Print

PrintLarry Fink is Founder, Chairman and CEO of BlackRock Inc. This post is based on Mr. Fink’s annual letter to investors.

Time to rethink retirement

When my mom passed away in 2012, my dad started to decline quickly, and my brother and I had to go through my parents’ bills and finances.

Both my mom and dad worked great jobs for 50 years, but they were never in the top tax bracket. My mom taught English at the local state college (Cal Northridge), and my dad owned a shoe store.

I don’t know exactly how much they made every year, but in today’s dollars, it was probably not more than $150,000 as a couple. So, my brother and I were surprised when we saw the size of our parents’ retirement savings. It was an order of magnitude bigger than you’d expect for a couple making their income. And when we finished going over their estate, we learned why: My parents’ investments.

My dad had always been an enthusiastic investor. He encouraged me to buy my first stock (the DuPont chemical company) as a teenager. My dad invested because he knew that whatever money he put in the bond or stock markets would likely grow faster than in the bank. And he was right.

I went back and did the math. If my parents had $1,000 to invest in 1960, and they put that money in the S&P 500, then by the time they’d reached retirement age in 1990, the $1,000 would be worth nearly $20,000.[1] That’s more than double what they would have earned if they’d just put the money in a bank account. My dad passed away a few months after my mom, in his late 80s. But both my parents could have lived beyond 100 and comfortably afforded it.

Why am I writing about my parents? Because going over their finances showed me something about my own career in finance. I had been working at BlackRock for almost 25 years by the time I lost my mom and dad, but the experience reminded me — in a new and very personal way — why my business partners and I founded BlackRock in the first place.

Obviously, we were ambitious entrepreneurs, and we wanted to build a big, successful company. But we also wanted to help people retire like my parents did. That’s why we started an asset manager — a company that helps people invest in the capital markets — because we believed participating in those markets was going to be crucial for people who wanted to retire comfortably and financially secure.

We also believed the capital markets would become a bigger and bigger part of the global economy. If more people could invest in the capital markets, it would create a virtuous economic cycle, fueling growth for companies and countries, which would, in turn, generate wealth for millions more people.

My parents lived their final years with dignity and financial freedom. Most people don’t have that chance. But they can. The same kinds of markets that helped my parents in their time can help others in our time. Indeed, I think the growth- and prosperity-generating power of the capital markets will remain a dominant economic trend through the rest of the 21st Century.

This letter attempts to explain why.

A brief (and admittedly incomplete) history of U.S. capital markets

In finance, there are two basic ways to get or grow money.

One is the bank, which is what most people historically relied on. They deposited their savings to earn interest or took out loans to buy a home or expand their business. But over time a second avenue for financing arose, particularly in the U.S., with the growth of the capital markets: publicly traded stocks, bonds, and other securities.

I saw this firsthand in the late 1970s and early 1980s when I played a role in the creation of the securitization market for mortgages.

Before the 1970s, most people secured financing for their homes the same way they did in the Christmas classic It’s a Wonderful Life — through the Building & Loan (B&L). Customers deposited their savings into the B&L, which was essentially a bank. Then that bank would turn around and lend out those savings in the form of mortgages.

In the movie — and in real life — everything works fine until people start lining up at the bank’s front door asking for their deposits back. As Jimmy Stewart explained in the film, the bank didn’t have their money. It was tied up in somebody else’s house.

After the Great Depression, B&Ls morphed into savings & loans (S&Ls), which had their own crisis in the 1980s. Approximately half of the outstanding home mortgages in the U.S. were held by S&Ls in 1980, and poor risk management and loose lending practices led to a raft of failures costing U.S. taxpayers more than $100 billion dollars.[2]

But the S&L crisis didn’t cause the American economy lasting damage. Why? Because at the same time the S&Ls were collapsing another method of financing was getting stronger. The capital markets were providing an avenue to channel capital back to challenged real estate markets.

This was mortgage securitization.

Securitization allowed banks not just to make mortgages but to sell them. By selling mortgages, banks could better manage risk on their balance sheets and have capital to lend to home buyers, which is why the S&L crisis didn’t severely impact American homeownership.

Eventually, the excesses of mortgage securitization contributed to the crash in 2008, and unlike the S&L crisis, the Great Recession did harm home ownership in the U.S. The country still hasn’t fully recovered in that respect. But the broader underlying trend — the expansion of the capital markets — was still very helpful for the American economy.

In fact, it’s worth considering: Why did the U.S. rebound from 2008 faster than almost any other developed nation?[3]

A big part of the answer is the country’s capital markets.

In Europe, where most assets were kept in banks, economies froze as banks were forced to shrink their balance sheets. Of course, U.S. banks had to tighten capital standards and pull back from lending as well. But because the U.S. had a more robust secondary pool of money – the capital markets — the nation was able to recover much more quickly.

Today public equities and bonds provide over 70% of financing for non-financial corporations in the U.S. – more than any other country in the world. In China, for example, the bank-to-capital market ratio is almost flipped. Chinese companies rely on bank loans for 65% of their financing.[4]

In my opinion, this is the most important lesson in recent economic history: Countries aiming for prosperity don’t just need strong banking systems — they also need strong capital markets.

That lesson is now spreading around the world.

Replicating the success of America’s capital markets

Last year, I spent a lot of days on the road, logging visits to 17 different countries. I met with clients and employees. I also met with many policymakers and heads of state, and during those meetings, the most frequent conversation I had was about the capital markets.

More and more countries recognize the power of American capital markets and want to build their own.

Of course, many countries do have capital markets already. There are something like 80 stock exchanges around the world, everywhere from Kuala Lumpur to Johannesburg.[5] But most of these are rather small, with little investment. They’re not as robust as the markets in the U.S., and that’s what other nations are increasingly looking for.

In Saudi Arabia, for example, the government is interested in building a market for mortgage securitization, while Japan and India want to give people new places to put their savings. Today, in Japan, it’s mostly the bank. In India, it’s often in gold.

When I visited India in November, I met policymakers who lamented their fellow citizens’ fondness for gold. The commodity has underperformed the Indian stock market, proving a subpar investment for individual investors. Nor has investing in gold helped the country’s economy.

Compare investing in gold with, let’s say, investing in a new house. When you buy a home, that creates an economic multiplier effect because you need to furnish and repair the house. Maybe you have a family and fill the house with children. All that generates economic activity. Even when someone puts their money in a bank, there’s a multiplier effect because the bank can use that money to fund a mortgage. But gold? It just sits in a safe. It can be a good store of value, but gold doesn’t generate economic growth.

This is a small illustration — but a good one — of what countries want to accomplish with robust capital markets. (Or rather, of what they can’t accomplish without them.)

Despite the anti-capitalist strain in our modern politics, most world leaders still see the obvious: No other force can lift more people from poverty or improve quality of life quite like capitalism. No other economic model can help us achieve our highest hopes for financial freedom — whether we want it for ourselves or our country.

That’s why the capital markets will be key to addressing two of the mid-21st Century’s biggest economic challenges.

- The first is providing people what my parents built over time — a secure, well-earned retirement. This is a much harder proposition than it was 30 years ago. And it’ll be a much harder proposition 30 years from now. People are living longer lives. They’ll need more money. The capital markets can provide it — so long as governments and companies help people invest.

- A second challenge is infrastructure. How are we going to build the massive amount the world needs? As countries decarbonize and digitize their economies, they’re supercharging demand for all sorts of infrastructure, from telecom networks to new ways to generate power. In fact, in my nearly 50 years in finance, I’ve never seen more demand for energy infrastructure. And that’s because many countries have twin aims: They want to transition to lower-carbon sources of power while also achieving energy security. The capital markets can help countries meet their energy goals, including decarbonization, in an affordable way.

Asking the old age question: How do we afford longer lives?

Last year, Japan passed a demographic milestone. The country’s population has been aging since the early 1990s, as the pool of working-age people has shrunk and the number of elderly has risen. But 2023 was the first time that 10% of their people exceeded 80 years old,[6] making Japan the “oldest country in the world” according to the United Nations.[7]

This is part of the reason the Japanese government is making a push for retirement investment.

