of dissent against director re/elections. and there are a variety of reasons why this is so. Usually, shareholders opt to vote against director re/elections to flag their dissatisfaction with governance issues, ESG shortcomings and the broader strategic direction of a company.

The stakes are high and director re/elections are becoming a popular tool with which investors can send a clear message that they expect better from a company. In the first half of 2023, support for global director re/elections has declined to 95.6%, compared to 96.4% and 96.1% throughout 2021 and 2022, respectively.

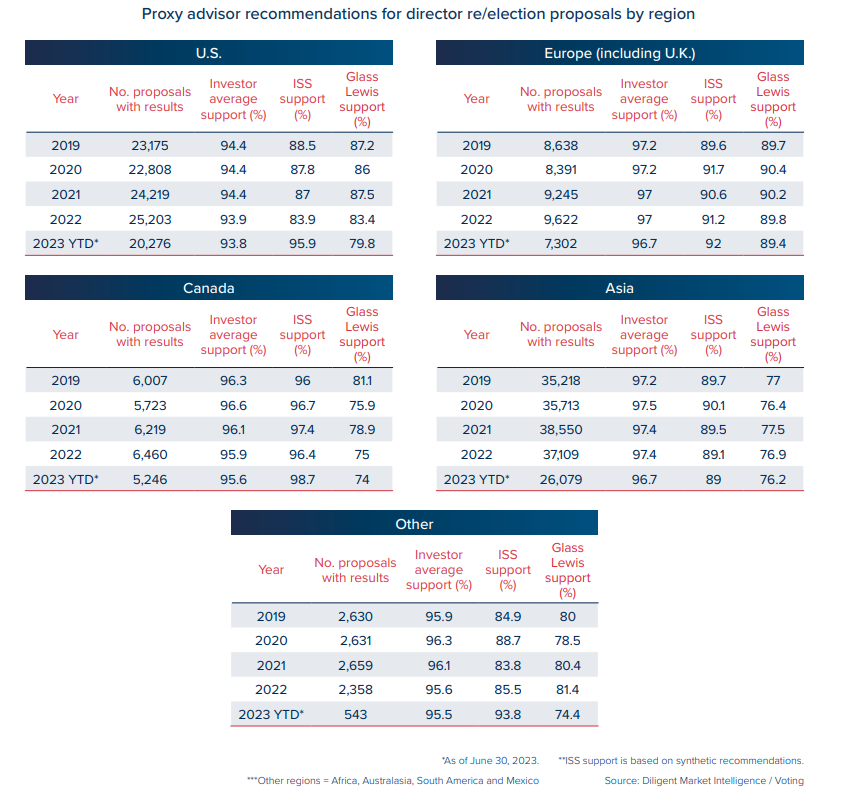

Proxy advisors Glass Lewis and Institutional Shareholder Services (ISS) also appear to be taking opposing sides when it comes to issuing recommendations on directors. Globally, Glass Lewis has endorsed just 77.9% of director re/election proposals in the first half of the year, compared to 79% in 2022. ISS’ support, however, has increased to 95.1%, up from 86.3% in 2022.

Regional nuances

When comparing data from the largest indices in the U.S. and U.K., support for directors is holding relatively steady, with support for U.K. directors somewhat higher than their American counterparts.

In the first half of 2023, FTSE 350 director re/elections have won 97.5% support, down from 97.7% throughout 2022. 2023 marks the first time in five years where FTSE 350 directors have failed to receive majority support, with five (0.3%) director proposals failing. Average support for S&P 500 directors is lower, at 95.9%, up from 95.7% a year prior. Despite this, only three (0.1%) of S&P 500 director election proposals have failed so far this year.

Again, the role of proxy advisory firms in director election votes cannot be overlooked. Both advisors have been more critical of S&P 500 directors, with Glass Lewis and ISS endorsing 93.4% and 97.1% of director re/election proposals, respectively, compared to 98.7% and 99% of FTSE 350 director re/election proposals in the same period.

CEO compensation is likely a determining factor behind the rise in proxy advisor opposition towards S&P 500 directors, with average CEO total realized pay reaching $78 million in 2021, a 174% increase on 2020’s $28 million.

Across Europe, investor support for director re/elections has averaged 96.7% in the first half of 2023, while advisor support has increased by approximately two percentage points compared to 2022 levels. Asia is a somewhat different story. Average investor support has declined to 96.6%, compared to 97.4% throughout 2022, while both ISS and Glass Lewis support dropped by approximately two percentage points each, compared to 2022.

Skillsets and gender diversity

Analyzing more than 110,000 global directors in 7,266 publicly listed companies from DMI, only 0.8% and 9% of directors, respectively, have sustainability and technology specialist backgrounds, skills which are becoming increasingly critical for addressing today’s business operations and stakeholders’ needs.

Again, advisors are becoming conscious of the increasing need for ESG and technology knowledge on boards. For the first time in 2023, Glass Lewis updated its policy to note that it would “closely evaluate” U.S.- and Canada-listed company disclosure in instances where cyber-attacks have caused “significant harm to shareholders” and may recommend against appropriate directors, should it find such disclosure to be insufficient.

DMI data also suggest that female directors formed approximately 38% of global director appointments in the past year. As of the end of June, 22.4% and 54% of S&P 500 and FTSE 350 boards feature a minimum of 40% female representation, respectively.

Starting in 2023, Glass Lewis completed its phased transition from a fixed numerical approach to a percentage-based approach for board gender diversity, recommending votes against Russell 3000 nominating committee chairs for boards featuring less than 30% gender diversity.