Most Japanese keep the bulk of their retirement savings in banks, earning a low interest rate. It wasn’t such a bad strategy when Japan was suffering from deflation, but now the country’s economy has turned around, with the NIKKEI surging past 40,000 for the first time this month (March 2024).[8]

Most aspiring retirees are missing out on the upswing. The country didn’t have anything resembling a 401(k) program until 2001, but even then, the amount of income people could contribute was quite low. So a decade ago, the government launched the Nippon Individual Savings Accounts (NISA) to encourage people to invest even more in retirement. Now they’re trying to double NISA’s enrollment. The goal is 34 million Japanese investors before the end of the decade.[9] It will require the Japanese government to expand their capital markets, which historically had very little retail participation.

Japan isn’t alone in helping more of its citizens invest for retirement. BlackRock has a joint venture — Jio BlackRock — with Jio Financial Services, an affiliate of India’s Reliance Industries. Over the past 10 years, India has built a huge digital public infrastructure network that connects nearly one billion Indians to everything from healthcare to government payments via their smartphones. Jio BlackRock’s goal is to use the same infrastructure to deliver retirement investing (and more).

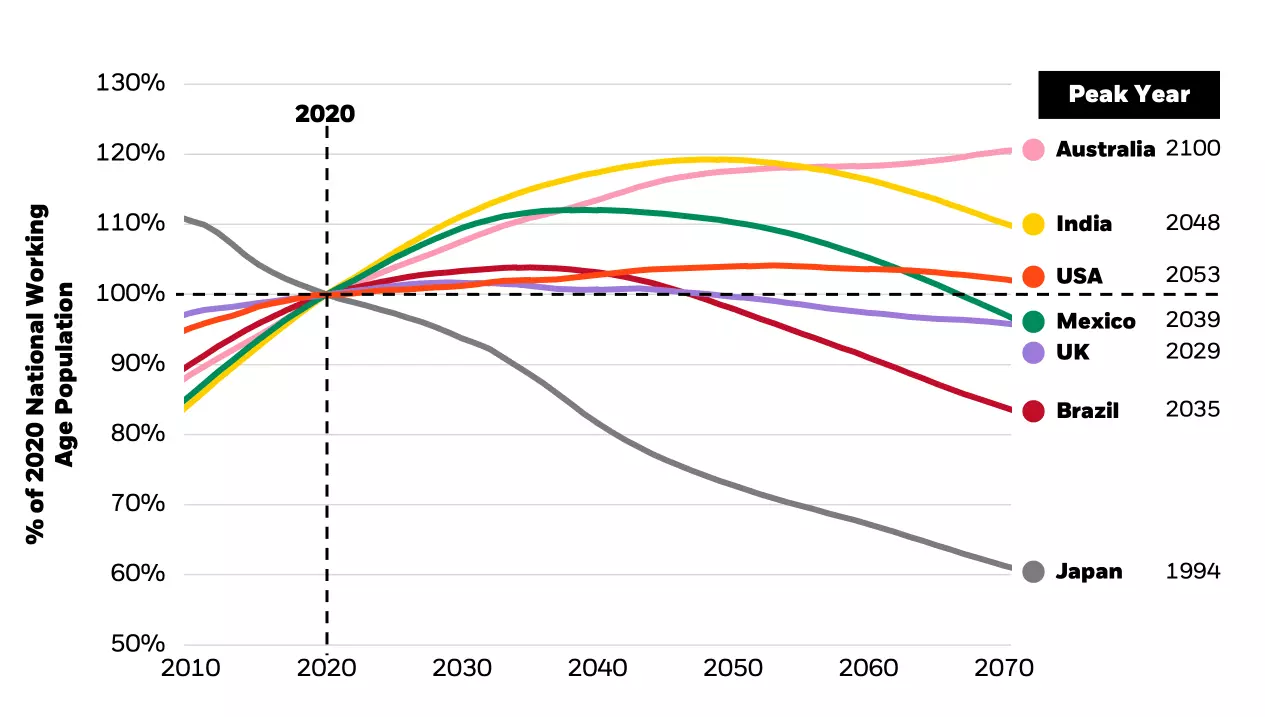

After all, India is aging, too. The whole world is, albeit at different speeds. Brazil will start seeing more people leave its workforce than enter it by 2035; Mexico will reach peak workforce by 2040; India sometime around 2050.

As populations age, building retirement savings has never been more urgent

Working-age population (ages 15-64): UN “medium trend[10]

Working-age population (ages 15-64): UN “medium trend[10]

By the mid-century mark, one-in-six people globally will be over the age of 65, up from one-in-11 in 2019.[11] To support them, governments are going to have to prioritize building out robust capital markets like the U.S. has.

But this isn’t to say the U.S. retirement system is perfect. I’m not sure anybody believes that. The retirement system in America needs modernizing, at the very least.

Rethinking retirement in the United States

This was particularly clear last year as the biotech industry pumped out a rush of new, life-extending drugs. Obesity, for example, can take more than 10 years off someone’s life expectancy, which is why some researchers think that new pharmaceuticals like Ozempic and Wegovy can be life-extending drugs, not just weight-loss drugs.[12] In fact, a recent study shows that semaglutide, the generic name for Ozempic, can give people with cardiovascular disease an extra two years of life where they don’t suffer a major condition like a heart attack.[13]

These drugs are breakthroughs. But they underscore a frustrating irony: As a society, we focus a tremendous amount of energy on helping people live longer lives. But not even a fraction of that effort is spent helping people afford those extra years.

It wasn’t always this way. One reason my parents had a financially secure retirement was CalPERS, California’s state pension system. As a public university employee, my mom could enroll. But pension enrollment has been declining across the country since the 1980s.[14] Meanwhile the federal government has prioritized maintaining entitlement benefits for people my age (I’m 71) even though it might mean that Social Security will struggle to meet its full obligations when younger workers retire.

It’s no wonder younger generations, Millennials and Gen Z, are so economically anxious. They believe my generation — the Baby Boomers — have focused on their own financial well-being to the detriment of who comes next. And in the case of retirement, they’re right.

Today in America, the retirement message that the government and companies tell their workers is effectively: “You’re on your own.” And before my generation fully disappears from positions of corporate and political leadership, we have an obligation to change that.

Maybe once a decade, the U.S. faces a problem so big and urgent that government and corporate leaders stop business as usual. They step out of their silos and sit around the same table to find a solution. I participated in something like this after 2008, when the government needed to find a way to unwind the toxic assets from the mortgage crisis. More recently, tech CEOs and the federal government came together to address the fragility of America’s semiconductor supply chain. We need to do something similar for the retirement crisis. America needs an organized, high-level effort to ensure that future generations can live out their final years with dignity.

What should that national effort do? I don’t have all the answers. But what I do have is some data and the beginnings of a few ideas from BlackRock’s work. Because our core business is retirement.

More than half the assets BlackRock manages are for retirement.[15] We help about 35 million Americans invest for life after work,[16] which amounts to about a quarter of the country’s workers.[17] Many are educators like my mom was. BlackRock helps manage pension assets for roughly half of U.S. public school teachers.[18] And this work — and our similar work around the globe — has given us some insight into how a national initiative to modernize retirement might begin.

We think the conversation starts by looking at the challenge through three different lenses.

- What’s the issue from the perspective of a current worker, someone who’s still trying to save for retirement?

- What about someone who has already retired? We have to look at the problem from the retiree’s point of view — an individual who has already saved enough to stop working but is worried the money will run out.

- But first it’s important to look at retirement in America like you’d look at a map of America — a high-level picture of the problem, the kind a national policymaker might look at. What’s the issue for the population as a whole? (It’s demographics.)

The demographics don’t lie

There’s a popular saying in economics: “You just can’t fight demographics.” And yet, when it comes to retirement, the U.S. is trying anyway.

In wealthy countries, most retirement systems have three pillars. One is what people invest personally (my dad putting his money in the stock market). Another is the plans provided by employers (my mom’s CalPERS pension). A third component is what we hear politicians mostly talking about – the government safety net. In the U.S., this is Social Security.

You’re probably familiar with the economics behind Social Security. During your working years, the government takes a portion of your income, then after you retire, it sends you a check every month. The idea actually originates from pre-World War I Germany, and these “old-age insurance” programs gradually became popular over the 20th Century largely because the demographics made sense.

Think about someone who was 65 years old in 1952, the year I was born. If he hadn’t retired already, that person was probably getting ready to stop working.

But now think about that person’s former colleagues, all the people around his age who he’d entered the workforce with back in the 1910s. The data shows that in 1952, most of those people were not preparing for retirement because they’d already passed away.

This is how the Social Security program functioned: More than half the people who worked and paid into the system never lived to retire and be paid from the system.[19]

Today, these demographics have completely unraveled, and this unraveling is obviously a wonderful thing. We should want more people to live more years. But we can’t overlook the massive impact on the country’s retirement system.

It’s not just that more people are retiring in America; it’s also that their retirements are increasing in length. Today, if you’re married and both you and your spouse are over the age of 65, there’s a 50/50 chance at least one of you will be receiving a Social Security check until you’re 90.[20]

All this is putting the U.S. retirement system under immense strain. The Social Security Administration itself says that by 2034, it won’t be able to pay people their full benefits.[21]

What’s the solution here? No one should have to work longer than they want to. But I do think it’s a bit crazy that our anchor idea for the right retirement age — 65 years old — originates from the time of the Ottoman Empire.

Humanity has changed over the past 120 years. So must our conception of retirement.

One nation that’s rethought retirement is the Netherlands. In order to keep their state pension affordable, the Dutch decided more than 10 years ago to gradually raise the retirement age. It will now automatically adjust as the country’s life expectancy changes.[22]

Obviously, implementing this policy elsewhere would be a massive political undertaking. But my point is that we should start having the conversation. When people are regularly living past 90, what should the average retirement age be?

Or rather than pushing back when people receive retirement benefits, perhaps there’s a more politically palatable idea: How do we encourage more people who wish to work longer, with carrots rather than sticks? What if the government and the private sector treated 60-plus year-olds as late-career workers with much to offer rather than people who should retire?

One way Japan has managed its aging economy is by doing exactly this. They’ve found new ways to boost the labor force participation rate, a metric that has been declining in the U.S. since the early 2000s.[23] It’s worth asking: How can America stop (or at least, slow) that trend?

Again, I’m not pretending to have the answers. Despite BlackRock’s success helping millions retire, these questions are going to have to be posed to a broader range of investors, retirees, policymakers, and others. Over the next few months, BlackRock will be announcing a series of partnerships and initiatives to do just that, and I invite you to join us.

For workers, make investing (almost) automatic

When the U.S. Census Bureau released its regular survey of consumer finances in 2022, nearly half of Americans aged 55 to 65 reported not having a single dollar saved in personal retirement accounts.[24] Nothing in a pension. Zero in an IRA or 401(k).

Why? Well, the first barrier to retirement investing is affordability.

Four-in-10 Americans don’t have $400 to spare to cover an emergency like a car repair or hospital visit.[25] Who is going to invest money for a retirement 30 years away if they don’t have cash for today? No one. That’s why BlackRock’s foundation has worked with a group of nonprofits to set up an Emergency Savings Initiative. The program has helped mostly low-income Americans put away a total of $2 billion in new liquid savings.[26]

Studies show that when people have emergency savings, they’re 70% more likely to invest for retirement.[27] But this is where workers run into another barrier: Investing is complex even if you can afford it.

No one is born a natural investor. It’s important to say that because sometimes in the financial services industry we imply the opposite. We make it seem like saving for retirement can be a simple task, something anyone can do with a bit of practice, like driving your car to work. Just grab your keys and hop in the driver’s seat. But financing retirement isn’t so intuitive. The better analogy is if someone dropped a bunch of engine and auto parts in your driveway and said, “Figure it out.”

At BlackRock, we’ve tried to make the investing process more intuitive by inventing simpler products like target date funds. They only require people to make one decision: What year do they expect to retire? Once people choose their “target date,” the fund automatically adjusts their portfolio, shifting from higher-return equities to less risky bonds as retirement approaches.[28]

In 2023, BlackRock expanded the types of target date ETFs we offer so people can more easily buy them even if they don’t work for employers offering a retirement plan. There are 57 million people like this in America — farmers, gig workers, restaurant employees, independent contractors — who don’t have access to a defined contribution plan.[29] And while better investment products can help, there are limits to what something like a target date fund can do. Indeed, for most people, the data shows that the hardest part of retirement investing is just getting started.

Other nations make things simpler for their part-time and contract workers. In Australia, employers must contribute a portion of income for every worker between the ages of 18 and 70 into a retirement account, which then belongs to the employee. The Superannuation Guarantee was introduced in 1992 when the country seemed like it was on the path to a retirement crisis. Thirty-two years later, Australians likely have more retirement savings per capita than any other country. The nation has the world’s 54th largest population,[30] but the 4th largest retirement system.[31]

Of course, every country is different, so every retirement system should be different. But Australia’s experience with Supers could be a good model for American policymakers to study and build on. Some already are. There are about 20 U.S. states — like Colorado and Virginia — that have instituted retirement systems to cover all workers like Australia does, even if they’re gig or part-time.[32]

It’s a good thing that legislators are proposing different bills and states are becoming “laboratories of retirement.” More should consider it. The benefits could be enormous for individual retirees. These new programs could also help the U.S. ensure the long-term solvency of Social Security. That’s what Australia found — their Superannuation Guarantee relieved the financial tension in their country’s public pension program.[33]

But what about workers who do have access to an employer retirement plan? They need support too.

Even among employees who have access to employer plans, 17% don’t enroll in them, and the hypothesis among retirement experts is this is not a conscious choice. People are just busy.

It sounds trivial, but even the hour or so it takes someone to look through their work email inbox for the correct link to their company’s retirement system, and then select the percentage of their income they want to contribute can be the unclearable hurdle. That’s why companies should make a conscious effort to look at what their default option is. Are people automatically enrolled in a plan or not? And how much are they auto-enrolled to contribute? Is it a minimum percentage of their income? Or the maximum?

In 2017, the University of Chicago economist Richard Thaler won the Nobel Prize, in part, for his pioneering work around “nudges” — small changes in policy that can have enormous impact in people’s financial lives. Auto-enrollment is one of them. Studies show that the simple step of making enrollment automatic increases retirement plan participation by nearly 50%.[34]

As a nation, we should do everything we can to make retirement investing more automatic for workers. And there are already bright spots. Next year, a new federal law will kick in, requiring employers that set up new 401(k) plans to auto-enroll their new workers. Plus, there are hundreds of major companies (including BlackRock) that have already taken this step voluntarily.

But firms can do even more to improve their employee’s financial lives, such as providing some level of matching funds for retirement plans and offering more financial education on the tremendous long-term difference between contributing a small percentage of your income to retirement versus the maximum. I also think we should make it easier for workers to transfer their 401(k) savings when they switch jobs. There is a menu of options here, and we need to explore all of them.

For retirees, help them spend what they saved

In 2018, BlackRock commissioned a study of 1,150 American retirees. When we dug into the data, we found something unexpected — even paradoxical.

The survey showed that after nearly two decades of retirement, the average person still had 80% of their pre-retirement money saved. We’re talking about people who were probably between the ages of 75 and 95. If they had invested for retirement, they were likely sitting on more than enough money for the rest of their lives. And yet the data also showed that they were anxious about their finances. Only 32% reported feeling comfortable about spending what they saved.[35]

This retirement paradox has a simple explanation: Even people who know how to save for retirement still don’t know how to spend for it.

In the U.S., this problem’s roots stretch back more than four decades when employers began switching from defined benefit plans — pensions — to defined contribution plans like 401(k)s.

In a lot of ways, pensions were much simpler than the 401(k). You had a job somewhere for 20 or 30 years. Then when you retired, your pension paid you a set amount — a defined benefit — every month.

When I entered the workforce in the 1970s, 38% of Americans had one of these defined benefit plans, but by 2008 the percentage had been cut almost in half.[36] Meanwhile, the fraction of Americans with defined contribution plans almost quadrupled.[37]

This should have been a good thing. Beginning with the Baby Boomers, fewer and fewer workers spent their entire careers in one place, meaning they needed a retirement option that would follow them from job to job. In theory, 401(k)s did that. But in practice? Not really.

Anyone who’s switched jobs knows how unintuitive it is to transfer your retirement savings. In fact, studies show that about 40% of employees cash out their 401(k)s when they switch jobs, putting themselves back at the starting line for retirement savings.[38]

The real drawback of defined contribution was that it removed most of the retirement responsibility from employers and put it squarely on the shoulders of the employees themselves. With pensions, companies had a very clear obligation to their workers. Their retirement money was a financial liability on the corporate balance sheet. Companies knew they’d have to write a check every month to each one of their retirees. But defined contribution plans ended that, forcing retirees to trade a steady stream of income for an impossible math problem.

Because most defined contribution accounts don’t come with instructions for how much you can take out every month, individual savers first must build up a nest-egg, then spend down at a rate that will last them the rest of their lives. But who really knows how long that will be?

Put simply, the shift from defined benefit to defined contribution has been, for most people, a shift from financial certainty to financial uncertainty.

That’s why around the same time we saw the data that retirees were nervous about spending their savings, we started wondering: Was there something we can do about it? Could we develop an investment strategy that provided the flexibility of a 401(k) investment but also the potential for a predictable, paycheck-like income stream, similar to a pension?

It turns out, we could. That strategy is called LifePath Paycheck™, which will go live in April. As I write this, 14 retirement plan sponsors are planning to make LifePath Paycheck™ available to 500,000 employees. I believe it will one day be the most used investment strategy in defined contribution plans.

We’re talking about a revolution in retirement. And while it may happen in the U.S. first, eventually other countries will benefit from the innovation as well. At least, that is my hope. Because while retirement is mainly a saving challenge, the data is clear: it’s a spending one too.

Fear vs. hope

Before I conclude this section on retirement, I want to share a few words about one of the largest barriers to investing for the future. In my view, it’s not just affordability or complexity or the fact that people are too busy to enroll in their employer’s plan.

Arguably the biggest barrier to investing for retirement — or for anything — is fear.

In finance, we sometimes think of “fear” as a fuzzy, emotional concept — not as a hard economic data point. But that’s what it is. Fear is as important and actionable a metric as GDP. After all, investment (or lack thereof) is just a measure of fear because no one lets their money sit in a stock or a bond for 30 or 40 years if they’re afraid the future is going to be worse than the present. That’s when they put their money in a bank. Or underneath the mattress.

This is what happens in many countries. In China, where new surveys show consumer confidence has dropped to its lowest level in decades, household savings have reached their highest level on record — nearly $20 trillion — according to the central bank.[39] China has a savings rate of about 30%. Nearly a third of all money earned is socked away in cash in case it’s needed for harder times ahead. The U.S., by comparison, has a savings rate in the single digits.[40]

America has rarely been a fearful country. Hope has been the nation’s greatest economic asset. People put their money in American markets for the same reason they invest in their homes and businesses — because they believe this country will be better tomorrow than it is today.

This big, hopeful America has been the one I’ve known my whole life, but over the past few years, especially as I’ve had more grandchildren, I’ve started to ask myself: Will they know this version of America, too?

As I was finishing this letter, The Wall Street Journal published an article that caught my attention. It was titled “The Rough Years that Turned Gen Z into America’s Most Disillusioned Voters,” and it included some eye-catching — and really disheartening — data.

The article showed that from the mid-1990s through most of the early 21st Century, most young people — around 60% of high school seniors, to be specific — believed they’d earn a professional degree, would land a good job, and go on to be wealthier than their parents. They were optimistic. But since the pandemic, that optimism has fallen precipitously.

Compared with 20 years ago, the current cohort of young Americans is 50% more likely to question whether life has a purpose. Four-in-10 say it’s “hard to have hope for the world.”[41]

I’ve been working in finance for almost 50 years. I’ve seen a lot of numbers. But no single data point has ever concerned me more than this one.

The lack of hope worries me as a CEO. It worries me as a grandfather. But most of all, it worries me as an American.

If future generations don’t feel hopeful about this country and their future in it, then the U.S. doesn’t only lose the force that makes people want to invest. America will lose what makes it America. Without hope, we risk becoming just another place where people look at the incentive structure before them and decide that the safe choice is the only choice. We risk becoming a country where people keep their money under the mattress and their dreams bottled up in their bedroom.

How do we get our hope back?

Whether we’re trying to solve retirement or any other problem, that is the first question we have to ask, although I readily admit that I do not have the solution. I look at the state of America — and the world — and I am as answerless as everyone else. There’s so much anger and division, and I often struggle to wrap my head around it.

What I do know is that any answer has to start by bringing young people into the fold. The same surveys that show their lack of hope also show their lack of confidence — far less than any previous generation — in every pillar of society: In politics, government, the media, and in corporations. Leaders of these institutions (I am one) should be empathetic to their concerns.

Young people have lost trust in older generations. The burden is on us to get it back. And maybe investing for their long-term goals, including retirement, isn’t such a bad place to begin.

Perhaps the best way to start building hope is by telling young people, “You may not feel very hopeful about your future. But we do. And we’re going to help you invest in it.”

The new infrastructure blueprint: steel, concrete, and public-private partnership

I started traveling to London in the 1980s, and back then, if you had a choice between the city’s two major international airports — Heathrow or Gatwick — you probably chose Heathrow. Gatwick was farther from the city. It was also in a comparative state of disrepair.

But things changed in 2009 when Gatwick was purchased by Global Infrastructure Partners (GIP). They increased runway capacity and instituted commonsense changes, like oversized luggage trays that cut security screening times by more than half.

“The thing about infrastructure businesses… is a lot of them tend not to focus on customer service,” GIP’s CEO Bayo Ogunlesi told The Financial Times. GIP wanted to make Gatwick different. In the process, they also turned the airport into a prime example of how infrastructure will be built and run in the 21st century — with private capital.[42]

In the U.S., people tend to think of infrastructure as a government endeavor, something built with taxpayer funds. But because of one very big reason that I’ll dive into momentarily, that won’t be the primary way infrastructure is built in the mid-21st Century. Rather than only tapping government treasuries to build bridges, power grids, and airports, the world will do what Gatwick did.

The future of infrastructure is public-private partnership.

Debt matters

The $1 trillion infrastructure sector is one of the fastest growing segments of the private markets, and there are some undeniable macroeconomic trends driving this growth. In developing countries, people are getting richer, boosting demand for everything from energy to transportation while in wealthy countries, governments need to both build new infrastructure and repair the old.

Even in the U.S., where the Biden Administration has signed generational infrastructure investments into law, there’s still $2 trillion worth of deferred maintenance.[43]

How will we pay for all this infrastructure? The reason I believe it’ll have to be some combination of public and private dollars is that funding probably cannot come from the government alone. The debt is just too high.

From Italy to South Africa, many nations are suffering the highest debt burdens in their history. Public debt has tripled since the mid-1970s, reaching 92% of global GDP in 2022.[44] And in America, the situation is more urgent than I can ever remember. Since the start of the pandemic, the U.S. has issued roughly $11.1 trillion of new debt, and the amount is only part of the issue.[45] There’s also the interest rate the Treasury needs to pay on it.

Three years ago, the rate on a 10-year Treasury bill was under 1%. But as I write this, it’s over 4%, and that 3-percentage-point increase is very dangerous. Should the current rates hold, it amounts to an extra trillion dollars in interest payments over the next decade.[46]

Why is this debt a problem now? Because historically, America has paid for old debt by issuing new debt in the form of Treasury securities. It’s a workable strategy so long as people want to buy those securities — but going forward, the U.S. cannot take for granted that investors will want to buy them in such volume or at the premium they currently do.

Today, around 30% of U.S. Treasury securities are held by foreign governments or investors. That percentage will likely go down as more countries build their own capital markets and invest domestically.[47]

More leaders should pay attention to America’s snowballing debt. There’s a bad scenario where the American economy starts looking like Japan’s in the late 1990s and early 2000s, when debt exceeded GDP and led to periods of austerity and stagnation. A high-debt America would also be one where it’s much harder to fight inflation since monetary policymakers could not raise rates without dramatically adding to an already unsustainable debt-servicing bill.

But is a debt crisis inevitable? No.

While fiscal discipline can help tame debt on the margins, it will be very difficult (both politically and mathematically) to raise taxes or cut spending at the level America would need to dramatically reduce the debt. But there is another way out beyond taxing or cutting, and that’s growth. If U.S. GDP grows at an average of 3% (in real, not nominal terms) over the next five years, that would keep the country’s debt-to-GDP ratio at 120% – high, but reasonable.

I should be clear: 3% growth is a very tall order, especially given the country’s aging workforce. It will require policymakers to shift their focus. We can’t see debt as a problem that can be solved only through taxing and spending cuts anymore. Instead, America’s debt efforts have to center around pro-growth policies, which include tapping the capital markets to build one of the best catalysts for growth: Infrastructure. Especially energy infrastructure.

Energy pragmatism

Roads. Bridges. Ports. Airports. Cell towers. The infrastructure sector contains multitudes, but the multitude where BlackRock sees arguably the greatest demand for new investment is energy infrastructure.

Why energy? Two things are happening in the sector at the same time.

The first is the “energy transition.” It’s a mega force, a major economic trend being driven by nations representing 90% of the world’s GDP.[48] With wind and solar power now cheaper in many places than fossil-fuel-generated electricity, these countries are increasingly installing renewables.[49] It’s also a major way to address climate change. This shift – or energy transition – has created a ripple effect in the markets, creating both risks and opportunities for investors, including BlackRock’s clients.

I started writing about the transition in 2020. Since then, the issue has become more contentious in the U.S. But outside the debate, much is still the same. People are still investing heavily in decarbonization. In Europe, for example, net-zero remains a top investment priority for most of BlackRock’s clients.[50] But now the demand for clean energy is being amplified by something else: A focus on energy security.

Governments have been pursuing energy security since the oil crisis of the 1970s, (and probably as far back as the early Industrial Revolution), so this is not a new trend. In fact, when I wrote my original 2020 letter about sustainability, I also wrote to our clients that countries would still need to produce oil and gas to meet their energy needs.

To be energy secure, I wrote, most parts of the globe would need “to rely on hydrocarbons for a number of years.”[51]

Then in 2022, Putin invaded Ukraine. The war lit a fresh spark under the idea of energy security. It disrupted the world’s supply of oil and gas causing massive energy inflation, particularly in Europe. The UK, Norway, and the 27 EU countries had to collectively spend 800 billion euros subsidizing energy bills.[52]

This is part of the reason I’m hearing more leaders talk about decarbonization and energy security together under the joint banner of what you might call “energy pragmatism.”

Last year, as I mentioned, I visited 17 countries, and I spent a lot of time talking to the people who are responsible for powering homes and businesses, everybody from prime ministers to energy grid operators. The message I heard was completely opposite to what you often hear from activists on the far left and right, who say that countries have to choose between renewables and oil and gas. These leaders believe that the world still needs both. They were far more pragmatic about energy than dogmatic. Even the most climate conscious among them saw that their long-term path to decarbonization will include hydrocarbons, albeit it less of them, for some time to come.

Germany is a good example of how energy pragmatism is still a path to decarbonization. It’s one of the countries most committed to fighting climate change and has made enormous investments in wind and solar power. But sometimes the wind doesn’t blow in Berlin, and the sun doesn’t shine in Munich. And during those windless, sunless periods, the country still needs to rely on natural gas for “dispatchable power.” Germany used to get that gas from Russia, but now it needs to look elsewhere. So, they’re building additional gas facilities to import from other producers around the world.[53]

Or look at Texas. They face a similar energy challenge – not because of Russia but because of the economy. The state is one of the fastest growing in the U.S.,[54] and the additional demand for power is stretching ERCOT, Texas’ energy grid, to the limit.[55]

Today, Texas runs on 28% renewable energy[56] – 6% more than the U.S. as a whole.[57] But without an additional 10 gigawatts of dispatchable power, which might need to come partially from natural gas, the state could continue to suffer devastating brownouts. In February, BlackRock helped convene a summit of investors and policymakers in Houston to help find a solution.

Texas and Germany are great illustrations of what the energy transition looks like. As I wrote in 2020, the transition will only succeed if it’s “fair.” Nobody will support decarbonization if it means giving up heating their home in the winter or cooling it in the summer. Or if the cost of doing so is prohibitive.

Since 2020, economists have popularized better language to describe what a fair transition actually means. One important concept is the “green premium.” It’s the surcharge people pay for “going green”: for example, switching from a car that runs on gas to an electric vehicle. The lower the green premium, the fairer decarbonization will be because it’ll be more affordable.

This is where the power of the capital markets can be unleashed to great effect. Private investment can help energy companies reduce the cost of their innovations and scale them around the world. Last year, BlackRock invested in over a dozen of these transition projects on behalf of our clients. We partnered with developers in Southeast Asia aiming to build over a gigawatt of solar capacity (enough to power a city) in both Thailand and the Philippines.[58] We also invested in Lake Turkana Wind Power, Africa’s largest windfarm. It’s located in Kenya and currently accounts for about 12% of the country’s power generation.[59]

There are also earlier-stage technologies, like a giant “hot rock” battery being built by Antora Energy. The company heats up blocks of carbon with wind or solar power during parts of the day when renewable energy is cheap and abundant. These “thermal batteries” reach up to 2,400 degrees Celsius and glow brighter than the sun.[60] Then, that heat is used to power giant industrial facilities around-the-clock, even when the sun isn’t shining, or the wind isn’t blowing.

BlackRock invested in Antora through Decarbonization Partners, a partnership we have with the investment firm, Temasek. Our funding will help Antora scale up to deliver billions of dollars worth of zero-emission energy to industrial customers.[61] (One day, their thermal batteries might help solve the kind of dispatchable power problem that Texas and Germany are facing – but without carbon emissions.)

The final technology I’ll spotlight is carbon capture. Last year, one of BlackRock’s infrastructure funds invested $550 million in a project called STRATOS, which will be the world’s largest direct air capture facility when construction is completed in 2025.[62] Among the more interesting aspects of the project is who’s building the facility: Occidental Petroleum, the big Texas oil company.

The energy market isn’t divided the way some people think, with a hard split between oil & gas producers on one side and new clean power and climate tech firms on the other. Many companies, like Occidental, do both, which is a major reason BlackRock has never supported divesting from traditional energy firms. They’re pioneers of decarbonization, too.

Today, BlackRock has more than $300 billion invested in traditional energy firms on behalf of our clients. Of that $300 billion, more than half – $170 billion – is in the U.S.[63] We invest in these energy companies for one simple reason: It’s our clients’ money. If they want to invest in hydrocarbons, we give them every opportunity to do it – the same way we invest roughly $138 billion in energy transition strategies for our clients. That’s part of being an asset manager. We follow our clients’ mandates.

But when it comes to energy, I also understand why people have different preferences in the first place. Decarbonization and energy security are the two macroeconomic trends driving the demand for more energy infrastructure. Sometimes they’re competing trends. Other times, they’re complementary, like when the same advanced battery that decarbonizes your grid can also reduce your dependence on foreign power.

The point is: The energy transition is not proceeding in a straight line. As I’ve written many times before, it’s moving in different ways and at different paces in different parts of the world. At BlackRock, our job is to help our clients navigate the big shifts in the energy market no matter where they are.

BlackRock’s next transformation

One way we’re helping our clients navigate the booming infrastructure market is by transforming our company. I began this section by writing about the owners of Gatwick Airport, GIP. In January, BlackRock announced our plans to acquire them.

Why GIP? BlackRock’s own infrastructure business had been growing rapidly over the past several years. But to meet demand, we realized we needed to grow even faster.

It’s not just debt-strapped governments that need to find alternate pools of financing for their infrastructure. Private sector firms do too. All over the world, there’s a vast infrastructure footprint that’s owned and operated entirely by private companies. Cell towers are a good example. So are pipelines that deliver the feedstocks for chemical companies. Increasingly, the owners of these assets prefer to have a financing partner, rather than carrying the full cost for the infrastructure on their balance sheet.

I had been thinking about this trend and called an old colleague, Bayo Ogunlesi.

Both Bayo and I started our careers in finance at the investment bank First Boston. But our paths diverged. I lost $100 million on a series of bad trades at First Boston and…well, nobody needs to hear that story again. But it led me (and my BlackRock partners) to pioneer better risk management for fixed income markets. Meanwhile, Bayo and his team were pioneering modern infrastructure investing in the private markets.

Now, we plan to join our forces again. I think the result will be better opportunities for our clients to invest in the infrastructure that keeps our lights on, planes flying, trains moving, and our cell service at the maximum number of bars.

More about BlackRock’s work in 2023

In this letter, I’ve shared my view that the capital markets are going to play an even bigger role in the global economy. They’ll have to if the world wants to address the challenges around infrastructure, debt, and retirement. These are the major economic issues of the mid-21st Century. We’re going to need the power of capitalism to solve them.

The way BlackRock figures into that story is through our work with clients. We want to position them well to navigate these trends, which is why we’ve tried to stay more connected to our clients than ever.

Over the past five years, thousands of clients on behalf of millions of individuals have entrusted BlackRock with managing over $1.9 trillion in net new assets. Thousands also use our technology to better understand the risks in their portfolios and support the growth and commercial agility of their own businesses. Years of organic growth, alongside the long-term growth of the capital markets, underpin our $10 trillion of client assets, which grew by over $1.4 trillion in 2023.

In good times and bad, whether clients are focused on increasing or decreasing risk, our consistent industry-leading organic growth demonstrates that clients are consolidating more of their portfolios with BlackRock. In 2023, our clients awarded us with $289 billion in net new assets during a period of rapid change and significant portfolio de-risking.

BlackRock’s differentiated business model has enabled us to continue to grow with our clients and maintain positive organic base fee growth. We’ve grown regardless of the market backdrop and even as most of the industry experienced outflows.

I think back to 2016 and 2018 when uncertainty and cautious sentiment impacted investment behavior among institutions and individuals. Many clients de-risked and moved to cash. BlackRock stayed connected with our clients. We stayed rigorous in driving investment performance, innovating new products and technologies, and providing advice on portfolio design. Once clients were ready to step back into the markets more actively, they did it with BlackRock – leading to new records for client flows, and organic base fee growth at or above our target.

Flows and organic base fee growth accelerated into the end of 2023. We saw $96 billion of total net inflows in the fourth quarter and we entered 2024 with great momentum.

In 2024, I plan to do what I did in 2023 – spend a lot of time on the road visiting clients. I’ve already taken several trips in the U.S. and around the world, and it’s clearer than ever that companies and clients want to work with BlackRock.

For companies where we are investing on behalf of our clients, they appreciate that we typically provide long-term, consistent capital. We often invest early, and we stay invested through cycles whether it’s debt or equity, pre-IPO or post-IPO. Companies recognize BlackRock’s global relationships, brand, and expertise across markets and industries. This makes us a valuable partner, and in turn supports the sourcing and performance we can provide for clients.

Over the past 18 months, we’ve sourced and executed on a number of deals for clients. In addition to the STRATOS direct air capture project, our funds partnered with AT&T on the Gigapower JV to build out broadband in communities across the U.S. We also made investments globally, including in Brasol (Brazil), AirFirst (South Korea), Akaysha Energy (Australia), and the Lake Turkana Wind Farm (Kenya).

Our ability to source deals for clients is a primary driver of demand for BlackRock private markets strategies. These strategies saw $14 billion of net inflows in 2023, driven by infrastructure and private credit. We continue to expect these categories to be our primary growth drivers within alternatives in the coming years.

Our active investment insights, expertise and strong investment performance similarly differentiate BlackRock in the market. We saw nearly $60 billion of active net inflows in 2023, compared with industry outflows.

In ETFs, BlackRock generated an industry-leading $186 billion of net inflows in 2023. Our leadership in the ETF industry is another testament to our global platform and connectivity with clients.

What we have seen in market after market is that if we can make investing easier and more affordable, we can quickly attract new clients. We are leveraging digital wealth platforms in local markets to provide more investment access and accelerate organic growth for iShares ETFs.

In EMEA, BlackRock powers ETF savings plans for end investors, partnering with many banks and brokerage platforms, including Trade Republic, Scalable Capital, ING, Lloyds, and Nordnet. These partnerships will help millions of people access investments, invest for the long-term, and achieve financial well-being.

In 2023, we also announced our minority investment in Upvest, which will help drive innovation in how Europeans access markets and make it cheaper and simpler to start investing.

Then there is our work with Britain’s leading digital bank, Monzo, to offer its customers our products through its app, with minimum investments as low as £1. Through these relationships, we’re evolving our iShares ETF franchise to meaningfully increase access to global markets.

Let me also say a few words about Aladdin. It remains the language of portfolios, uniting all of BlackRock, and providing the technological foundation for how we serve clients across our platform. And Aladdin isn’t just the key technology that powers BlackRock; it also powers many of our clients. The need for integrated data and risk analytics as well as whole portfolio views across public and private markets is driving annual contract value (ACV) growth.

In 2023, we generated $1.5 billion in technology services revenue. Clients are looking to grow and expand with Aladdin, reflected in strong harvesting activity, with over 50% of Aladdin sales being multi-product.

As we look ahead, the re-risking of client portfolios will create tremendous prospects for both our public and private markets franchises. And integrated technology will be needed to help clients be nimble while operating at scale.

These are the times where investors are making broad changes to the way they build portfolios. BlackRock is helping investors build the “portfolio of the future” – one that integrates public and private markets and is digitally enabled. We view these changes as big catalysts. With the diversified investment and technology platform we’ve built, we’ve set ourselves up to be a structural grower in the years ahead.

Positioning our organization for the future

Just as we continually innovate and evolve our business to stay ahead of our clients, we also evolve our organization and our leadership team.

Earlier this year we announced changes to reimagine our business and transform our organization to better anticipate what clients need – and shape BlackRock so clients can continue to get the insights, solutions, and outcomes they expect from us.

For years, BlackRock has worked with clients across the whole portfolio, albeit with distinctions between product structures for ETFs, active mutual funds, and separate accounts.

Now, the traditional lines between products are blurring. Clients are building portfolios that seamlessly combine both active and index strategies, including liquid and illiquid assets and spanning public and private markets, across ETF, mutual fund, and separate account structures.

BlackRock has been critical in expanding the market for ETFs by making them accessible to more investors and delivering new asset classes (like bonds) and investment strategies (like active). As a result of that success, the ETF is no longer just an indexing concept – it is becoming an efficient structure for a range of investment solutions.

We always viewed ETFs as a technology, a technology that facilitated investing. And just as our Aladdin technology has become core to asset management, so too have ETFs. That’s why we believe embedding our ETF and Index expertise across the entire firm will accelerate the growth of iShares and every investment strategy at BlackRock.

We’ll be nimbler and more closely aligned with clients through our new architecture with the aim of delivering a better experience, better performance, and better outcomes.

Voting choice

Healthy capital markets depend on a continuous feedback loop between companies and their investors. For more than a decade, BlackRock endeavored to improve that feedback loop for our clients.

We’ve done it by building an industry-leading stewardship program, one that’s focused on engaging investee companies on issues impacting our clients’ long-term economic interests. This requires understanding how companies are positioned to navigate the risks and opportunities they face – for example, how geopolitical fragmentation might rewire their supply chains or how higher borrowing cost might impact their capacity to deliver sustained earnings growth.

To do that, we built one of the largest stewardship teams to engage with companies, often alongside our investment teams, because we never believed in the industry’s reliance on the recommendations of a few proxy advisors. We knew our clients would expect us to make independent proxy voting decisions, informed by our ongoing dialogue with companies – a philosophy that continues to underpin our stewardship efforts today. For our clients who have entrusted us with this important responsibility, we remain steadfast in promoting sound corporate governance practices and financial resilience at investee companies on their behalf.

And for our clients who wish to take a more direct role in the proxy voting process, we continue to innovate to provide them with more choice. In 2022, BlackRock was the first in our industry to launch Voting Choice, a capability that enabled institutional investors to participate in the proxy voting process. Today, about half of our clients’ index equity assets under management can access Voting Choice. And in February, we launched a pilot in our largest core S&P 500 ETF, enabling Voting Choice for individual investors for the first time.

We welcome these additional voices to corporate governance and believe they can further strengthen shareholder democracy. I believe that more asset owners can participate in this important process effectively if they are well-informed. We are encouraged by their engagement and the continued transformation of the proxy voting ecosystem but continue to believe that the industry would benefit from additional proxy advisors.

Strategy for long-term growth

For 36 years, BlackRock has led by listening to our clients and evolving to help them achieve long-term outcomes. That commitment has been behind everything we’ve done as a firm, whether it’s unlocking new markets through iShares, pioneering whole portfolio advisory, launching Aladdin on the desktops of investors and so much more. Clients have been at the foundation of our mindset and our growth strategy, informing the investments we’ve made across our businesses.

The combination of technology and advisory, alongside ETFs, active and private markets capabilities, enables us to deliver a better client experience – leading to clients consolidating more of their portfolios with BlackRock or engaging us for outsourcing solutions. We believe this in turn will drive continued differentiated organic growth into the future.

As we do each year, our management team and Board spent time assessing our strategy for growth. We challenge ourselves to think: What opportunities will this economic environment create for BlackRock and our clients, what more can we do to meet and anticipate their needs? How can we evolve our organization, operating structure, investment capabilities, and service models and, in doing so, keep leading the industry?

We have strong conviction in our strategy and our ability to execute with scale and expense discipline. Our strategy remains centered on growing Aladdin, ETFs, and private markets, keeping alpha at the heart of BlackRock, leading in sustainable investing, and advising clients on their whole portfolio.

We have continually made internal investments for organic growth and efficiency, investing ahead of client opportunities in private markets, ETFs, technology, and whole portfolio solutions.

In private markets, we are prepared to capitalize on structural growth trends. Whether it’s executing on demand for much-needed infrastructure, or the growing role of private credit as banks and public lenders move away from the middle market, private capital will be essential. BlackRock is poised to capture share through our scale, proprietary origination, and track record. And we believe our planned acquisition of GIP will meaningfully accelerate our ability to offer our private markets capabilities to our clients.

In ETFs, we will continue to lead by expanding investment access globally and through innovation. The ETF is an adaptable piece of financial technology, and over time we’ve been able to do more with it than just making investing more affordable. We’ve been able to bring better liquidity and price discovery to more opaque markets. One recent example is offering people exposure to Bitcoin through ETFs.

ETFs have been an incredible growth story in the U.S., with iShares leading the way. We believe global ETF adoption is set to accelerate as catalyst trends that we saw in the U.S. years ago like the growth of fee-based advisory and model portfolios are just beginning to take root. Nearly half of 2023 iShares net inflows were from our ETFs listed internationally in local markets, led by European iShares net inflows of $70 billion.

Active asset allocation, security selection and risk management have consistently been key elements in long-term returns. Our active teams across multi-asset, fixed income and equities are well-positioned to seize on broad opportunities arising out of this new interest rate and potentially more volatile regime. We are particularly excited about the opportunity in fixed income and how artificial intelligence is propelling performance in our systematic investing businesses.

Fixed income is going to be increasingly relevant in the construction of whole portfolios with higher yields and better return potential compared to the low-rate environment of the last 15 years. Now that the rate on 10-year U.S. Treasuries is near long-term averages, clients are reconsidering bond allocations.

BlackRock is well-positioned with a diversified, fixed income platform. It’s not going to be just about index, where we manage nearly $1.7 trillion. Or just about active where we manage over $1 trillion. Some of the most interesting portfolio conversations are with allocators who are blending ETFs with active or using innovations like our active ETFs for professionally managed income solutions.

Across asset classes, the need for integrated data, technology and risk management will continue to drive demand for Aladdin. Through its dynamic ecosystem of over 130,000 users, the Aladdin platform is constantly innovating and being improved. Investments in Aladdin AI copilots, enhancements in openness supporting ecosystem partnerships, and advancing whole portfolio solutions are going to further augment the value of Aladdin.

We are honored that our clients entrusted us with $289 billion of net new assets in 2023. And over the past few months, we’ve seen a decidedly more positive sentiment and tone in markets and among clients that I’m very optimistic will carry into the rest of 2024.

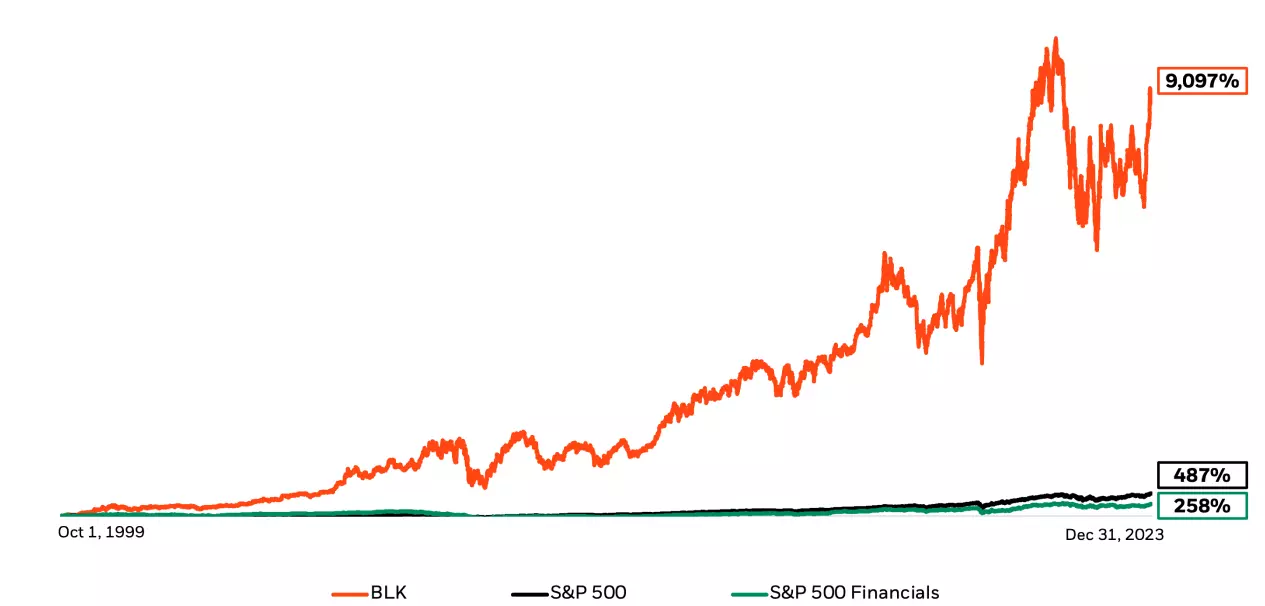

Our ability to adapt, evolve, and grow has generated a total return of 9,000% for our shareholders since our IPO in 1999. That is well in excess of the S&P 500 return of 490% and representative of a business model serving all our stakeholders.

Total return since BlackRock’s IPO through December 31, 2023

S&P Global. The performance graph is not necessarily indicative of future investment performance.

S&P Global. The performance graph is not necessarily indicative of future investment performance.

Our Board of Directors

BlackRock’s Board plays an integral role in our strategy, our growth and our success.

The diverse experiences and backgrounds of our Directors enable us to have rich discussions and debates. At each meeting, our Directors review components of our long-term strategy and foster constructive dialogue with our leadership team on strategic opportunities, priorities and risks facing BlackRock’s business. This dialogue ultimately pushes us to make the sometimes tactical and sometimes transformational moves to build a better BlackRock. This includes the two transformational moves we made in January: The strategic re-architecture of our organization and our agreement to acquire GIP.

These two transformational changes are the largest since our acquisition of Barclays Global Investors nearly 15 years ago.

Following the closing of the GIP transaction, we plan to have Bayo Ogunlesi join our Board of Directors. We will continue to evolve our Board over time to reflect the breadth of our global business and to guide us as we evolve ahead of our clients’ needs.

A final note

Over the past 36 years, BlackRock has grown from a company of eight people in a tiny Manhattan office into the largest asset manager in the world. But our growth is just a small part of a much larger success story.

It’s part of the same story that includes my parents retiring comfortably after 50 years of hard work. The same story where America was able to endure the 1980s S&L crisis and 2008 financial crisis – and rebound quickly and with growing strength.

And it’s the story that, hopefully, will include more people around the world. Nations that can outgrow their debt. Cities that can afford to power more homes and build more roads. Workers who can live out their golden years with dignity.

All of these stories are only possible because of the power of the capital markets and the people who are hopeful enough to invest in them.

Endnotes

1Based on a $1,000 investment from January 1960 to December 1990. Assumes reinvestment of all dividends. Past performance is not indicative of future results.(go back)

2Federal Reserve History, Savings and Loan Crisis(go back)

3OCED Economic Surveys: United States (2016)(go back)

4Securities Industry and Financial Markets Association, Capital DMarkets Fact Book (2023), p.6(go back)

5World Federation of Exchanges, Market Statistics-February 2024, (2024)(go back)

6World Economic Forum, Ageing and Longevity, (2023)(go back)

7United Nations, World Population Ageing, (2017), p.8(go back)

8The Wall Street Journal, Japan’s Nikkei Tops 40000 for First Time, Driven by AI Optimism, (2024)(go back)

9Cabinet Secretariat of Japan, Doubling Asset-based Income Plan, (2022), p.2(go back)

10Note: 1. Format adapted from Adele M. Hayutin, New Landscapes of Population Change: A Demographic World Tour (Hoover Press, 2022). Data from United Nations Population Division, World Population Prospects. (latest refresh 2022), Medium Fertility Projection. 2. Peak year is defined as the year in which working age population reaches its maximum for a country. Sources: United Nations Population Statistics (as of 2022). OECD (as of 06/2023). World Bank (as of 2022).(go back)

11United Nations, UN DESA releases new report on ageing, (2019)(go back)

12The New York Times Magazine, Can We Live to 200? (2021)(go back)

13National Library of Medicine, Estimated Life-Years Gained Free of New or Recurrent Major Cardiovascular Events With the Addition of Semaglutide to Standard of Care in People With Type 2 Diabetes and High Cardiovascular Risk, (2022)(go back)

14Source 1: Bureau of Labor Statistics, Employee Benefits in the United States, (2023), p.1; Source 2: Bureau of Labor Statistics, Employee Benefits in Industry, (1980), p. 6(go back)

15BLK Estimates based on AUM as of December 31st, 2021 and Cerulli data as of 2020. ETF assets include only qualified assets based on Cerulli data, and assumes 9.5% of institutionally held ETFs are related to pensions or retirement. Institutional estimates includes assets defined as “related to retirement” and are based on products and clients with a specific retirement mandate (e.g., LifePath, pensions). Estimates for LatAm based on assets managed for LatAm Pension Fund clients, excluding cash.(go back)

16BlackRock as of Dec. 31, 2021. The overall number of Americans is calculated based on estimates of participants in BlackRock’s Defined Contribution and Defined Benefit plan clients. The Defined Contribution number is estimated based on data from FERS as well as ISS Market Intelligence BrightScope for active participants across 401(k) and 403(b). Defined Contribution includes plans with over $100M+ in assets where participants have access to one or more BlackRock funds; some may not be invested with BlackRock. The Defined Benefit number is estimated based on data from public filings and Pension & Investments for the total number of participants across the 20 largest U.S. Defined Benefit plans that are not also Defined Contribution clients of BlackRock.(go back)

17U.S. Bureau of Labor Statistics, Labor Force Statistics from the Current Population Survey, (Feb. 2023)(go back)

18Represents the total number of active public schoolteachers enrolled in defined benefit plans with assets managed by BlackRock. Excludes Virginia, Alaska and Pennsylvania pension clients, as the states’ DB plan is not the default plan for its participants. Public school teachers count from the National Center for Education Statistics, projection for 2022 school year. Pensions participation rate based on data from the U.S. Bureau of Labor Statistics: 89% as of March 2022.(go back)

19Social Security, Life Tables for the United States Social Security Area 1900-2100, Figure 3a(go back)

20Social Security, When to Start Receiving Retirement Benefits, (2023), p.2(go back)

21Social Security, Summary: Actuarial Status of the Social Security Trust Funds, (2023)(go back)

22Dutch Government, Why is the state pension age increasing? (translated from Dutch)(go back)

23U.S. Bureau of Labor Statistics, Civilian labor force participation rate, (2000-2024)(go back)

24U.S. Census Bureau, Survey of Income and Program Participation (SIPP), (2022)(go back)

25Federal Reserve, Economic Well-Being of U.S. Households in 2022, (2023), p.2(go back)

26BlackRock, Emergency Saving Initiative: Impact and Learnings Report, (2019-2022), p.2(go back)

27BlackRock, Emergency Savings Initiative: Impact and Learnings Report, (2019-2022), p.12(go back)

28BlackRock, What are target date funds?(go back)

29AARP, New AARP Research: Nearly Half of Americans Do Not Have Access to Retirement Plans at Work, (2022)(go back)

30CIA: The World Factbook, Country Comparisons: Population (2023 est.)(go back)

31OECD, Pensions at a Glance 2023, (2023), 222(go back)

32Georgetown University Center for Retirement Initiatives, State-Facilitated Retirement Savings Programs: A Snapshot of Program Design Features, (2023)(go back)

33Parliament of Australia, Superannuation and retirement incomes(go back)

34Human Interest, The power of 401(k) automatic enrollment, (2024)(go back)

35BlackRock, To spend or not to spend? (2023), p. 2-5(go back)

36Source 1: The Wall Street Journal, The Champions of the 401(k) Lament the Revolution They Started, (2017); Source 2: Social Security Office of Retirement and Disability Policy, The Disappearing Defined Benefit Pension and Its Potential Impact on the Retirement Incomes of Baby Boomers, (2009)(go back)

37U.S. Chamber of Commerce, Statement of the U.S. Chamber of Commerce, (2012), p. 3(go back)

38Harvard Business Review, Too Many Employees Cash Out Their 401(k)s When Leaving a Job, (2023)(go back)

39The Wall Street Journal, Why China’s Middle Class Is Losing Its Confidence, (2024)(go back)

40The Wall Street Journal, Covid-Era Savings are Crucial to China’s Economic Recovery, (2023).(go back)

41The Wall Street Journal, The Rough Years That Turned Gen Z Into America’s Most Disillusioned Voters, (2024)(go back)

42Financial Times, How Abebayo Ogunlesi’s contrarian bet led to $12.5bn BlackRock tie-up, (2024)(go back)

43American Society of Civil Engineers (ASCE), 2021 Report Card For America’s Infrastructure, (2021), p. 5(go back)

44International Monetary Fund, Global Debt Is Returning to its Rising Trend, (2023)(go back)

45Fiscal Data: U.S. Treasury, Debt to the Penny, (Debt was $23.4T in March 2020 and $34.5T in March 2024)(go back)

46The Wall Street Journal, A $1 Trillion Conundrum: The U.S. Government’s Mounting Debt Bill, (2024)(go back)

47US Department of Treasury, Table 5: Major Foreign Holders of Treasury Securities(go back)

48As of March 2024. Net Zero Tracker, https://zerotracker.net (last visited March 18th, 2024)(go back)

49Associated Press News, The year in clean energy: Wind, solar and batteries grow despite economic challenges, (2023)(go back)

50BlackRock iResearch Services global survey, sample size n=200, May-June 2023. Survey covered institutional investors’ attitudes, approaches, barriers, and opportunities regarding transition investing. 83% of EMEA respondents surveyed have net zero by 2050 or other date as a transition objective across their portfolio. https://www.blackrock.com/corporate/literature/brochure/global-transition-investing-survey.pdf(go back)

51BlackRock’s 2020 Letter to Clients, Sustainability as BlackRock’s New Standard for Investing, (2020)(go back)

52Reuters, Europe’s spend on energy crisis nears 800 billion euros, (2023)(go back)

53The New York Times, Germany Announces New L.N.G. Facility, Calling It a Green Move from Russian Energy, (2022)(go back)

54Texas Fall 2023 Economic Forecast(go back)

55Federal Reserve Bank of Dallas, Texas electrical grid remains vulnerable to extreme weather events, (2023)(go back)

56U.S. Energy Information Administration: Electricity Data Browser(go back)

57U.S. Energy Information Administration, Solar and wind to lead growth of U.S. power generation for the next two years, (2024)(go back)

58BlackRock Alternatives, CFP, 2023(go back)

59Kenya Power, Annual Report & Financial Statements, (2022)(go back)

60Reuters, BlackRock, Temasek-led group invest $150 mln in thermal battery maker Antora, (2024)(go back)

61Business Wire, Antora Energy Raises $150 Million to Slash Industrial Emissions and Spur U.S. Manufacturing, (2024)(go back)

62Oxy, Occidental and BlackRock Form Joint Venture to Develop STRATOS, the World’s Largest Direct Air Capture Plant, (2023)(go back)

63As of June 30, 2022. “Energy companies” refers to corporations classified as belonging to the GICS-1 Energy Sector.(go back)